da-kuk

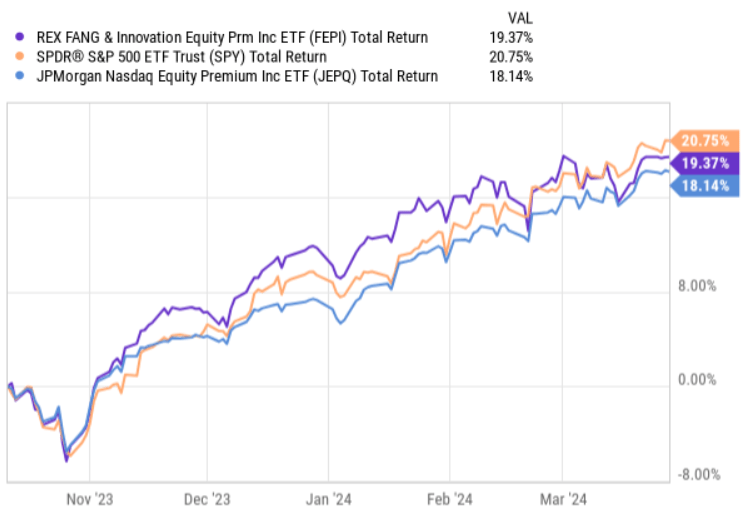

REX FANG & Innovation Equity Premium Income ETF (NASDAQ:NASDAQ:FEPI) is a relatively fresh covered call ETF that was established back in November, 2023.

Since the inception, it has managed to keep up with the well-performing S&P 500 delivering attractive distribution income from the written options.

Ycharts

During this time period, FEPI has even slightly outperformed the more popular JPMorgan Nasdaq Equity Premium Income ETF (NASDAQ:JEPQ), which carries some features that correlate with those of FEPI.

Even though we do not have much to assess from the FEPI’s historical data given its recent inception date, we can still take a look at the underlying mechanics of FEPI and see how the ETF could fit into investor portfolios.

The structure

At its core, FEPI is a conventional covered call ETF, which tracks a selected universe of stocks, while selling out of the money calls to capture income.

The expense ratio is at 0.65%, which is more or less in line with what we can find in the overall covered call ETF space. It is not cheap nor is it expensive.

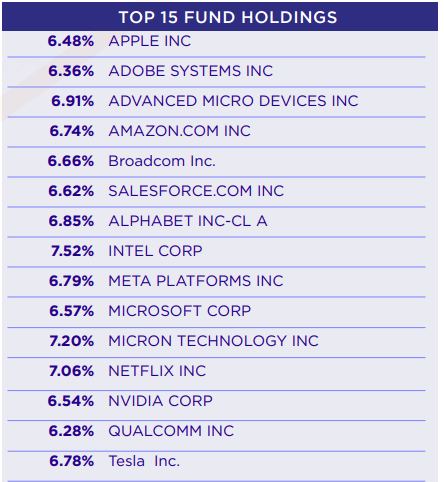

What is rather FEPI specific is the sample of stocks it tracks or holds as the underlying investments against which the calls are sold. The exposure here is mostly in the leading tech firms that constitute notable share of the S&P 500 and the Nasdaq 100.

FEPI fact sheet

As we can see in the chart above, the Top 15 (which is comprised of large-cap tech companies) explain the entire holdings base of FEPI.

Moreover, it is worth underscoring the distribution among these Top 15 names. Opposite to most other covered call ETFs like JEPQ or popular indices such as the S&P 500 and the Nasdaq 100, FEPI’s portfolio is structured on an equal-weight basis, thereby avoiding excessive concentration in couple of companies that have exhibited strong momentum in their market cap levels.

In terms of the covered call programme, there is nothing that deviates from the traditional approach within other similar ETF vehicles:

- Duration of written calls is usually bound by 30 days.

- FEPI does not sell in the money or at the money calls.

- The call strikes are usually relatively far from the underlying stock price (albeit, the Management has the luxury to maneuver here by assuming tactical bets depending on the market conditions and the overall opportunity).

Thesis

Now, once we have established a basis (i.e., how FEPI is structured and how the risk and return drivers look like), I will elaborate on two distinct advantages of FEPI that could motivate investors going long the ETF.

The first one is the enhanced yield potential, which stems from the relatively concentrated positions in only 15 companies.

