Marje

Investment Thesis

UMH Properties, Inc. (NYSE:UMH) is a REIT that focuses on manufactured housing in the United States in the residential space. With 135 manufactured home communities, the REIT has a total of 25,800 homesites located in the eastern and central regions of the United States, namely the eastern or central regions of New Jersey, New York, Ohio, Pennsylvania, Tennessee, Indiana, Michigan, Maryland, Alabama, South Carolina and Georgia. I recommend a ‘buy’ on the REIT given its favorable exposure to the rebounding shale boom, steady rental increases, improving occupancy ratios, and a stable balance sheet and FFO generation that should support its growing dividend.

Shale Region Exposure

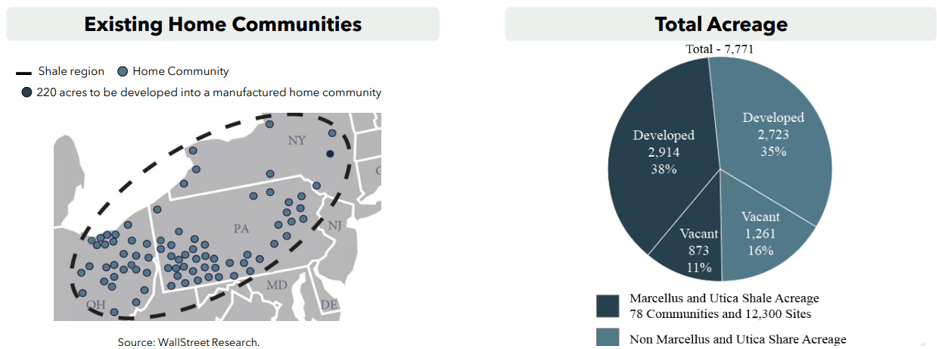

Many of UMH’s properties are located in and around the Marcellus & Utica Shale region. This is a large area of land that is located around Pennsylvania, Ohio, West Virginia and New York, housing large natural gas fields below and it is considered one of the largest natural shale gas sources in the U.S. Historically, prior to the Great Financial Crisis, the region had been overlooked because of limestone layers that made it expensive and extremely difficult to build wells for extraction of natural gas.

It wasn’t until horizontal drilling and hydraulic fracturing (i.e. fracking) practices became common and widespread that resource companies in the area began to take notice, noting the untapped potential of the shale region. With this still being a region with large natural gas field in operation today, UMH Properties benefits from this trend providing manufactured housing to many work there. With 3800 acres in this community, roughly half of the company’s rental income is derived from the region.

Marcellus & Utica Shale Region Exposure (Investor Presentation)

With natural gas down 32% year to date and 28% in 2023, shale drillers have already started to ramp up their U.S. natural gas rigs in preparation for a rebound in 2024. There is a growing sense of optimism for a rebound and I believe that UMH Properties is poised to benefit from this trend.

Steady Rental Increases

Oftentimes, since these workers are not intending to root their lives here long-term, they need affordable housing that meets their needs. Most of the new manufactured homes that UMH sells start at as low as $90,000 and the rents can start at $1000 per month. Even with pricing power, UMH generally avoids increasing beyond its standard 5-6% increase per year in order to manage good relationships with tenants.

When we look at the latest Q4 and full year 2023 results, we can see this in play. In Q4 on a same-property basis, rental income rose 11% and net operating income (NOI) jumped 19%. On a full year basis, the increases were 9% and 13% for rental income and NOI, respectively. Some of this was driven by rental revenue increases with the monthly rent per site going up by 4% on a year over year basis, but the remaining increase was driven by occupancy of 632 units. So with the combination of a rising occupancy ratio and the ability to increase rents a few hundred basis points over the inflation rate, the NOI increases can be pretty meaningful.

