Lakes4life/E+ via Getty Images

Overview

I recently covered Oxford Lane Capital (OXLC) and within that article I briefly gave an overview to compare Eagle Point Credit (NYSE:ECC) since both of the funds operate as Closed End Funds with a focus on CLOs. From the comments on my OXLC article, it seemed like the general consensus was that ECC was the preferred CLO Closed End Fund between the two. The last time I fully covered Eagle Point Credit was in August of 2023 so I thought it would be a good time to give a full analysis on the updated portfolio and performance since then.

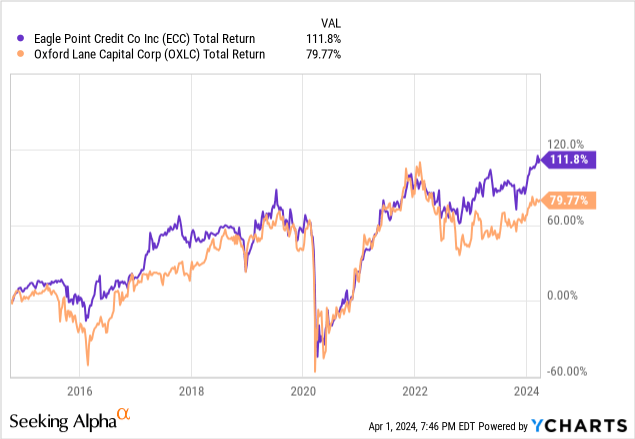

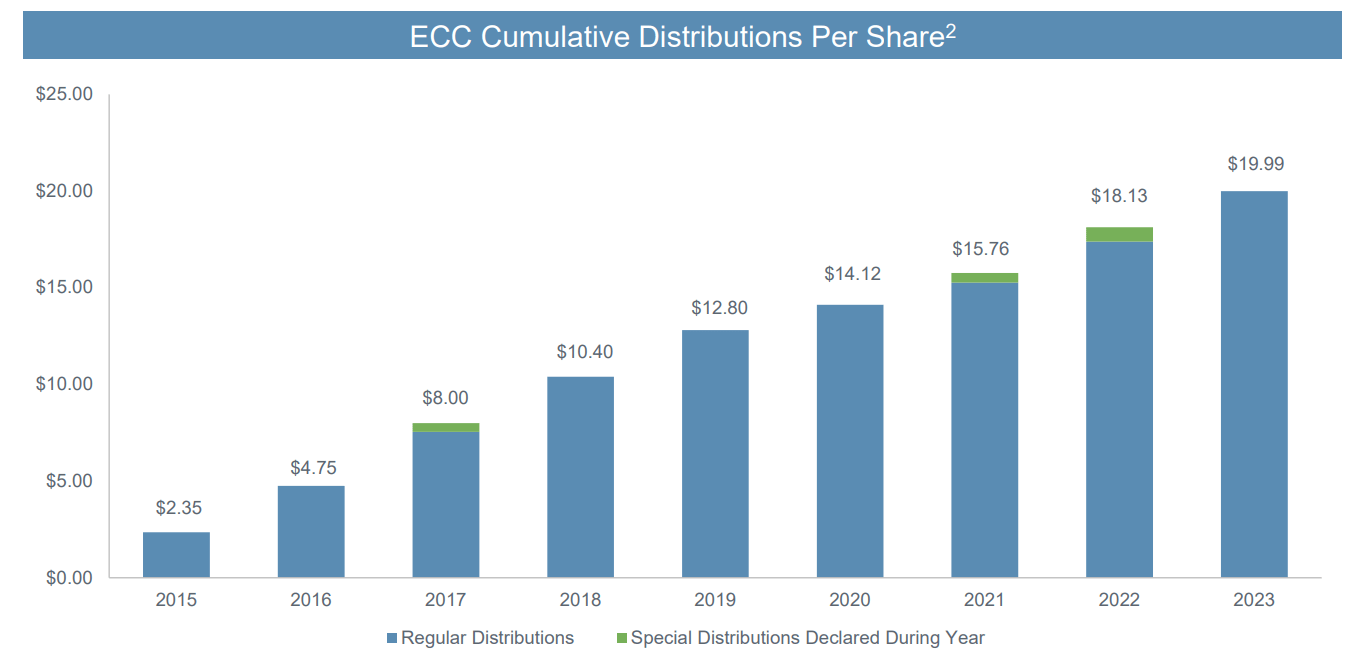

We can see how ECC has provided a superior total return compared to OXLC over the last near ten year period. ECC currently has a yield of 16.6% and the dividend is distributed out on a monthly basis. ECC has really been able to benefit from the rise of interest rates over the last 2 year period. As a result, shareholders have collected an abundance of supplemental dividends alongside the base distribution. The price has floated between $9 – $11 per share for some time now. Entry below $10 per share would be more ideal but ECC still remains a Buy.

