The exterior of a TD Bank building. Marvin Samuel Tolentino Pineda/iStock Editorial via Getty Images

All else equal, I especially prefer to invest in businesses with demonstrable track records as dividend payers. The longer the dividend-paying streak that a company possesses, the more it catches my attention.

In my opinion, there is no greater commitment to shareholders that a company can exhibit than maintaining and/or growing dividends for decades or even centuries.

This is why the major Canadian banks especially stand out to me as interesting options for reliable income. Last week, I took another look at Scotiabank (BNS).

Today, I’m going to be highlighting its larger peer, The Toronto-Dominion Bank (NYSE:TD), and why I am initiating coverage with a buy rating.

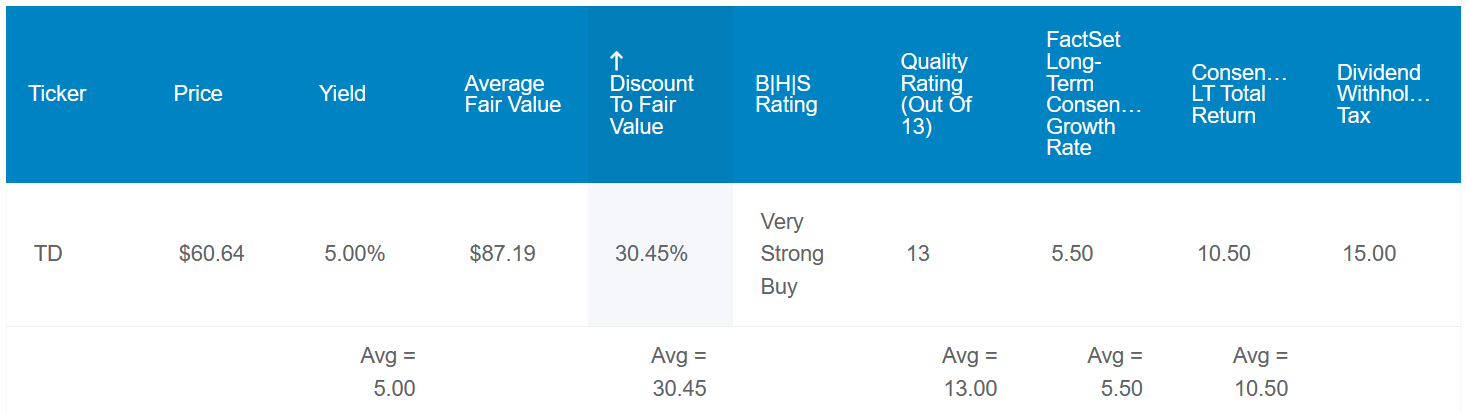

Dividend Kings Zen Research Terminal

TD’s 5% forward dividend yield is markedly higher than the financial sector’s 3.4% median forward dividend yield. This is why Seeking Alpha’s Quant System awards a B+ grade to the company on forward dividend yield. Additionally, the company’s dividend payment streak (more on that later) is enough to earn an A grade on dividend consistency from the Quant System.

TD’s 51% EPS payout ratio is roughly in line with the 50% EPS payout ratio that rating agencies prefer from the banking industry.

The company’s leadership in the consolidated Canadian banking industry and robust financials have allowed it to secure an AA- credit rating from S&P on a stable outlook. This implies the probability of TD going to zero over the next 30 years is 0.55%. In other words, the company would remain in business in 181 out of 182 30-year simulations.

For these reasons, the likelihood of a dividend cut in the next average recession is 0.5% in the Zen Research Terminal. This would grow to 2% in the next severe recession. For context, these are both the lowest values possible within the Zen Research Terminal.

Dividend Kings Zen Research Terminal

If TD’s promising fundamentals weren’t enough, the stock also looks to be a solid value here. Its five-year average dividend yield of 4.1% according to Dividend Kings’ Automated Investment Decision Bot could suggest shares are worth $73 each. Since the company’s fundamentals appear to be intact, I don’t think it’s unreasonable to anticipate an eventual reversion to this dividend yield.

