Andrii Dodonov

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Municipal Bond Fund (NYSE:EIM) suffered substantial losses like many of its peers when the Fed was hiking rates aggressively. Being a leveraged fund added further pressure due to the Fed raising short-term rates, causing the borrowing rate on their floating rate notes to climb materially. Risk-free rates shot higher, and that meant the underlying portfolio of long-duration municipal bonds shot lower.

Today, the fund’s discount looks appealing and a recent distribution increase could be a catalyst to see that narrow. However, this distribution bump doesn’t look like it came out of nowhere. Instead, we see an activist group targeting this fund heavily more recently, similar to several of its muni CEF peers.

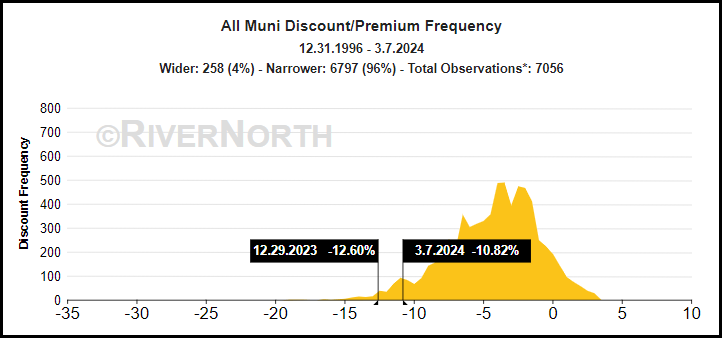

In general, municipal bond funds overall are the most heavily discounted in the entire closed-end fund space. The average discounts for muni bond CEFs have only been wider 4% of the time since 1996, according to RiverNorth’s data.

Muni CEF Discount/Premium Compared to Historical Levels (RiverNorth)

EIM Basics

- 1-Year Z-score: 2.14

- Discount: -10.12%

- Distribution Yield: 5.41%

- Expense Ratio: 1.05%

- Leverage: 30.83%

- Managed Assets: $1.2 billion

- Structure: Perpetual

EIM’s investment objective is to “provide current income exempt from federal income tax.”

They intend to achieve this through:

… at least 80% of the Fund’s net assets will be invested in municipal obligations, the interest on which is exempt from federal income tax, including the alternative minimum tax (“AMT”), and that are rated A or better by Moody’s Investors Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”). The foregoing 80% policy may not be changed without shareholder approval. Under normal market conditions, the Fund expects to be fully invested (at least 95% of its net assets) in accordance with its investment objective. The Fund may invest up to 20% of its net assets in municipal obligations rated BBB/Baa or below (or unrated obligations deemed by the Fund’s adviser, Eaton Vance Management (“Eaton Vance”), to be of equivalent quality), provided that not more than 15% of its net assets may be invested in municipal obligations rated below B (or unrated obligations deemed by Eaton Vance to be of equivalent quality) and may invest up to 20% of its net assets in bonds on which the interest is subject to the AMT. When a municipal obligation is split rated (meaning rated in different categories by Moody’s, S&P or Fitch) the Fund will deem the higher rating to apply

When including the fund’s interest expense for borrowings, the total expense ratio comes to 3.17%.

Recent Distribution Bump Looks Like Activist Pressure

The pressures of higher borrowing costs naturally led to several distribution cuts throughout 2022 and into 2023. According to their latest annual report for fiscal year-end 2023, the fund’s cost of the leverage on their floating rate notes was pushing into the 4% range.

