JulPo

Introduction and thesis

Carrier Global Corporation (NYSE:CARR) is a leading provider of heating, ventilation, and air conditioning (HVAC), refrigeration, fire, security, and building automation technologies. The company operates globally and serves both residential and commercial markets. With a history dating back over a century, Carrier has established itself as a pioneer in climate control solutions.

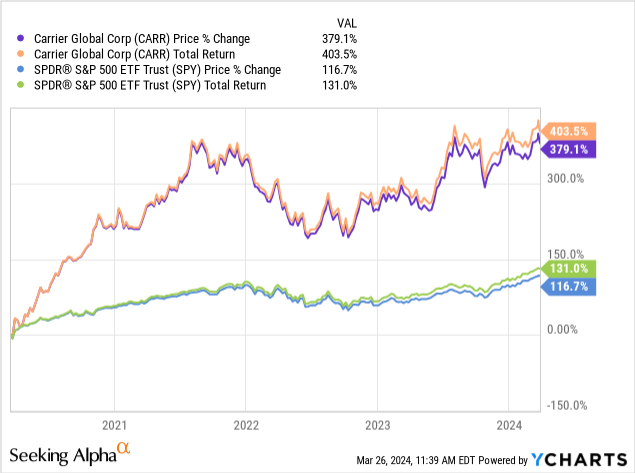

We are positive about the future outlook of CARR. The company is transitioning to a pure-play HVAC business, which positions it to maximize returns from industry tailwinds. Investors are equally positive, with a considerable share price run since 2020.

We do have some reservations, as the stock is priced for margin improvement and an increase in its organic growth trajectory. We do see a route to delivering this but believe there to be execution risk, particularly with the realization of cost synergies.

With limited margin for error in its valuation, we rate the stock a hold.