My inputs into the dividend discount model show shares to be worth $76 apiece: A $3.026 annualized dividend per share (annualizing the last two dividend payments), a 10% discount rate, and a 6% annual dividend growth rate (more to come on why I am using this as the DGR).

Averaging out the Zen Research Terminal’s overall fair value of $87 with my $76 fair value, this would be an average fair value of $81 a share. That could mean shares are priced 26% below fair value from the current $60 share price (as of March 28, 2024).

If TD meets the growth consensus and returns to fair value, here are the total returns that could be in store for the coming 10 years:

- 5% yield + 5.5% FactSet Research annual growth consensus + a 3% annual valuation multiple upside = 13.5% annual total return potential or a 255% 10-year cumulative total return versus the 9.8% annual total return potential of the S&P 500 (SP500) or a 155% 10-year cumulative total return

TD Is A Financial Juggernaut

Since its formation in 1855, TD has grown from a single bank branch location serving grain millers and merchants, to a dominant financial services company. As of Jan. 31, TD’s more than 2,200 retail banking locations were entrusted with 1.9 trillion CAD in total assets by over 27 million customers (info sourced from TD’s Q1 2024 Quick Facts PDF).

TD Bank Q1 2024 Investor Presentation

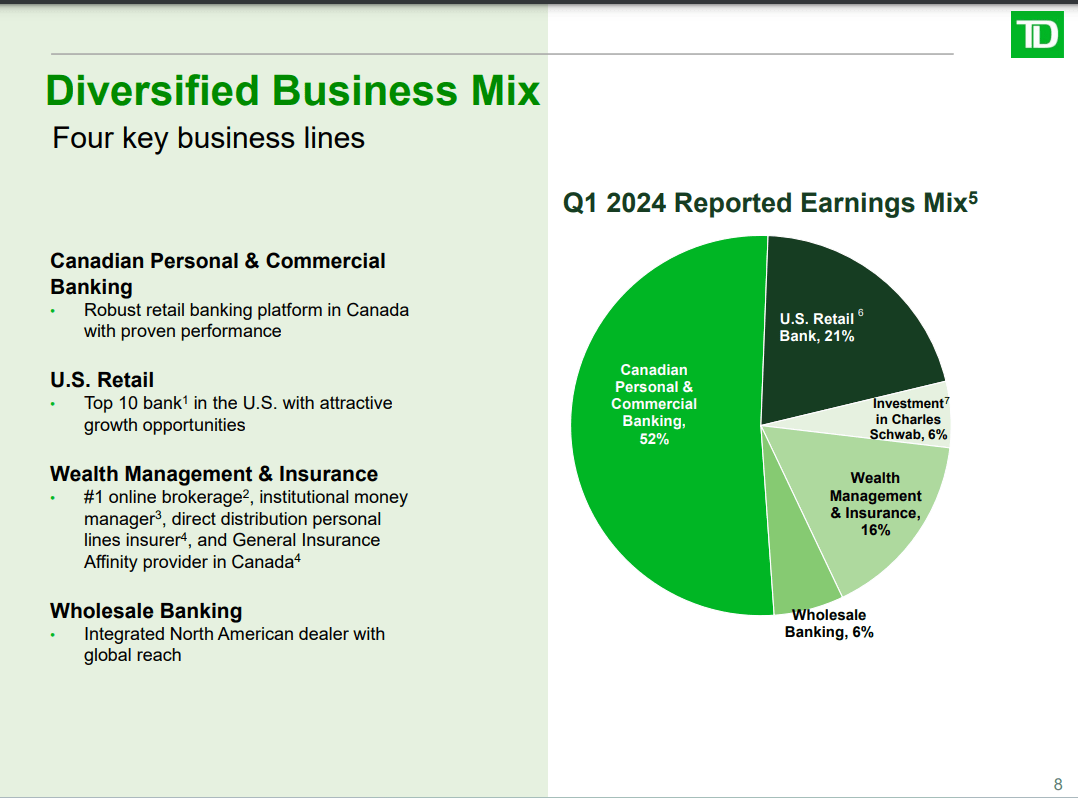

In recent years, TD has undergone a steady transformation from merely a bank into a holistic financial services company. In its fiscal year 2018, the company’s Canadian Retail and U.S. Retail banking segments made up 86% of its reported earnings mix (per slide 9 of 34 of TD Bank’s Q1 2019 Investor Presentation). That has since come down to a combined 79% as of Q1 2024.