EIM Leverage Costs (Eaton Vance (highlights from author))

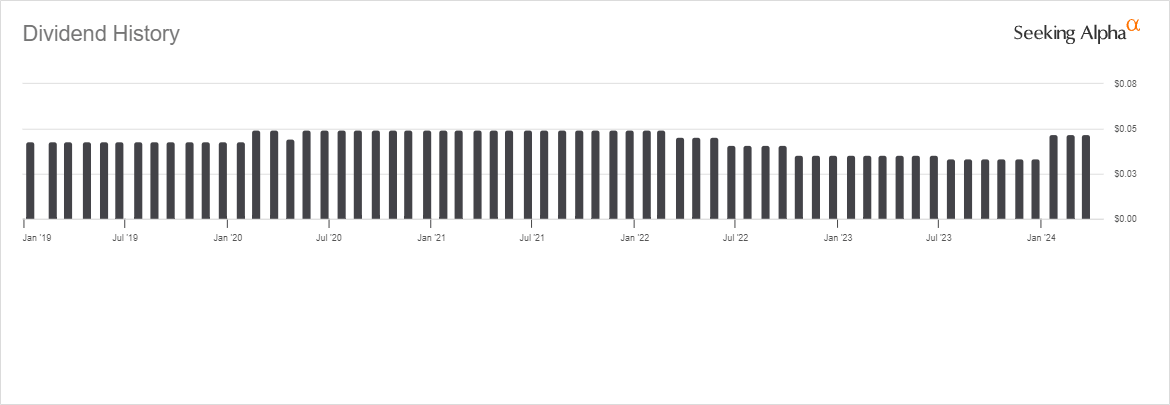

However, more recently, the fund has increased its distribution quite substantially. This is also similar to a number of other muni CEF peers. The increase took the distribution from $0.0333 per month to $0.0468, which amounts to an increase of over 40%. That’s certainly massive. It doesn’t put it back to the pre-hiking cycle high distribution amount of $0.0496, but it is close.

EIM Distribution History (Seeking Alpha)

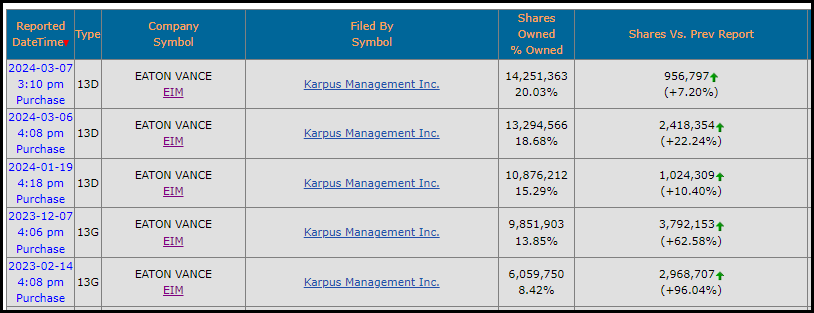

This is happening despite not getting any rate cuts, yet even that would naturally see net investment income rise once more. Instead, similar to its peers, this fund seems to have become a target for the activist group Karpus Management. They have recently crossed over 20% ownership of this fund.

EIM Activist Ownership (SecForm4)

Since we haven’t seen net investment income rise just yet — though it should when rates are cut — that simply means that distribution coverage has slipped.

