Smederevac

A few months ago, I wrote an initiation article on the KraneShares China Internet & Covered Call Strategy ETF (NYSEARCA:KLIP). In my opinion, the limited upside/unlimited downside structure of the KLIP ETF was not appealing, despite the fund’s large headline distribution yields.

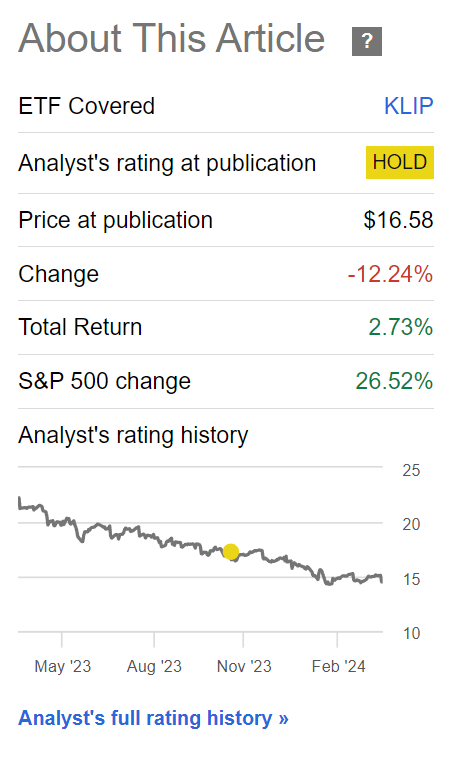

With a few months gone by since my initiation article, I want to revisit the fund, to see if my initial assessment was correct. Since my article, the KLIP ETF has declined by 12%, although the fund’s high distribution yield has allowed the fund to deliver positive total returns (Figure 1).

Figure 1 – KLIP has returned 3% since October (Seeking Alpha)

Brief Fund Overview

First, an overview of KLIP’s investment strategy, for those not familiar. The KraneShares China Internet & Covered Call Strategy ETF is KraneShares’ foray into ultra-high yielding ETFs.

The actual strategy behind the KLIP ETF is relatively straightforward and has been employed by many other asset managers like Global X with its highly successful (in terms of AUM) Global X NASDAQ 100 Covered Call ETF (QYLD) and JPMorgan with its JPMorgan Equity Premium Income ETF (JEPI).

