Wipada Wipawin

Now more than ever, in my view, is a great time to pick up contrarian stock investments while the market is hovering around all-time highs. Not all great growth stories in the tech sector have to do with AI, after all. Plenty of overlooked stocks have equally exciting growth trajectories this year and are about to turn the corner on profitability.

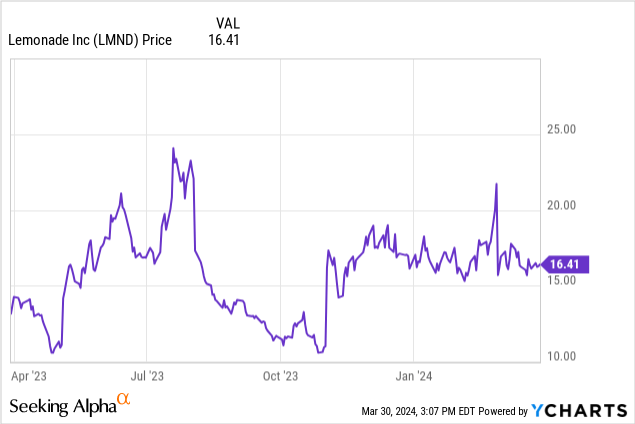

With this in mind, consider picking up shares of Lemonade (NYSE:LMND). The digital insurance platform has seen its share price dip this year while other tech peers have rallied, making now a great time to reexamine the bull case for this company.

I last wrote a bullish opinion on Lemonade in December; when the stock was trading closer to $18 per share. Since then, Lemonade has continued to decline while at the same time releasing strong Q4 results and bullish commentary for FY24. There couldn’t be a better time, in my view, to pick up this stock while it’s low. I remain bullish on Lemonade – either hold on to your existing positions for more upside or take the muted activity so far in 2024 as an opportunity to add more.

Two factors are worth mentioning that we’ll dive into further detail in this article. First: Lemonade is planning on accelerating its growth in IFP, or in force premium. The company is seizing an opportunity to invest more dollars into customer acquisition this year in an attempt to bolster its scale. The company is also expanding its footprint in Europe, diversifying further away from the US. Second: losses are coming down. The company has been intentional about managing its portfolio, in particular reducing its exposure to losses in housing insurance. It expects to be steadily FCF positive by the end of this year.

Here’s a refresher on my longer term bull case on Lemonade:

- Consistent and aggressive growth rates demonstrate a greenfield market opportunity. Lemonade continues to grow IFP at a >20% y/y clip. And though the current market is very nonchalant about these impressive growth rates, to me, this shows a business that is still very much in its nascency and able to scale to much greater heights.

- Lemonade is the new way to buy insurance. Gone are old-school insurance agencies and insurance agents; nowadays, just like everything else, we buy insurance online. As the new generation of tech-savvy millennials and younger cohorts dominate the consumer base, insurtech vendors like Lemonade will gain market share versus their legacy counterparts.

- Healthy product diversification and cross-selling product flywheel. When it started out, Lemonade just offered home and renters insurance. Now, the company is also offering bundles with pet insurance and car insurance as well (the latter through its acquisition of Metromile). Perhaps in no other industry is diversification more vital than in insurance, so Lemonade’s ability to continue growing into other insurance streams will be critical to its success.

- Loss ratios are set to improve. Lemonade is already on a positive trajectory for loss ratios, driven by both increased scale as well as efficiency of its AI bot for paying off small, legitimate claims. Progress toward regulatory approval for rate changes will help to accelerate the trajectory of loss ratio improvements as well. In addition, lower exposure to house insurance as a percentage of its total portfolio will help improve loss ratios as well.

All in all, I believe Lemonade remains substantially underappreciated. Stay long here and wait for the rebound.

