DINphotogallery/iStock via Getty Images

Investment Thesis

Being long in car carrier stocks was pleasant during 2023, but they have remained roughly flat since the start of 2024. Oslo Stock Exchange-listed Höegh Autoliners ASA (OTCPK:HOEGF) has fallen about 30 percent since its peak on February 14, 2024. Valuation calculations (dividend discount model and NAV) indicate that this fall is overblown. Combined with its new, ambitious dividend policy, this solid company offers a strong balance sheet, a newbuild program about to deliver its first efficient ships, and an excellent management track record. Even with a large global order book, projected demand indicates that this capacity will be absorbed.

Company Overview

Höegh Autoliners ASA is a global logistics company in the Ro-Ro space. It operates a fleet of 33 owned and long-term chartered Pure Car and Truck Carriers, ranging from 2,300 to 8,500 car equivalent units (ceu). HOEGF transports about 1.6 million ceu annually.

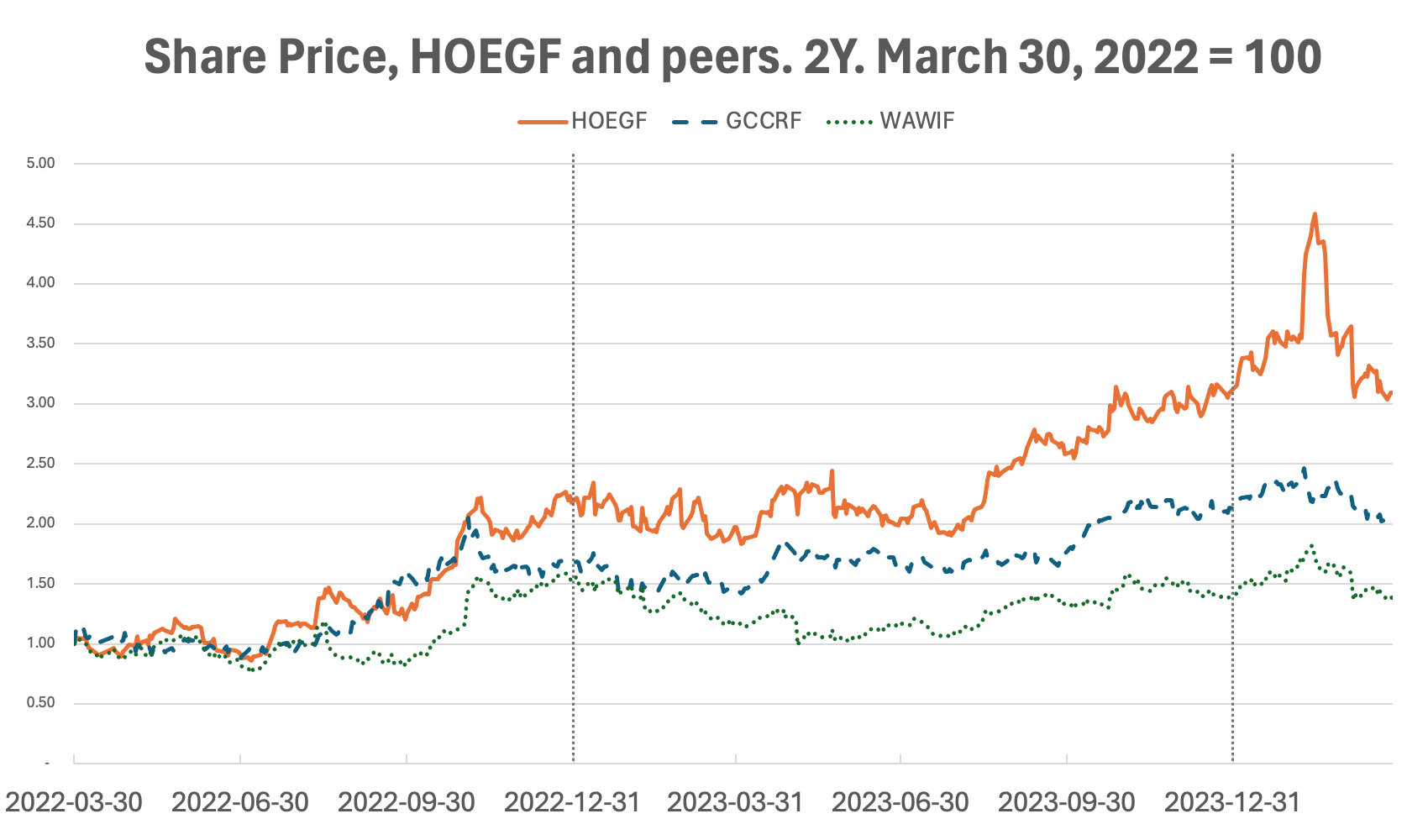

In the past two years, HOEGF has risen almost threefold after peaking at nearly 4.5 times in mid-February:

