Phiromya Intawongpan

Shares of expense management platform Expensify, Inc. (NASDAQ:EXFY) have rebounded more somewhat since the company reported a better-than-expected Q4 2023 bottom line on February 22, 2024. Cost cutting measures were responsible for the beat, but top line growth remains challenging as existing customer seats contracted by 42,000 in FY23 after expanding 85,000 in FY22. With a rolling launch of its new platform throughout 2024 and a questionable marketing approach, the beneficial owner buying into this busted IPO merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview:

Expensify, Inc. is a Portland, Oregon headquartered cloud-based expense management software platform primarily for small and medium-sized businesses, or SMBs. It boasted ~719,000 paid members across an average of 47,000 businesses in over 200 countries and territories in the final quarter of 2023. Expensify was formed in 2008 and went public in 2021, raising net proceeds of $57.5 million at $27 per share. The stock trades around $1.70 a share, translating to an approximate market cap of $145 million.

The company is capitalized by three classes of stock. The 70.6 million shares of publicly traded Class A stock confer economic interest and one vote per share. The 7.3 million shares of the privately held LT10 stock bestow economic interest and ten votes per share, while the 7.3 million shares of the privately held LT50 stock provide economic interest and 50 votes per share. Owing to this arrangement, the owners of the LT10 and LT50 shares represent 17% of the economic interest and 86% of the voting power in Expensify.

Technology & Business Model

The backbone of its raison d’etre is SmartScan, which permits users (individuals or employees) to take a photo of any receipt of nearly any quality, after which Expensify’s technology transcribes and categorizes the information, sends it along for approval, and provides next-day reimbursement. These services have since expanded into the management of corporate credit cards, invoice generation, bill pay, collections, and travel bookings all from its mobile app or website.

Individuals can sign up for a free subscription that includes Track, which permits use of its SmartScan receipt scanning functionality up to 25 times a month; and Submit, which allows expense report submission for reimbursement. Those free plans turn into paying customers when the 25 scans per month threshold is eclipsed. Expensify believes that the individuals using its software and/or app are its best marketing tool, as they will tell their managers to get a firm-wide subscription to its services.

Those business services include Collect and Control plans, where clients pay either a flat monthly fee for each active member or an annual plan, where they commit to a minimum number of monthly seats in exchange for a discount. Businesses can qualify for a free plan if they launch a corporate card program using the Expensify (Visa (V)) Card, which gives them the ability to reimburse cash expenses for employees, send invoices to clients, and set up bill payments. The paid Collect and Control plans allow clients to integrate with small business accounting, travel, and human resources systems, configure expense report approval workflows, pay employees and contractors via ACH or internationally through Global Reimbursements. Also, Expensify receives a percentage of the interchange for all spend on its card.

