Sundry Photography/iStock Editorial via Getty Images

Investment Thesis

Union Pacific Corporation (NYSE:UNP) is rated as a buy as operations improve. We believe the new management will continue implementing significant improvements that will enable UNP to unlock superior shareholder returns. Previous management delivered a poor multi-year operational performance and at its current valuation, UNP is a long-term buy.

Introduction

UNP is one of the Class 1 freight railroad companies in the United States. The company is 161 years old and its rail network covers 23 states. UNP’s rail network is below indicating good coverage across the U.S.

UNP Factbook

We strongly believe that UNP will embark on a multi-year period of improvements and growth unlocking shareholder returns. The main reason for this is twofold. Firstly, UNP appointed Jim Vena as the new CEO of the company effective August 2023. We think the new CEO is the right person to transform UNP into an efficient railway company unlocking shareholder returns. He has over 40 years of experience in the industry and knows UNP as he served as the UNP COO and advisor to the chairman in the past. Secondly, U.S. railways stand to benefit from several tailwinds. If management achieves operational improvements then the impact will be significant as they will be able to capitalise on these tailwinds. Tailwinds for the U.S. railway companies include the increased investments happening for the U.S. industries and the fact that railways are a form of greener transport when compared with alternatives such as truck deliveries. The U.S. investment cycle is driven by the onshoring of supply chains which will take significant investments to reverse the old trend of offshoring and the decarbonisation efforts from government and industry. A clear example of this is the recent infrastructure bill signed by the U.S. government of c.$1.2 trillion. A lot of these new investments and projects will need support from railways for transportation. In addition, given that businesses and society become more sensitive to the sustainability of goods we expect railways to gain market share from trucks for example. Railways are considered a greener alternative and with the limited additional investments needed to capitalise on this, we expect that their market share will increase over the years.

Hence, the key to superior shareholder returns is management’s ability to deliver. We talk about the early signs below.

Management and Operational Performance

Our opinion is that UNP’s old management has failed to unlock most of UNP’s value and as a result shareholder returns were below those of competitors.

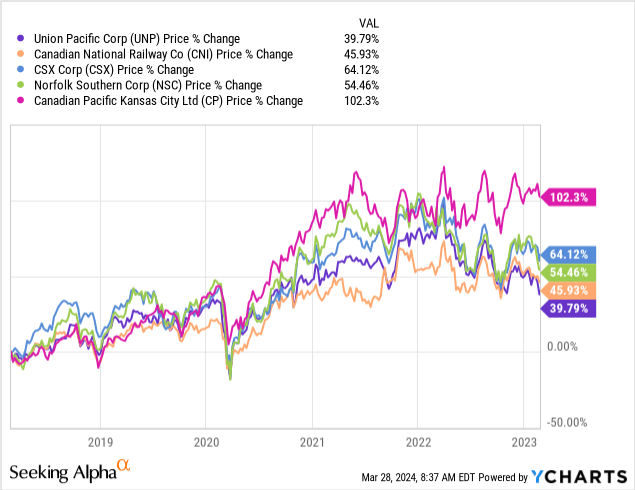

This is indicated by the chart below which is the 5-year chart up to 26 February 2023, the date when UNP announced that they are looking for a new CEO. As indicated below, UNP underperformed materially when compared with industry competitors.

As we mentioned above the new CEO was put in place effective 13 August 2023. Since then there have been a few key changes that we believe were important in setting up UNP to improve and unlock shareholder value.

To start with, the company appointed different people in the place of CEO and chairman of the board. Before Lance Fritz was filling both roles. The fact that a CEO is accountable to the board of directors and as a result, the chairman, means that having different people filling the different roles creates some accountability. Having the same person as the CEO and as a chairman means that companies can hand over too much influence on one person and remove accountability. Having these roles split means that the board of directors can focus on setting the right objectives and incentives for the CEO to ensure shareholder value is unlocked. Additionally, if a CEO is not performing well enough then the board of directors can more easily fire the CEO if they are not acting as the chairman of the board having significant influence.

Secondly, Jim Vena set up a new multi-year strategy tackling UNP’s problems. The strategy is “Safety + Service & Operational Excellence = Growth.” In the 2023 annual report, Jim Vena summarises the purpose of this strategy succinctly.

Safety is UNP’s first area of focus as it sets the right mindset, culture, and personal accountability. Service is the focus to deliver what promises have been made to customers and lastly, operational excellence is the ability to operate efficiently and productively. Achieving all three will lead to UNP growing its business and make UNP an industry leader unlocking superior shareholder returns.