Share price, HOEGF, and peers. 2Y (Author’s work. Historical share prices downloaded from Euronext)

In the graph above, HOEGF is shown together with its Oslo Stock Exchange-listed peers Wallenius Wilhelmsen ASA (OTCPK:WAWIF), a logistics company, and tonnage provider Gram Car Carriers ASA (OTCQX:GCCRF).

By comparison, the Oslo Stock Exchange Benchmark Index was nearly flat in the same period, and the S&P 500 was up about 15 percent.

Recently, the stock had some wild swings after posting Q4 2023 results. It gained 15 percent after posting its record result but later fell back to its previous level. On March 6, the stock tumbled 13 percent on reports that the EU will commence customs registration of Chinese EVs in connection with a probe that could result in tariffs.

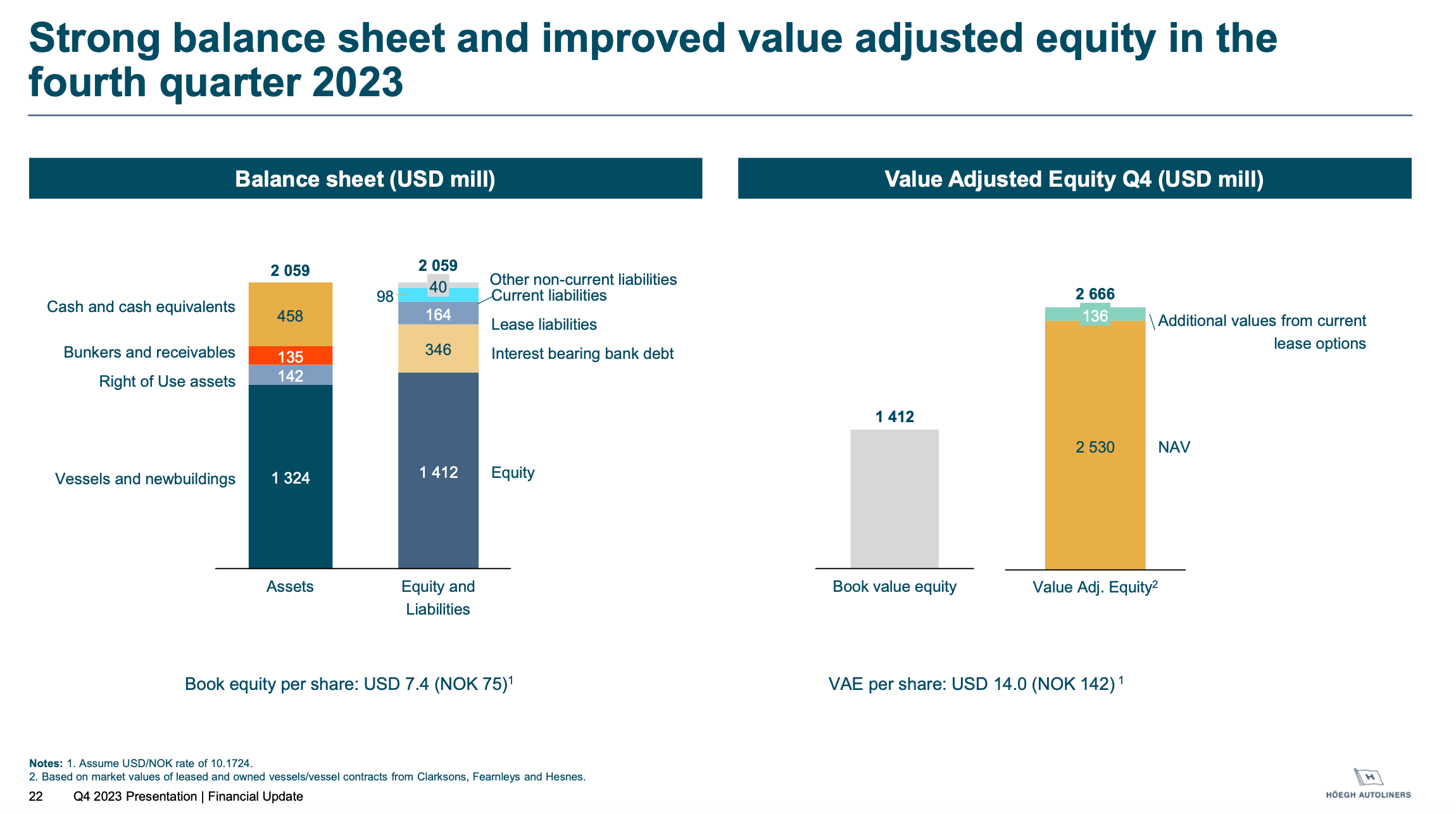

Balance Sheet: Cannot Complain

As the slide below illustrates, the HOEGF balance sheet is in good shape. With $458 million in cash, it can immediately meet almost all its interesting-bearing debt and lease liabilities. Its equity to total capital ratio is a healthy 68 percent.

According to the sources it consulted, the NAV per share is about NOK 142. On March 27, the share closed at NOK 92.20 – a 35 percent discount to NAV.

Balance sheet and NAV, Q4 2023 (HOEGF Q4 2023 presentation)

Ownership Structure Points to Credibility Among Professional Investors

Höegh Autoliners is majority-owned by the Høegh family, represented by its 53 percent ownership through Leif Höegh & Co AS. The Høegh family name has been known for its good name for decades. A 2016 article in the Norwegian daily Aftenposten chronicled the family’s efforts through generations to focus on doing the right things and avoid scandals and negative publicity.

Several institutional investors are among the top 20 shareholders. This indicates that the stock enjoys credibility among professional investors, which is usually a good sign.

New Dividend Policy: 100% of Cash Generation

The revised dividend policy states that the company aims to pay out 100 percent of “cash generation after amortization of debt facilities, capital expenditures, and payable taxes” will be distributed. The market outlook and “the Company’s financial position” will also be considered. In other words, it aims to pay out its full free cash flow.