Commercial analysis

Capital IQ

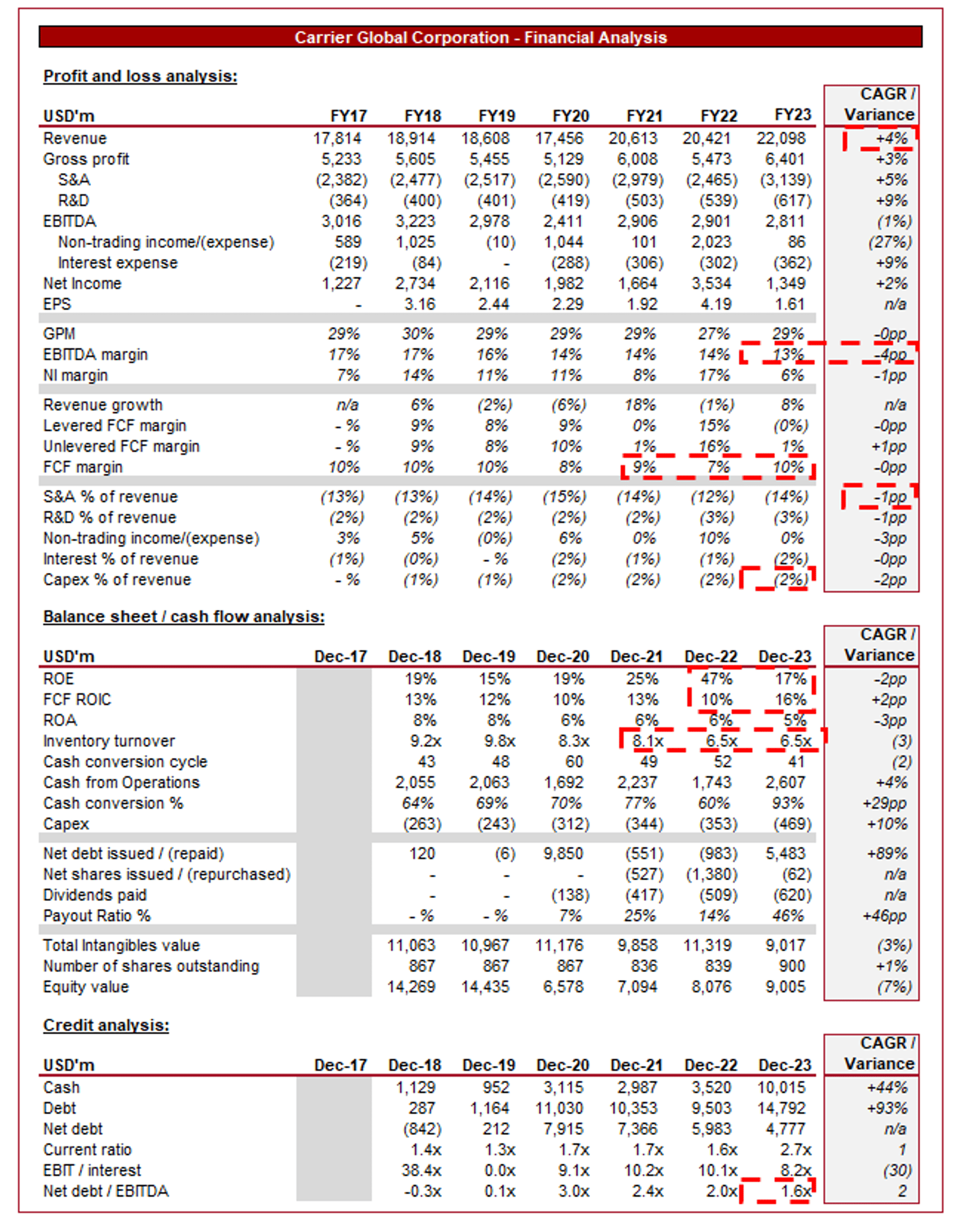

Presented above are CARR’s financial results.

CARR’s revenue growth since FY17 has been modest, with a CAGR of +4% into FY23. During this period, its portfolio has been reshuffled, with a number of acquisitions and disposals. In conjunction with this, profitability has declined, with EBITDA falling at a CAGR of -1%.

Business Model

CARR is a leading provider of heating, ventilation, air conditioning (HVAC), refrigeration, fire, security, and building automation technologies. The company offers a wide range of products and services designed to improve indoor air quality, temperature control, and energy efficiency in residential, commercial, and industrial buildings.

Similarly to its peers, CARR has expanded beyond HVAC to related industries, remaining within its industrials sphere of expertise. The benefit of this has been to widen its total addressable market and further monetize its B2B relationships. This has been delivered in large part by acquisitions (~$1.4b of cash spent since FY17), with the subsequent focus on commercial and cost synergies.

CARR has a strong global presence with operations in over 180 countries and a network of manufacturing facilities, distribution centers, and service locations worldwide. At its existing scale and global reach, the company has broadly resilient revenue generation, regardless of cyclical swings. This said, we believe it has likely reached a realistic maximum for economies of scale, with limited incremental GM% gains in recent years despite revenue growth.

As previously touched on, CARR actively pursues strategic acquisitions and partnerships to expand its product offerings, enter new markets, and enhance its competitive position. CARR has operational expertise and industry relationships, while lacking specific production expertise and brands in specific segments, making M&A a natural approach. Whilst this has supported CARR’s upward trajectory, we are not wholly convinced by its execution. CARR’s FCF ROIC, which we use as a proxy for returns as NI has been impacted by asset sales, was declining, only improving in FY23 due to a NWC swing. Given the company’s size, seeking accretive acquisitions is far more beneficial in our view, as incremental margin improvement can be far more lucrative.

Strategy

CARR has transitioned its focus to energy-efficient solutions to meet the growing demand for sustainable building technologies. The company’s products are designed to minimize energy consumption and reduce greenhouse gas emissions, with considerable exposure to heat pumps, which are growing in the double-digits.