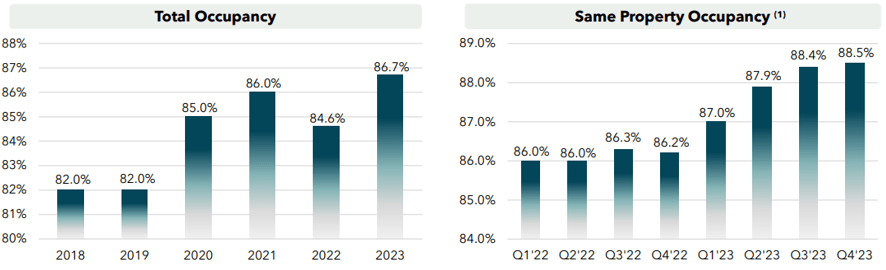

Improving Occupancy

One of the attributes I like about UMH Properties (and one I think can be a tailwind for NOI growth in the future) is its improving occupancy. On a total occupancy basis, the REIT had a ratio of 86.7% at year end, which was 470 basis points higher than in 2018. On a same property occupancy basis, the ratio improved sequentially for the last four quarters with steady improvements to 88.5% now.

Investor Presentation

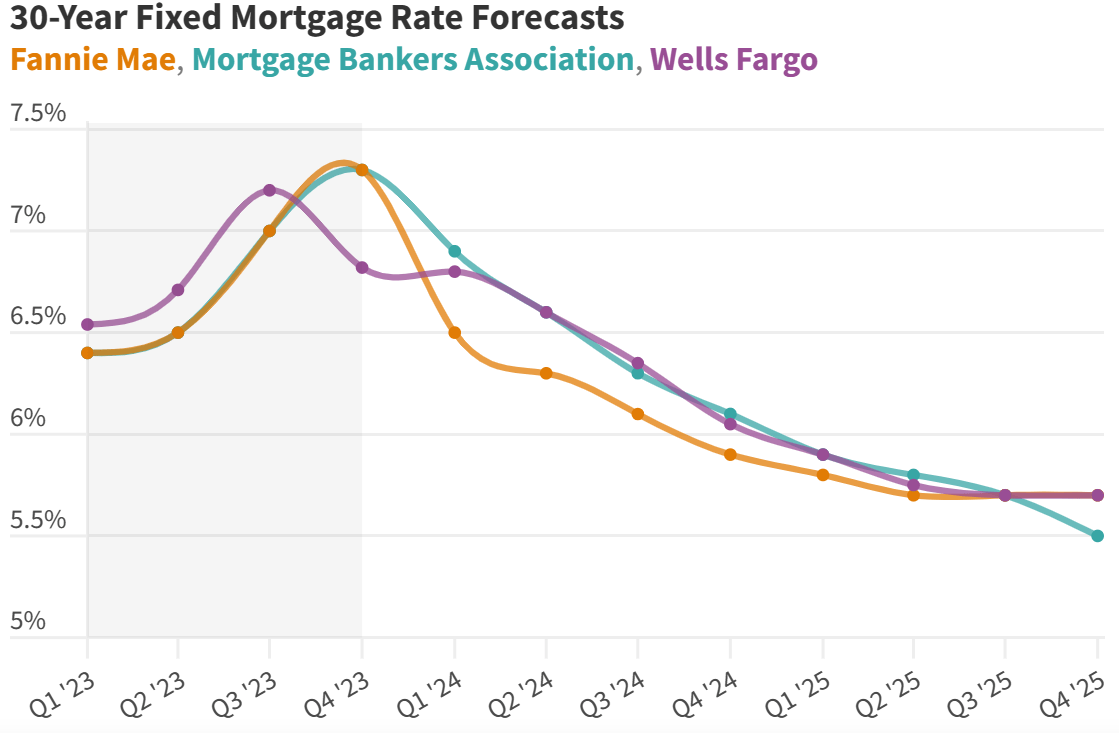

Compared to other peers like Sun Communities (SUI) which has a same property occupancy of 98.9%, there is still room for improvement and for the gap to close, but the trend as of late has been in the right direction. In my view, I think UMH Properties can get to the low-90s for its same property occupancy as the real estate market recovers. With 30-year mortgage rate is expected to fall to the low-6% territory by the end of the year and into the high-5% range by spring of 2025, this should restore some confidence in the market. In addition to a U.S. consumer sentiment rising to a 2.5-year high as inflation expectations subside, this should be a positive for UMH going forward.

