M-image/iStock via Getty Images

It has been over a year since my last Xeris Biopharma (NASDAQ:XERS) article, where I reviewed the company’s 2022 achievements including record net product revenue, driven by robust growth in our approved product portfolio. In addition, I also pointed out that company management was confident in their trajectory toward cash flow breakeven by the end of 2023. At that time, XERS was trading near $1.25 per share with a market cap of approximately $189M, I observed a notable disparity between the stock’s valuation and its growth potential. As a result, I stood firm with the choice to keep XERS as a “Top Idea” in the my Seeking Alpha Investing Group and discussed my plans for 2023. Well, my plan has been a partial success by grabbing some XERS shares around $1.15 per share back in March of last year… but that was my last XERS transaction. Unfortunately, despite significant growth, the company has not hit breakeven as Keveyis deals with generics. Xeris may no longer be worthy of a “Top Idea” designation.

I intend to provide a brief background on Xeris and will take a look at the company’s recent performance. Then, I will point out some of the primary growth drivers that could move them closer to breakeven. In addition, I point out some risks that XERS investors should consider when managing their position. Finally, I debate whether XERS is still a “Top Idea” and deliberate on my plans for managing my XERS position as we head deeper into 2024.

Recap On Xeris Biopharma

Xeris Biopharma is a biotech firm committed to revolutionizing the treatment of diseases in endocrinology and neurology. The company’s innovative formulation technologies are intended to improve patient outcomes and quality of life. Xeris is centered on its proprietary XeriSol and XeriJect technologies, which have generated several candidates with formulations of ready-to-use, liquid-stable injectables of peptides, proteins, antibodies, and small molecules. XeriSol enhances the stability, solubility, and bioavailability of a multitude of therapeutics, while XeriJect safeguards accurate and expedient formulations for use in auto-injectors and infusion pumps.

Currently, Xeris boasts three approved products in the United States and one in Europe. One of its flagship products, Gvoke, offers a ready-to-use liquid glucagon solution for severe hypoglycemia, available in three different formats: Gvoke HypoPen, Gvoke PFS, and Gvoke Kit. Gvoke is also marketed in Europe under the name Ogluo. Additionally, Xeris acquired two other approved products, Keveyis for primary periodic paralysis, and Recorlev for endogenous Cushing’s syndrome, through its merger with Strongbridge.

Xeris Biopharma Products (Xeris Biopharma)

In addition to its existing product portfolio, Xeris maintains an active pipeline of development programs utilizing its XeriSol and XeriJect platforms.

Following its merger with Strongbridge, Xeris is showing promising momentum, particularly with Recorlev and Keveyis demonstrating strong growth, and Gvoke gaining traction in the market.

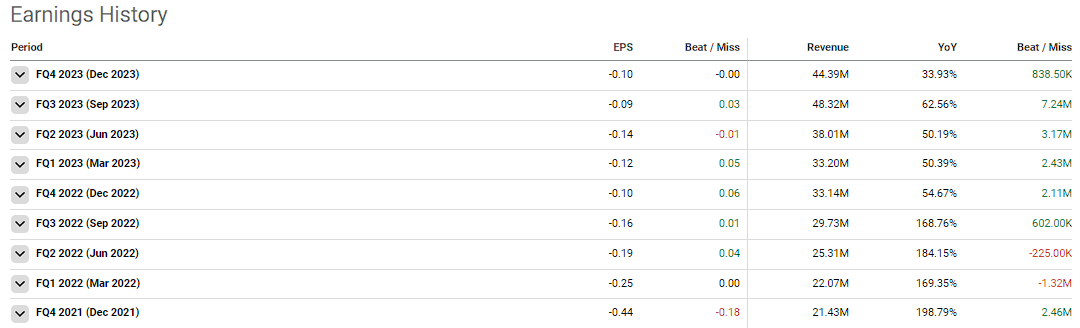

Xeris Biopharma Earnings History (Seeking Alpha)

In fact, in Q4 of 2023, Xeris achieved total revenue exceeding $44M, marking a significant 34% bump over Q4 2022. Commercial highlights for the fourth quarter include significant growth in product revenue across Gvoke, and Recorlev, with Gvoke prescriptions exceeding 59K for the first time. Furthermore, for the full year of 2023, the company recorded about $164M in total revenue, representing an eye-catching 49% increase over the prior year. At the end of 2023, Xeris had over $72M in cash, cash equivalents, and short-term investments. Notably, the company achieved a positive cash flow of over $6M in the fourth quarter.