CARR’s considerable scale is fundamentally important to its growth potential. The company invests heavily in research and development (~3% of revenue) to drive innovation and technological advancements in the HVAC and refrigeration industry. With the energy transition in full force and legislative action slowly developing, we are reassured by CARR’s level of spending that it will be able to modernize its offering.

Further, CARR is transitioning its portfolio to higher growth and future-tied segments. The company has thus far disposed of its Security business (proceeds: ~$5b) and Commercial Refrigeration operations (~$0.8b), with its Industrial Fire and Resi/Comm. Fire segments are on track for a late 2024 sale. We find this an interesting strategy by Management as CARR’s Fire and Security segment currently has an adj. OP% of 14.2%, which is higher than both HVAC (12.1%) and Refrigeration (10.5%). For this reason, it is actively choosing to dilute margins in order to improve growth. We are not entirely convinced by this strategy (desire to immediately become a pure-play HVAC provider), albeit acknowledging that the raised capital will be attractive returns for investors and can be utilized to better position the portfolio for the long-term following its blockbuster acquisition.

Finally, the company has closed the acquisition of Viessmann Climate Solutions for ~€12b. Management considers this a game-changer for the Group, allowing for MSD growth and high-teens EBITDA margin. This will be delivered through considerable cost synergies and product launches across Europe and the US. We certainly agree that there is considerable potential here, particularly with margins, albeit the execution risk is high. We see this as a “wait and see” situation.

HVAC Industry

The HVAC industry is forecast to grow at a CAGR of +7% during the coming decade, driven by economic development, rapid urbanization, population growth, and technological advancements (clean energy and smart tech). The demand for heat pumps is called out in particular as an area of outsized growth, which is where CARR has increased its exposure.

Major competitors of CARR include companies such as Trane Technologies (TT), Daikin Industries (OTCPK:DKILF), Lennox International (LII), and Johnson Controls (JCI).

Financials

CARR’s recent performance has been healthy, with top-line growth of +13.3%, +15.0%, +5.1%, and -0.1% in its last four quarters. In conjunction with this, margins have continued to step down.

The company’s growth has been driven in part by its Refrigeration segment, with an improvement in demand following a period of softening spending, as evidenced by a YoY growth rate of containers by ~60%. This segment appears primed to benefit from electric transport units due to the energy transition trend.

Growth has dragged in the last two quarters due to its HVAC segment, with North American residential sales down considerably (high teens) while NA commercial HVAC continues to grow in the low double-digits.

CARR’s primary growth driver has been the aftermarket segment, which has experienced 3 successive years of double-digit growth. CARR has performed well to increase its exposure to this segment and also the attractiveness of its offering, contributing to an impressive attachment rate of ~45% (nearly double historical levels).

Whilst we are not yet entirely convinced by the scope for margin improvement outside of Viessmann, it is worth highlighting GM% has increased from 27% in FY22 to 29% in FY23. This has been wholly offset by an increase in S&A costs but the expectation is for this to be diluted going forward, allowing for an expansion.