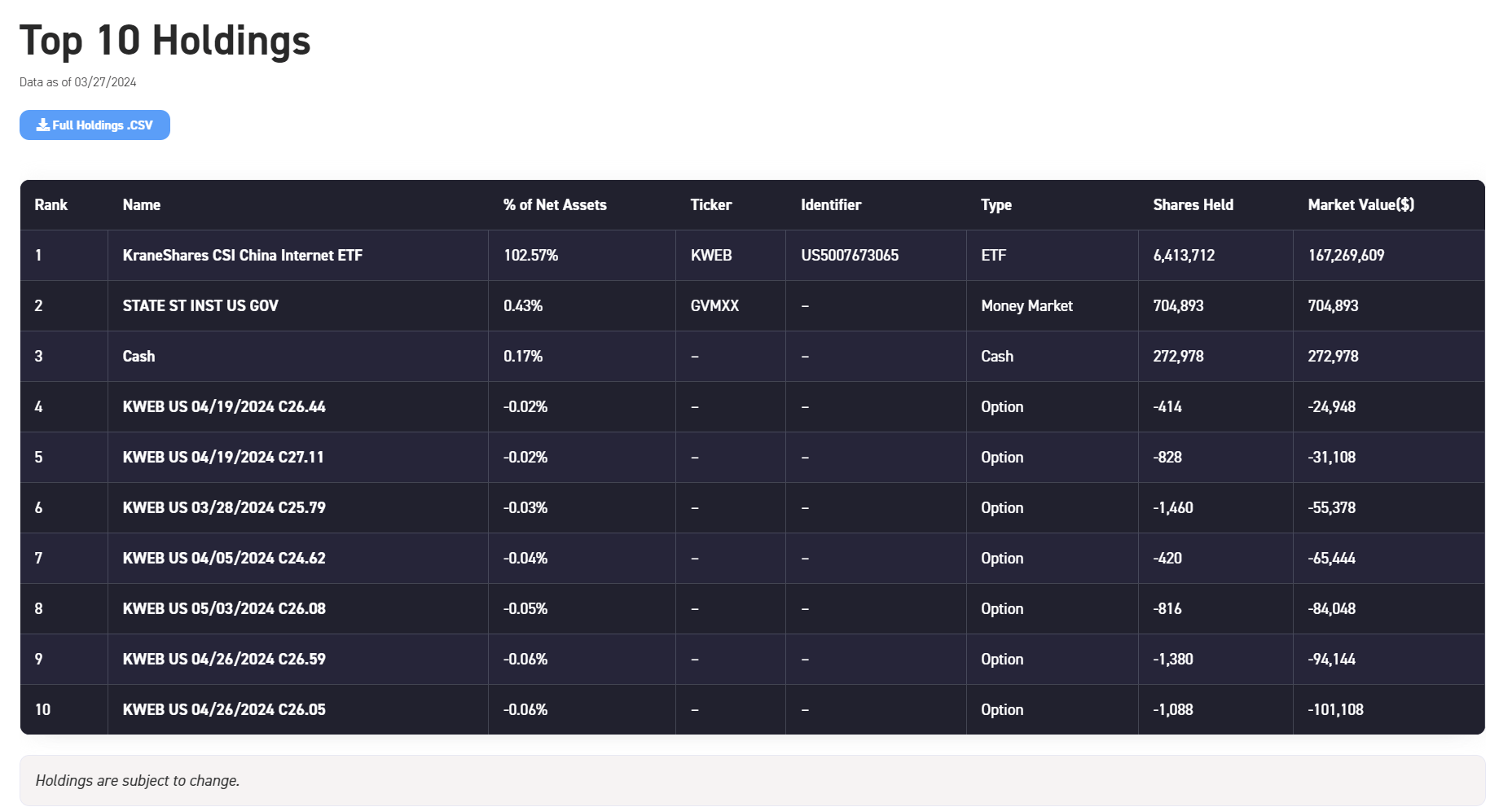

KLIP employs a ‘covered-call’ or ‘buy-write’ strategy where the fund owns the KraneShares CSI China Internet ETF (KWEB) and writes call options against this long position (Figure 2).

Figure 2 – KLIP holdings (kraneshares.com)

As we can see from Figure 2, KLIP writes a series of short-dated call options against its long holdings in the KWEB ETF. The main goal of the KLIP ETF is to provide investors with an attractive current yield while retaining capped participation in the upside potential of the KWEB ETF.

KLIP Has Delivered On Its Yield Promise

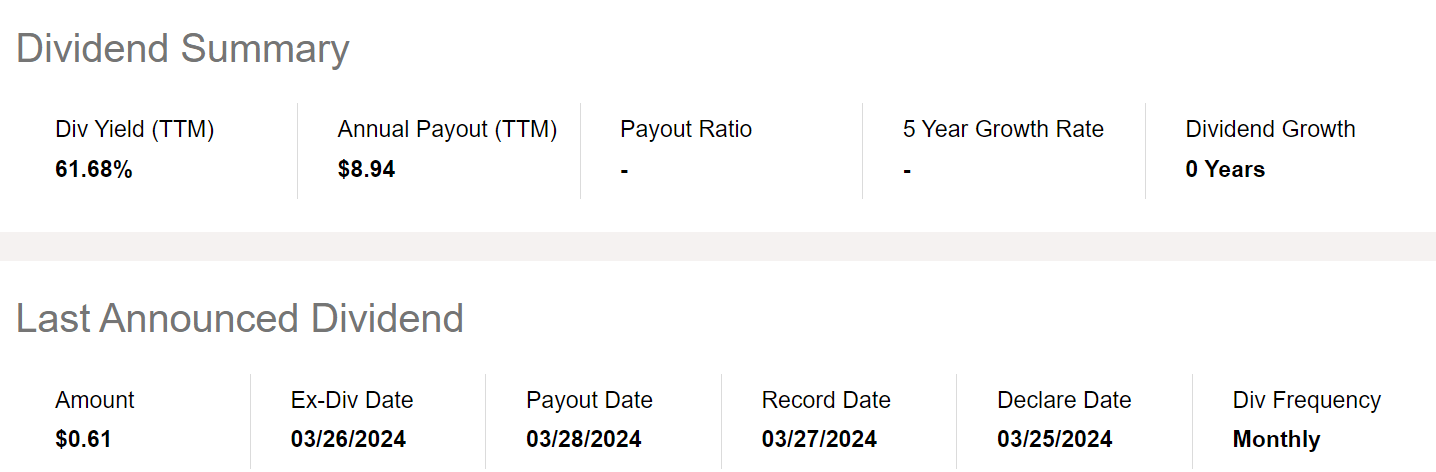

Looking at KLIP’s dual mandate of providing an attractive current yield and upside participation, we can see that KLIP has certainly delivered on the yield mandate, as the fund has paid $8.94 in trailing 12 month distribution or a 61.7% distribution yield (Figure 3).