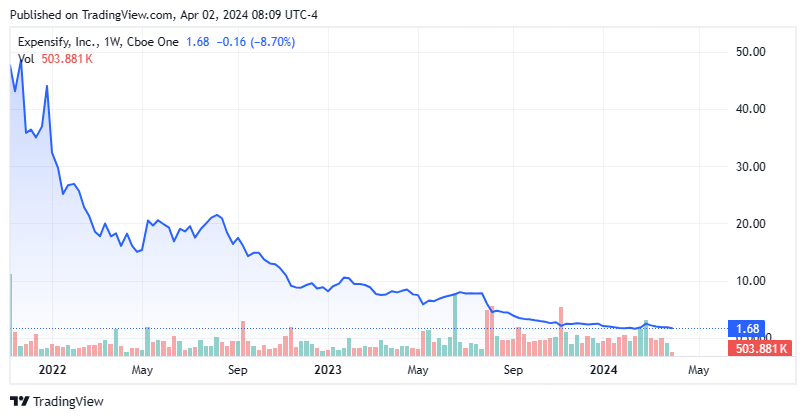

Share Price Performance

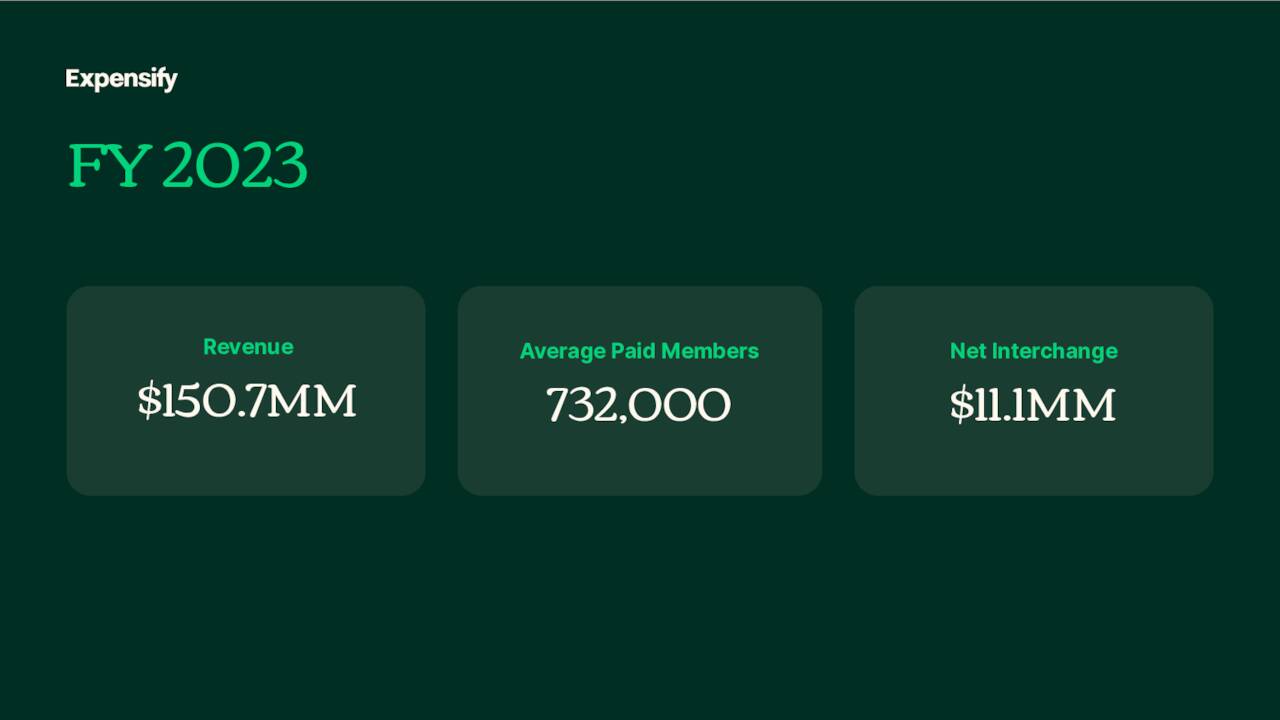

So, with an expense management, invoice, and bill pay platform complemented by its own credit card, the company has sought to grow its customer base through the addition of new platform features and word-of-mouth recommendations. With a playing field that includes over a dozen privately held competitors – including a rival named Expensya – vying for a share of the 33.2 million strong domestic small business market, there has been nothing that has distinguished Expensify, except for the fact that it is publicly traded. As such, its top line has floundered, dropping 11% to $150.7 million in FY23. This is in stark contrast to management’s 25% to 35% long-term growth objective laid out after its Q4 2021 financial report in March 2022. As such, the once very hot IPO – priced at $27, first-trade $39.75, and peak of $51.06 only 11 trading sessions into its publicly traded existence – cratered 94% from its IPO pricing and 97% from its peak when it retouched its all-time intraday low of $1.52 a share on February 22, 2024.

In an attempt to reinvigorate growth, management is launching a 2.0 version of its platform that it describes as a cross between PayPal’s (PYPL) Venmo, Meta Platforms’ (META) WhatsApp, and Dropbox (DBX). It will feature recently added free (for now) chat functionality. It will become active throughout 2024.

Q4 2023 Financials & FY24 Outlook

More details on that rolling launch were provided as part of Expensify’s Q4 2023 financials, which were reported after the close on February 22, 2024. The company posted earnings of $0.04 per share (non-GAAP) and Adj. EBITDA of $5.9 million on revenue of $35.2 million versus earnings of $0.09 per share (non-GAAP) and Adj. EBITDA of $11.2 million on revenue of $43.5 million in 4Q22, representing declines of 58%, 48%, and 19%, respectively. Although dour on a year-over-year basis, the bottom line was $0.09 better than consensus forecast, while the top line was essentially flat. It was the first time in four quarters that Expensify did not come in short of expectations at the net income line. Cost cutting measures contributed to the improvement versus expectations.

February 2024 Company Presentation

That brought the FY23 to a loss of $0.01 a share (non-GAAP) and Adj. EBITDA of $13.2 million on revenue of $150.7 million, as compared to a gain of $0.31 a share (non-GAAP) and Adj. EBITDA of $42.5 million on revenue of $169.5 million in FY22, for decreases of 102%, 69%, and 11%. The biggest factor in these declines was not new customer adds, which were essentially the same (43,000 seats in FY23 vs 42,000 in FY22), nor customer churn from leaving the platform or going out of business (-62,000 seats vs -62,000), but rather existing customer expansion which went from an addition of 85,000 seats in FY22 to a contraction of 42,000 in FY23. Expensify laid the blame for this dynamic on a lousy macroeconomic backdrop.

