OpenRangeStock/iStock via Getty Images

I covered SNDL (NASDAQ:SNDL) last April and gave the company a Hold rating. The stock has gained 26.81% since my coverage. Most of the gain occurred in the last thirty days and surrounds the current cannabis sector rally. I continue a Hold rating for SNDL and will consider in this article some of the factors weighing down on the US and Canadian cannabis markets. SNDL’s recent Q4-2023 earnings release gives us insight into some of the important issues.

Recent Cannabis Rally

Two events seemed to cause the cannabis sector rally last week. Analysts cited the Schumer petition as to why there was a cannabis sector rally. This event seems less important since it indicates the continued failure of our legislature to pass the SAFER Banking Act. There is still no timeline for its passage and now there is a debate around rescheduling. The other event was the passage of recreational cannabis legislation in Germany. This news would seem to apply most to Canopy Growth (CGC), since it has a direct play in German cannabis markets. As is usual with cannabis stocks, when one starts rising, the others follow.

The rally has mostly fizzled out, although a new downtrend has not yet set in. If investors want to play cannabis stocks, then one must consider the fundamental financial performance of the companies and not hype in the media. SNDL discusses in its Q4-2023 earnings report how it is in a good position financially because it does not owe back taxes on cannabis sales. The company explains that many Canadian retail cannabis companies owe an extreme amount of excise tax and that this debt will ultimately force those companies to go out of business.

SNDL believes that the Canadian cannabis markets will consolidate over time and that it will be there to subsume the losers into its fold. The point here is that the Canadian cannabis markets are experiencing negative growth and shrinkage. The negative growth includes price per gram compression and business conditions with break-even expectations. The US cannabis markets are in a similar predicament, but not because of the same reasons. The US markets are suffering from a lack of banking regulation and lack of national legalization. There too the price per gram is lowering and price compression is present.

Let’s consider SNDL’s current financial performance and see how the company aims to survive in the long-term. It has made many improvements to its business strategy, which should prove fruitful. For background on SNDL, please consult my previous coverage. During 2022 and 2023PY, SNDL completed key acquisitions and underwent restructuring. SNDL now operates in four segments: beer / liquor retail sales, cannabis retail sales, cannabis operations (growing and product manufacture), and cannabis investments.

SNDL Revenue by Segment

|

CA$ millions |

Q4-2023 |

Q3-2023 |

Q2-2023 |

Q1-2023 |

Q4-2022 |

|

Liquor Retail Sales |

159.5 |

151.8 |

151.7 |

115.9 |

159.7 |

|

Cannabis Retail Sales |

75.2 |

75.5 |

71.9 |

67.4 |

68.4 |

|

Cannabis Operations |

26.0 |

21.0 |

20.9 |

29.6 |

18.7 |

Data from SNDL’s quarterly presentations

Through acquisitions, SNDL has vastly increased its revenues and revenue potential. The numbers have shown improvement over the last five quarters. SNDL credits higher liquor and cannabis sales partially to its proprietary data analysis software, which gives insight into the best-selling and least-selling SKUs. The company highlights its improvement in cannabis operations via its acquisition of Valens, a vertically integrated cultivation and product manufacture business. Valens and its facilities have allowed SNDL to restructure its cannabis operations. SNDL has lowered its exposure to large scale cultivation and increased its procurement of flower. The company states that operations under Valens have resulted in CA$22 million in yearly cost savings. Accordingly, SNDL’s cannabis operations revenues are finally increasing from quarter to quarter.

Setting aside liquor sales, cannabis retail and cultivation revenues indicate that SNDL’s enmeshment with the market is becoming more efficient. In a shrinking market, SNDL is able to report higher revenues. The company is able to compete in the environment. As of the end of Q4-2023, SNDL reported operating 170 retail liquor locations in Alberta and British Columbia and 187 retail cannabis locations in AB, BC, MB, ON, and SK.

SNDL’s US Cannabis Interests

SNDL’s investment portfolio has a value of CA$572 million, with CA$538 million through SunStream. During Q3-2023, SunStream Bancorp launched SunStream USA. This group holds SNDL’s US cannabis interests without presenting a conflict of interest between Canadian LPs and the US cannabis markets. The group holds non-voting equity in Skymint and Parallel, including licenses in Florida, Michigan, Massachusetts, and Texas. Once US law allows it, SNDL will have voting control in these companies. The structure of SunStream USA is still under review by NASDAQ.

SNDL reports its income or loss per quarter on its investment portfolio. The data is part of its long-term investments and investment income (other income). It is not reported under revenue. SunStream is important in the long-run for SNDL’s entrance into US markets and for its future success.

SNDL’s Q4-2023 Earnings Results

SNDL reported Q4-2023 net revenue of CA$249 million, representing a 3% increase YoY (Q4-2022 = CA$240 million). Gross profit of CA$57 million sets a new record and represents 23% of total sales. The company attributes higher profit partially to the closing of its Olds cultivation facility in Alberta and further optimization of its supply chain.