Why is this important? Because the previous management failed to achieve these goals leading to inferior shareholder returns. Lance Fritz’s performance as a CEO was one of poor shareholder return, poor safety, poor revenue growth and poor cost management. UNP became the go-to railway company to highlight what not to do as a railway company. For example, in Q3 2023 UNP received a letter from regulators stating how unsafe the trains and the equipment used were.

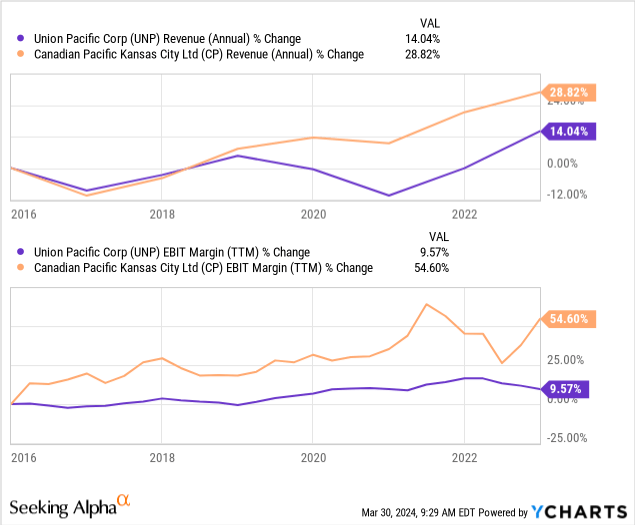

On the revenue and cost management performance side of things, we can compare UNP’s performance with Canadian Pacific Kansas City Limited (CP) which is a well-run railway company in our opinion. As we can see below since the appointment of Lance Fritz, CP had superior revenue growth and a better EBIT margin.

The question then becomes how is Jim Vena doing? We think there are already positive results appearing in the business results.

Firstly, let’s examine the weekly 2023 performance metrics data since Jim Vena took over relative to a year ago (we are comparing August to December 2023 with August to December 2022 average weekly data).

| New CEO | Old CEO | |

| Freight Car Velocity | 211 | 191 |

| Train Velocity (MPH) | 20 | 17 |

| Switch and Run-Through Car Dwell | 8 | 9 |

| Operating Car Inventory | 171,624 | 189,367 |

In all four of the metrics, Jim Vena has better performance relative to the performance under the old CEO. For freight car velocity and train velocity, higher figures are better and for switch and run-through car dwell and operating car inventory, lower figures are better.

If you are wondering what these metrics are we provide some explanations below. Definitions can also be found here.

Car Velocity: Measures the average daily miles a car moves. More miles mean better utilisation of freight cars.

Train Velocity: Measures the time from origin departure until final arrival, including time at intermediate terminals. More miles per hour means better utilisation of trains.

Switch & Run-through Car Dwell: Measures dwell in hours for any car classification or run-through train activity at a railroad station. The higher the figures the longer the dwell time and the lower the utilisation.

Operating Car Inventory: Daily snapshot of cars in normal movement, hold, or released at customer status. Indicates how well inventory is managed. If the number goes down it means that your inventory is managed more effectively.

These operational metric improvements are also present in the 2024 year-to-date data when compared with the equivalent period one year prior.

Operational improvements are also present in the Q4 2023 results. Quarterly freight car velocity saw a 14% year-on-year improvement. Quarterly locomotive productivity improved by 14% year on year. Average maximum train length saw a 2% year-on-year increase. Quarterly workforce productivity improved by 4% to 1,051 car miles per employee and lastly, the fuel consumption rate of 1.091, measured in gallons of fuel per thousand GTMs, deteriorated by 3% compared to a year ago. All of these performance metrics are moving towards the right direction and their continuous improvement will lead to superior shareholder returns.

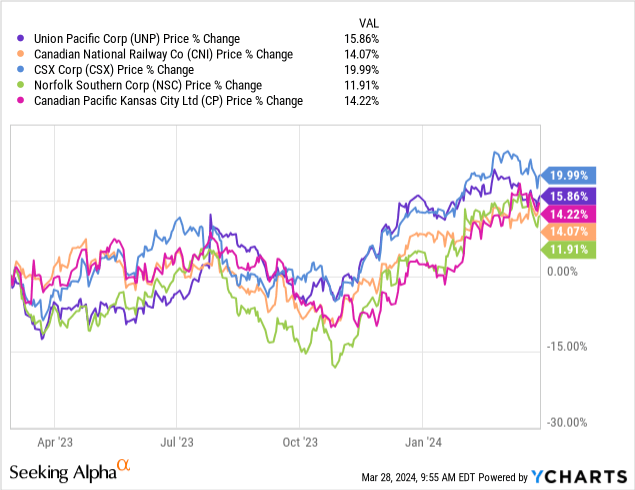

What about shareholder returns? The chart below starts from the period following the announcement of the old management stepping down. Since then UNP saw a stronger performance than most of its competitors. In addition, the spike in UNP’s stock price around the 26th of July is the impact of Jim Vena’s announcement as the new UNP CEO.

