Jonathan Knowles/DigitalVision via Getty Images

The CELH Long-Term Investment Thesis Is Highly Promising, Though Overly Inflated Here

Celsius Holdings (NASDAQ:CELH) could be the next big thing in the global energy drink market, attributed to its impressive share gains against incumbents such as Monster Beverage Corporation (MNST) and privately owned Red Bull GmbH.

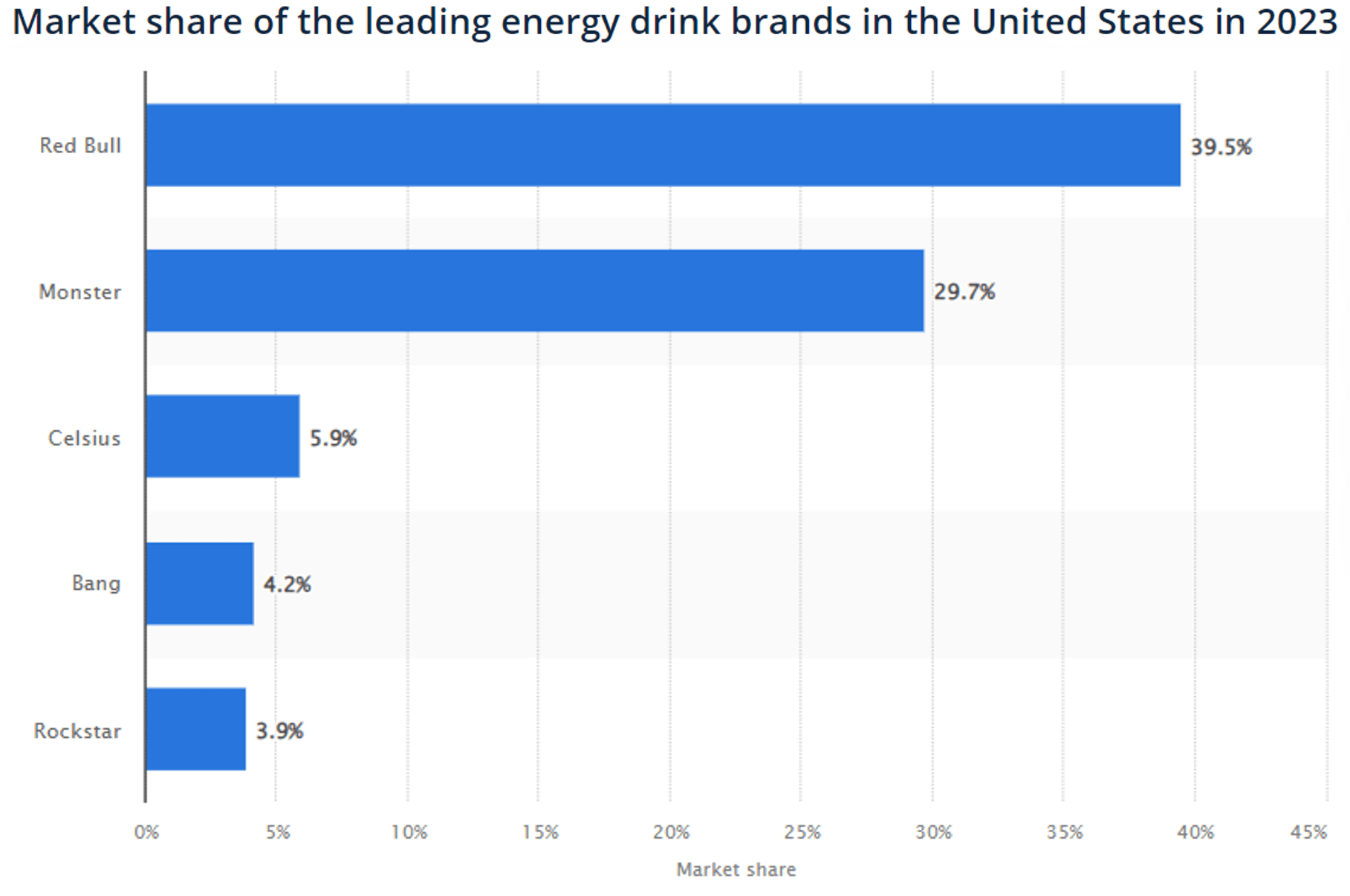

Market share of the leading energy drink brands in the US in 2023

Statista

For example, CELH only reported 5.9% of the energy drink market share in the US for the 52 weeks ending May 21, 2023. By February 11, 2024, the number has nearly doubled to 11.5%, with certain states already exceeding 15%, as per the FQ4’23 earnings call.

Combined with the management’s commentary on the “energy drink category now being a 3-team race” and the market projection of $240B in 2027 global TAM (expanding at a CAGR of +5.6%), we can understand why CELH has been reporting triple digit growth over the past three years.

For context, CELH reported exemplary FY2023 revenues of $1.31B (+101.7% YoY) and adj EBITDA of $295.6M (+315.7% YoY), implying growing consumption in existing consumers as well as successful adoption among new customers.

This proves that the management’s intensified marketing efforts have worked as intended to grow market share and brand awareness, with the impact on its FQ4’23 operating margins of 17% (-8.4 points QoQ/ +34.1 YoY) likely to be temporal.