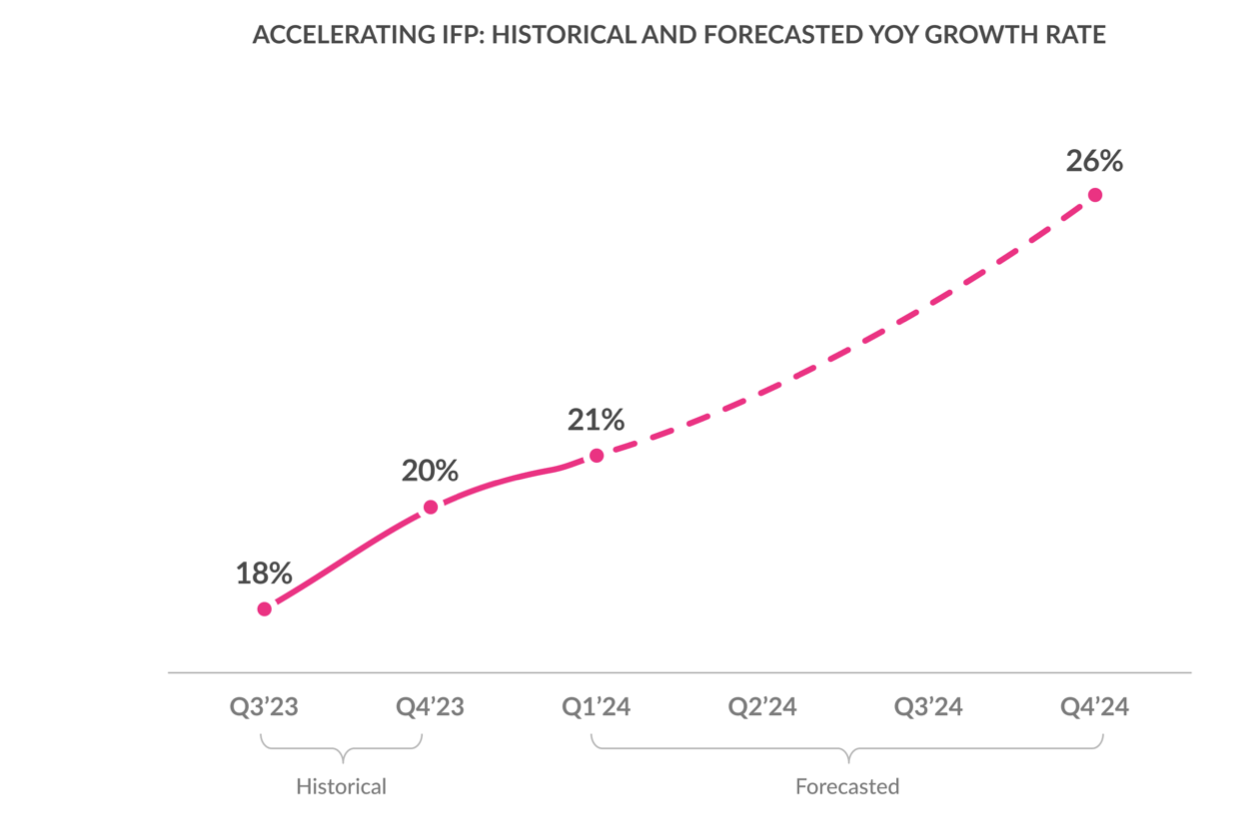

Accelerating IFP growth expected for 2024

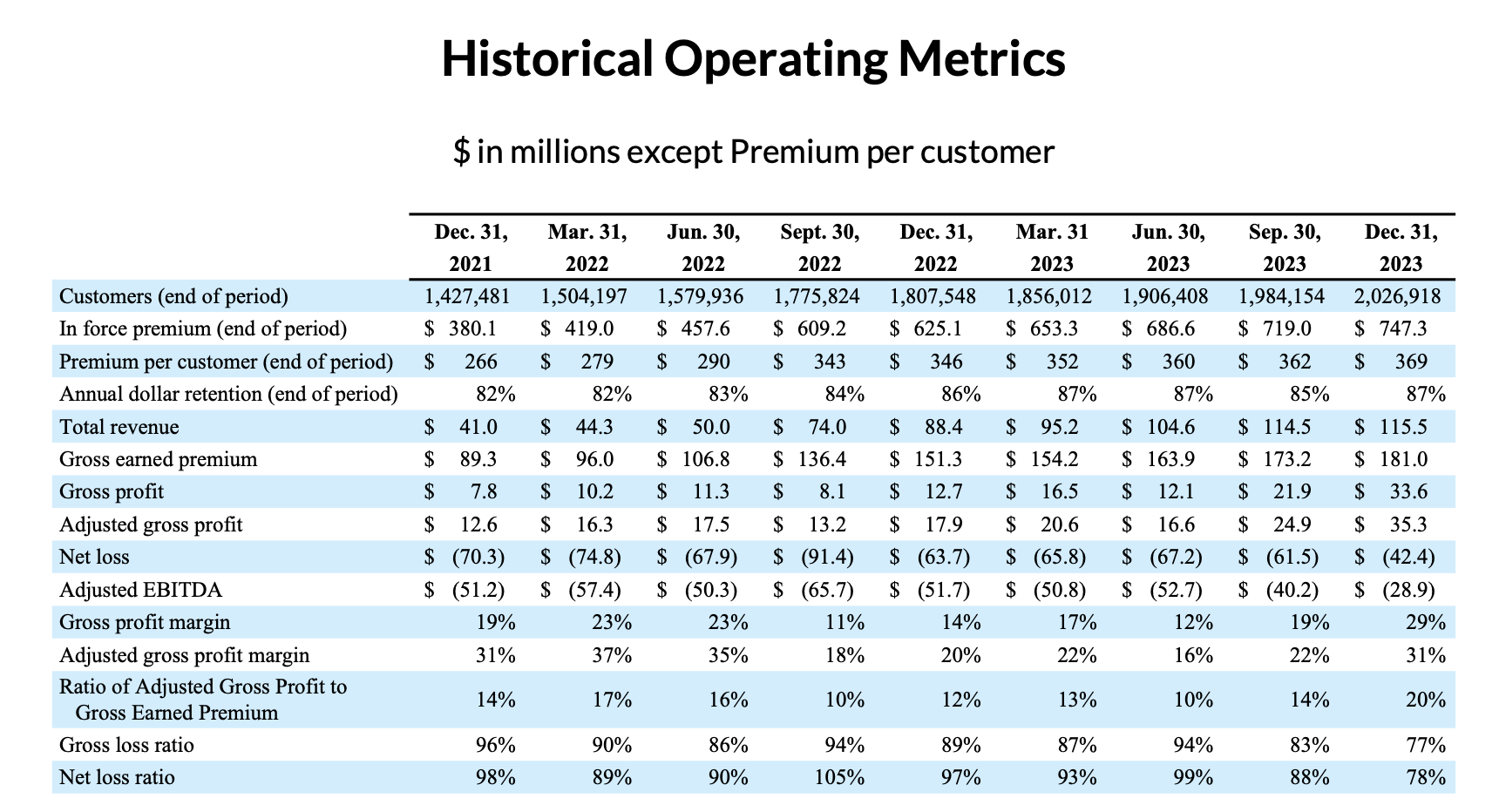

2024 is shaping up to be a year of growth for Lemonade. Note that the company exited the fourth quarter of 2023 on a high note:

Lemonade key trended metrics (Lemonade Q4 shareholder letter)

As shown in the chart above, IFP grew 21% y/y to $747.3 million, accelerating over 19% y/y growth in Q3. Revenue growth, meanwhile, clocked in much higher at 31% y/y to $115.5 million, ahead of Wall Street’s $111.5 million (+26% y/y) expectations by a wide five-point margin.

It’s important to recognize that Lemonade is intent on growing smartly and not signing on to every policy opportunity that comes its way. It is still waiting on a number of rate increase approvals that will allow it to become more profitable, and until that happens, it’s limiting its growth of new policies (as a personal anecdote: I failed to get a quote from Lemonade on home insurance recently, signaling that the company is being very conservative in policy growth). And in spite of these policies, it is still growing IFP at a >20% clip.

Per CFO Shai Winiger’s remarks on the Q4 earnings call regarding the company’s growth policy:

We still await significant further rate approvals. And so for much of 2024, we will continue to constrain sales of two products with the highest average premium and the largest markets, Home and Car.

