isayildiz/E+ via Getty Images

Investment Thesis

Shift4 (NYSE:FOUR) presents an intriguing investment opportunity supported by its strong financial performance, innovative solutions, and strategic acquisitions. With a solid track record of revenue growth, margin expansion, and efficient cost management, Shift4 is well-positioned for sustained growth of 29.6% in the next 3 years in the dynamic payment processing landscape. I believe Shift4 is priced at a premium for good reasons, and therefore, I rate it as a buy.

About Shift4

Shift4 is a payment software company that generates revenues in 2 ways:

-

Facilitates payment for merchants across a range of sectors including restaurants, casinos, and hotels, to sports teams. This makes up the bulk of its revenues.

-

Charges a monthly subscription fee to merchants for using Shift4’s POS system

Financials

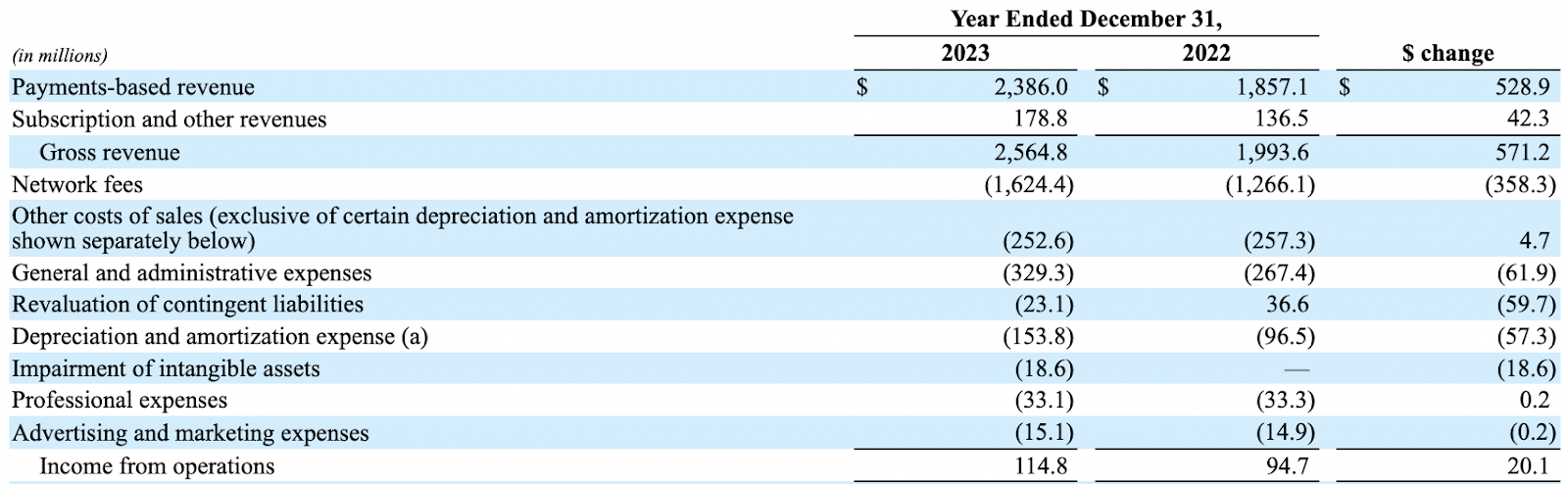

FY23 10-K FY23 10-K

In FY23, Shift4’s end-to-end payment volume grew 52.3% YoY to $109 billion, highlighting the increased merchant adoption of its payment processing solution. In particular, during the 4Q23 earnings call, management has reported enterprise wins spanning multiple sectors including sports and entertainment, hotel and resort, and as well as major sports team and entertainment venues. This helped drive a higher volume of payment processed on Shift’s platform, and as a result, payment-based revenue grew 28.5% YoY to $2.4 billion.

Moreover, Shift4’s recent acquisitions of Appetize and Finaro have demonstrated successful integrations and realized synergies. Appetize was strategically acquired by Shift4 to enhance its presence in the sports and entertainment industry. Currently, Shift4 provides mobile commerce, point-of-sale (POS), and loyalty solutions to clients in this sector through its VenueNext Technology. The integration of Appetize’s payment software solution with VenueNext strengthens Shift4’s foothold in the sports and entertainment vertical, enabling a wider array of services and solutions. Whereas, the acquisition of Finaro aimed to expand Shift4’s presence in European markets.

