piranka

Introduction

Sterling Infrastructure, Inc. (NASDAQ:STRL) is a small-cap construction and engineering company that provides infrastructure services and solutions to a wide range of customers. With expected exponential growth in artificial intelligence, electric vehicles, and semiconductor-related projects, Sterling’s E-Infrastructure segment holds the necessary tools to make this growth feasible. Furthermore, its strategic refocus from lower-margin projects towards high-margin, high-growth opportunities allows for a strong foundation. Despite the ~200% stock price increase since the start of 2023, I believe STRL still has significant room for growth. I recommend a buy for Sterling Infrastructure with a price target of $146 and ~29% upside. My target is based on 2025 EBITDA of $340 million and a 13x EBITDA multiple.

Company Overview

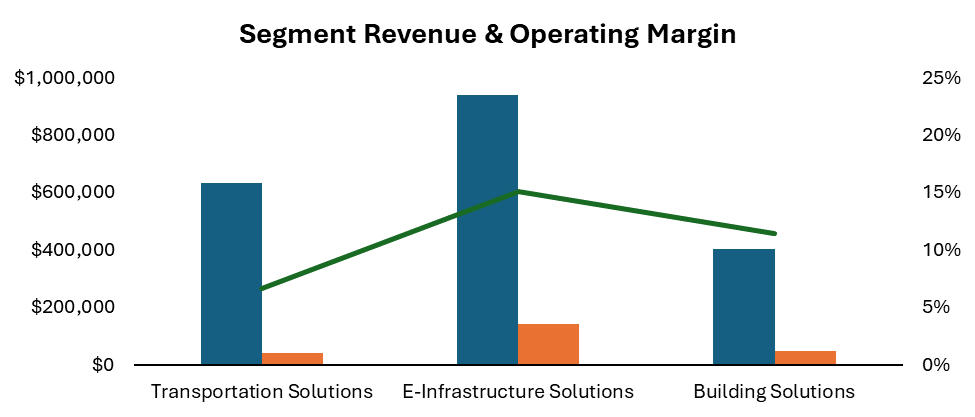

Sterling operates through three main segments: E-Infrastructure Solutions, Transportation Solutions, and Building Solutions. The E-Infrastructure segment contributes to 48% of total revenue with a 15% operating margin and is the fastest-growing segment. It serves large blue-chip end users in e-commerce, data centers, manufacturing, and power generation. It has already been awarded several large projects in EV and solar. The Transportation Solutions segment, primarily driven by government spending, contributes to 32% of total revenue with a 7% operating margin. It has seen substantial change since 2016 as it moved from low-bid heavy highway projects to higher margin projects including airports. In 2016, these low-margin projects accounted for 79% of revenue, but now only account for 15%. Finally, Building Solutions, which mainly operates out of Dallas-Fort Worth, contributes to 20% of company revenue with an 11% operating margin. Management expects continued decline in this segment on the commercial side, offset by strong dynamics on the residential side from continued population growth and housing shortages.

STRL Investor Presentation – Sidoti Jan. Micro-Cap Conference

Financial Positioning

While some view the recent stock price run as unsustainable, I see it aligning the company closer to industry norms while still retaining an attractive valuation. Looking in comparison to the construction and engineering industry, I don’t see a single data point that could be considered overvalued. From a debt perspective, it has a 2.9 debt to FCF ratio compared to the industry median of 10. From a capital structure perspective, it currently has a debt-to-equity ratio of 64% compared to the median of 80%. Moving to margins, STRL further shows its strong positioning with an FCF margin of ~20% making it the highest in the industry. This is all backed by price multiples that are either in-line or trade below the comparable companies. I talk more about the relative valuation at the end of this article, and you can see the segmental breakdown below.

Revenue in Thousands USD (Excel)

Strategic Refocus

Management has made clear plans to move away from lower-margin heavy highway and water treatment projects towards high-margin, high-growth areas in E-Infrastructure and Building Solutions. This can be seen with its recent divesture in Myers for $18 million alongside acquisitions in Concrete Construction Services of Arizona LLC and Professional Plumbers Group, both of which pivot towards more lucrative residential markets. This shift supports a sustainable growth trajectory through enhancing gross margins and diversifying its revenue streams. Unlike many competitors that spread efforts across a broad range of projects, STRL now remains focused on high-quality projects that allow for margin expansion.

