PM Images

Absurdities of Market Structure

“We live in an upside-down age where making a profit distribution to company owners is viewed, incredibly, as a failing by many S& P 500 Index companies and nothing less than heresy by the overwhelming majority of new economy companies.” -Daniel Peris

We live in interesting times. Nowhere is that more evident than in the structure of the equity markets. Previous market environments saw companies pay their investors a portion of their profits, known as a dividend. This dividend culture was a traditional part of investing in equity markets. Corporate boards and management saw dividends as an integral part of the capital return policies they pursued and pushed dividends up to entice investors to become owners in their stock. This is a thing of the past, as the number of stocks that pay dividends has dwindled, and the overall yield on the S&P 500 has fallen to a mere 1.58%.

Consider that dividends made up 75% of the total return for the S&P 500 index from 1871-1989. But from 1990-2023, dividends made up only 30% of the total return. What explains this change?

One can obviously point to the 1982 legislation that made stock buybacks acceptable, even preferred by management. It is important to note that prior to 1982, buybacks were uncommon and seen as a form of market manipulation, how the times have changed. One might also look to the dawn of the technology sector, and its period of dominance over the market capitalization during the 1990-present period. But the true culprit is the adoption by corporate boards and management of principles of theoretical finance that made the case that dividends did not matter. That it was merely a capital structure decision and dividend policy was less than meaningless, it was irrelevant.

This sentiment is reiterated today by factor investors and those who believe the arguments of theoretical finance made in the latter half of the 20th century without questioning these obviously dubious theories. The 2008 financial crisis certainly should have made us question these theories and their applicability to modern markets, as nearly every risk model based on these academic theories was proven worthless.

The 20 year under performance of value to growth should have also made investors question the findings of academics who claim that investors should pay additional fees to chase an academic definition of value on a total return basis without consideration of dividends. It should be noted that the original Fama & French factor model research executed the value factor through a long/short strategy, not by merely owning value stocks long only. This just proves that most of the practitioners in this area fail to even read the research, and even fewer understand its implications. A fact that becomes evident when you engage with factor investors who believe in the factors with religious like zeal.

Instead let me contend and prove in this piece that investors need to take a different approach to investing. I want to review the literature that got us to this place where market participants actually believe in the dividend irrelevance theory and prove why this is misguided at best and harmful at worst. I will further make the case for renewing an old idea, of viewing investments in equity securities as pieces of real businesses, businesses that should be paying their owners a piece of the profits earned. Based on the evidence one could even make the argument that dividends are the ONLY reason to invest in stocks.

Consider the return in the stock market from 1871-2023. Stocks returned 7.01% real return including dividends. This number drops to a mere 2.5% real return when dividends are taken out. It is dividends that have driven the returns in equity securities for this 152-year time period. When viewed across the span of market history, we see just how anomalous the current low dividend environment is.

Challenging Academic Finance

The fundamental parameters of academic finance have shaped the world we live in today. They act as a sort of ordering system to bring order to chaos and make the world of finance make sense. But there is an alternative view to the ideas put forth by financial theory. Daniel Peris, noted historian, and Portfolio Manager at Federated-Hermes, posits some of these critiques in his previous book, “Getting Back to Business”, a thorough refutation of modern portfolio theory. He furthers his analysis to looking at the academic literature around dividends in his new book, The Ownership Dividend.

In it he challenges the assumptions made by Markowitz in his landmark paper by making the point that there is a vast amount of subjectivity in the creation of these models. This makes them less reliable, and unrealistic for application to the real world.

We also see this in the area of diversification. The academic definition of diversification would require an investor to hold thousands of companies in the often-cited total stock market index. This, they argue, ensures you get the best returns by owning the whole market. This argument comes directly from academic finance, and loads of investors have piled on the train, bringing their self-fulfilling prophecy to fruition.