Figure 3 – KLIP has paid 61.7% distribution yield (Seeking Alpha)

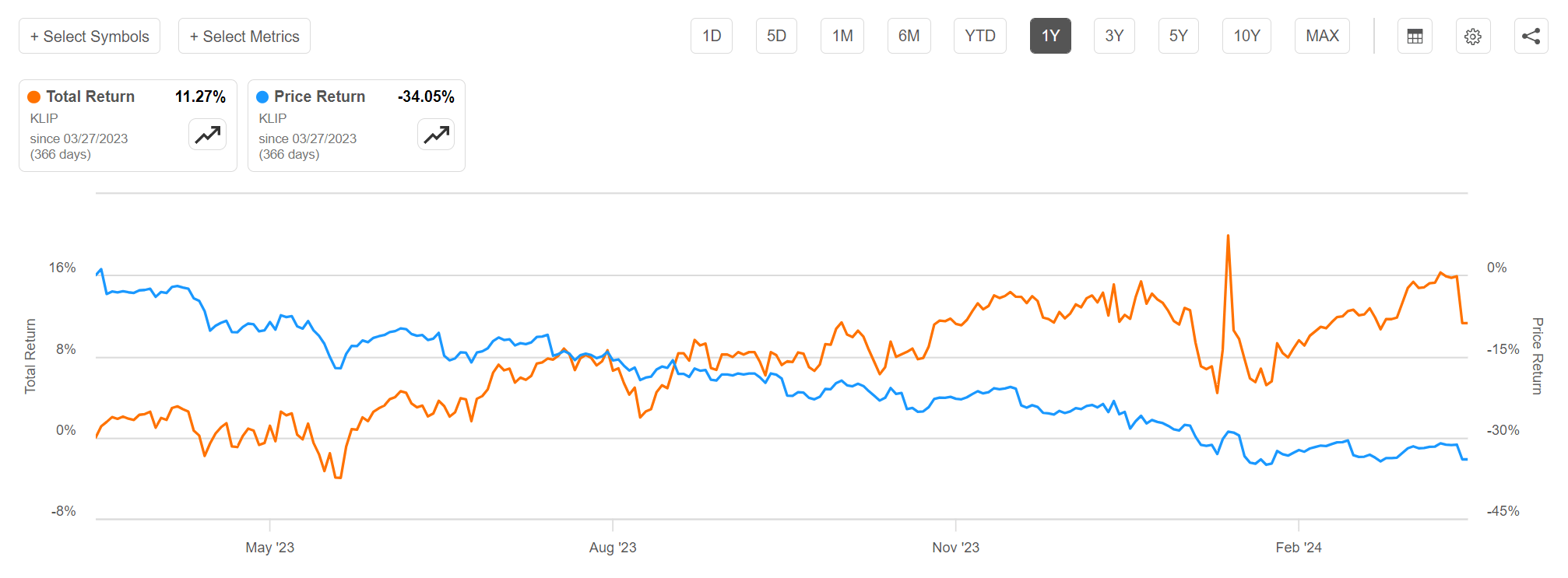

However, offsetting KLIP’s high yield has been a relentless reduction in the fund’s net asset value (“NAV”) such that 1 year total returns were only 11.3% (Figure 4).

Figure 4 – KLIP’s total returns have been much lower than its yield (Seeking Alpha)