The company also owns an approximately 12% stake in Charles Schwab (SCHW) as of Jan. 31. This made up another 6% of its earnings mix in Q1 2024 and is part of the U.S. Retail banking segment.

Geography aside, these segments provide products to consumers like mortgages, auto loans, and credit cards. Other products include savings accounts, checking accounts, certificates of deposit, and small business banking.

TD has been leaning into wealth management and insurance as of late. The Wealth Management & Insurance segment made up 16% of its earnings mix in Q1 2024. That includes estate and trust planning annuity products, insurance products, and asset management services.

Lastly, the company’s Wholesale Banking segment comprised the remaining 6% of its earnings mix in Q1 2024. This business serves over 17,000 corporate, government, and institutional clients in financial markets around the world. Any time a corporate, governmental, or institutional client needs capital, the company’s capital market and investment banking services can meet their needs.

Despite TD’s continued efforts to branch out, this hasn’t hurt the direction of the company. Its total assets are up nearly 50% from 1.3 trillion CAD in 2018. This means that throughout this time, the company has maintained its ranking of being the sixth-largest North American bank by assets.

TD Bank Q1 2024 Investor Presentation

Moving forward, the outlook for TD remains promising.

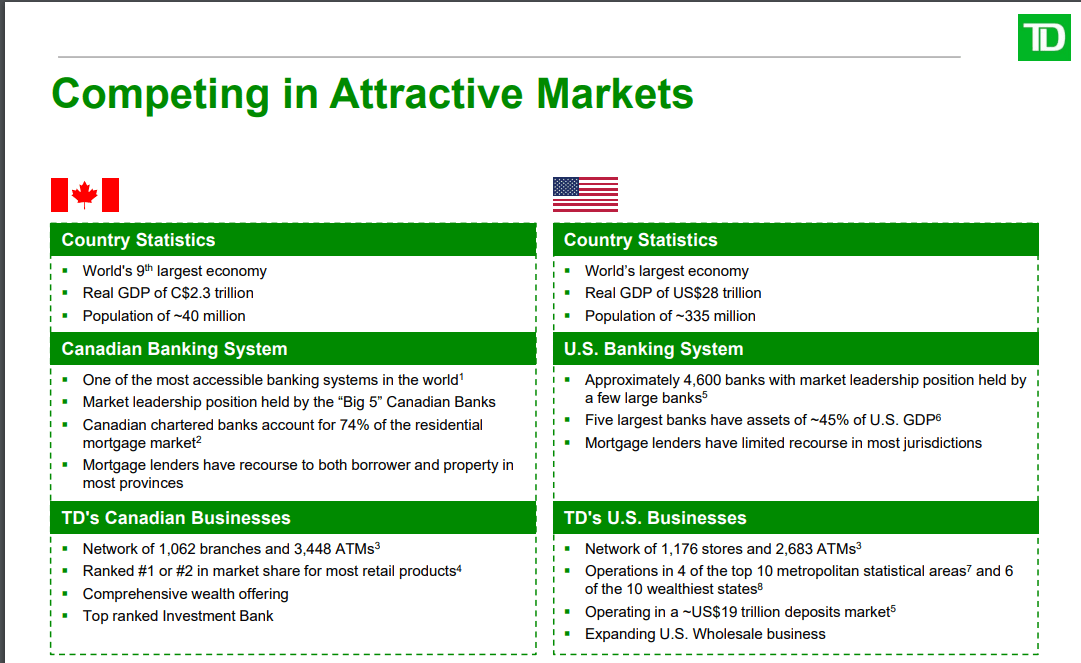

For one, the company is the second largest bank in Canada behind Royal Bank of Canada (RY). The Canadian market is very concentrated, with chartered banks accounting for 74% of the residential mortgage market. In Canada, TD’s network of 1,000-plus branches and 3,400-plus ATMs positions it as first or second in total market share for most retail products.