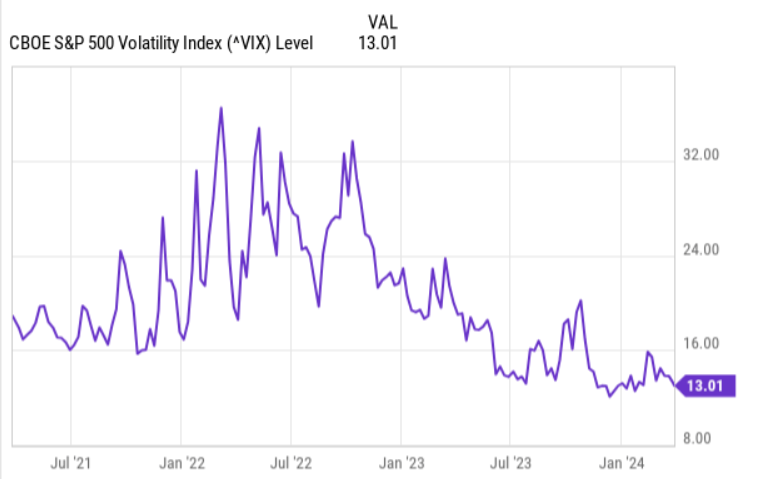

The way how covered call ETFs can distribute enticing income, while not divesting the underlying NAV base is through option-writing. The higher the price of option, the higher the received income that can be then paid out to unit holders. One of the fundamental drivers of option price is the implied volatility level. Namely, the more volatile the stock is against which the call is sold, the higher premium can be pocketed by the ETF.

Currently, the overall volatility levels are depressed, rendering covered call strategies less attractive across the board.

Ycharts

However, if we look at FEPI’s distribution yield, it is still in the double digit territory at ~ 10.6%.

So, in FEPI’s case there are two specific drivers that provide a direct support for the yield-generation:

- FEPI does not sell calls against a broad index, which per definition is less volatile than individual stocks or an index that is constituted of a small sample of stocks. Hence, by having fewer positions based on which the calls are written, the implied volatility levels are oftentimes higher than in usual situations / covered call ETFs.

- The stocks themselves that are tracked by FEPI are quite volatile and given the tech-focus are also strongly correlated that, again, is supportive of capturing higher volatility.

For example, if we compare JEPQ with FEPI, we will notice that the latter is able to offer positive spread in yield of ~ 170 basis points.

With that being said, carrying a more concentrated exposure comes with some additional risks as well. While the yield might be higher, the sensitivity to major price corrections in the FEPI’s holding companies (or even a single company) can cause the ETF to decrease accordingly.

The second one is related to the skew towards Magnificent 7 companies that have really driven the stock market for quite some while. As we know, if one adjusted for the Magnificent 7, the overall stock market would be in a completely different zone (i.e., nowhere near the all time highs).

Here it boils down to investors’ subjective views as to whether these same individual stocks will manage to maintain the assumed momentum, thereby pushing the stock market to incremental highs. If this is the case, and, even more, if the gains take place in a constant and gradual fashion, FEPI will be the clear beneficiary.

Conversely, if the small-cap factor suddenly comes back into vogue, while the large cap names stagnate or drop due to optically stretched multiples, FEPI will suffer accordingly. Granted, there is some embedded protection in the form of call premiums, but in the scenario of really large drawdowns this will not move the needle.

The bottom line

In my opinion, FEPI presents an interesting opportunity, where investors can isolate booming tech exposure, while extracting most of the gains in the form of attractive current income. At the same time, by going long FEPI, investors can obtain some layer of downside protection due to the inherent covered call programme, where the pocketed premiums can partially compensate the loss from price depreciation in the underlying portfolio.

Having said that, there are also some clear risks. The most notable, in my opinion, is the opportunity cost of not fully participating in the continued gains of the Magnificent 7 names. While there is some distance between the underlying price and option strike price, it is not that meaningful since FEPI has to concentrate on yield generation.

The scenario in which FEPI would thrive has to be associated with an gradual uptick in large-cap and tech-related companies as in this case, no major opportunity cost is incurred and the investors can safely capture the above average yield due to higher vol options.

For me FEPI is a hold.

Q2 2024 Earnings Call Transcript")