U.S. News (Data sourced from Fannie Mae, MBA, Wells Fargo)

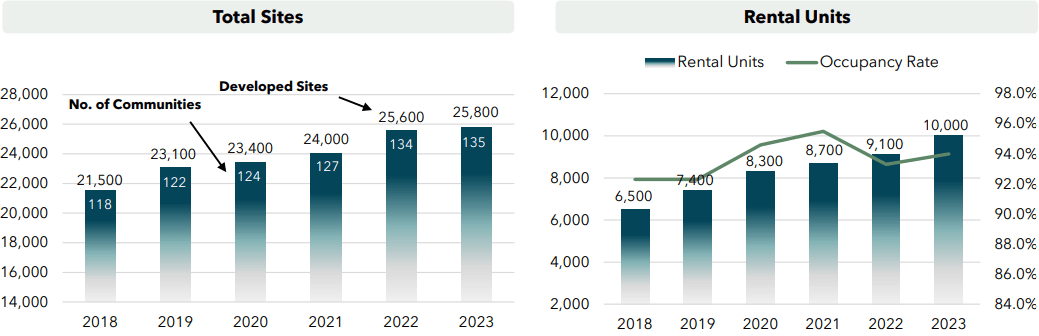

Coupled with improving occupancy, UMH has also been expanding its total number of units by building more housing. For example, since 2018, the REIT has grown the number of rental units under its belt from 6,500 to 10,000, which equates to a 9% CAGR, all while maintaining comparable leverage. With backlogs normalizing as manufacturers are able to supply inventory, UMH expects to add between 800 to 900 homes next year to its rental home portfolio.

Investor Presentation

Balance Sheet

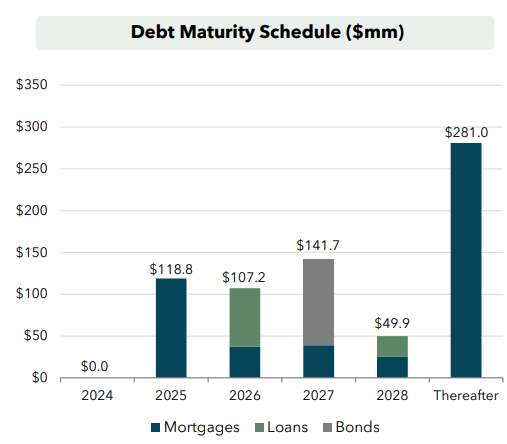

REITs are levered by their nature but in the case of UMH Properties, the balance sheet appears to be reasonable. On its books, the REIT carries $690 million of debt, 72% of which is mortgage debt. The mortgage debt was a weighted average interest rate of 4.17% which was 24 basis points higher than last year. The weighted average maturity was 5.3 years.

There was also $93.5 million of loans payable and a Series A Bond that bears interest at 4.72% and comes due in 2027. Adding two line items to the total debt gives us a weighted average interest rate of 4.63%, so the cost of debt appears to be low and very reasonable. With a cash position of $57.3 million, UMH currently has a Net Debt to EBITDA ratio of 6.2x and an interest coverage ratio of 2.7x, so the debt metrics are not cause for concern as the REIT is appropriately levered.

Investor Presentation Company Filings

Lastly, UMH also has some preferred stock on its books for about $290 million in aggregate across all the series. The most recent issuance of 2.6 million shares of Series D which generated $55.7 of cash for the company. These have a coupon of 6.375% at issuance and currently yield 7.0%. To grow its property portfolio, UMH has traditionally relied on a combination of debt, and common stock, and preferreds to access capital to expand its total number of properties.