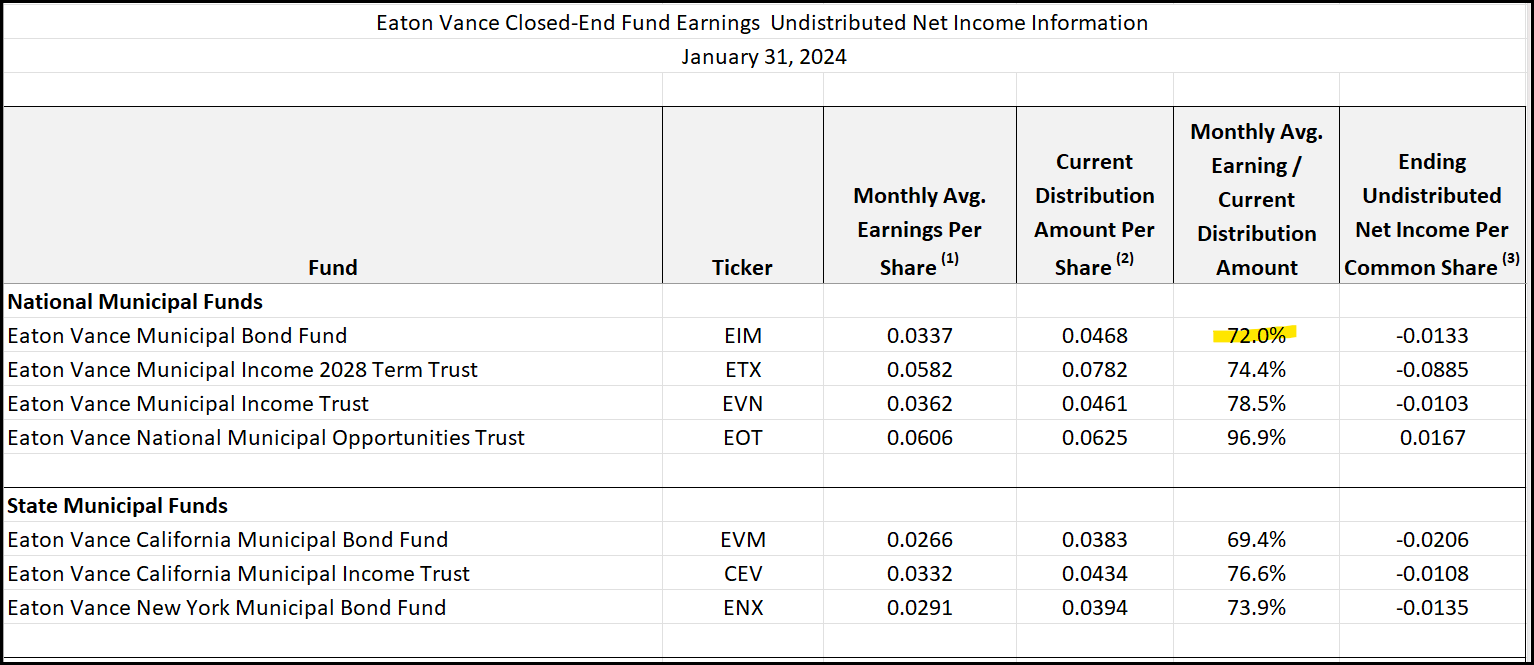

NII coverage based on the last three months for the period ended January 31, 2024, came to 72%. Ideally, we’d want to see this at over 100% for fixed-income funds, as most of the distribution should be covered by the recurring interest payments from the underlying portfolio.

EIM Distribution Coverage (Eaton Vance)

The one national muni fund that didn’t increase its distribution was Eaton Vance National Municipal Opportunities Trust (EOT), which sports a relatively stronger distribution coverage of nearly 97%. At the same time, Eaton Vance Municipal Income 2027 Term Trust (ETX) and Eaton Vance Municipal Income Trust (EVN) also saw distribution increases. Their coverage dropped as well, but they don’t appear to have any significant activist pressure.

A three-month period can have some variability and cause some lumpy data, so looking back at the last annual report, per share, NII came to $0.39. Bearing in mind the fiscal year-end, here is September 30, so there were more rate increases in this period, meaning that NII would have likely been under further pressure. Still, that would put NII coverage based on the current annualized payout of $0.5616 at about 70%.

Distribution Coverage Looking Forward

The average borrowing rate for those floating rate notes we can safely assume is around 4% now based on the last reported average of 3.56%, but where the range listed above is probably more accurate on the higher end.

We’ll use 4% for simplicity’s sake. Based on their borrowings of $356,644,991, if rates are cut by 25 basis points, their borrowings should drop by a similar amount. That would put the cost for these notes at $13.374 million for a 12-month period, down from a $14.266 million current annualized cost. That isn’t necessarily too much in terms of leverage cost savings, but it does work out to about $0.0125 per share. With 75 basis points of cuts that are expected this year, we could see $0.037. Still, nothing too substantial, but it would all help.

These are just to give a rough idea of what changes in interest rates can do to the fund. What we can’t predict is exactly what the management team will do. Portfolio turnover in the last year was actually quite high at 52%. That was the highest in five years.

Further, adding or reducing the amount of floating notes outstanding would impact these numbers as well. This actually was the case as the fund’s average borrowings over the last FY was $481.541 million, but at the end of the FY, we saw borrowings standing at $356.645 million.

