VIDOK/iStock Unreleased via Getty Images

The Western Union Company (NYSE:WU) recently reported a new agreement with a large credit card company to send money to card holders. With this relevant net income driver, I think that recent stock repurchases or the use of artificial intelligence to enhance customer experiences could bring significant stock demand. The 5 year dividend growth rate of 4.07% may also bring the interest of new investors. There are obvious risks coming from geopolitical tensions, goodwill impairments, or regulatory changes. However, I do believe that the company appears quite cheap at close to 9x Non-GAAP TTM earnings.

Western Union

Western Union is a recognized money and parcel remittance company providing services in accordance with international standards. Digital financing instances have been added to its services in recent years based on market trends in general. By the end of 2023, the company reached 400,000 active agencies across 200 countries, serving clients ranging from individual consumers to large companies that use Western Union to facilitate monetary transactions and cross-border shipments of products.

The operations of WU are carried out via two segments; Monetary Transactions segment and Consumer Services segment. The Monetary Transactions segment represents the highest percentage of income on an annual basis for the company. The Consumer Services segment, which represents a smaller percentage of the company’s activities, is dedicated to the administration and collection of activities related to customer service.

The Monetary Transactions segment offers the possibility of sending physical money through its network of agencies with an international presence and the possibility of making payments and transactions digitally in some countries. In any case, retail activity continues to prevail over digital options, although the company directs its efforts towards the development of platforms that offer services in this regard. The particularities of this segment highlight that sending money can occur in diverse ways that are not only limited to physical money, but payments can be made with credit and debit cards as well as different lines of financing so that another person receives the money physically in one of the authorized agencies. The company’s income comes from the collection of commissions from the sender of the payment and the recipient.

On the other hand, the Consumer Services segment, which represents a smaller percentage of the company’s activities, is aimed at offering retail solutions such as tax payments through its platforms or digital wallet services among others.

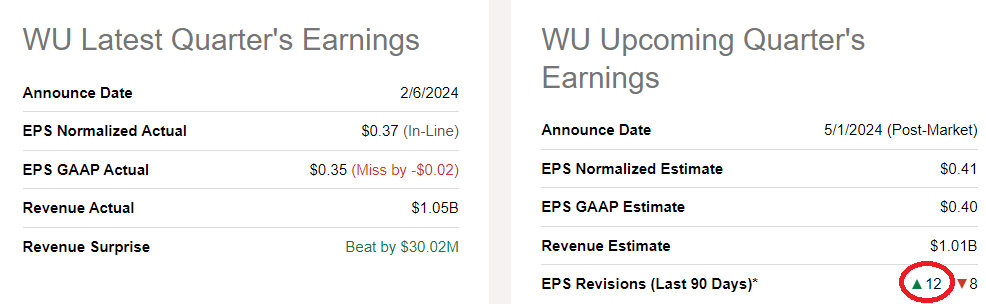

I believe that WU is a must-follow stock because of the recent earnings reported and recent increase in EPS earnings expected. With quarterly revenue of $1.05 billion, which was better than expected, 12 analysts increased their EPS expectations in the last 90 days. 2025 EPS expectations stand at about 1.78%, which would represent growth of about 4.4%. With these figures in mind, I believe that there is significant optimism around this ticker.

Source: Seeking Alpha Source: Seeking Alpha

Balance Sheet

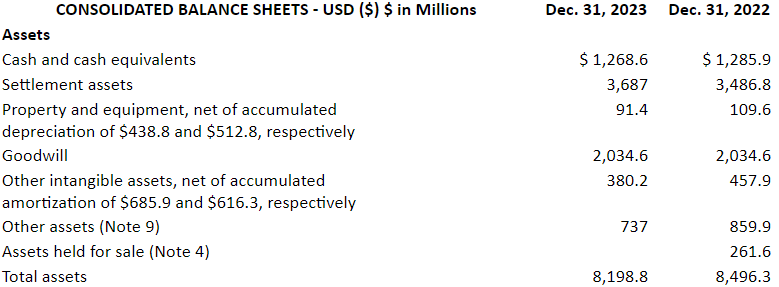

As of December 31, 2023, the company reported a significant amount of cash in hand, close to $1.2 million. Moreover, the asset/liability ratio is larger than 1x. Hence, I do believe that the balance sheet appears quite stable.

Source: 10-k

Furthermore, with goodwill close to $2 billion, WU appears to be quite active in the M&A markets. Given the total amount of cash, I expect acquisitions in the coming years, which may accelerate net sales growth and economies of scale. The last annual report noted that the company may acquire new targets. Besides, the current Executive Vice President reports expertise in Mergers and Acquisitions.