Stable Dividend

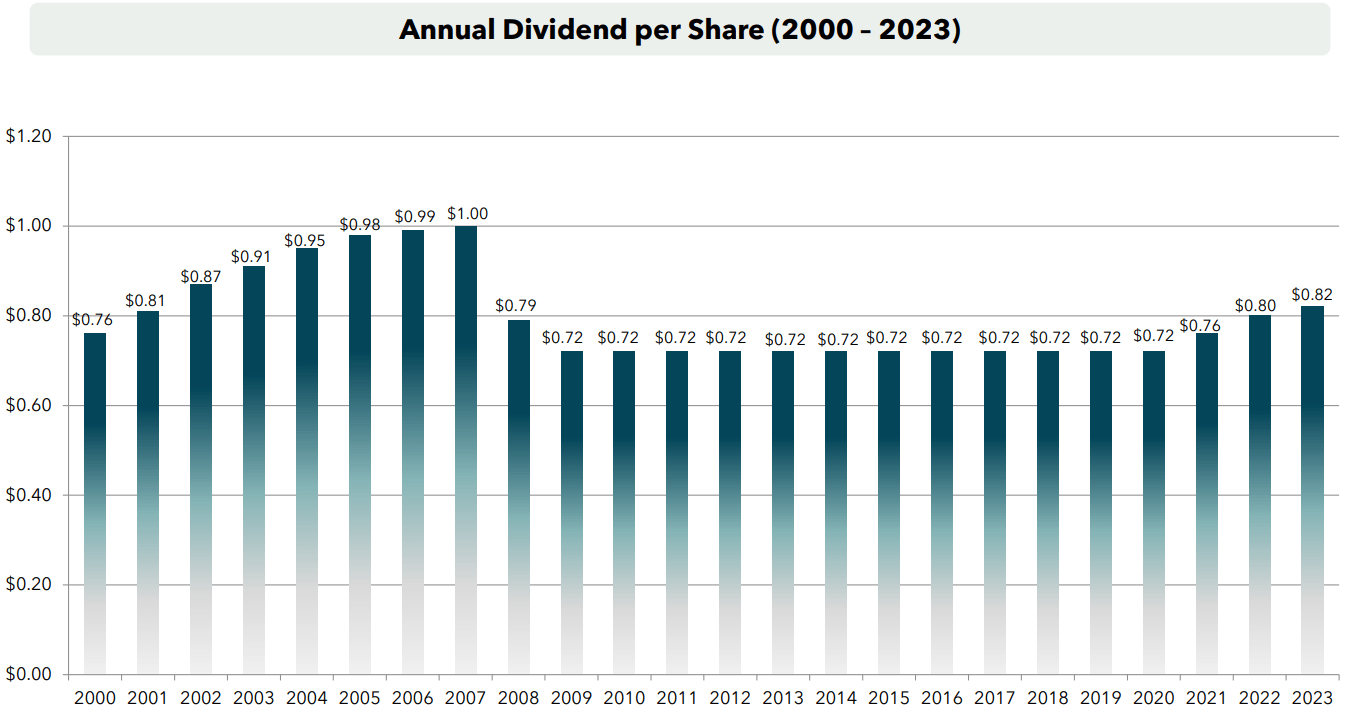

If you own REITs, you likely own them for the dividends. And in my opinion, UMH’s distributions are about as safe as I can find for a REIT. During the Great Financial Crisis of 2008-09, UMH was one of the few REITs that didn’t slash its dividend entirely. While it did cut it from annual dividends per share of $1.00 to $0.79, and subsequently $0.72 in 2009 where it remained for many years, it had a great track record of providing reliable income. So with growing FFO on a per share basis, the dividend is unlikely to be cut with a 95% payout ratio.

Investor Presentation

Risks

As for the risks to my investment thesis, there are a few risks that investors should consider. Firstly, one potential risk I see is that refinancing below 5% is likely to be difficult going forward. In my view, this is a known risk and one that the market has likely priced in, but it’s noteworthy to mention as interest expenses are a significant expense for UMH Properties. The most recent debt the company took on was a credit facility at 5.97% (fixed) so that should give us an idea of the upper bounds of where the company can refinance, considering that mortgage rates are already starting to head lower.

Another risk to consider is that occupancy doesn’t improve much from here. As I’ll discuss in the next section, UMH Properties trades at a higher valuation and closing the gap between its peers in terms of its occupancy ratio is something I think investors are counting on. With new units that UMH is building, it’ll be important to monitor whether the REIT is able to secure tenants for them.