Overall during their first months, it is clear that the new management is taking the correct actions to improve UNP’s operational performance. In our opinion, if management continues to incrementally improve UNP’s operational performance and achieves industry-leading metrics shareholders will benefit from superior returns. Small incremental improvements over a long period will have a significant impact on the business.

Relative Valuation

Below we look at UNP’s relative valuation compared to Canadian National Railway Company (CNI), CSX Corporation (CSX), Norfolk Southern Corporation (NSC) and Canadian Pacific Kansas City Limited (CP).

| UNP | CNI | CSX | NSC | CP | |

| P/E fwd | 21.9 | 22.4 | 18.7 | 20.9 | 28.3 |

| P/Cash flow fwd | 15.8 | 15.0 | 12.3 | 13.1 | 19.0 |

| EV/EBIT fwd | 18.6 | 18.8 | 15.7 | 17.4 | 23.2 |

| Operating ratio Q4 23 % | 60.9 | 59.3 | 64.1 | 68.8 | 58.7 |

As we can see above UNP sits in the middle of the valuation range, with CSX being the relatively cheaper option and CP the most expensive one based on valuation multiples. On a relative valuation basis, UNP seems to be fairly valued.

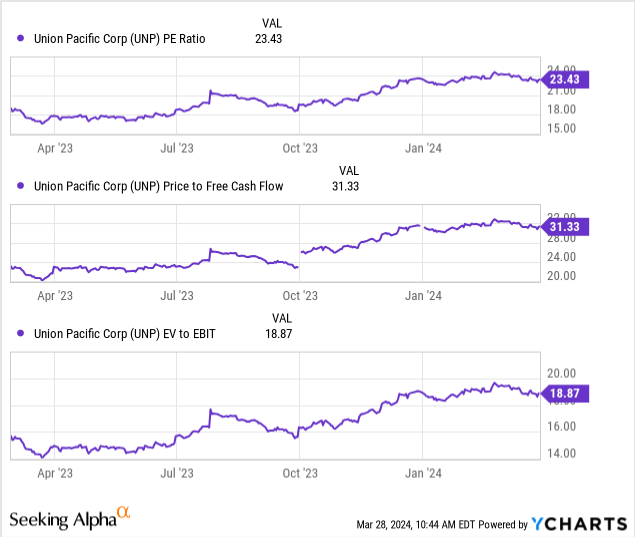

Secondly, let us look at the absolute valuation multiples since the old management announced they would be stepping down.

As we can see from the charts above on an absolute basis all valuation multiples have expanded since February 2023. More specifically, the price-to-earnings ratio rose by 24%, the price-to-free cash flow ratio increased by 36% and the enterprise value to earnings before interest and tax increased by 20%. Even though these multiples have expanded over the last year if UNP achieves industry-leading operational performance we believe that multiples will expand further.

If management can improve its operating ratio (operating expenses divided by revenue) closer to the CP’s operating ratio we expect valuation multiples to further improve closer to CP’s ratios.

This goes back to the importance that management will play in unlocking shareholder value. Incremental improvements over a long period will lead to higher profitability, higher valuation multiples and higher shareholder returns.

Risks

As we discussed above our thesis is focused on management unlocking superior shareholder returns. New management has demonstrated early on that they can improve the company’s operations. The first signs are encouraging, however, there is the risk that management will fail to deliver meaningful and additional improvements. Given that on a relative valuation basis UNP seems to be in the middle of the range, operational improvements are key to unlock superior returns. These early positive operational performance signs might be down to poor luck. Operational performance needs to be monitored for longer to declare victory by management. In addition, UNP’s business is sensitive to the economic cycles. If the economy enters into a hard recession economic activity will likely decline which will impact demand and hence the business as a whole. No management improvements will lead to superior shareholder returns if the economy enters into a recession.

Conclusion

The new management has provided early signs that it can improve UNP’s operational performance. Improving their performance over time will enable them to become an industry leader and capitalise on the tailwinds we discussed above. On a relative basis, UNP is at the middle of the valuation multiple range. Hence, management needs to continue to operationally improve the performance of the company. We believe over the longer term management will continue to achieve meaningful improvements that will translate to superior shareholder returns. We rate UNP as a long-term buy.

Q2 2024 Earnings Call Transcript")