Xeris anticipates continuing their success in 2024 with “total revenue in the range of $170 million to $200 million” and expects to “end 2024 with a very healthy cash position of $55 million to $75 million.” Although going from $164M in 2023 to $170M-$200M in 2024 is not a breakneck growth rate, I must point out that the growth is from the company’s currently approved products. Therefore, the growth is likely to come from additional market penetration.

Growth Drivers

Several factors strengthen Xeris Biopharma’s growth trajectory in the both near term and long term. First, the successful commercialization of Xeris; products will likely facilitate additional market penetration into underserved patient populations, establishing Xeris as a prominent player in diabetes and chronic disease management.

Second, the company’s formulations hold colossal potential in numerous therapeutic indications, comprising diabetes, epilepsy, and other endocrine and neurological disorders. Notably, the company’s XeriSol levothyroxine candidate (XP-8121) is moving through Phase II, with data expected in mid-2024. With a growing prevalence of these conditions globally, combined with increasing demand for advanced therapies, Xeris should benefit from being one of a few players in these arenas offering specialized products.

Third, Xeris has ample opportunities to broaden its product portfolio and penetrate new markets, driving revenue diversification and growth. This can be compounded by pushing partner programs, which can provide significant revenue and improve a product’s likelihood of being a success.

Notable Risks

Even though XERS is identified as a “Top Idea” within my speculative portfolio Seeking Alpha Investing Group, it brings along hallmark risks seen in the small-cap biotech industry. Primarily, clinical development risks efficacy, safety, and regulatory approval. These pose significant risks to the candidate, as well as other pipeline candidates that utilize the same technology. An issue with a Xeriject or Xerisol candidate or product could create some uncertainty around the other related pipeline programs.

Another concern is the intense competition within the company’s markets from some of the biggest healthcare companies in the world, which may impede market share expansion and revenue growth. Xeris Biopharma’s primary competitors include Novo Nordisk (NVO), Eli Lilly (LLY), Sanofi (SNY), and Aquestive Therapeutics, among others.

It’s important to recognize that not every product in Xeris’ portfolio holds a promising outlook. With the FDA greenlighting a generic version of Keveyis (dichlorphenamide), the product faces imminent competition, potentially leading to a decline in sales. Keveyis pulled in a little over $14M in Q4, which was only up roughly 1.9% year-over-year and down 11% from Q3 of 2023. While the company may still report respectable revenue from Keveyis, declining sales seem inevitable in the near term.

Finally, Xeris continues to consume cash at a high rate with cash utilization for 2023 at $49.5M. Indeed, that is a significant decrease in cash burn over 2022’s cash utilization of more than $100M, and they project to finish 2024 with $55M-$75M in cash. However, I must point out that the company finished 2023 with about $72.5M in cash, and they are adding roughly $35M from the refinance in the first quarter. So, they are working with about $107.5M cash during 2024, and expected to leave 2024 with $55M-$75M, meaning $32.5M-$52.5M in cash burn. Essentially, Xeris might report a bump or slight decrease in cash utilization this year. Assuming the company’s cash burn rate remains the same, the company should have enough cash to last into 2026. Although Xeris should continue to report revenue growth and reduce cash burn in the coming years, investors should acknowledge their is a possibility Xeris will need perform some dilutive funding. As a result, the market will likely undervalue the stock until the company reports positive earnings per share.

While these risks may not pose significant threats to the company’s business, they can certainly impact the share price, potentially causing frustration for investors given the company’s positive fundamental outlook. From a personal perspective, my focus remains on the long-term trend, leading to a conviction level of 3 out of 5 for XERS.

XERS Still A “Top Idea”?

Despite inherent risks and competitive pressures, Xeris Biopharma’s long-term outlook remains promising. The company has an innovative platform technology along with three approved products. Furthermore, Xeris has a robust pipeline and strategic initiatives in place that have positioned them for additional growth and value creation in the coming years.

