photoman

Introduction

ProShares Short VIX Short-Term Futures ETF (BATS:SVXY) is an interesting ETF that makes daily short trades on VIX futures. Technically the fund is labeled as a “leveraged” ETF but it’s actually the opposite of leveraged because it offers only 0.5x exposure to shorting of VIX futures so the fund is only using half of its buying power to make trades and only exposed to half of the movement in VIX in the inverse.

ProShares Short VIX Short-Term Futures ETF seeks daily investment results, before fees and expenses, that correspond to one-half the inverse (-0.5x) of the daily performance of the S&P 500 VIX Short-Term Futures Index.

Still, even at the negative leverage, the fund still runs the risk of a total wipeout of VIX were to suddenly climb 400% overnight so even though it’s a very small risk, it’s still there. One could probably reduce their risk by using a hedge such as buying out of money VIX calls (strike price of 60 should do it). By design, leveraged funds are not meant to be held forever and they are meant for short term trading but then again this fund isn’t exactly leveraged and as long as you keep your position small (less than 5% of your portfolio) you would be fine in most situations.

Past Performance

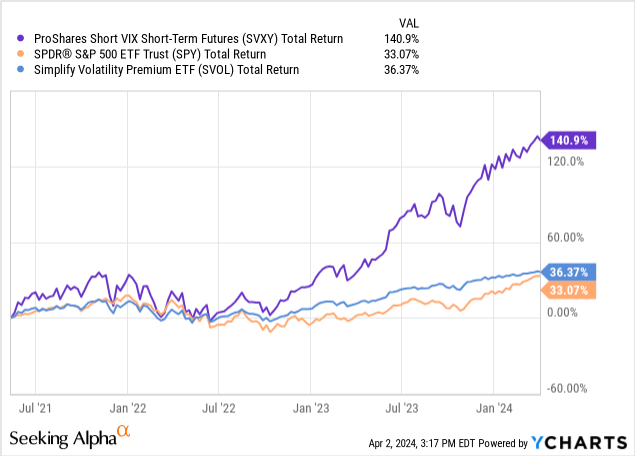

This fund is different from highly popular Simplify Volatility Premium ETF (SVOL) which I’ve covered several times in past articles. Those who follow me know that I’ve been bullish on SVOL and it’s been performing very well so far, beating S&P 500 (SPY) in total returns since inception. Here is the thing though, SVXY seems to be doing even better than SVOL and beating the overall market by an even larger margin in the last 5 years or so.

How is it different from SVOL?

But how? How is SVXY different from SVOL and how is it outperforming by so much? There are a few big differences. First, SVOL uses only about 0.25x buying power when shorting VIX futures whereas SVXY uses 0.50x buying power so it uses twice as much buying power which will help it outperform when VIX is declining or flat but also underperform when VIX is raging. If you are super bearish on VIX, you might want to buy SVXY whereas if you are neutral or just slightly bearish on VIX, you might want to stick with SVOL.

The second difference is that SVOL uses a variety of hedges such as buying VIX call options that are deeply out of money whereas SVXY does no such thing. As I mentioned above, if you have SVXY and you are concerned about risk, you can always do what SVOL does and protect yourself by buying out of money call options in VIX. Just make sure that your broker allows you to trade VIX options because not all brokers do (for example highly popular Robinhood doesn’t). The fact that this fund doesn’t use any hedges probably helps explain its outperformance too because SVOL uses some of its gains to buy hedges whereas this fund keeps all of its gains since it doesn’t use any hedges. While this will work for the fund while things are going well, it can hurt the fund tremendously when things aren’t going well.

How does it behave in extreme cases?

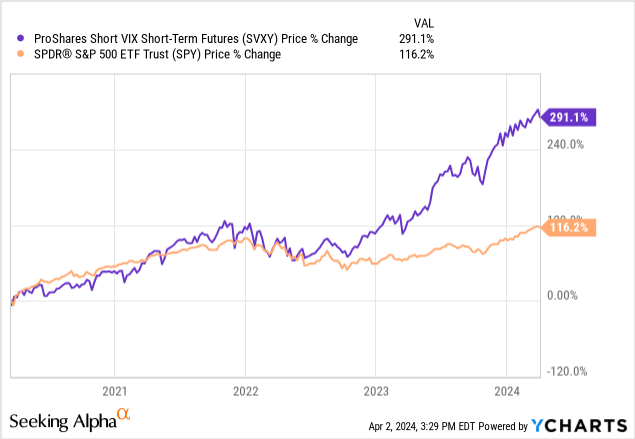

Since SVXY has been around for longer than SVOL, we have data showing how it behaved in extreme cases. For example, let’s go to March 2020 when the market dropped -35% due to lockdowns driven by the pandemic and VIX suddenly jumped about 300% in a few short weeks. Notice that SVXY saw its value drop by almost half during this chaotic period but to its credit, it still didn’t blow up which is a major concern with volatility related products, especially those that are considered leveraged.

What did it do since then? Apparently it did very well, almost tripling in price and outperforming the market handily. This doesn’t mean that the fund will continue on performing like this forever but it should perform decently in most environments.