The index revolution may have started in 1976 with Jack Bogle and the creation of the first index fund, but the theoretical underpinnings for the total market index fund started well before that. In recent years we have really seen an acceleration in the adoption of index products. This is especially true in those seeking to retire early, the so-called “FIRE” communities. Investors in these communities are piling into total market index funds, with many using it for ALL of their money on the advice of several gurus in the movement. But what do these investors really own? If you ask them, they will say they own the entire market. If you asked them further if they were well diversified, they would say “of course! I own over 3,000 companies!”

In reality however, they would be wrong. The total market index may in fact have 3,000 companies in it, but it is far less diversified than most of its holders realize.

More than a quarter of the fund’s assets are found in its top 10 holdings. 50% of the portfolio’s assets are in its top 50 holdings, representing a mere 1.6% of portfolio positions. The other 50% is scattered among thousands of companies having little if any effect on the overall performance of the fund, it is diversification for diversifications sake, or what Charlie Munger called “diworsification.”

So, in reality, the total stock index is a momentum driven, highly concentrated portfolio representing a market popularity contest, and leaving those who put their hard-earned money into it exposed to the most risk, at the highest prices, for the most popular stocks that climb to its top 10. This is maximum risk for BELOW average return after fees and expenses. This is not investing, so let’s call it what it is, this is speculating.

“There’s only one intelligent form of investing: figuring out what something is worth and seeing if you can buy it below that price. It’s all about value. -Howard Marks

Every investor should read the 2017 piece, “The Active Equity Renaissance: The Rise and Fall of MPT” by C. Thomas Howard, on the CFA institute blog, it gives a great summary of the rise and fall of accepted dogma within the financial community and makes a call for evidence and rationality in a world of emotional decision making. In my favorite section from the piece, the author states:

Much of finance pushes aside the mounting contrary evidence and soldiers on under the yoke of the MPT paradigm. This might seem surprising: Isn’t finance a discipline based on empiricism, one that only accepts concepts supported by evidence? Unfortunately, as Thomas Kuhn argued years ago in his classic work, The Structure of Scientific Revolutions, scientific and professional organizations are human and are susceptible to the same cognitive errors that afflict individual decision making.

This critique of academic finance naturally flows to the dividend puzzle and the notion that dividends are irrelevant. In order to dissect this viewpoint we must begin with Markowitz and his foundational idea of modern portfolio theory and the notion of diversification.

As Daniel Peris states:

“Markowitz follows with another assertion in 1952 that “diversification is both observed and sensible; a rule of behavior which does not imply the superiority of diversification must be rejected both as a hypothesis and as a maxim.” I do not dispute this assertion, but I do want to note that it is no less a subjective choice than his other first principles. And I would repeat my earlier observation that in practice, having 30-40 stocks verses 3 or 4, as was common then, is indeed risk-reducing diversification, but that having many hundreds or even thousands of holdings in one’s portfolio, as is common today through index funds and ETF’s, is not.

He continues:

Markowitz could never have imagined, nor could he have intended such an absurd state of affairs. Worse, the extreme diversification so popular currently is a form of self-deception in that the overdiversified investors are really choosing not to choose, while all the time thinking they have made very responsible decisions.

In the Dividend Puzzle, Black states the following:

“The choice between a common stock that pays a dividend and a stock that pays no dividend is similar, at least if we ignore such things as transaction costs and taxes. The price of the dividend-paying stock drops on the ex-dividend date by about the amount of the dividend. The dividend just drops the whole range of possible stock prices by that amount. The investor who gets a $2 dividend finds himself with shares worth about $2 less than they would have been worth if the dividend hadn’t been paid, in all possible circumstances.”

In this analysis Black ignores two fundamental concepts.

1. The investor who gets the $2 dividend and reinvests it now owns more shares than they did before the company paid the dividend. While their total balance does not change as Black correctly states, the price of the stock drops to reflect the payment of dividends, it is accretive to the long-term investor who acts like an owner. It steadily increases their shares over time providing them with a larger and larger claim on the company’s earnings.

2. The income investor does not have to deplete their ownership stake to receive income from the investment in the shares if they receive a dividend. In the case of the income investor, the price of the stock drops by $2, and the investor will get $2 in dividend income. The investor who invests in non-dividend paying stocks because they believe dividends do not matter, will have to sell their shares to create an equivalent amount of “income” by realizing capital gains.