Solid Backlog

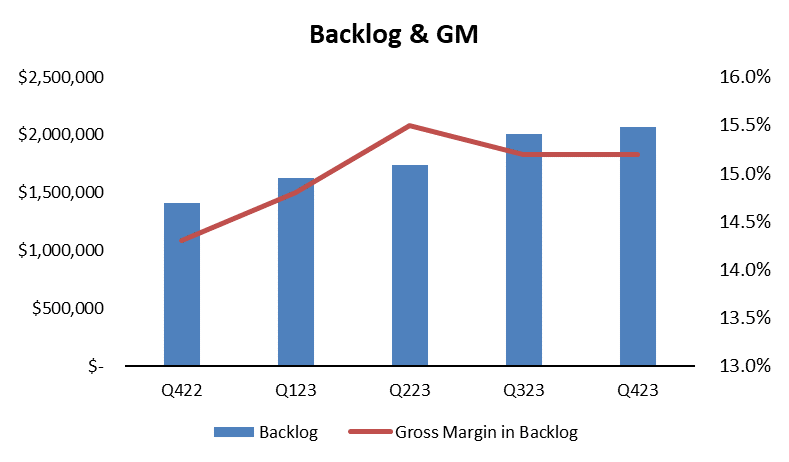

For more vision into Sterling’s growth sustainability, we can look at its backlog which stood at $2.07 billion at the end of 2023, up from $1.41 billion the previous year. Furthermore, the quality of these projects has improved substantially which is evident by its gross profit margin of 17% in 2023, compared to 15% in 2022. This robust pipeline of work, backed by the enhancement of operational efficiency, illustrates STRL’s positioning within the space. Management expects ~65% of this backlog to be completed in 2024. Other competitors have seen substantially less backlog growth over the same period: Construction Partners, Inc. (ROAD) has only seen a 14% increase, Comfort Systems USA, Inc. (FIX) only a 26% increase, and Dycom Industries (DY) only 13%. This compared to Sterling’s robust 46% backlog increase, further shows the sustainability of its competitive advantage.

Backlog in Thousands USD (Excel)

E-Infrastructure Opportunity

Sterling has a clear solidified positioning within the infrastructure space, which is further supported by diversification and high-quality project selection. I see the most opportunity within its E-infrastructure segment which provides the necessary tools for data center, semiconductor, and electric vehicle projects, all of which will see continued exponential growth. The US data center market is expected to grow at 14% CAGR through 2032, the US government has announced plans to spend $11 billion on semiconductor R&D, and the EV market is expected to grow at a CAGR of 17% through 2028. Sterling Infrastructure provides the necessary pickaxe to mine for this gold. Still, many believe we are in an AI bubble, similar to that of the Dotcom bubble, but I don’t believe this is the case. AI will change every industry, and the lack of supply amid strong demand is evident. The current obstacle hindering this growth is inadequate infrastructure behind data centers and energy support. This creates a direct market opportunity for Sterling to take advantage of. STRL has already announced contracts with leading companies including Rivian, Meta, and Amazon to build data centers and next-gen manufacturing locations. These relationships will only create further networking benefits and allow Sterling to gain substantial market share over the next 10 years. While there are many strong players in this space, the demand for E-Infrastructure solutions still vastly outpaces supply, creating plenty of room for further opportunity.

Relative Valuation

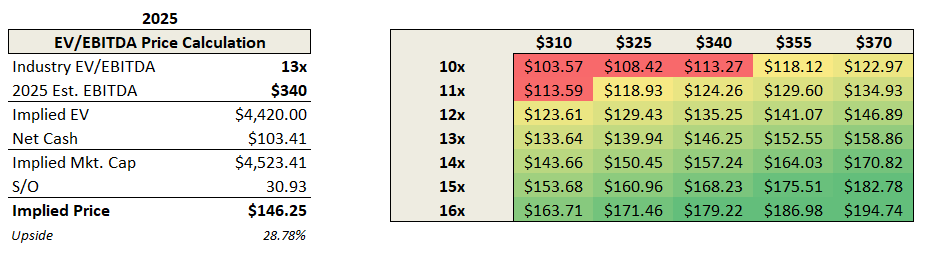

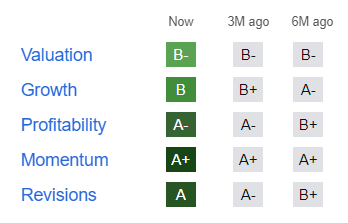

My relative valuation projects 2025 EBITDA of $340 million based on a multiple of 13x EBITDA. For comparables, I looked at the Construction & Engineering Industrials sub-industry and what management considered comparable companies in the most recent 10-K; both yielded relatively similar results. In terms of EV/EBITDA, the average range is 14x-16x, with STRL currently at 13x. While consensus EBITDA for 2025 is $321 million, only one Wall Street analyst covers the stock, creating a higher chance for a change in expectations. My $340 million in EBITDA implies a ~14% margin and is driven by exponential increase in technology-related projects supported by margin expansion in the transportation solutions segment. Furthermore, based on the competitive landscape, I believe a 13x multiple is more than reasonable. This valuation is also further supported by STRL’s Seeking Alpha Quant Rating of 4.93.