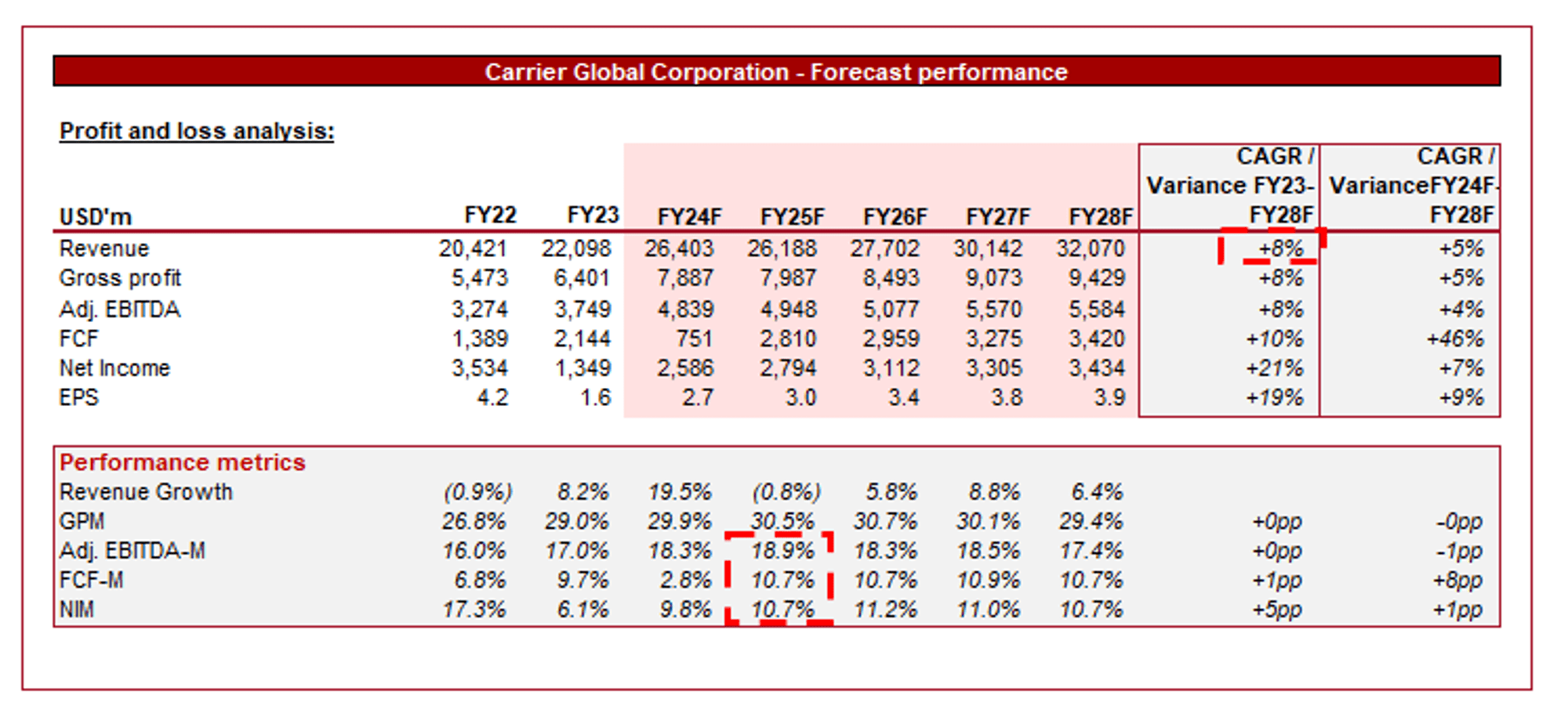

Looking ahead, analysts are forecasting revenue growth of +8%, alongside a small amount of margin improvement. The forecast growth rate broadly aligns with the industry forecast, which we believe is reasonable. Whilst CARR will have greater issues reaching the average due to its scale, its portfolio appears very well placed to exploit tailwinds.

Regarding margins, we concur wholly with the clear analyst uncertainty visible in the forecasts below. It is far too early to judge the achievability of synergies and where the normalized level will be.