This is yet another example of how academic finance fails to account for the real-world application of these theories. Dividends are most certainly not irrelevant for long term investors who seek to compound their wealth over decades. Consider that in Modigliani and Millers 1961 exposition of the dividend irrelevance theory they made a number of assumptions such as taxes do not exist, there are no flotation costs or transaction costs for issuing stock, dividend policy has no impact on capital budgeting decisions, leverage has zero impact on the cost of capital, and finally the most absurd of all assumptions and the vital belief of making the theory work, firms pay out 100% of Free Cash Flow (FCF).

In reality none of these assumptions hold true.

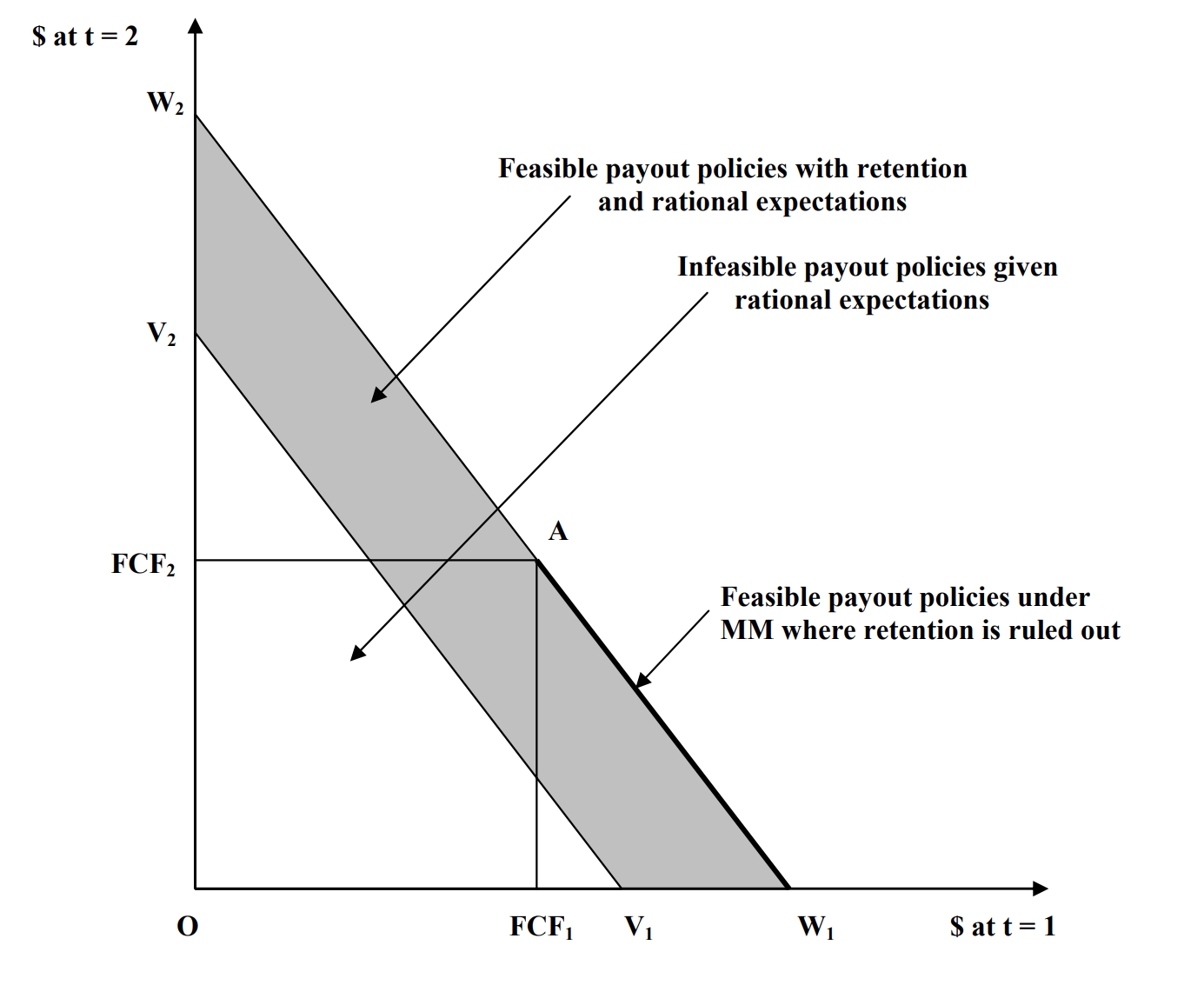

The best critique I have found of the dividend irrelevance theory, and the Dividend Puzzle of Fischer Black who relies on Modigliani and Miller’s dividend irrelevance, comes from Harry and Linda DeAngelo of the Marshall School of Business at USC. In their paper “The Irrelevance of the MM Dividend Irrelevance Theorem“, they critique Miller and Modigliani’s assumption of 100% FCF payout, an assumption that when we allow for retention of free cash, fails.

The Irrelevance of the MM Dividend Irrelevance Theorem, Figure 2 (DeAngelo)

“Because their assumptions ensure payout policy optimality by forcing 100% FCF distribution to be an automatic by-product of the investment choice, MM (1961) confound investment and payout policy and mistakenly attribute the value impact of payout policy optimization to investment policy. Payout policy matters when MM’s assumptions are relaxed to allow retention of FCF because there is no longer a one-to-one correspondence between feasible and optimal policies.”

One challenge to this point is the idea that even with retention allowed, the dividend irrelevance theory holds as long as the net present value (NPV) of investment policy is fixed. In this challenge lies the very evidence needed to disprove dividend irrelevance. Because when you allow for retention, you give managers the ability to make decisions on payout policy, just as they have in the real world. Therefore, Miller and Modigliani’s theory of dividend irrelevance is making assumptions that do not carry over to practical application. Payout policy is very relevant to managers, and stockholders.

A final critique of Fischer Black’s dividend puzzle, which relies on dividend irrelevance, demonstrates how the logic of the entire theory fails when applied to real world decision making by corporations:

“Black argues that when taxes are added to the MM framework, firms should largely eliminate payouts to stockholders,1 which they obviously do not. But the logic Black uses to generate this prediction is flawed. In all cases, including those in which payouts are taxed, optimal payout policy requires distributions that are large in present value terms; if managers actually implemented Black’s suggestion to eliminate virtually all payouts, they would destroy untold amounts of stockholder wealth. (emphasis mine)

Conclusion

Bringing up the topic of dividends shouldn’t be controversial, but in personal finance circles, this is a rather controversial topic. Some argue that dividend investors are “unsophisticated” and instead investors should be focused on total return. They cite the research of Fischer Black in his seminal work “The Dividend Puzzle,” as evidence for their superiority. But in the process, they ignore a plethora of evidence on returns that categorically denies their view. The reality is that dividends make up nearly all of the return that investors receive from equity securities. Investing in non-dividend paying stocks proved to produce the lowest returns as I showed here.

In conclusion, dividends remain an important part of investment in the capital markets as noted portfolio manager David Bahnsen lays out in this clip from his Dividend Cafe podcast in which he discusses the logic of dividends vs. speculative madness.

I hope Daniel Peris is correct, and we are entering a new paradigm shift, away from share buybacks and back towards the resumption of dividend payments as the preferred capital return policy. I end with a quote from The Ownership Dividend discussing the importance of dividends and the non-equivalence of dividends and buybacks:

Whether in theory or in practice, these two activities—on one hand, clipping your coupons; on the other hand, going out and selling securities—are most certainly not the same. Having capital gains depends on market sentiment, on the views of people often far removed from the activities of a company. In contrast dividends are a function of a company’s operations. A dollar may be fungible; how it is generated is not. Drawing this distinction—between a capital markets activity and a business outcome—may be the most important assertion in this book. The rest of the argument follows naturally from it. -Daniel Peris, The Ownership Dividend

Q2 2024 Earnings Call Transcript")