Excel Seeking Alpha

Absolute Valuation

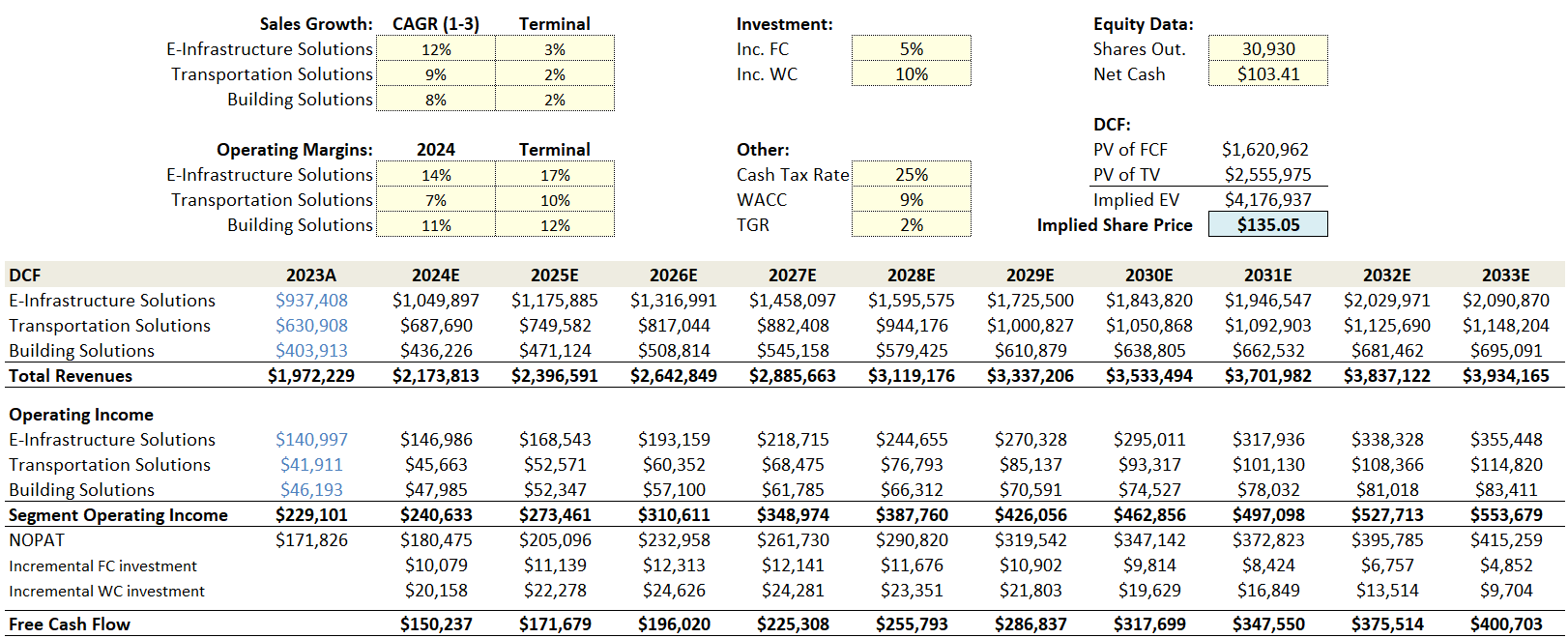

For my DCF valuation, I assumed a stable 3-year CAGR for revenue that trends down to a terminal value. For operating margins, I assumed further margin expansion mostly in E-infrastructure and Transportation Solutions. Looking at reinvestment, I opted for an incremental assumption based on change in sales. The larger need for working capital comes from the nature of its backlog and contracts. The WACC of 9% is based on a 10/90 split of debt to equity with a cost of equity at 9.6% and cost of debt at 5%. While arguments can be made about these assumptions, there is substantial room for value creation supported by margin expansion and bullish revenue growth opportunities in E-Infrastructure. My DCF price target is $135.05 implying ~20% upside.

Excel

Risks

The most notable risk is implied volatility as it was considered a micro-cap stock before 2020 and has only recently surpassed a market cap of $1 billion. Currently, its one-month implied volatility is ~45% compared to the SPDR S&P 500 ETF Trust (SPY) at ~11%. This means significant changes in expectations, or an earnings miss could cause a substantial change in price. Furthermore, as a small-cap stock, it has less access to affordable capital and a smaller market share compared to competitors with international footprints. Beyond this, any negative change in E-Infrastructure customer spending would cause a decrease in valuation. There is also potential for an AI-induced bubble, but I see this risk as minimal. It is important to note that the stock has risen almost 200% over the last year and is trading at a 52-week high. The downside risk could also be elevated if we were to experience any macroeconomic downturns, as infrastructure spending would drop significantly. For a final note, only one Wall Street analyst covers the stock and has a current hold rating.

Conclusion

Despite the significant increase in STRL’s stock price, I don’t see any substantial overvaluation. Comparatively, STRL has a fantastic capital structure and continues to de-lever, its margins are industry-leading, and it trades at a discounted EV/EBITDA multiple. On a fundamental level, it has shown significant margin expansion in the transportation segment, and the E-Infrastructure segment continues to show strength with clear industry tailwinds. From a financial standpoint, it has a growing backlog with high-margin projects and no notable areas of difficulty. Overall, I see robust long-term growth opportunities that are further supported by margin expansion. The volatility of the stock may provide better entry points over the next two years, but either way, I see plenty of opportunities ahead.

Q2 2024 Earnings Call Transcript")