It is worth noting that dividends will be declared in USD and paid in NOK. This conversion can affect investors with a brokerage account denominated in a currency other than NOK.

HOEGF started paying dividends in the second quarter of 2022, and its dividend has grown every quarter since.

Well-Timed Purchases of Leased Ships

HOEGF has leveraged options in its lease contracts to purchase leased ships at attractive prices.

| Announcement date | Ship | CEU capacity | Purchase price (million USD) | Reported market price (million USD) |

| Oct 30, 2023 | Höegh Jacksonville | 6,500 | 43.2 | 84.0 |

| Feb 27, 2024 | Höegh Jedda | 6,500 | 43.2 | 91.0 |

As the table above shows, HOEGF could save $88 million on these transactions compared to purchasing equivalent ships in the market.

In the same period, HOEGF sold Höegh Bangkok, a 6,500 ceu ship, for $63 million, and the 6,000 ceu Höegh Chiba for $61 million.

Newbuilding Program: Aiming for Fuel Optionality

HOEGF signed contracts for eight new ships, the dual-fuel powered Aurora class in 2022, and declared an option on an additional four in July 2023, bringing the total ships on order up to twelve. The Aurora class is both methanol and ammonia-ready, requiring only a conversion to burn ammonia and methanol. HOEGF secured USD 14 million in state-backed funding for two of these conversions. If the USD 7 million per ship figure remains accurate, Höegh will have to invest USD 70 million to convert all of its newbuilds when the time comes.

That time is expected to come in 2027, starting with “a gradual ramp-up” when “availability and price reach satisfactory levels.” In other words, the first two vessels will burn either MGO or LNG for at least three years.

The new ships can use up to 44% of their cargo capacity on valuable high and heavy cargoes. Hoegh’s current fleet has about 22 percent. HH cargo represents an interesting income stream. Construction equipment has slightly different market dynamics than light vehicles and enables value-adding services due to their handling requirements.