Capital IQ

Industry analysis

Seeking Alpha

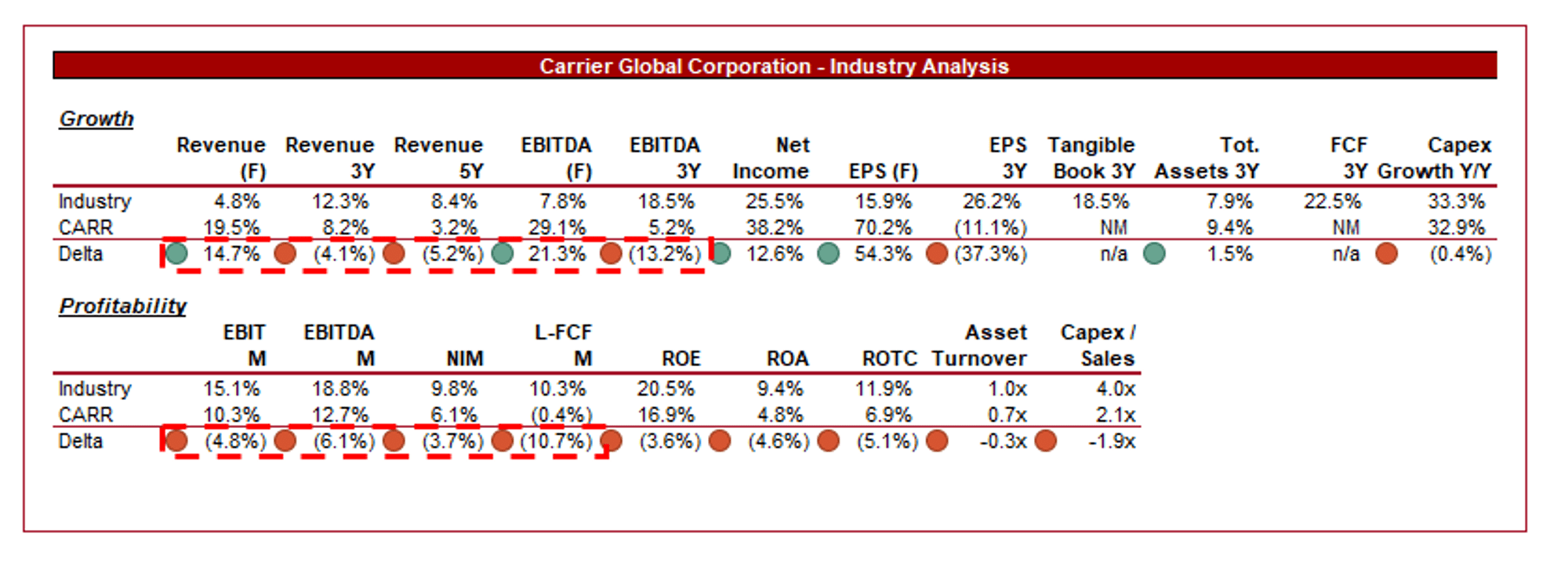

Presented above is a comparison of CARR’s growth and profitability to the average of its industry, as defined by Seeking Alpha (37 companies).

CARR‘s current financial performance leaves much to be desired when compared to its peers. Whilst the business has broadly tracked on growth, albeit clearly lacking over a 3-5Y period, its biggest issue is margins.

If we consider where CARR could land in the next 2 years, it will likely still be behind on margins, although to a smaller degree, with comparable growth when including the potential for M&A.

For this reason, we believe CARR should be trading at a small discount to its peers on a normalized basis to reflect this financial weakness but strong commercial position and tailwind benefits.