Cannabis retail sales for Q4-2023 were CA$75 million compared to CA$68 million representing a 10% increase YoY. Same store sales increased 2% for the quarter. Gross profit on cannabis retail sales was CA$20 million, an increase of 27% YoY.

Cannabis operations net revenue for Q4-2023 is CA$26 million, representing a 112% increase YoY and 24% increase QoQ. Besides reorganizing its cannabis operations, SNDL decreased is cannabis SKUs from 327 to 125 products.

Liquor retail revenue for Q4-2023 is CA$159.5 million, which was basically the same YoY and represents a 5% increase QoQ. Private label liquor sales increased 19% YoY and 20% QoQ. The company is using white label products to increase its margins.

Operating income was a loss of CA$85 million, which included CA$29 million restructuring costs and write-offs and CA$29 million in goodwill impairments. Operating loss improved 45% YoY (Q4-2022 = negative CA$155 million).

The company reports positive free cash flow for Q3 and Q4-2023. For Q4-2023, the company reports CA$1.4 million in positive free cash flow. Combined with Q3-2023, the company reported a total CA$17.7 million positive free cash flow for 2023PY. The company also reports a positive EBITDA of CA$3.5 million, representing a 147% increase YoY.

The company reports CA$766 million in cash and short-term investments. SNDL says that its net book value is CA$1.2 billion. SNDL is still debt-free and owes no back taxes on Canadian retail cannabis sales.

Market estimate for SNDL’s Q1-2024 revenue is CA$209.30 million, which will represent a slight increase YoY and a decrease QoQ.

SNDL’s Historical Financial Performance and Valuation

|

Amounts in CA$ millions |

Q4-2023 |

Q3-2023 |

Q2-2023 |

Q1-2023 |

Q4-2022 |

|

|

Revenues |

248.5 |

237.6 |

220.5 |

202.5 |

240.4 |

|

|

Cost of Revenues |

191.1 |

189.0 |

168.6 |

169.9 |

196.8 |

|

|

Gross Profit |

57.3 |

48.6 |

51.9 |

32.5 |

43.6 |

|

|

Operating Expenses |

73.3 |

72.5 |

74.2 |

70.8 |

71.5 |

|

|

Net Income |

(82.8) |

(21.8) |

(32.5) |

(35.6) |

(125.8) |

|

|

Cash and ST Investments |

198.7 |

205.6 |

212.0 |

247.2 |

308.1 |

|

|

Accounts Receivable |

30.0 |

29.1 |

36.3 |

37.4 |

26.3 |

|

|

Total Current Assets |

406.9 |

423.7 |

459.7 |

492.9 |

501.5 |

|

|

Long-Term Investments |

568.0 |

579.6 |

542.5 |

545.9 |

610.0 |

|

|

Total Assets |

1,473.2 |

1,563.3 |

1,571.8 |

1,617.7 |

1,559.4 |

|

|

Accounts Payable |

22.0 |

57.2 |

62.6 |

62.1 |

9.8 |

|

|

Current Liabilities |

103.1 |

97.8 |

102.5 |

100.7 |

89.4 |

|

|

Total Liabilities |

243.8 |

241.9 |

243.9 |

248.5 |

231.7 |

|

|

Book Value Per Share US$ |

$3.48 |

$3.68 |

$3.79 |

$3.84 |

$4.10 |

|

|

Book Value US$ |

769.6 |

794.7 |

819.6 |

841.4 |

860.0 |

|

|

Free Cash Flow CA$ |

11.29 |

24.50 |

(10.09) |

(50.19) |

24.60 |

|

|

Current |

||||||

|

NTM Total EV/Revenues |

0.63x |

0.60x |

0.61x |

0.41x |

0.57x |

0.68x |

|

Price US$ |

1.75 |

1.64 |

1.90 |

1.37 |

1.60 |

2.09 |

|

Total Enterprise Value US$ |

449.52 |

416.32 |

479.81 |

318.48 |

416.13 |

487.91 |

|

Market Cap US$ |

460.40 |

427.20 |

494.87 |

356.55 |

422.72 |

494.49 |

|

Stock Price Target Mean US$ |

4.95 |

4.96 |

4.38 |

4.37 |

4.66 |

4.65 |

Financial Data from Seeking Alpha. Valuations from TIKR.com

Over the last five quarters, SNDL has reported consistent results, both consistent profit and consistent net loss. It is as positive sign to see the company reporting free cash flow, but one would also want to see net income reported. Since I began my coverage of SNDL some years ago, the company’s financials have improved overall and shown more efficiency in expenses and higher profits.

SNDL is undervalued by US$300 million or $1.73 per share. The company’s stock trades at $1.75 per share and its book value is $3.48 per share. The company’s total enterprise value of US$460 million is more than half of the company’s current long-term assets. The current market mean target price for SNDL is $4.95 per share. Current market volatility and cannabis sector volatility will likely keep SNDL’s stock price down and undervalued.