In other words, we will continue to throttle growth this year too. That said, the tide has definitely turned. With every passing months, we are seeing more and more opportunities for profitable growth across our portfolio, including Home and Car, and we will be relaxing these growth constraints accordingly.

This is great news. And it’s the reason we’re projecting to begin to accelerate growth this year. Growth may be a virtue in its own right, but for us it’s a necessity. Our business is still subscale and so we need to continue growing. And so in 2024, we plan to accelerate our growth rate, but beyond being a welcome sign of improving conditions accelerated growth also presents challenges we want you to be aware of.”

The chart below, meanwhile, showcases that the company expects IFP growth to accelerate every quarter this year:

Lemonade IFP expectations (Lemonade Q4 shareholder letter)

This is driven by two factors: first, loosening up on the aforementioned growth restrictions once rate increase approvals come in; and second, the company plans to spend an additional $55 million on marketing this year.

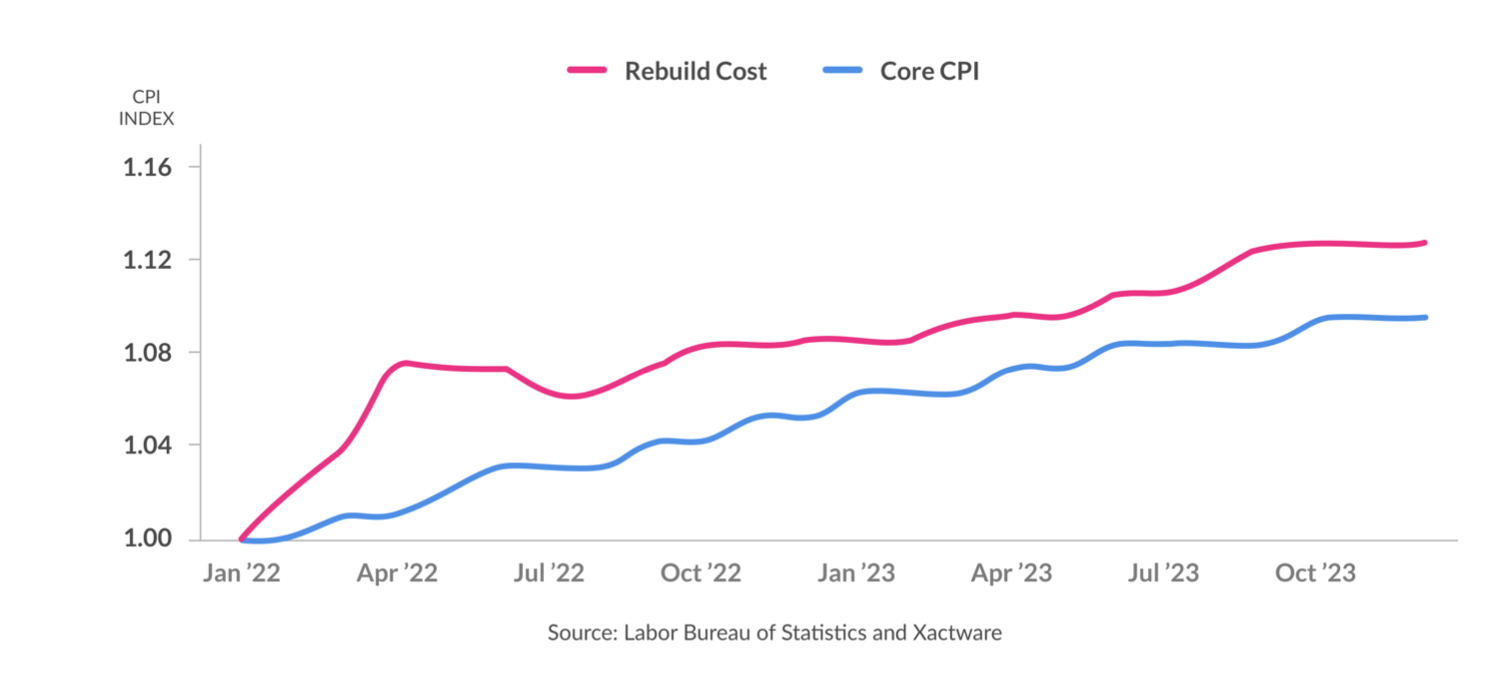

Smart portfolio decisions have helped to bring down loss ratios

To flesh out exactly how Lemonade has been smart about growing its book of business, consider the chart below from the company’s recent Q4 shareholder letter. Management is illustrating here that the rebuild out of new homes has far outpaced core CPI inflation for several years:

Housing rebuild costs (Lemonade Q4 shareholder letter)

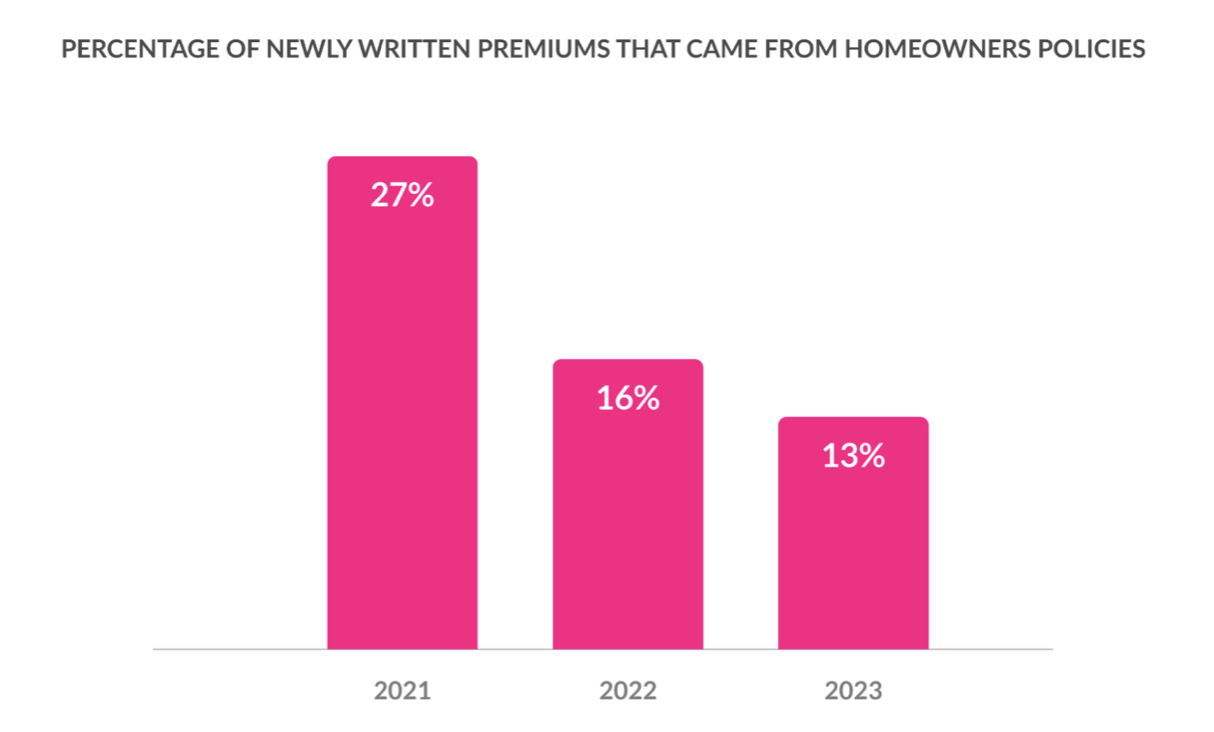

Recognizing that home insurance policies have been a loss leader over the past several years (at least until rate changes come into play), Lemonade has shrunk down the percentage of newly written premiums anchored by homeowners policies, as shown in the chart below:

Lemonade portfolio composition (Lemonade Q4 shareholder letter)