The timing of these acquisitions is crucial, as evidenced by comparing HOEGF to its peer, WAWIF. The latter was slower in commencing its fleet renewal program, resulting in it having to contract new ships at higher prices and later delivery dates.

HOEGF has not revealed the purchase price, but sources claim the cost is about $97.5 million per ship for the first eight ships.

Peer WAWIF announced its first firm orders in August 2023, one and a half years later. The 9,350 ceu, methanol-capable, and ammonia-ready Shaper class will see its first deliveries in Q2/Q3 2026. According to Norwegian finance daily Finansavisen, the average price is about $112 million per ship. Since then, WAWIF has increased its order to eight ships.

In summary, HOEGF is getting a competitive advantage over its peers by receiving ships two years earlier at a 12 percent lower cost.

Market Outlook

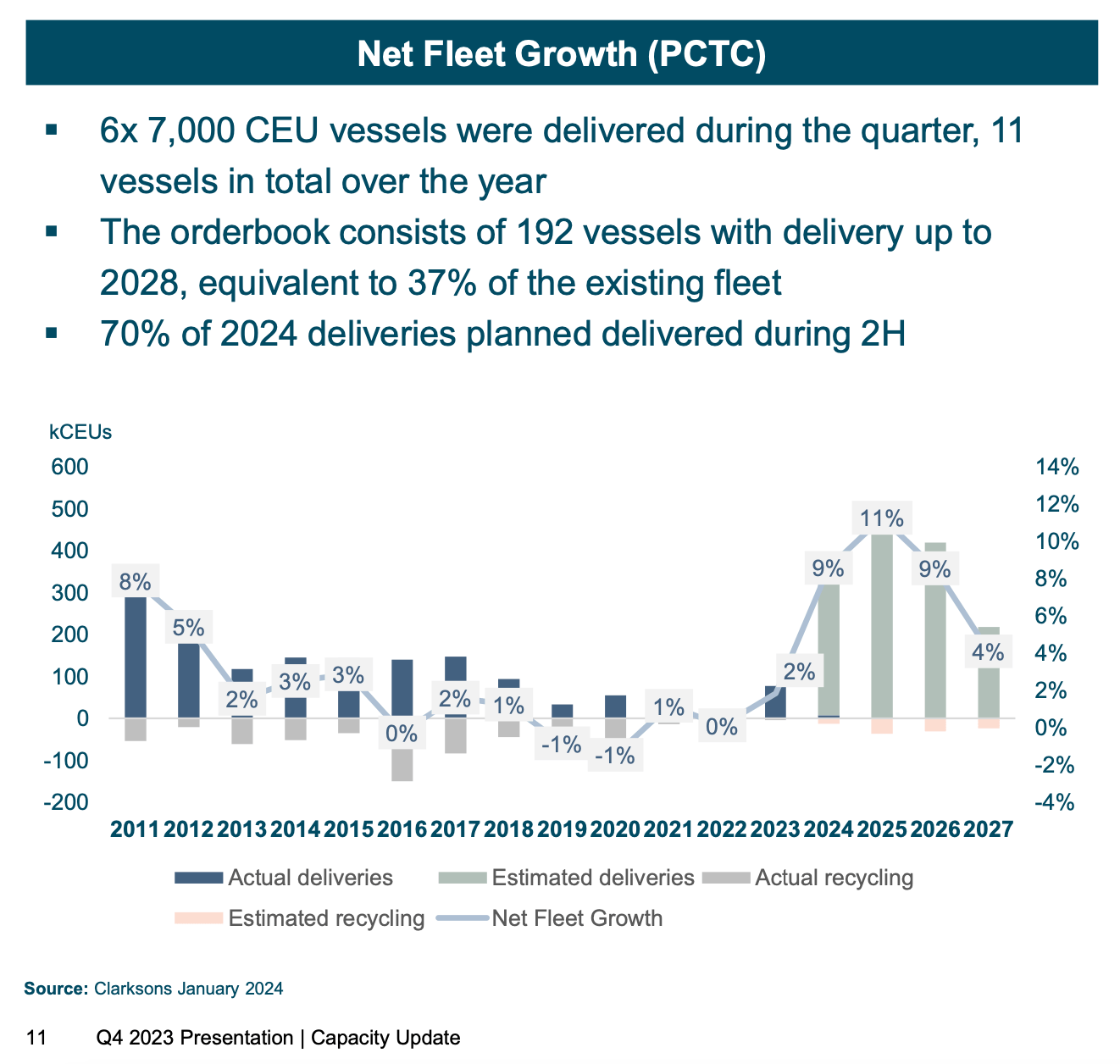

Headwinds: Ballooning Order Book

HOEGF acknowledged the high fleet growth expected in the coming years. But, as we’ll see below, more than this net fleet growth might be needed to absorb demand – especially if the Red Sea rerouting continues.