We have acquired and may acquire businesses both inside and outside the United States. Source: 10-k

Benjamin Adams is our Executive Vice President, Chief Legal Officer. From 2007 to 2015, Mr. Adams served as Assistant General Counsel, Global Commercial Lead for Microsoft Corporation and held various senior legal positions at Nokia Corporation, including Head of Legal, Americas Region, Head of Legal, India and Emerging Market Services, and Head of Legal, Mergers and Acquisitions. Source: 10-k

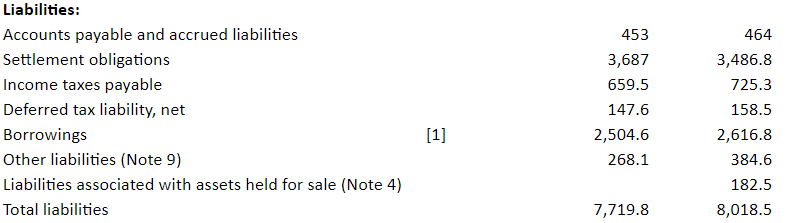

Borrowings are not small. However, the management did reduce the total amount of debt in 2023. As of December 31, 2023, the total amount of debt declined to about $2.504 billion. Total liabilities stood at close to $7.7 billion, which are lower than that in 2022.

Source: 10-k

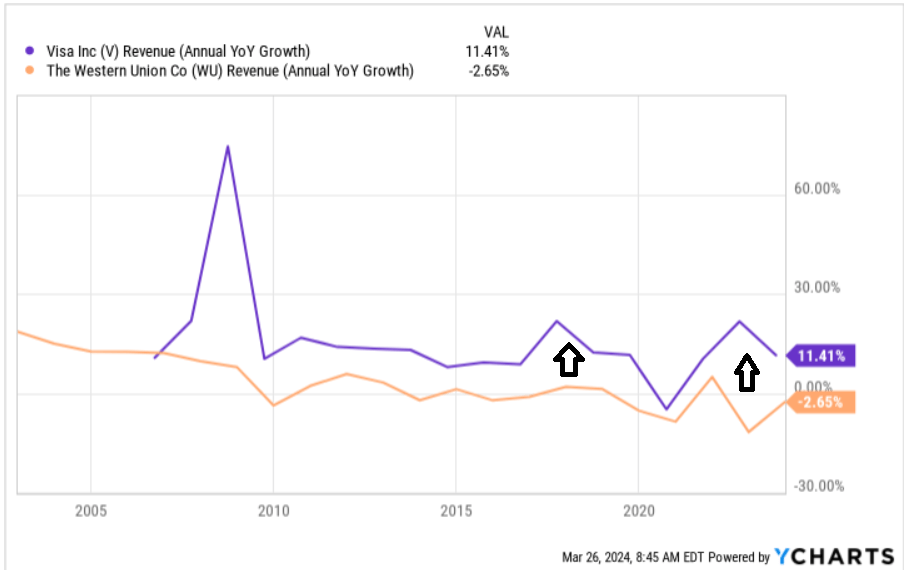

Assumption 1: Digitalization, And The Recent Agreement With Visa (V) Could Bring Net Sales Growth Of Close To 7% In The Base Case Scenario