With CELH successfully reporting four consecutive quarters of positive operating margins, we can understand why the management has also reported growing net cash on balance sheet at $755.98M (inline QoQ/ +23% YoY), further aided by its lack of debts.

We expect the beverage company to sustain its profitable growth trend ahead as well, given the consumers’ increasingly health-conscious beverage preferences, attributed to the company’s new zero sugar and/ or non-carbonated energy drink options.

At the same time, CELH has strategically partnered with PepsiCo (PEP), leveraging on the latter’s distribution system and shelf space planning, naturally contributing to its long-term growth opportunities.

Readers must also note that this particular partnership has contributed to the former’s expanding gross margins of 47.8% (-2.6 points QoQ/ +3.4 YoY) in FQ4’23 and 48% (+6.6 points YoY) in FY2023, due to the improved efficiencies in its promotional allowances and distribution channel.

This is on top of the expanding partnerships across convenience/ retail/ foodservice channels, such as Jersey Mike and Dunkin’ Donut locations nationwide, with the management already eying other opportunities through vending machines, hospitals, corporate cafeterias, and college campuses, amongst others.

Combined with the multi-year sponsorship for Formula One’s iconic Ferrari racing team, the Major League Soccer, and multiple Super Bowl advertisements, it is apparent that the management is deeply committed to delivering growth over the next few years.