Expected net fleet growth, 2024-2027 (HOEGF Q4 2023 presentation)

In addition, Chinese automakers continue to invest in their ships. A more integrated value chain may reduce the addressable market for players like Höegh.

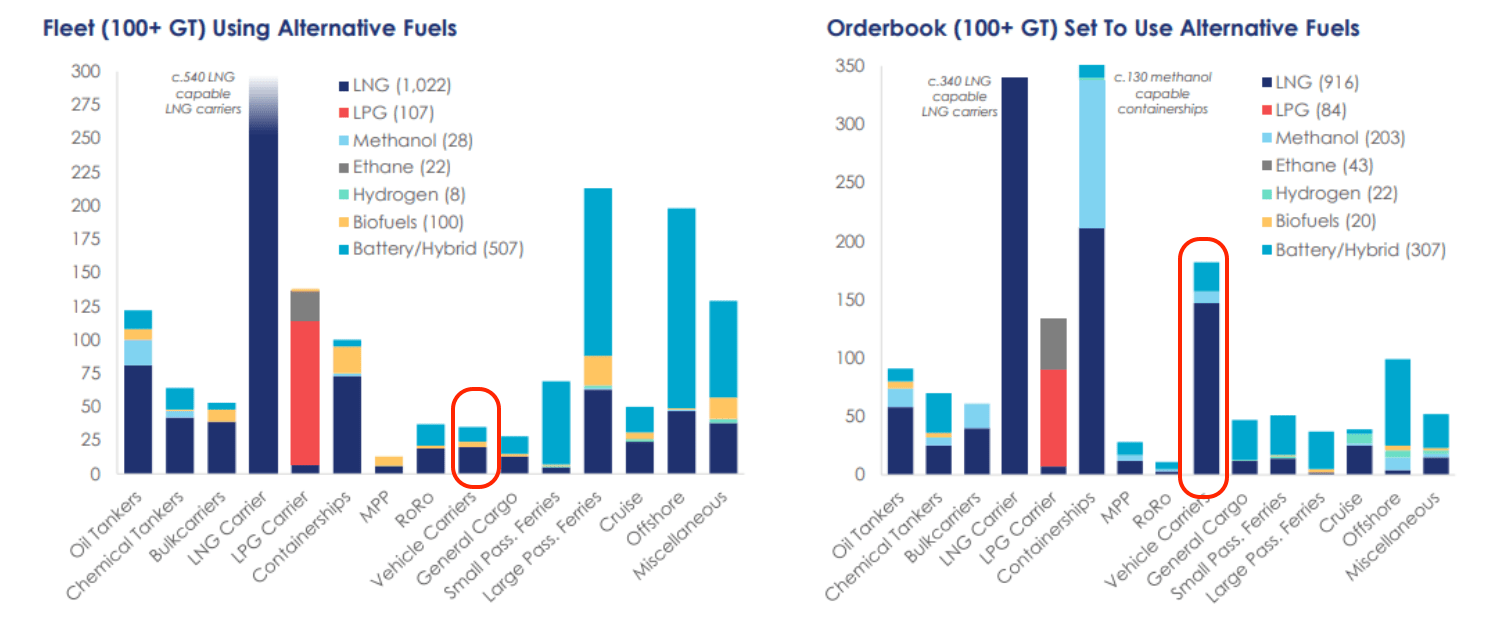

Tailwinds: Demand for Greener Supply Chains and Vessels on Water Shortfall

For some time, charterers have been looking to reduce the carbon footprint of their supply chains.