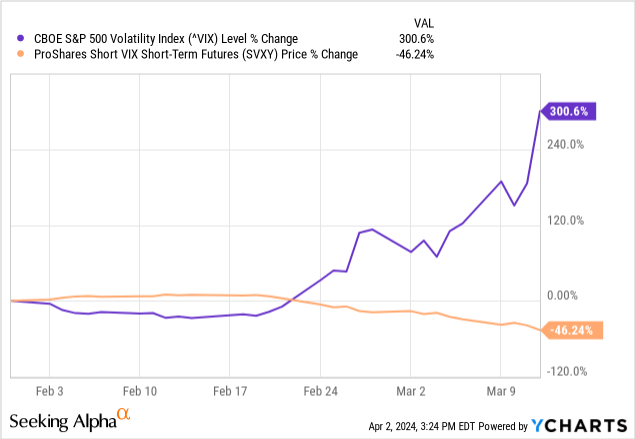

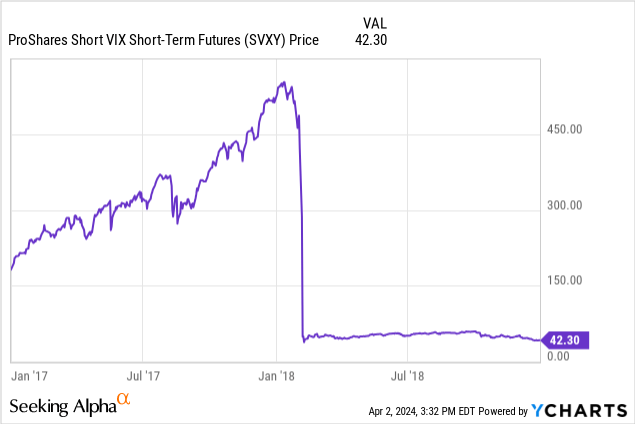

There is one period when this fund performed pretty badly though and that’s during the famous “Volmageddon” of 2018 when volatility suddenly had a massive spike overnight when S&P 500 dumped -4% in one day spooking investors, which wiped out several funds that were busy shorting VIX. Back then this fund was structured differently though and it was shorting VIX using all of its buying power so it was -1.0x short VIX whereas now it’s only -0.5x short vix so the fund is now different than how it was back then. If it continued as a -1.0x short VIX it would have probably been wiped out completely during the March 2020 crash instead of being cut by half.

No Distributions Though

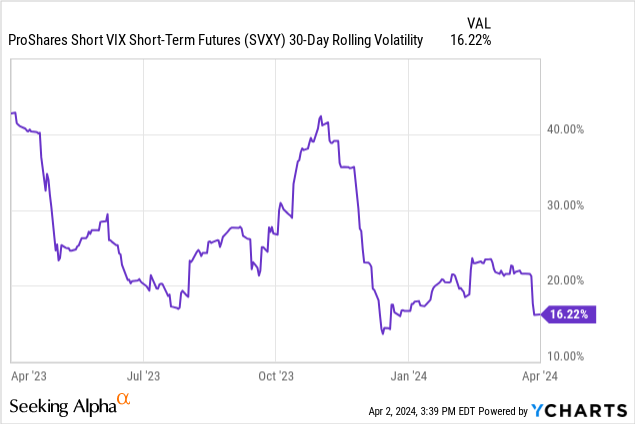

Unlike SVOL which pays monthly dividend distributions that have an annualized yield of 16%, SVXY doesn’t have any distributions. Thus, one could say that SVOL is created for generating income whereas SVXY is more about obtaining price gains. Then again, one could create their own income from SVXY either by selling a portion of their shares for capital gains or writing covered calls against it (which could also add some hedging at least but it would be super limited). Currently SVXY has a 30-day rolling volatility of 16% which can generate you about 8-12% from selling covered calls if you chose to go that route. Another way of hedging SVXY might be buying out of money SVXY puts since the fund has its own options chain. To be frank though, the best and simplest hedge is to keep your position size small so that you won’t lose sleep over it if one of your positions go against you.

Verdict

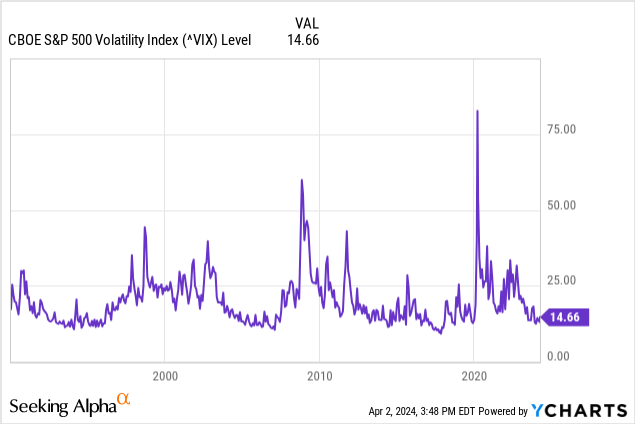

Even if you don’t want to consider buying this fund right now, you should still add it to your watchlist at the very least because you might be tempted to buy it the next time we see a large spike in volatility. You never know when that will happen (that’s why those VIX spikes happen so suddenly and take everyone by surprise) but if you are prepared when it happens, you might be able to take advantage of it. VIX will have spikes here and there every couple years but those spikes never stay elevated for long. Sooner or later VIX always returns to its normal range of 10 to 20, often times as quickly as it rose. Whenever VIX roses above 20-25, you might want to buy this fund and ride it up as VIX returns back to its range in the next few weeks.

I am personally holding a small position of this even though it’s not the “recommended” usage of this fund. My position is small enough that it won’t cause me much headache and I have enough cash on the sidelines to buy the dip if such opportunity arose.

Q2 2024 Earnings Call Transcript")