Valuation

Capital IQ

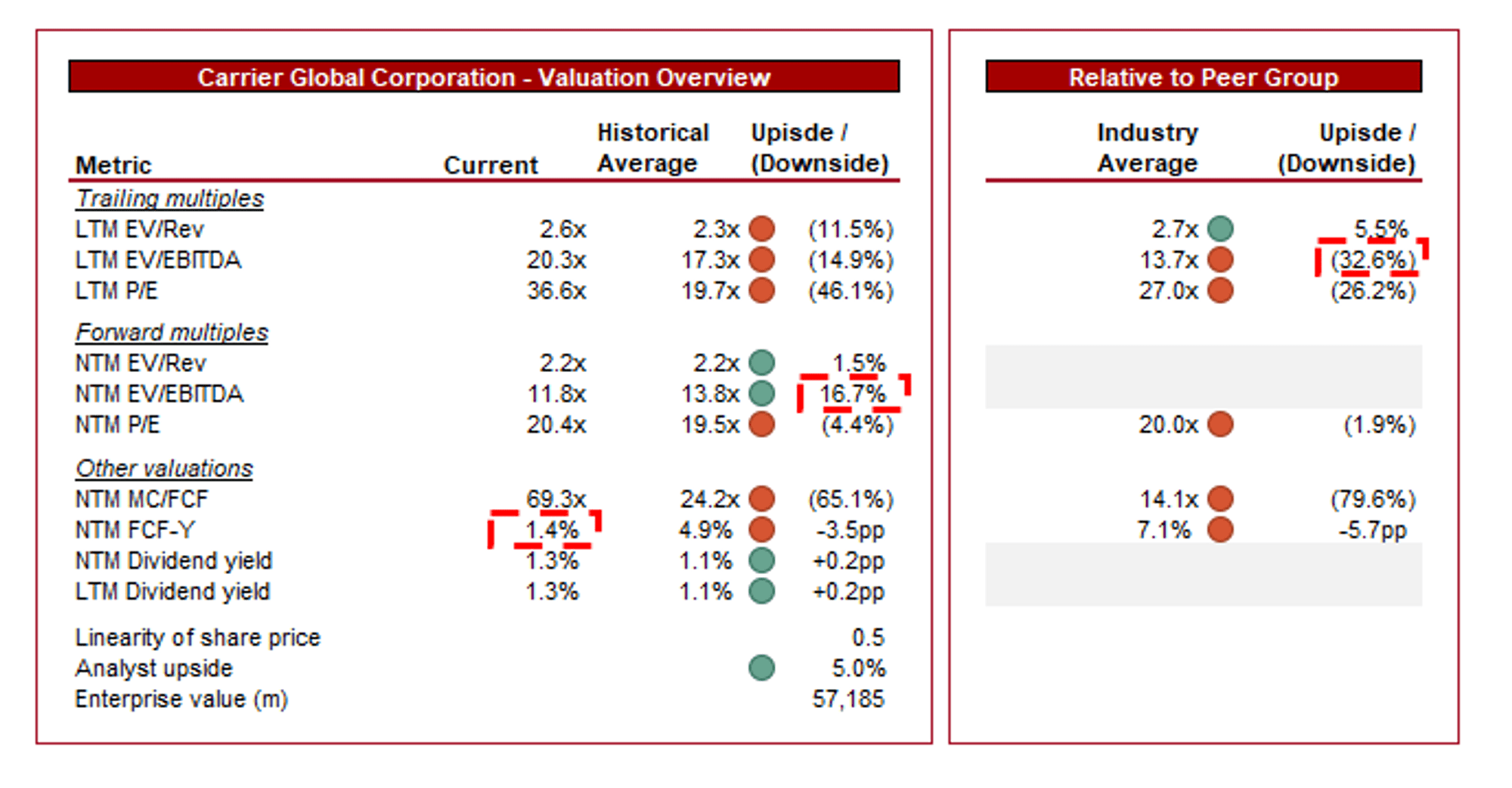

CARR is currently trading at 20x LTM EBITDA and 12x NTM EBITDA. This is a discount to its historical average on a NTM basis.

A discount to its historical average is warranted in our view, primarily due to the margin risk given CARR has historically operated at an EBITDA-M in excess of 15%.

Further, the company is trading at an LTM EBITDA premium of ~33%, declining to ~2% in the forecast period. The LTM premium here is slightly misleading due to the impact of the acquisition and how CARR’s financial profile will change. The company is currently essentially trading in line with its peers when you consider the NTM valuation, which implies it is broadly within the range of its fair value we feel.

Key risks with our thesis

The largest risk to CARR currently is the integration of its acquisition. This can be highly successful or a resounding failure based on how Management executes over the coming years.

Final thoughts

CARR is a high-quality business, owing to its strong commercial position in the HVAC industry and global reach. The company is currently going through a transformation exercise, which coincides with growing industry tailwinds, positioning CARR for long-term success.

We are broadly positive about the developments ahead, while challenging other decisions. With such a large execution, it is incredibly difficult to assess how things will actually play out. Importantly for us, we do not see sufficient margin of error, implying a hold rating.

Q2 2024 Earnings Call Transcript")