TD’s dominance in the U.S. isn’t quite comparable to Canada, but it remains quite established for a non-domestic-based bank. The company’s network of almost 1,200 branches and nearly 2,700 ATMs positions it just inside of the top 10 banks within the country by assets.

Aside from TD’s industry leadership, the macro environment within these two key markets is quite positive. According to Statista, real U.S. GDP is forecasted to compound by around 2% annually from 2024 to 2028. Statista’s projections for the Canadian economy are also about the same.

As TD adapts to the preferences of its customers who are overall becoming richer each year, total assets should keep growing in the years to come. That should also drive the company’s revenue and earnings higher over time.

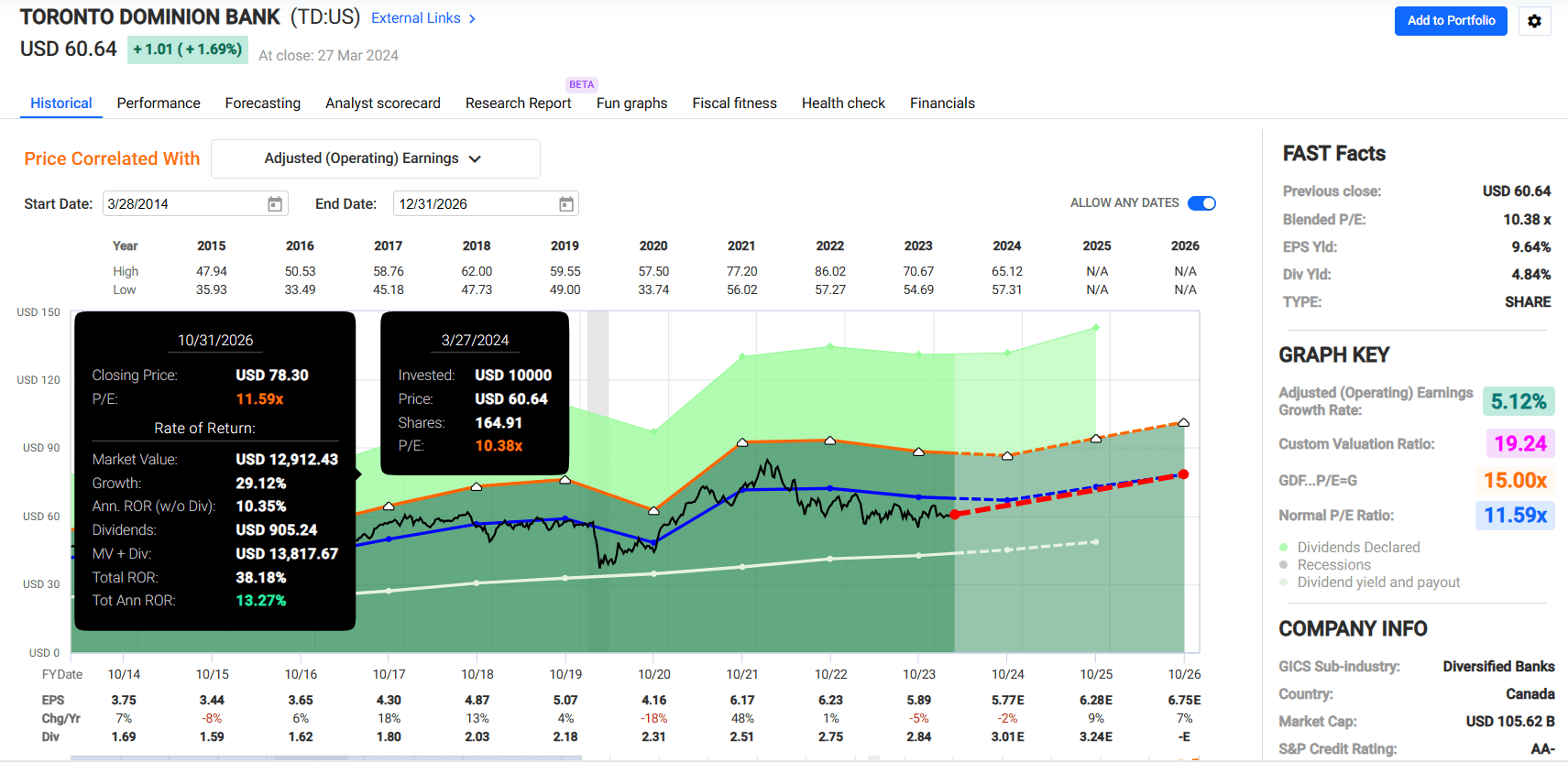

The FAST Graphs consensus is for a 2% decline in fiscal year 2024 earnings to $5.89 in USD. But beyond that time, earnings are expected to grow by 8.8% to $6.28 in fiscal year 2025 and another 7.5% in fiscal year 2026 per FAST Graphs.

TD’s financial position is also relatively strong, with the Common Equity Tier 1 or CET1 capital ratio improving from 11% in Q1 2023 to 11.5% in Q1 2024. This is how aside from the AA- rating from S&P, the company also possesses an AA2 (AA equivalent) credit rating from Moody’s and an AA credit rating from Fitch. These ratings also come with stable outlooks (unless otherwise noted or hyperlinked, all details were sourced from TD’s Q1 2024 Quick Facts PDF, TD’s Q1 2024 Investor Presentation, TD’s Q1 2019 Investor Presentation, and TD’s Q1 2024 Earnings Press Release, and TD’s 40-F filing).

A Safe Dividend With Room For Additional Growth

Having paid a dividend for 167 consecutive years, TD is a remarkable dividend stock. This is made all the more compelling by a 10% annualized growth rate in Canadian Dollars since 1998 (slide 28 of 88 of TD’s Q1 2024 Investor Presentation).