Finally, the concentration risk in the shale region and eastern United States in general is a factor to be aware of since these aren’t the fastest growing regions of the U.S. Weaker than expected demand for manufactured housing as well as not seeing the anticipated recovery in shale region activity would be negatives that would hinder UMH’s FFO growth.

Valuation and Wrap Up

Of the 5 analysts who cover UMH Properties, 3 analysts have a ‘buy’ rating and 2 have a ‘hold’ rating. The average price target is $18.60, with a high estimate of $21.50 and a low estimate of $16.00 (source: TD Securities). From the current price to the average price target one year out, this implies potential upside of 14.5%, not including the dividend yield of 5.0%. Therefore, it seems that analysts are moderately bullish with total return potential of 19.5% over the next year.

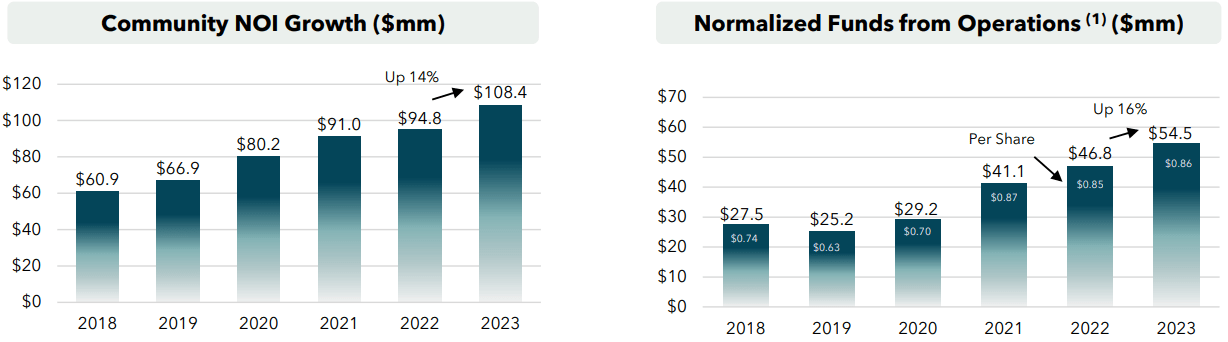

In my view, I believe the valuation seems reasonable. With FFO of $54.5 million in 2023 and a market capitalization of $1.13 billion, UMH Properties is trading at 20.7x P/FFO. While that may appear expensive at first glance, FFO is expected to reach $0.96 and $1.04 in 2024 and 2025, so the forward P/FFO ratios for this year and next year are 17.0x and 15.6x, respectively.

Unlike other REITs that should experience stable or even declining FFO next year, UMH offers investors a growing FFO on a per share basis. Likely the closest peer to UMH would be Sun Communities, which trades at a P/FFO of 18.1x and a forward P/FFO of 18.0x.

Given that there aren’t many levers to pull to increase FFO per share (given its higher occupancy), I don’t foresee much growth for the REIT. UMH on the other hand has significant potential, not to mention a better balance sheet that isn’t as levered and carries much more flexibility. Even if the company falls short of analysts’ expectations for FFO by 10% or so (which I think won’t happen given the priorities to expand the property portfolio and the addition of new units), UMH is cheaper on a forward basis. If UMH were to trade at Sun Properties’ forward valuation in one year’s time, then shares would be about 15.4% higher, or at about $18.40 per share.

Thus, despite an expensive multiple today, UMH has potential to grow into its current valuation based on its future FFO growth. This will give it the flexibility to continue growing its portfolio or reward shareholders with dividend increases.

Investor Presentation

So to conclude, I think UMH Properties looks like a buy at the current price of $16.24. While I don’t expect much capital appreciation, I view it as a safe way to generate a stable 5.1% yield. Given the fact that this is more of play for income-oriented investors, I would likely use options to generate additional yield. For example, the Sept 2024 $17.50 calls are currently selling for $0.55, so selling a covered call against a position would allow for upside of 7.8% before being called away to generate an annualized yield of 7.1% today in addition to the dividend.

Q2 2024 Earnings Call Transcript")