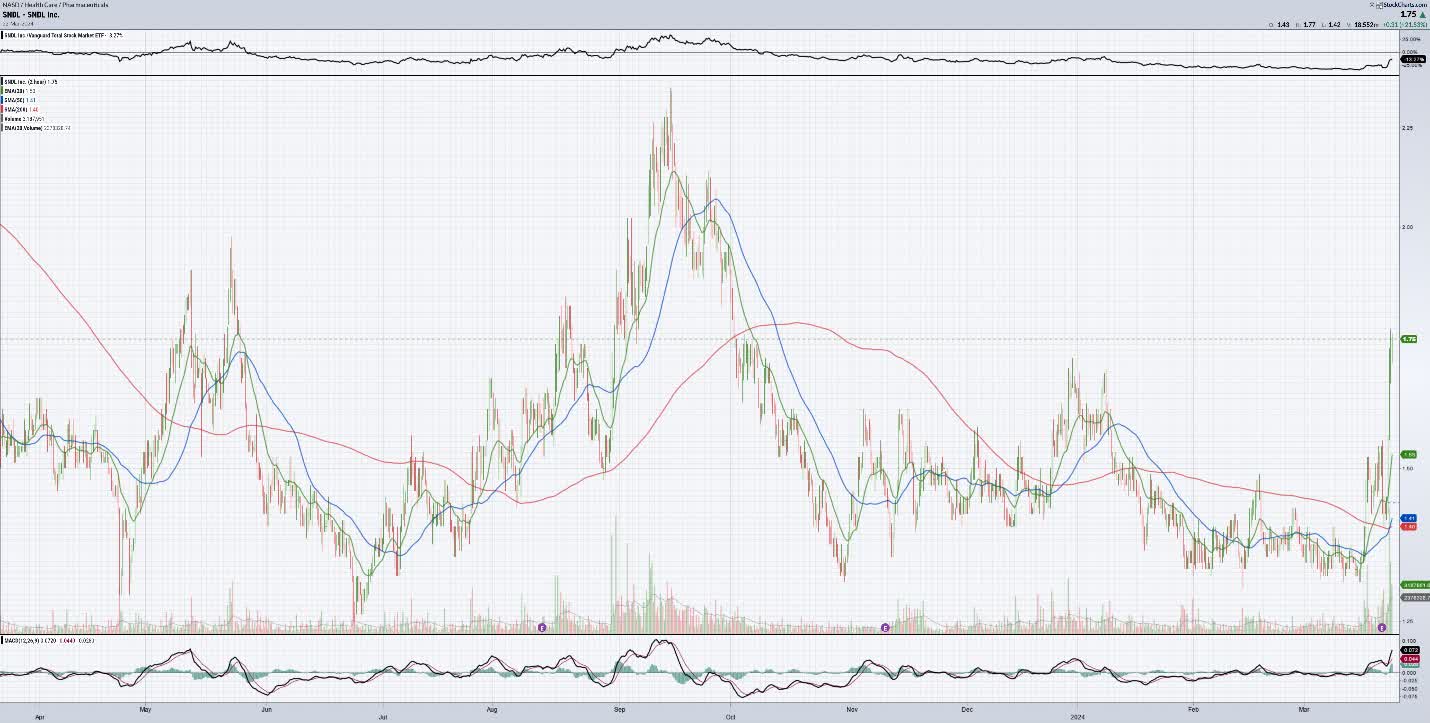

SNDL’s 1-YR Stock Price Movements

StockCharts.com

SNDL’s stock price has resided in the $1.00 to $2.00 price channel for the last year. The short-lived rally last September surrounded news of possible cannabis rescheduling in the US and brought SNDL’s stock price above $2.00 per share. The recent rally brought the price to $1.75 per share.

The company’s stock price is up 10% over 1-yr, 12% over 3-mo, 26% over 1-mo, and 16% over the last five days. The stock is currently trading over its 20/50/200 moving day averages. The company’s stock has low institutional ownership (only 5.5%). Momentum remains low for SNDL and the company’s stock has not recovered from its reverse split back in July 2022.

Investment Strategy

SNDL is at low risk of ill financial performance. Its revenue streams through its various segments will be present for many years to come. SNDL has plenty of resources to fulfill its current business strategy and future plans. The company has no debt and no back taxes. It half billion in cannabis investments show long-term potential.

An investment in SNDL’s stock comes at a moderate to high risk of ill performance due to market volatility. Even a long-hold position is at risk of further loss. I rate the stock as a Hold because the company’s finances are improving and because cannabis investors are awaiting key events to unfold, like US legalization. I feel that there is long-term potential in SNDL and its strategy. Holding the stock now will allow one to be prepared for future rallies and positive financial performance.

Conclusion

SNDL has shown marked improvement in its financial performance over the last year. Its Q4-2023 earnings results show an increase in revenue and profit, as well as positive free cash flow. SNDL is well positioned for US cannabis market entry when the time is right. The company’s previous restructuring is now bearing fruit. At the same time, cannabis sector stocks remain volatile and US legalization news is not forthcoming. The current rallies in cannabis stocks are short lived. Because of greater market volatility, I rate SNDL as a hold, which comes at a risk of loss. I am still hopeful that there are good things to come with US legalization and the opening of international markets. SNDL is ready for the larger game.

Q2 2024 Earnings Call Transcript")