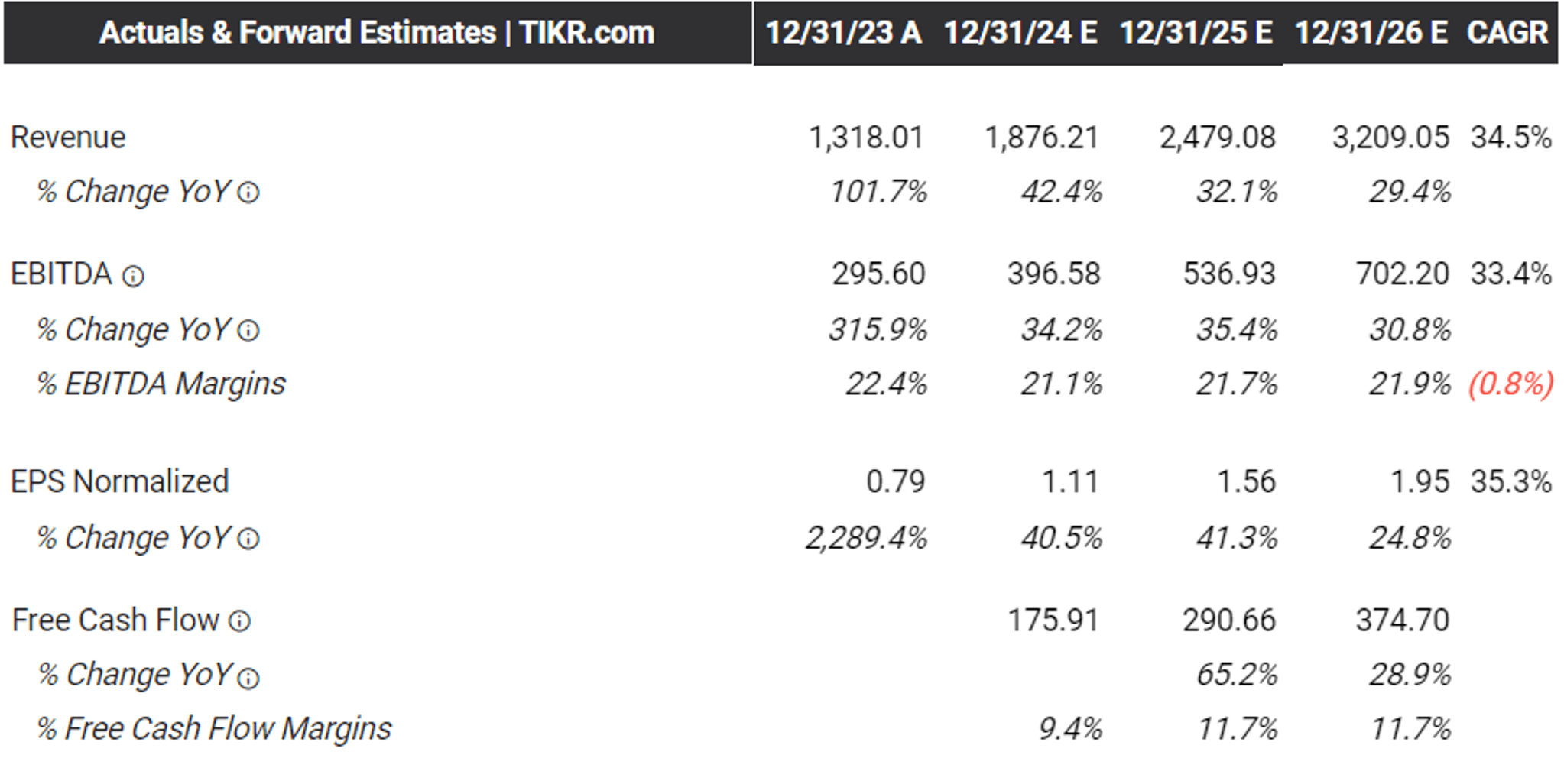

The Consensus Forward Estimates

Tikr Terminal

For now, while the management has elected to not offer forward guidance, these promising results have contributed to the raised consensus forward estimates, with CELH expected to generate an accelerated top/ bottom line growth at a CAGR of +34.5%/ +35.3% through FY2026.

This is compared to the previous estimates of +26.9%/ +29.2%, while building upon the historical growth at +104.6%/ +94.9% between FY2019 and FY2023, respectively.

Readers must also note that CELH is expected to outperform the energy beverage market leader, MNST at +10.8%/ +14.8% through FY2026, implying the former’s high growth stage as a relatively young/ promising player in a booming industry.