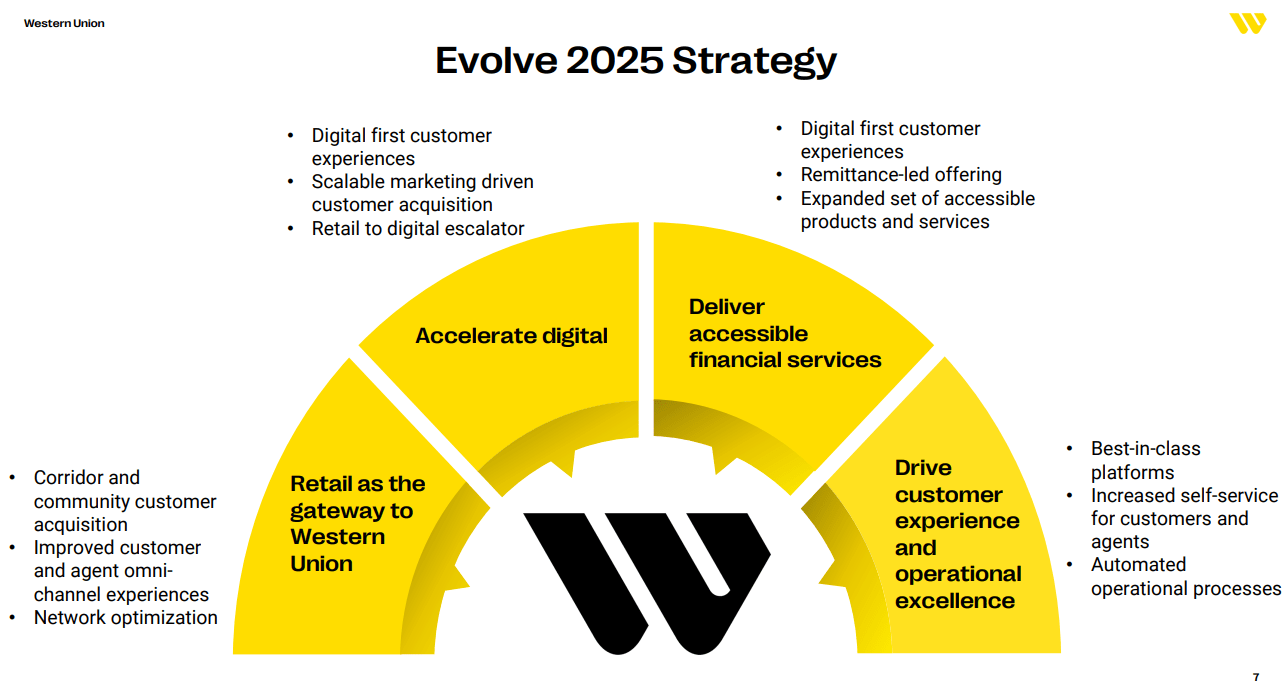

In the long term, Western Union’s strategy is aimed at strengthening the digital part of its business by responding to the trends of the decrease in the use of physical money and the increase in retail transactions at an international level. In addition, the company expects to accelerate digital efforts with new customer experiences, scalable marketing efforts, and network optimization. In the last presentation, WU offered the following information in this regard.

Source: Investor Presentation

I also believe that new agreements with other companies operating in the finance sector like Visa could be net revenue drivers. In particular, the fact that clients could send money to Visa card holders could bring a lot of new revenue. Visa signed a 7-year agreement with WU, applicable in 40 countries across five regions. Western Union clients could receive Visa prepaid cards in certain jurisdictions. In addition, new programs will help clients from ONGs and governments offer financial support during emergency situations. Under the agreement, WU could benefit from existing integration with the Visa Direct platform. Clients in the US and Europe will be able to send money to Visa cardholders. Considering the number of clients using Visa cards, in my view, economies of scale could enhance WU’s net sales growth..

Visa’s global scale and Western Union’s digital capabilities are revolutionizing how customers send funds around the world. We are proud to offer more people fast and efficient solutions for cross-border payments. Source: Press Release

Visa reported sales growth of more than 16% in the past. With these figures in mind, I assumed that Western Union will be able to deliver close to net sales growth close to 7% in the base case scenario, and close to 1% in the worst case scenario.

Source: YCharts

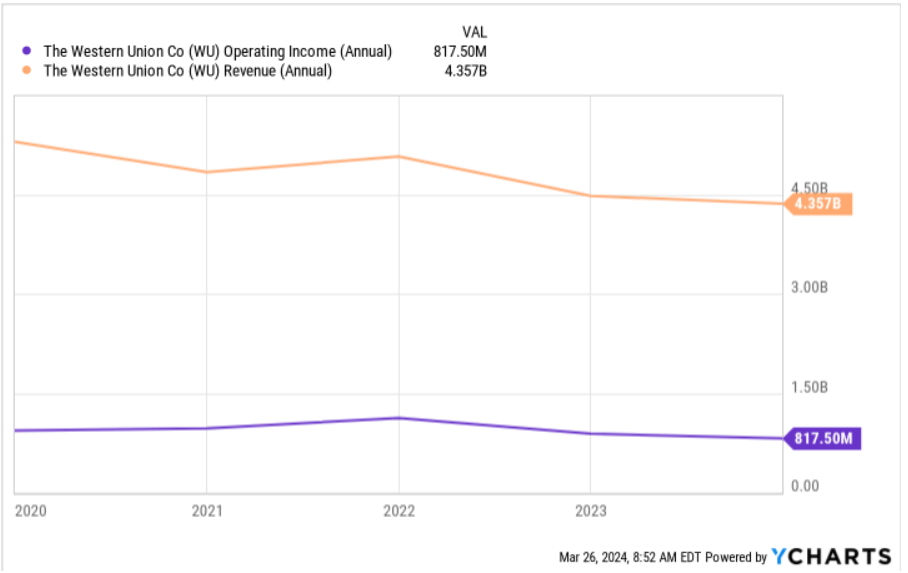

Assumption 2: Expense Redeployment Program Could Bring An Operating Income/ Revenue Close To 19%

During 2023, the company decided to sell the business solutions segment, which represented a very minor percentage of its total annual revenue, remaining in charge of the money transfer and consumer services segments, through which it organizes the entire business. In addition, the company recently delivered a significant number of transformative measures that I believe could lead to net income increases in the coming years.