Either way, the main takeaway is that lower rates will help with distribution coverage by increasing NII. We are expected to be at peak rates for this cycle, so the idea of seeing rate cuts over the next year or two is a high probability.

Another added benefit should be that if risk-free rates fall alongside the reduction in short-term rates, that could add a boost to the portfolio’s underlying portfolio. This is largely why muni CEFs look so appealing right now. The largely tax-free distribution rate of 5.41% is enticing, but there could be some capital gains to be made along the way over the coming years.

I believe that’s why Saba Capital and Karpus are targeting muni funds, as they look like a win-win situation. The big negative would be if rates do need to go higher, then we could see further downside pressure.

However, increasing the fund’s distribution now without coverage simply reduces the fund’s coverage. The longer this current payout is sustained, the more the fund’s NAV can be expected to erode. So, getting a reduction in rates sooner rather than later would be beneficial.

A Look At Valuation: Another Potential ‘Bonus’

Finally, the other ‘bonus’ added to muni CEFs right now is going back to those historically wide discounts. Investors can get 5% risk-free currently, so looking at leveraged funds – even after the increase coming in around 5.5% isn’t enticing enough for some investors, given the potential for losses.

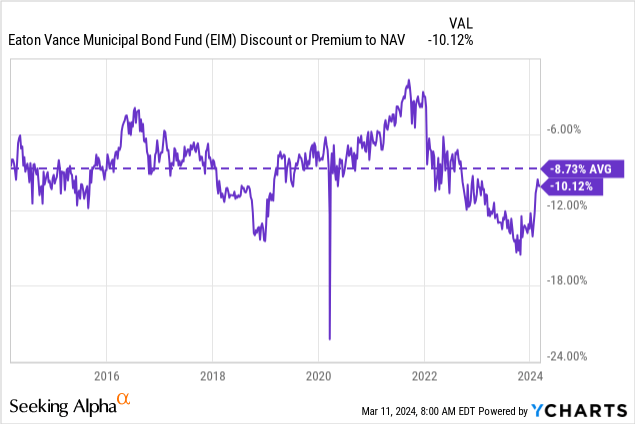

In the case of EIM, it certainly is trading at a historically wide discount similar to its sector peers. With the latest distribution bump, we already saw just how enthusiastic investors can get. The discount came off of some of the widest levels it has ever touched in the last decade. This is a case where the negative 1-year z-score is quite elevated, but this is a case where there is a specific catalyst that warrants such a move.

YCharts

Of course, depending on one’s tax bracket, the taxable equivalent yield will be more competitive. In the 24% bracket, you are looking at a TEY of just over 7% currently.

On that subject, though, it does get a bit murky and not as straightforward. Since they are overdistributing, they are starting to pay out the return of capital distributions. With the latest increase, that amount of ROC should increase this year. ROC distributions are more tax-deferred rather than tax-exempt because it reduces an investors cost basis.

EIM Distribution Tax Character (Eaton Vance (highlights from author))

So, in that situation, you could end up creating a capital gain when going to sell.

Conclusion

EIM looks to be another target of an activist group. After Saba had targeted a number of CEFs in the municipal bond space, Karpus took the lead on EIM. This isn’t their first foray into this fund, though. In 2019 and 2020, they held a sizeable position as well. EIM, at that time, ended up conducting small tender offers, which resulted in three total conditional tender offers. The first was 10% of the fund at 98% of NAV, and the second and third was 5% for 98% NAV. Karpus never entirely sold out, either; instead, they maintained around a 4.3% weighting over all these years.

Their interest first picked up in early 2023, but now, in the last quarter or so, they’ve become much more aggressive. Whether they force any sort of tender offer remains to be seen, but it appears that the pressure has led to a distribution increase, at the very least. With that distribution bump came weaker coverage but a much narrower discount for shareholders. In general, muni CEFs look like appealing investments at this time, given the expectation for lower rates to come.

Q2 2024 Earnings Call Transcript")