Capped Upside And Uncapped Downside

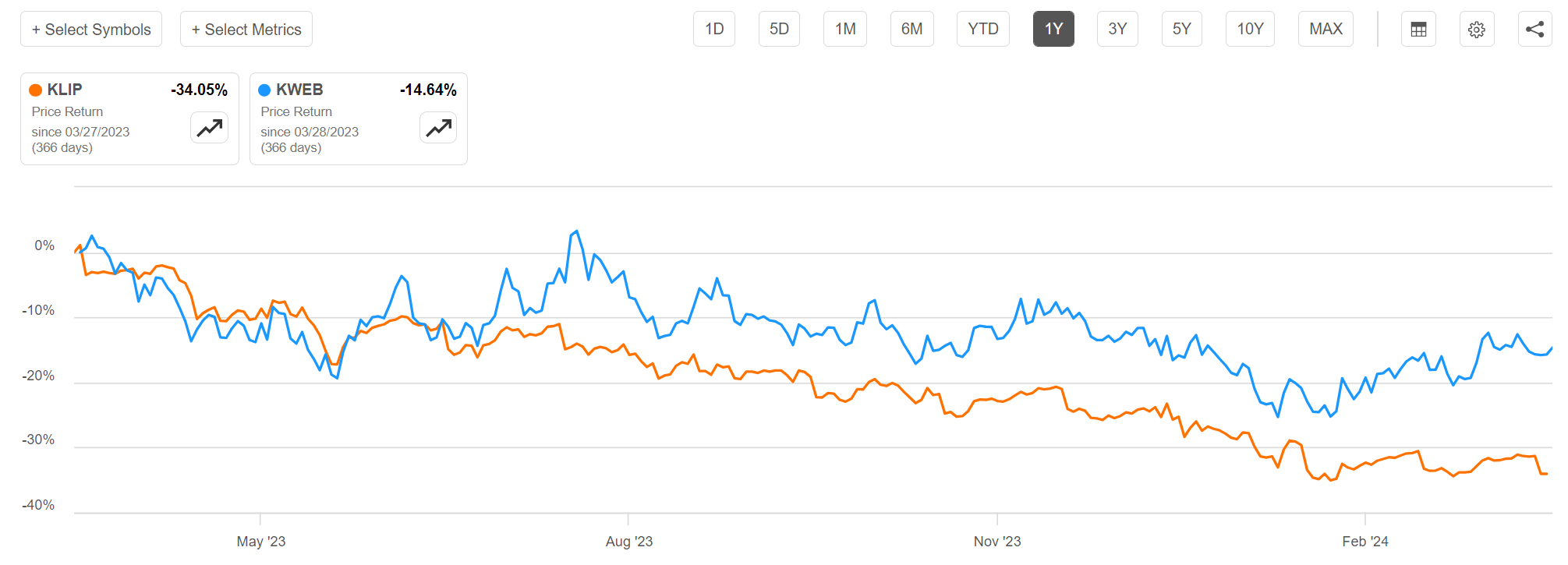

Part of the reason for KLIP’s NAV amortization is due to the fact that the underlying KWEB ETF has been performing poorly. Since KLIP holds only KWEB in its portfolio except for sold calls, when the value of KWEB declines, so does the value of KLIP (Figure 5).

Figure 5 – KLIP tracks KWEB weakness (Seeking Alpha)

Due to the nature of the covered call strategy, the KLIP ETF has capped upside and uncapped downside with respect to the underlying asset.