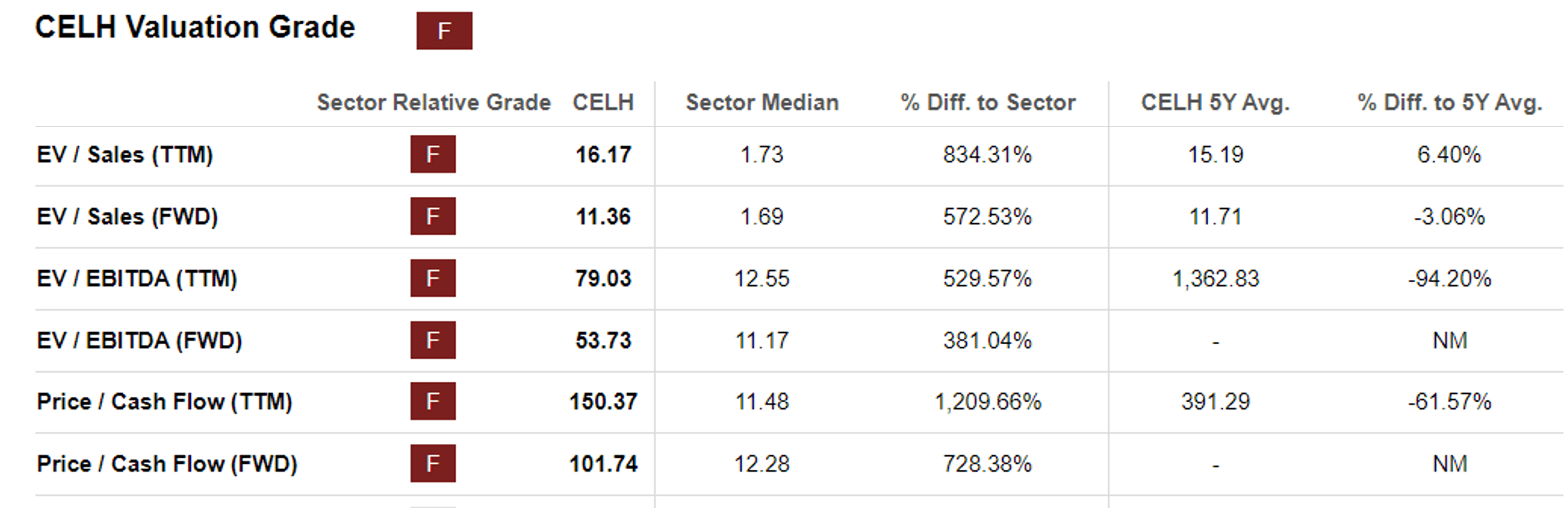

CELH Valuations

Seeking Alpha

Despite so, we are uncertain if it is wise to award CELH with the overly premium valuations here, based on the FWD EV/ EBITDA of 53.73x and FWD Price/ Cash Flow of 101.74x.

This is compared to its 1Y mean of 45.83x/ 117.21x, pre-pandemic mean of 49.13x/ -15.11x, and the sector median of 11.17x/ 12.28x, respectively.

Even if we compare CELH’s valuations to its direct competitor, MNST at 23.76x/ 33.26x, it is apparent that the former is rather expensive here, offering interested investors with a minimal margin of safety.

So, Is CELH Stock A Buy, Sell, or Hold?