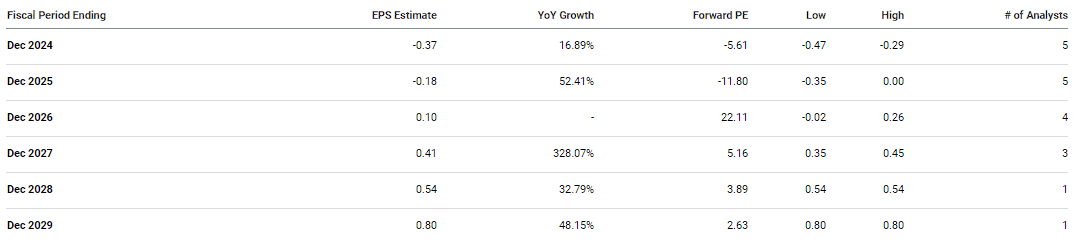

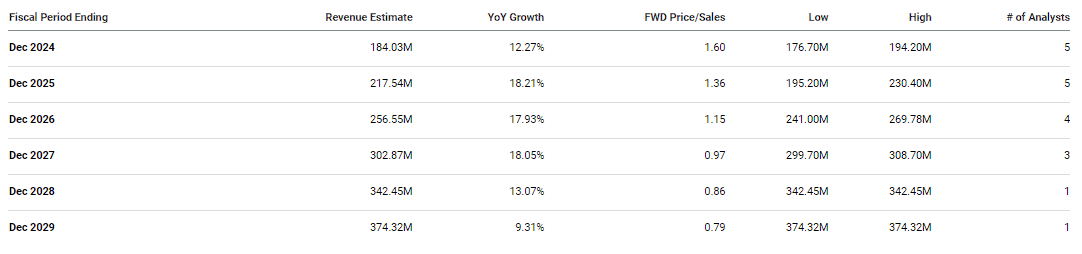

The Street expects Xeris to report double-digit growth for EPS and revenue for the remainder of the decade.

Xeris Biopharma EPS Estimates (Seeking Alpha) Xeris Biopharma Revenue Estimates (Seeking Alpha)

It looks as if analysts are projecting Xeris to report roughly $374M in revenue in 2029, which would be a forward price-to-sales of around 0.79x. Considering the industry’s average price-to-sales is 4x-5x, we can say XERS is trading at a discount for its estimated revenue growth. In fact, XERS is trading at roughly 1.6x for its estimated 2024 revenue… so, it is trading at a significant discount for 2024 estimates, and an absurd discount for its projected growth. Indeed, we don’t know if Xeris will hit these estimates, and the company will likely have to resort to some dilutive funding in the future. However, one must say that the ticker offers an enticing risk-reward profile at these levels, which is a key characteristic of a “Top Idea” in my speculative portfolio.

Certainly, we must consider the risks that I have discussed above, but most of those concerns are proposed and are not inevitable. If I look at the company’s current status…

Xeris achieved a total revenue exceeding $44M in Q4, indicating a significant 34% rise versus Q4 of 2022. Throughout the entirety of 2023, Xeris pulled in approximately $164M in revenue, showcasing an impressive 49% increase from the prior year. Plus, they closed out the year with more than $72M in cash, cash equivalents, and short-term investments and refinanced Hayfin’s term loan, resulting in a lower overall cost of capital and additional capital. Additionally, the company secured a global license agreement for the XeriJect formulation of teprotumumab with Amgen (AMGN) for thyroid eye disease. Lastly, the company’s full-year 2024 guidance has them achieving total net revenue to fall between $170M to $200M with a year-end cash position between $55M and $75M.

To recap, Xeris Biopharma recorded growth, secured more funding, finalized deals, and issued strong guidance. Furthermore, even with Keveyis generics on the market for a whole year, Xeris retained over 90% of their patients. So, for me,

Considering these points, I am keeping XERS as a “Top Idea” in my speculative portfolio for the foreseeable future.

My Plan

In my last XERS article, I revealed that I was adopting a patient stance, awaiting a strong reversal pattern coupled with multiple bullish indicators before considering further increases in position size. I planned to make periodic buy orders below my Buy Target 1 of $1.56, with the expectation of several small increments before the end of 2023, and swiftly transition my XERS position into a “house money” status. Well, I only made one major addition last year following that article, and the ticker failed to hit my targets at around $5 and $7 per share.