Over the past few years, we have been engaged in restructuring actions and activities associated with business transformation, productivity improvement initiatives, and expense reduction measures. Source: 10-k

It is also worth noting the operating expense redeployment program, which is expected to reduce total operating expenses from now to 2027. As a result, I believe that we could see increases in net income, and operating income/ revenue close to 19%.

We announced an operating expense redeployment program which aims to redeploy approximately $150 million in expenses in our cost base through 2027, accomplished through optimizations in vendor management, our real estate footprint, marketing, and people costs. We may implement additional initiatives in future periods. Source: 10-k

Source: YCharts

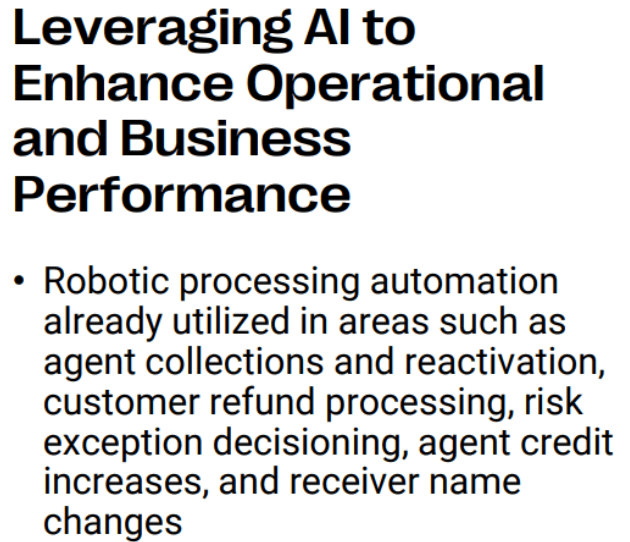

Assumption 3: Artificial Intelligence, And Machine Learning May Bring Net Income Growth

I believe that the recent efforts to develop artificial intelligence and machine learning to enhance agent collection, customer refunds, and risk management could bring revenue growth and FCF margin growth. In this regard, it is worth noting that the company, in the last quarterly presentation, also noted robot processing and leveraging AI in the works.

Source: Investor Presentation

WU is also using AI to better understand the behavior of employees as well as to enhance the communication process with teams all over the world. As a result, I think that WU may be able to better train new employees. New strategies with regard to customer engagement, customer retention, operational excellence, and other revenue drivers could be a bit more controlled. As a result, I assumed that WU will be able to deliver net income growth.

We assess employee engagement regularly, and our employee engagement system utilizes periodic surveys, artificial intelligence, and machine learning to help leaders better understand what our employees are thinking, what they value, and what they need. Source: 10-k

One of our ongoing goals is to foster greater communication to help ensure that our employees are informed, believe that their concerns are heard, and feel empowered to make decisions. Source: 10-k

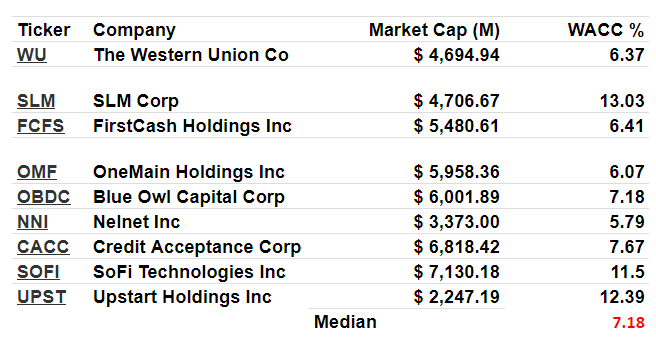

Assumption 4: Share Repurchases Could Bring Demand For The Stock, Lower Cost Of Capital, And A WACC Of 8.6%