You aren’t likely to see any price growth here as the fund’s main goal is to produce income. Eagle Point Credit invests in equity tranches of CLOs (collateralized loan obligations) which are the riskiest area of the corporate capital structure. This additional risk contributes to ECC’s ability to generate a higher yield for shareholders.

Structure & Portfolio

Collateralized loan obligations are often made up of corporate loans that are pooled together and then given different ratings of risk within. What makes these loans different are that they are often sourced from “high risk” corporate debt. In this context, high risk or “junk”, simply means “below investment grade”. The way that ECC brings in profit is by collecting interest on these loans issued. The higher yield is a result of the below investment grade companies. As the saying goes, the higher the yield, the higher the risk.

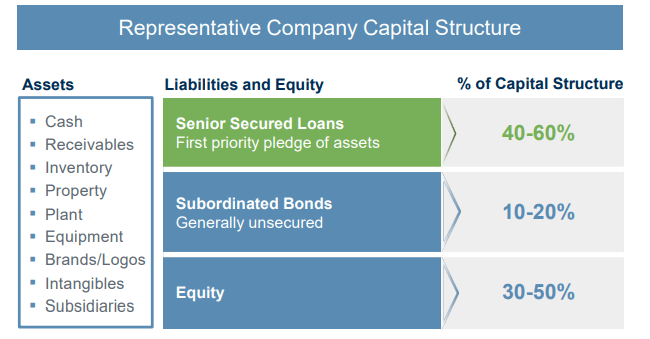

ECC Q4 Presentation

We can see how the capital structure is laid out here for ECC. At any given time, the portfolio may have exposure to the equity tranche totaling anywhere between 30-50% of the portfolio. Likewise, they may also have anywhere between 40-60% of the capital structure within senior secured loans. The obligors of the underlying loans consists of well know companies like Burger King, Hilton Hotels & Resorts, Petco, Albertsons (ACI), and Dell (DELL) for example.

The portfolio is very diverse in industry with the top industries being informational tech & software at 14.6%, Media at 6.5%, and Healthcare & Biotech at 5.6%. Geographically the USA makes up the largest exposure at over 92%. The portfolio does have very small amount of exposure globally, in places like Canada, the UK, Netherlands, France, and Iceland.

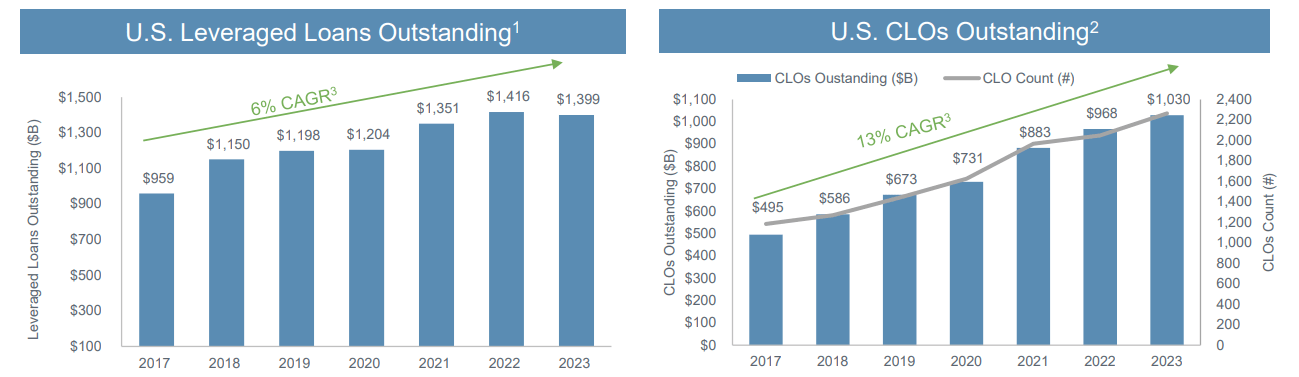

ECC has nearly 1,800 underlying loan obligors and 143 CLO equity securities within their portfolio. This portfolio growth can be attributed to the growing demand for capital. In fact, the CLO market is the largest source of capital for US-based senior secured loans. We can see how leveraged loans and CLOs outstanding have grown at a 6% and 13% CAGR (compound annual growth rate) respectively.