Even accounting for the weakness of the Canadian Dollar versus the U.S. Dollar in recent years, dividend growth has been compelling. According to info from Seeking Alpha, the company’s annual dividends per share in U.S. Dollars cumulatively compounded by 39.5% from 2018 to $2.8414 in 2023 – – a 6.9% compound annual growth rate.

For fiscal year 2024, the payout ratio is poised to come in at around 52% ($3.026 in annualized dividends per share divided by $5.77 EPS estimate). This is pretty close to being within the 40% to 50% payout ratio range that the company targets. That’s why I anticipate annual dividend growth near the high single digits to persist in the years ahead.

Risks To Consider

TD is an exceptional company, but an investment still carries risks with it.

Just as I highlighted in my recent Scotiabank article, the most significant risk to the company in the near term is the state of the consumer in Canada. Income growth outpaced debt growth in the most recent quarter, which helped household debt to disposable income improve to 178.7%. If the state of the consumer deteriorates, though, this could negatively impact the company’s financial results in the near term.

Another risk to TD (and all companies with scores of information valuable to hackers) is the potential for a sizable and successful cyber breach. The company takes many countermeasures to prevent such instances. But if this happened, its sensitive client data and proprietary data could be compromised. That could result in a loss of competitive positioning and litigation, which could hurt the growth story.

Summary: A World-Class Income Stock At A Great Value

FAST Graphs, FactSet

TD’s reputation as a company is admirable. The company’s brand is one of the most well-known and respected in its industry, the balance sheet is a fortress, and the dividend is well-covered.

Topping it off, TD’s blended P/E ratio of 10.4 is moderately below its 10-year normal P/E ratio of 11.6. If the company executes as predicted and returns to this valuation, 13% annual total returns could be generated between now and October 2026. That’s why I’m beginning coverage with a buy rating for now.

Q2 2024 Earnings Call Transcript")