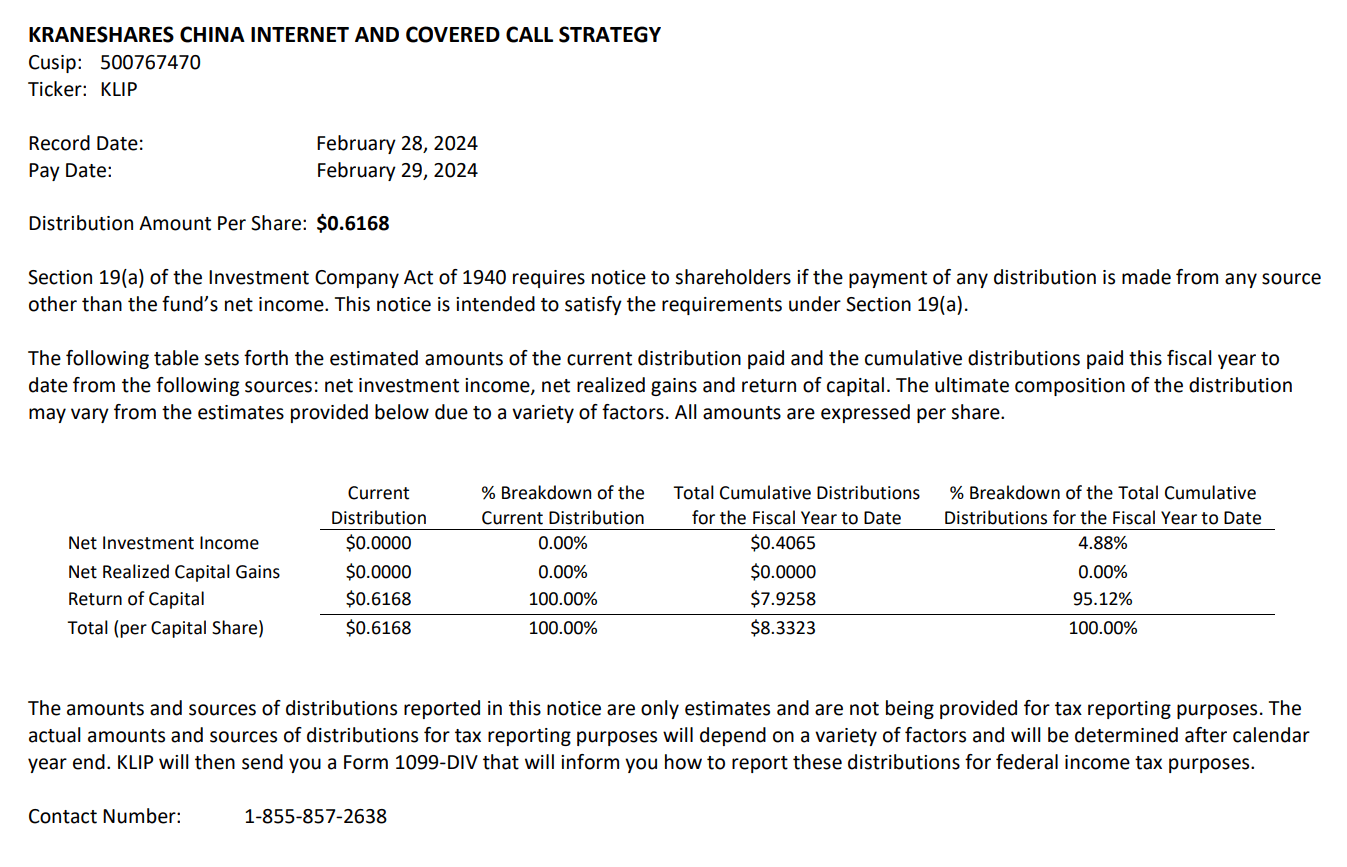

Heavy Use Of Return Of Capital

However, declines in the KWEB ETF does not explain all of KLIP’s NAV amortization, since KWEB only declined by 14.6% in the past year in price, but KLIP’s market price / NAV has declined by 34.1%.

What else could be the issue?

Looking through the fund’s literature, it appears another issue with the KLIP ETF is that 95% of the fund’s YTD distribution is estimated to be return of capital (“ROC”) (Figure 6). Return of capital means that the fund has been liquidating NAV to fund its distribution.

Figure 6 – KLIP distributions are mostly ROC (KLIP Section 19.a report)

While it is unclear why selling call options to generate option premium income is classified as ROC, for all intents and purposes, investors are just paid back their own capital, with not much real value created.

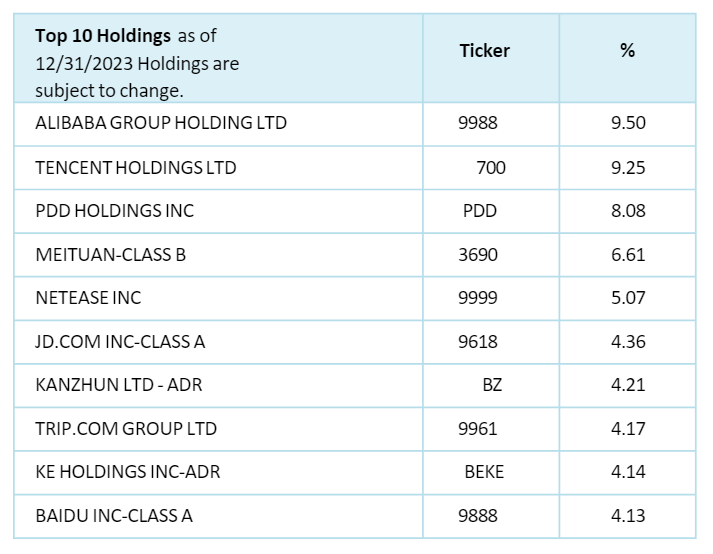

Geopolitical Risk Remains High

Looking at the underlying fund, KWEB, geopolitical risk remains top of mind as the KWEB ETF is filled with leading Chinese technology companies like Alibaba and Tencent (Figure 7).

Figure 7 – KWEB top 10 holdings (kraneshares.com)

In recent weeks, the U.S. House has voted for legislation that could ban the use of TikTok, a popular social media app that originated from China, unless its Chinese owners divest their holdings.

While the measure appears draconian, it does highlight the growing animosity between U.S. lawmakers and Chinese technology companies. It is therefore not unexpected that the KWEB ETF continues to underperform, declining by 13.2% in the past year and 3.4% YTD.

Conclusion

I believe my initial assessment on the KLIP ETF remains valid, as KLIP’s 61.7% distribution yield is too good to be true. Offsetting KLIP’s distribution has been a persistent NAV decline caused by declines in KWEB and also return of capital.

While it is unclear why selling call options will lead to distributions being deemed return of capital, it appears the fund is simply returning investors’ capital via the distribution and generates modest total returns. I continue to recommend investors avoid KLIP.

Q2 2024 Earnings Call Transcript")