ECC Q4 Presentation

Risk Profile

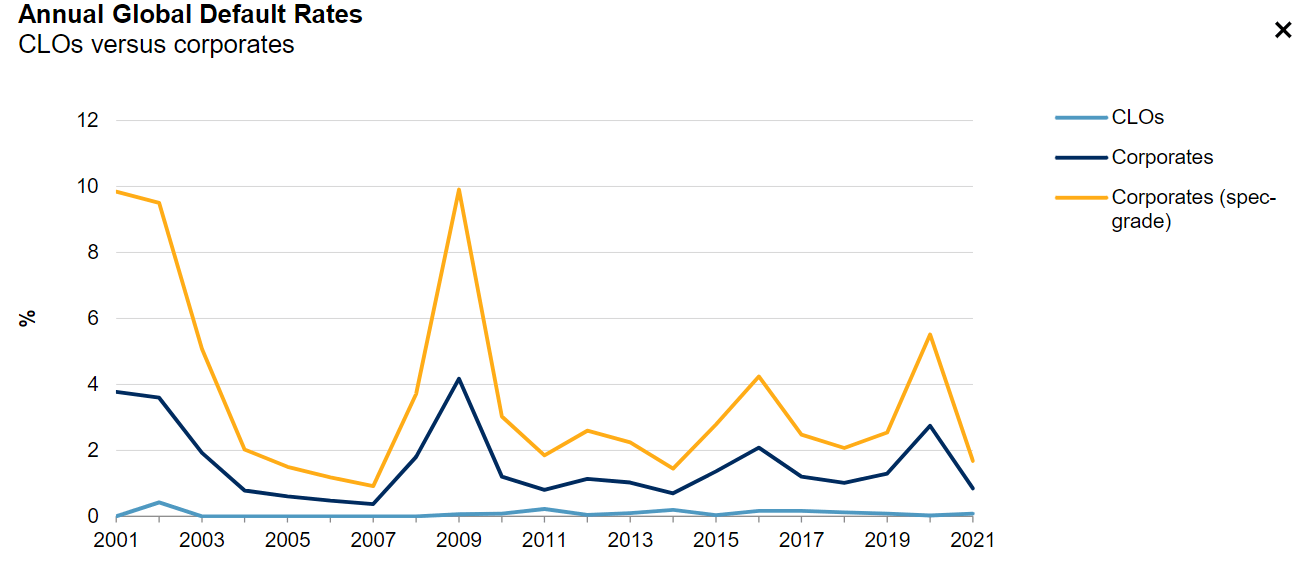

We’ve already established that the majority of the loan portfolio is comprised of debt that belongs to below investment grade companies. How risky is this really though? For reference, anything rated below BBB- is labeled as junk. Naturally, most people stay away from these kind of funds because of this. However, historical data tells us that this kind of CLO structure has a low default rate globally. We can see spikes in defaults around the GFC of 2009 as well as the Covid crash in 2020 but generally speaking, the default rates have been quite low for something labeled junk.