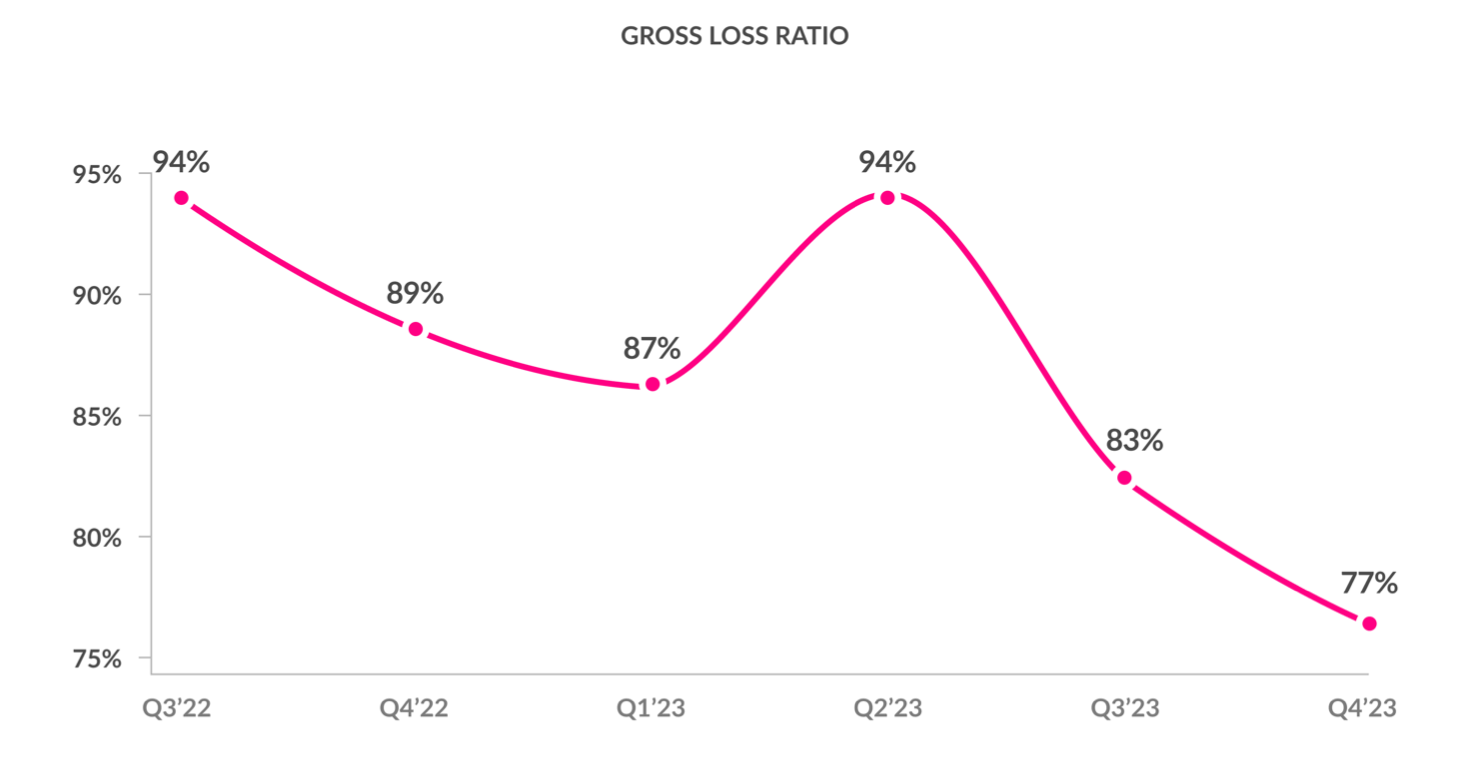

This, on top of growing economies of scale in general, have helped the company shrink down its gross loss ratios to 77% in the most recent quarter, not far from its longer-term target of 75%:

Lemonade loss ratios (Lemonade Q4 shareholder letter)

With these improvements in profitability, management notes that Lemonade is set to turn cash flow positive on a full-year basis by next year.

Key takeaways

With expectations for accelerating growth this year and a positive tilt toward profitability driven by prudent portfolio management, there’s a lot to like about Lemonade heading into the remainder of 2024. Though certainly still an early-stage disruptor, Lemonade has a lot of positive catalysts tilting in its direction. Stay long here.

Q2 2024 Earnings Call Transcript")