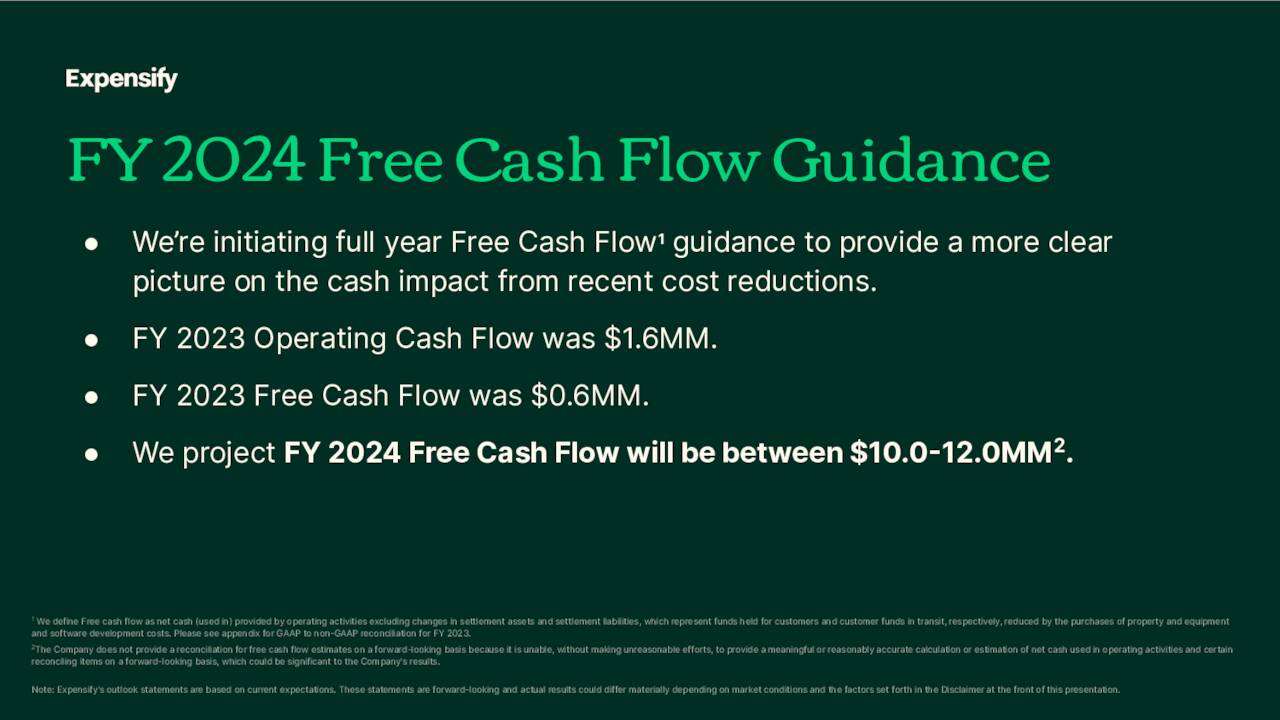

After free cash flow declined from $26.3 million in FY22 to $0.6 million in FY23, management indicated that it expected to generate $11.0 million in FY24, based on a range midpoint.

February 2024 Company Presentation

Since that relatively unexciting report, shares of EXFY first rallied nearly 50% off their February 22, 2024 close of $1.59. Over the past few weeks, the shares have given up most of those gains.

Balance Sheet & Analyst Commentary:

One point of encouragement was the fact that the company retired debt of $44.3 million in FY23, leaving its balance sheet in solid stead, reflecting cash and equivalents of $47.5 million and debt of $22.7 million. Expensify could put some of its projected FY24 free cash flow towards its $50 million stock repurchase program, under which it bought back 504,493 shares in FY23, leaving $41.0 million on its authorization. That said, even with its low share price, management has indicated that it is more focused on debt retirement than share repurchases as it enters 2024.

With its stock down 97% peak-to-trough, most of the Street has abandoned its sanguinity towards the company. Once unanimously positive in October 2022, analysts are decidedly negative, featuring two buy ratings against four holds, one underperform, and one sell, with a median price objective of $2 amongst those who have offered commentary in the past five months. On average, they expect Expensify to earn $0.16 a share (non-GAAP) on revenue of $143.3 million in FY24, followed by $0.19 a share (non-GAAP) on revenue of $152.4 million in FY25.

Beneficial owner Steven McLaughlin is decidedly more bullish than Street prognosticators, given his most recent purchase of 182,941 shares at $1.59 just before the earnings report on February 22, 2024. This transaction bolstered his ownership interest to 12%. It should be noted several company insiders including the CEO sold just over $1.4 million worth of shares collectively in March of this year.

Verdict:

Mr. McLaughlin’s cost averaging notwithstanding, Expensify has a commoditized offering, although management believes otherwise. The company should have spent more on brand recognition with the proceeds from its IPO, instead of relying on a bottom-up viral lead generation, word-of-mouth approach. That said, it does plan to spend more on search engine optimization in FY24, but that still does not seem like an optimal use of its marketing funds. In short, management doesn’t have any real game plan for growth.

That said, if the valuations are compelling, a blasé, somewhat rudderless story might be enough. However, based on FY24 Street projections, Expensify’s stock trades at a price-to-sales ratio of one times, and a P/E of just over 10. On These valuations seem fair but not particularly compelling given the company’s history of destroying shareholder value and little product differentiation. If the small business economy were to surge, shares of EXFY should enjoy a lift, but I don’t see that economic scenario on the horizon.

Now if the company was to deliver or exceed its free cash flow goals in 2024 and looked like it could continue to do so this time, Expensify, Inc. stock might be worth another look as that would give a free cash flow yield in the high single digits at current trading levels.

Q2 2024 Earnings Call Transcript")