On the other hand, FY23 subscription revenue grew 30.9% YoY to $178 million, fueled by the strong adoption of its SkyTab POS system, which according to management, they have installed over 25,000 systems in 2023. SkyTab is a next-gen POS system launched in Nov 2022, and by migrating customers over from its legacy POS system, they are now reporting a higher ARPU. Going towards 2024, management aimed to have 30,000 systems installed in the U.S. alone and 10,000 systems in Europe and Canada.

Overall, Shift4 experienced robust growth, with total revenue surging by 28.7% YoY to reach $2.6 billion. More impressively, gross profit soared by 46.3% YoY to $687.8 million — outpacing revenue growth, leading to a notable expansion in gross margin from 23.6% in FY22 to 26.8% in FY23. This remarkable achievement underscores Shift4’s exceptional efficiency in managing its costs, ultimately strengthening its profitability.

Profitability

FY23 10-K

FY23’s EBIT grew 21.7% — at a growth rate slower than the revenue growth. This resulted in EBIT margin falling from 4.75% in FY22 to 4.48% in FY23. However, if we exclude the non-recurring impairment of intangible assets of $18.6 million that was incurred in 4Q23 due to the cease of certain in–house projects, FY23 EBIT would have amounted to $133 million, growing 40% YoY and the margin would be 5.20%. This shows that the firm is demonstrating operating leverage, resulting in margin expansion.

Further Expansion in ARPU and Expectations of Near 30% Revenue Growth for the Next 3 Years

Looking ahead, the recent acquisition of Appetize not only opens doors to new market segments for Shift4 but also propels ARPU growth through increased upselling and cross-selling opportunities among the combined customer base. The primary driver of ARPU enhancement lies in the widespread adoption of Shift4’s payment solutions. As customers embrace more of Shift4’s offerings, ARPU naturally rises, increasing customer stickiness and better unit economics overall.

3 Year Revenue Growth

Based on management’s FY24 lower-end guidance of $1.3 billion gross revenue, Shift4’s current growth trajectory suggests a high likelihood of achieving its targeted near 30% growth over the next 3 years, assuming the annual revenue increment remains consistent. Assuming OpEx remains stable, this growth trajectory indicates potential margin expansion as we move into FY26.

Balance Sheet

On its balance sheet, as of FY23, Shift4 has $721.8 million in cash alongside a long-term debt of $1.7 billion. To gauge its capacity to manage this debt, we have to evaluate its cash flow statement. In FY23, Shift4 had recorded a positive cash flow of $388.3 million. Given the significant cash reserves held, this underscores Shift4’s ability to comfortably service its debt obligations while concurrently fueling its growth initiatives.

Valuation

Author’s Valuation

When assessing Shift4’s valuation, utilizing the EV/Sales metric provides a more suitable comparison, particularly considering that many of its peers are currently unprofitable. Notably, Shift4 commands a premium compared to its peers, except Toast. However, this valuation could be justified as Shift4 has demonstrated self-sustainability, a higher growth rate, and improved margins. These factors underscore the operational efficiency and scalability inherent in Shift4’s business model.

Risks

Some risks include:

-

The highly competitive payment processing industry could erode Shift4’s ability to compete for market share

-

Macroeconomic factors that could impact consumer spending patterns.

-

Challenges in integrating acquired companies, systems, and cultures could disrupt operations and impact financial performance

Conclusion

In conclusion, Shift4 demonstrates a robust financial performance, driven by its innovative payment processing solutions and strategic acquisitions. With significant growth in both end-to-end payment volume and subscription revenue, the company has solidified its position in various sectors, including sports and entertainment, hospitality, and retail. Notably, Shift4’s efficient cost management is evidenced by its remarkable expansion in gross profit and margin. Looking ahead, the company’s continued focus on margin improvement, coupled with its strong balance sheet and positive cash flow, positions it well for sustained growth of 29.6% in the next 3 years. Finally, I believe Shift4’s valuation is justified for above reasons, and therefore, i rate it a buy.

Q2 2024 Earnings Call Transcript")