This is evident in the amount of alternative-fueled ships in the order book for vehicle carriers. The order book of 200 is about four times the current fleet of roughly 50:

Order book (Offshore Energy citing Clarkson’s Research. Annotated by the author)

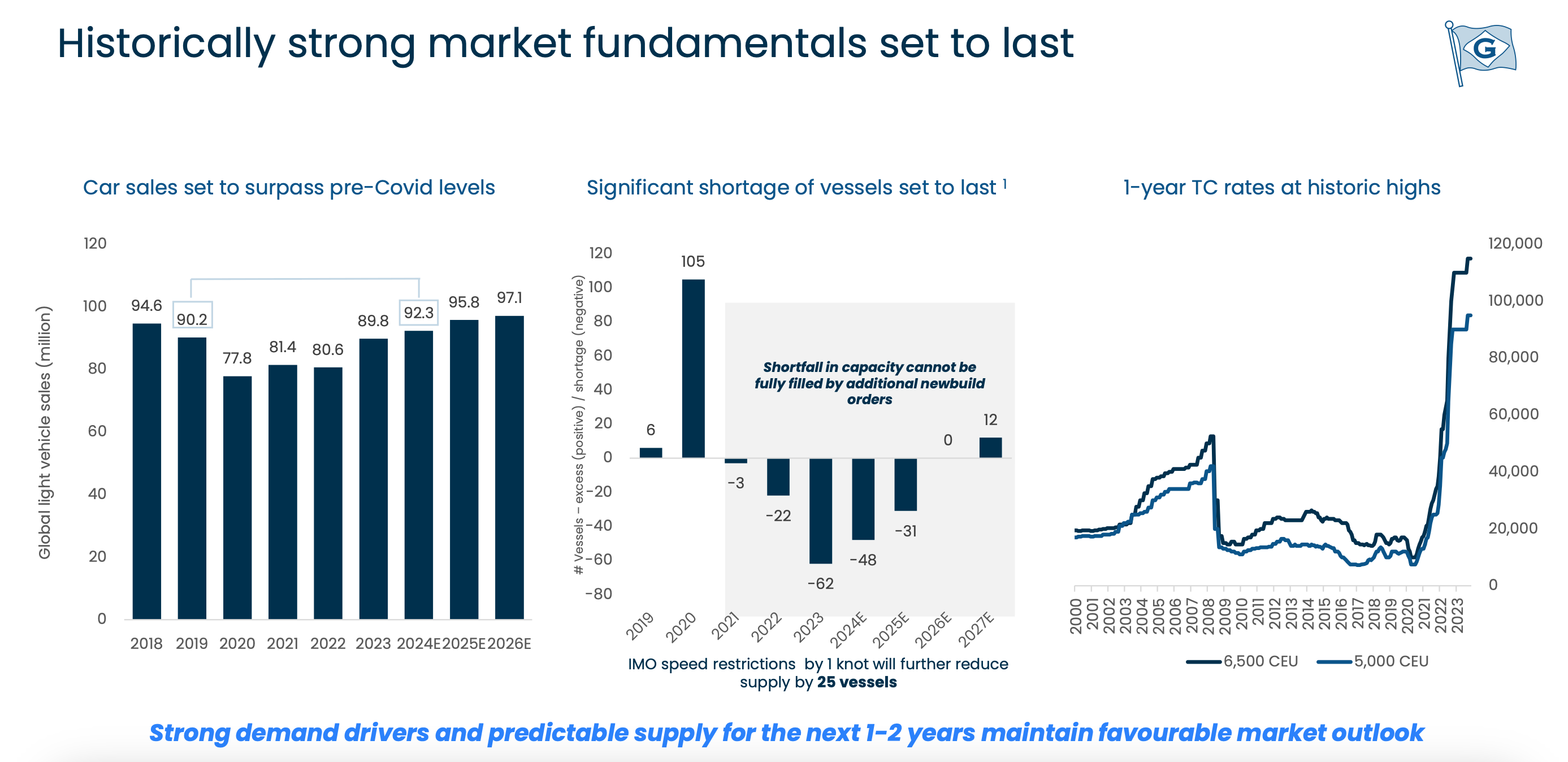

Peer Gram Car Carriers uses this slide in its latest earnings presentation (p. 5) to explain current market fundamentals. Light vehicle sales are expected to exceed pre-2020 sales, and there aren’t enough available ships on the water to absorb this demand:

Market fundamentals as of 2024 (Gram Car Carriers Q4 2023 presentation)