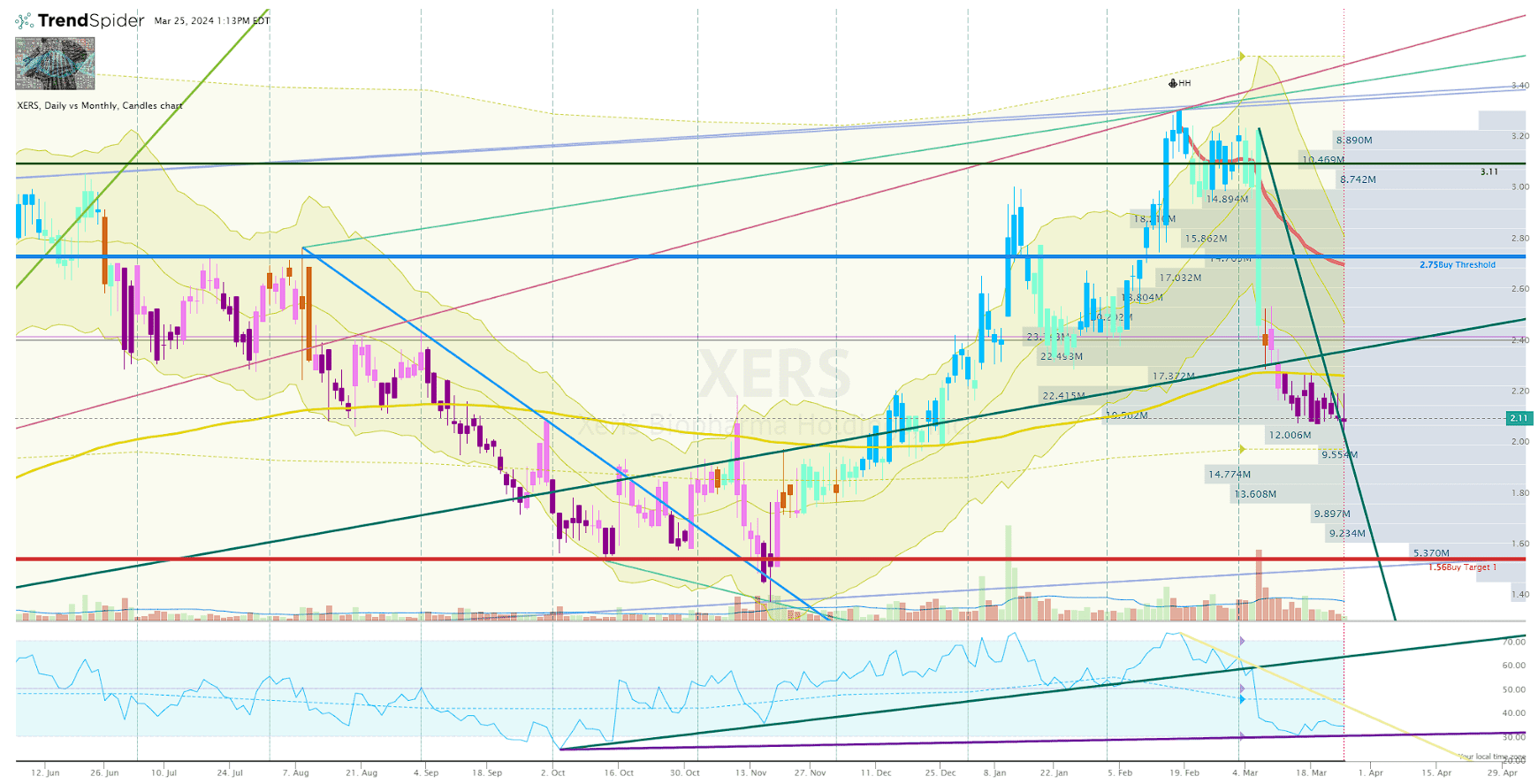

At the moment, XERS is trading below my Buy Threshold of $2.74 per share, so I am looking to make another addition at some point. Looking at the Daily Chart, we can see that XERS is below the 200-EMA and shows very bearish on the Go-No-Go indicator. In addition, I don’t see any signs of an uptrend ray starting to provide support for a potential reversal.

XERS Daily Chart (Trendspider)

Therefore, I am sitting on my hands until I see a high conviction reversal setup, or perhaps I will wait for a sign of “seller exhaustion.” Once I see a few bullish signals, I will not hesitate to add to this position.

In the long term, XERS is still poised to become a significant component of my speculative portfolio. I plan to trade the stock for at least another five years, gradually building a “house money” position to hopefully integrate into my growth-oriented portfolio one day.

Q2 2024 Earnings Call Transcript")