S&P Global

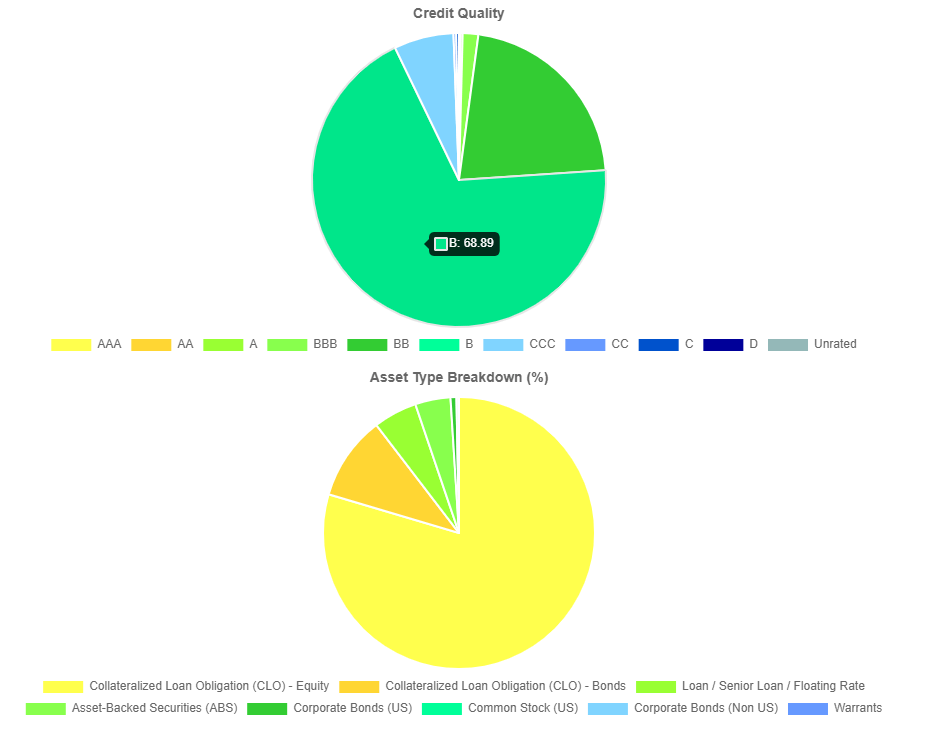

The largest slice of the credit rating goes to B rated holdings, making up approximately 69% of the whole portfolio. This is then followed by BB rated at 22% and CCC-rated at 6.5%. Only 2.12% of the portfolio’s credit quality is rated as investment grade at BBB and above while the total portion rated as non-investment grade equals 97.8%. I use tools like CEF Data to assess the risk of an asset because they have useful pie chart breakdowns that you can reference.

CEF Data

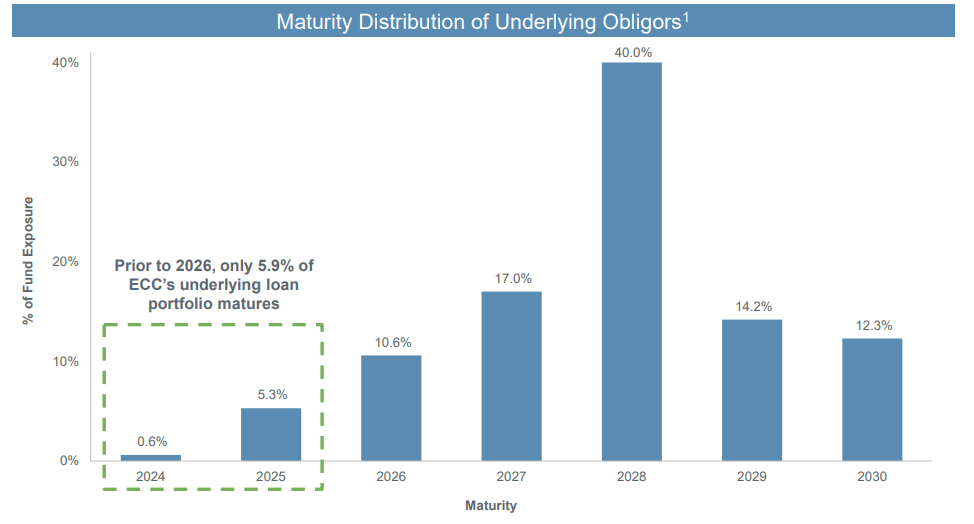

CLO equity has historically generated returns while maintaining a low loss rate. Between 2002 and 2011, only 4% of CLOs have delivered negative equity returns. In addition, ECC management has done a great job structuring out the underlying maturity schedule. For the next two years prior to 2026, only 5.9% of their underlying loan portfolio matures. This leaves a lot of run way for cash generation in this higher interest rate environment we are in.

ECC Q4 Presentation

It seems like the Fed is staying patient with assessing when they will start cutting interest rates. My personal guess is that we will see very light cuts of -50 basis points or less this year. Jerome Powell has already stated that rate cuts are not likely to happen soon. Even if rates are cut slightly, the days of near-zero interest rates are gone and this is a huge benefit to ECC. A higher average rate translates to a higher NII from the loans within their portfolio.

Even though I look at this data and feel comfortable investing funds into this type of vehicle, most investors should consider if this is something they are comfortable with. With data aside, the price has still come down drastically since inception. Even if distributions are sustained, the price may decrease further if market conditions worsen and this is something to consider.