A Note on Alternative Fuels

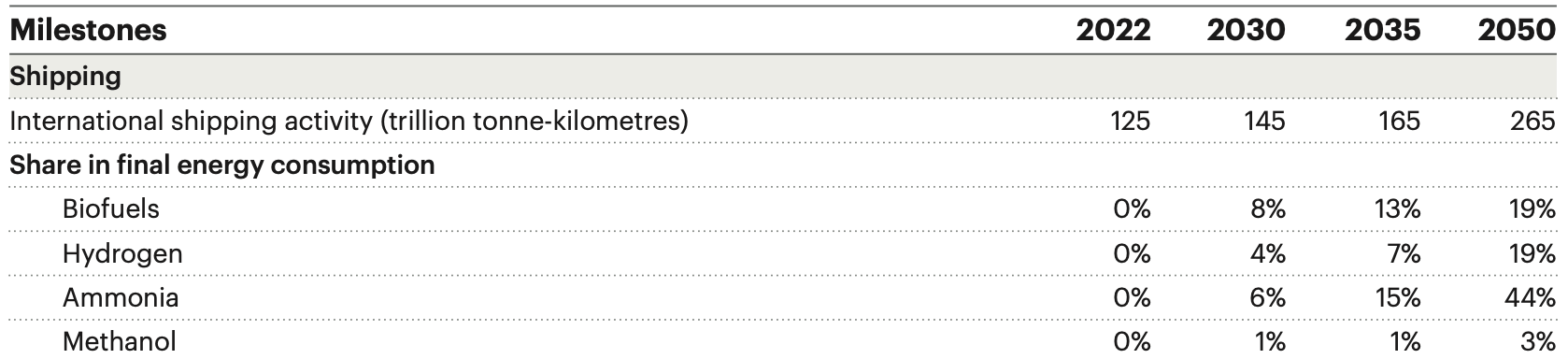

Adopting ammonia as a ship fuel is fraught with challenges but also opportunities, as Bureau Veritas’s excellent fact site shows. IEA’s Net Zero Roadmap (2023 update, p. 94) forecasts methanol consumption by ships at just 3 percent by 2050. Ammonia, on the other hand, is expected to make up 44 percent of the fuel mix by 2050:

IEA prediction for shipping fuel mix 2050 (2023 update9 (IEA Net Zero Roadmap)

Marine engine maker MAN expects its first ammonia engine to operate “from around 2026“. According to that same press release, MAN forecasts “around 27% of fuel used onboard large merchant-marine vessels to be ammonia by 2050.” If that figure is also used in the IEA forecast cited above, it implies that small merchant-marine vessels-and other classes-will consume ammonia to a much larger extent.

Then there’s the problem of producing “green” ammonia, as opposed to “brown” ammonia – a technology still in its infancy.

With its new fleet of ammonia- and methanol-ready vessels, Höegh will be ready to adapt to a changing fuel environment.

Valuation and Risks

After the recent share price drop, HOEGF trades below the midpoint of its 52-week range at a P/E of 2.8.

Valuation metrics, HOEGF (Seeking Alpha)

Assuming 3 percent growth and 12 percent cost of capital, the dividend discount model for perpetual dividends would yield an annual dividend of just NOK 8:

DDM (Author’s calculation)

In other words, with those assumptions, a quarterly dividend of NOK 2 supports current pricing.

Based on the above, I expect HOEGF’s dividend capacity to exceed NOK 2/quarter. HOEGF can provide dividends and capital gains from its current price of NOK 92. This point is also supported by its share trading at a 35 discount to NAV.

Of course, the assumptions may be simplified, particularly in an industry known for being cyclical, such as shipping.

Investing in shares on the Oslo Stock Exchange also carries its risks: The investor is exposed to the NOK, a relatively small and illiquid currency. Norway levies a dividend withholding tax, but you might be eligible to avoid this tax.

Conclusion

This article reviews one of the significant PCTC logistics companies listed on the Oslo Stock Exchange in light of its recent share price decline of about 30 percent from a high on February 14, 2024. This fall seems exaggerated, and given the company’s strong balance sheet and favorable market, there might be potential for a recovery.

Regardless of what fuel sources will be available and required in the next two decades, Höegh’s new class of 12 large, versatile ships will propel the company to the forefront of the industry. Their adaptability ensures they can transition to fuel types like ammonia or methanol following small conversions.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")