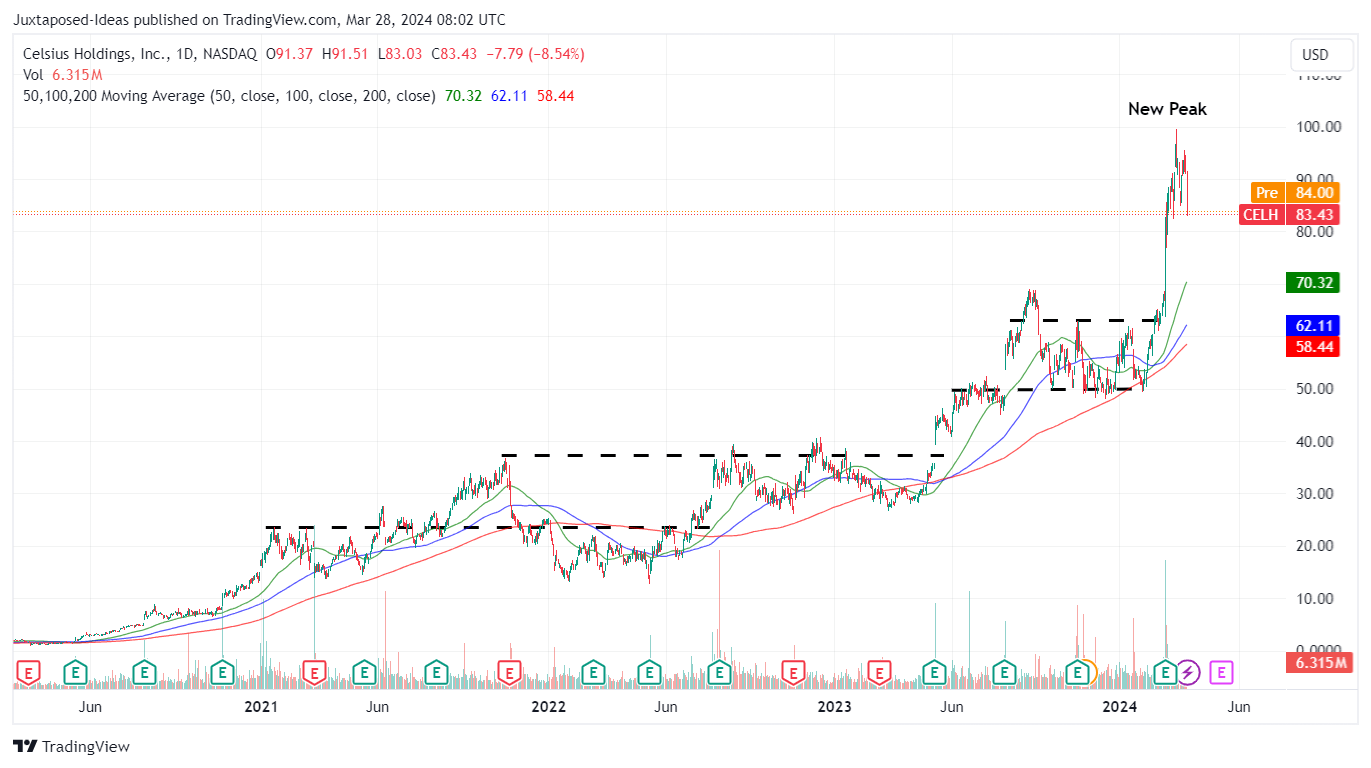

CELH 5Y Stock Price

Trading View

For now, CELH has broken out of its 50/ 100/ 200 day moving averages while charting a new peak at the $90s, with the YTD returns of +53% well outperforming the wider market at +10% and MNST at +2.7%.

Based on the FY2023 adj EBITDA of $295.6M and the latest share count of 236.96M, we are looking at an exemplary adj EBITDA per share of $1.24 (+300% YoY).

Combined with the FWD EV/ EBITDA valuations of 53.73x, it is apparent that CELH is trading way above our fair value estimate of $66.60, with an eye-watering premium of +25.2%.

While there appears to be an excellent upside potential to our long-term price target of $159, based on a similar calculation method using the consensus FY2026 adj EBITDA estimates of $702.2M and the projected adj EBITDA per share of $2.96, we believe that the stock is overly frothy here.

Readers must also note that with elevated valuations come great expectations, with any earning misses and/ or underwhelming forward guidance likely to bring forth painful corrections.

Most importantly, with 10.58% of short interest at the time of writing, we believe that there may be moderate volatility in the near term, potentially triggering capital losses depending on individual investor’s dollar cost averages.

Combined with the stock’s current retest of the previous support levels of $80s and the massive insider selling over the past few months, we prefer to rate the CELH stock as a Hold here.

Do not chase this rally.

It may be better to observe the stock’s movements for a little longer, before adding upon a deep pullback, preferably nearer to our fair value estimates.

At the same time, traders looking to lock in gains may also consider doing so here, since it remains to be seen if the stock is able to sustain this upward momentum for any longer.

Q2 2024 Earnings Call Transcript")