Financials & Dividend

So the question stands: if the portfolio here is comprised of loans that are classified as junk, how profitable can ECC actually be? Well, it may surprise you but the answer is very profitable! ECC reported their Q4 earnings report in February and this closed off their fiscal year. NII (net investment income) and realized capital gains for the quarter came in at $0.33 per share which was a sizeable improvement over 2022 Q4’s NII of $0.29 per share.

ECC Q4 Presentation

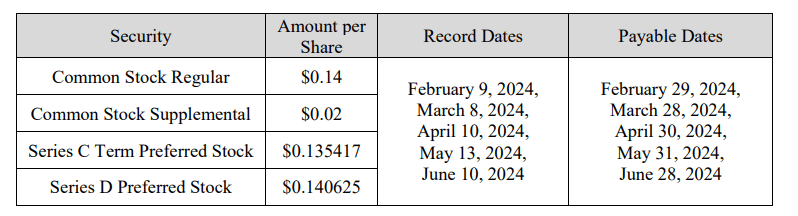

In addition, they received $0.82 per share in cash distributions from their investment portfolio. This works out to $60.7M in recurring cash distributions. This comfortably covers the monthly distribution of $0.14 per share, which has been declared through June 2024. Cash flow has been so strong that in addition to this base dividend, management has also declared a supplemental dividend of $0.02 per share through June 2024 as well.

Management has been actively growing the portfolio of investments also. Over the last quarter they deployed $34M into additional investments including CLO equity, debt, and loan accumulations. These new investments will continue to contribute towards the growth of the overall portfolio as the average yield on these new investments was nearly 23%.

ECC Q4 Update

The current dividend yield is 16.6% and distributions are issued on a monthly basis. Cash flow has been so strong that they’ve already declared a supplemental dividend of $0.02 per share through June of 2024. This supplement is in addition to the base distribution of $0.14 per share. For such a high yielding asset, the dividend growth has been impressive. All of the additional supplementals can likely be attributed to the rising interest rates. However, the distribution growth was strong even before rates went up.

ECC Q4 Presentation

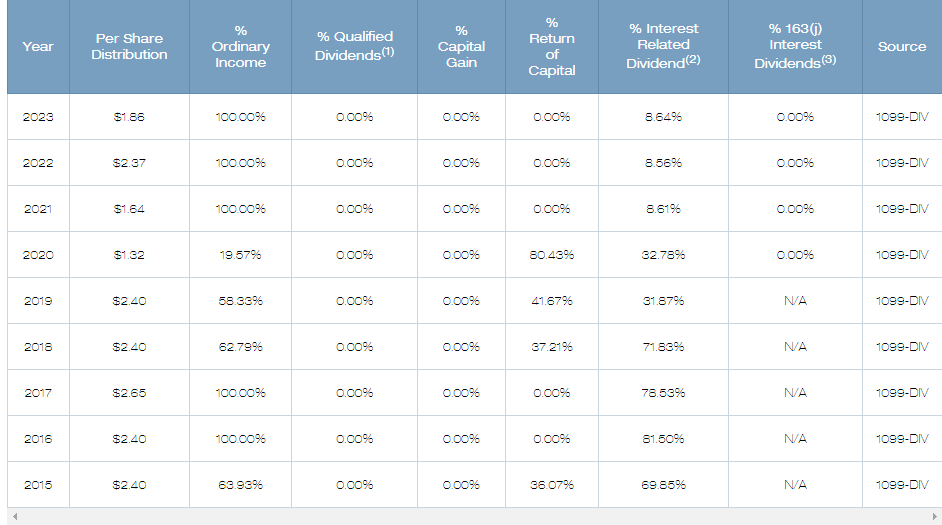

Unfortunately, the high income received from ECC has been classified as 100% ordinary income over the last three years. This means you will owe taxes on the distributions unless you hold this in a tax advantaged account. There were some years that the distribution also included a portion of ROC (return of capital) which can be more tax friendly but also harmful to NAV. I love how transparent their site and reporting metrics are because they have a full breakdown of how the distributions were classified.

ECC Tax Information

Lastly, I’d like to end with mentioning a DRIP (dividend reinvestment plan) they have included where you can get your dividends reinvested at a discount. The latest annual letter confirms the following:

We also want to highlight the Company’s dividend reinvestment plan for common stockholders. This plan allows common stockholders to have their distributions automatically reinvested into new shares of common stock. If the prevailing market price of our common stock exceeds our NAV per share, such reinvestment is at a discount (up to five percent) to the prevailing market price.

Valuation

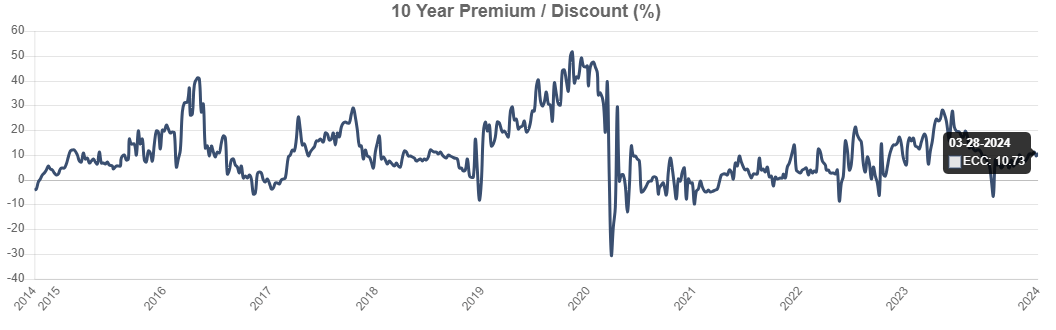

ECC has historical traded at a consistent premium to NAV. This may be because of the transparent management, excellent distribution history, or the consistent NII results. Right before the Covid crash, the premium spiked as high as 50%. Shortly after, the price dropped and resulted in trading at a severe discount at -30% for a brief moment.

CEF Data

Since then, the price premium has stabilized. Over the last 3 year period, the average premium has been 8.5%. ECC currently trades at an approximate 10% premium to NAV (net asset value). While this is expensive in relation to the average, it’s worth noting that a year ago in April of 2023, the premium was upward of 20%.

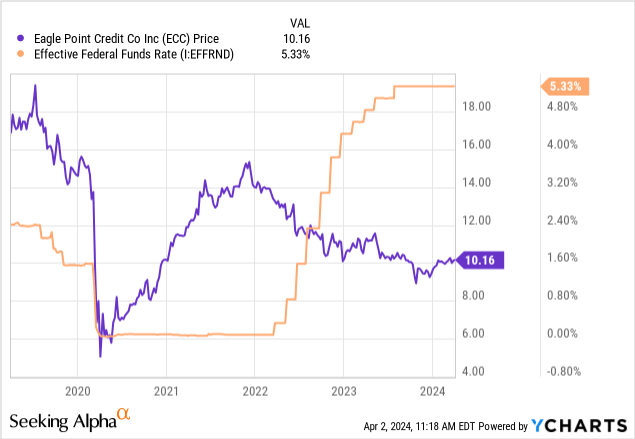

Despite the premium, I believe this to be an ideal entry point to start a position. This also serves as a great point to reinvest those dividends with the discount ‘DRIP’ benefit while the price currently trades above the NAV. In addition, we can see the inverse relationship that the effective federal funds rate had on the price action of ECC. When rates were cut to near-zero levels, the price moved up substantially. When rates started rising, the price came down, even though the NII rose. It wouldn’t be farfetched to see the price edging back upwards once the rates start to come back down in the near future.

However, I am aware that price movement comes secondary for funds like ECC. Most investors pile into high yielding assets such as this for the income that it can provide. While I believe the income will certainly persist in the future as we now approach an environment with a higher average rate, I also think that now is a great time to initiate a position.

Takeaway

Eagle Point Credit offers a way to capture a high yielding asset that pays out its distribution on a monthly basis. This is a great option for investors that value income. The total return has been over 110% through the last 5 year period but this mostly comes from the distribution. The distribution received here is mostly classified as ordinary income so this fund would be best utilized in a tax advantaged account.

The portfolio of ECC is diverse in industry but is mostly comprised of the riskiest equity part of the capital structure. However, the fund trades at a current premium to NAV of about 10%. In comparison, the average premium over the last 3 year period is only 8.5%. Despite the premium, I still believe ECC to be a buy with the impending rate cuts on the horizon. ECC has established a strong history of growing distributions despite what market cycle we are in.

Q2 2024 Earnings Call Transcript")