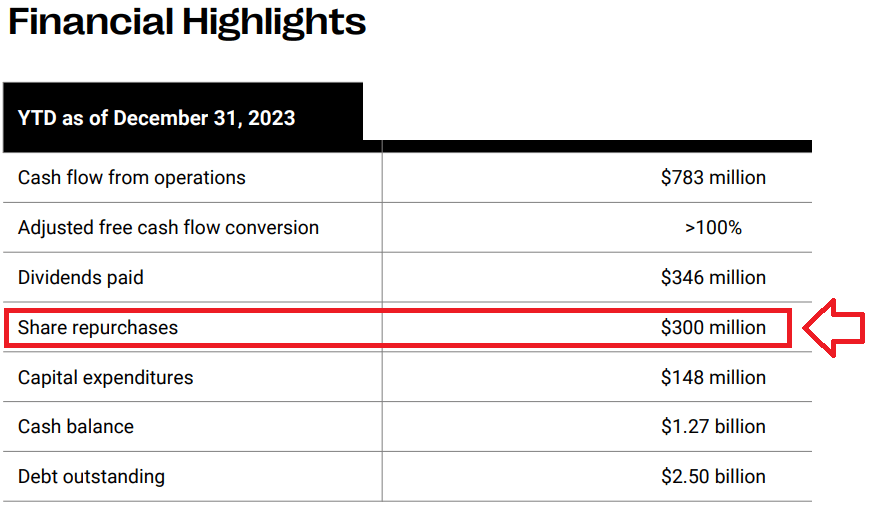

The company continues to acquire its own shares, which I believe could have positive effects on the valuation of WU. First, there is the demand created by the stock repurchase program, but there is also the demand created by other investors, who buy WU shares because the company is buying shares. At the end of the day, a company that buys its own shares sends a beneficial message to the market so that investors may think that the shares are cheap. In 2023, the company acquired stock valued at $300 million.

Source: Investor Presentation

Under my base case scenario, I assumed that stock repurchases may bring stock demand, lower cost of capital, and WACC close to 8.6%.

My Base Case Scenario Based On Previous Assumptions Implied A Valuation Of $22 Per Share

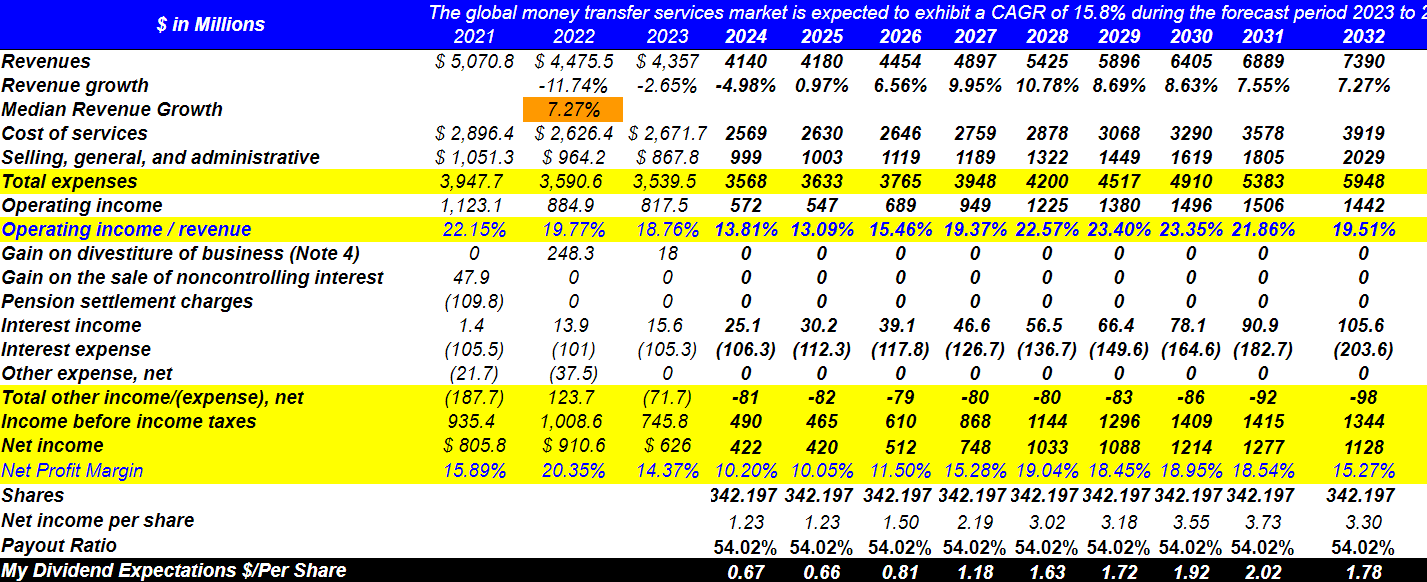

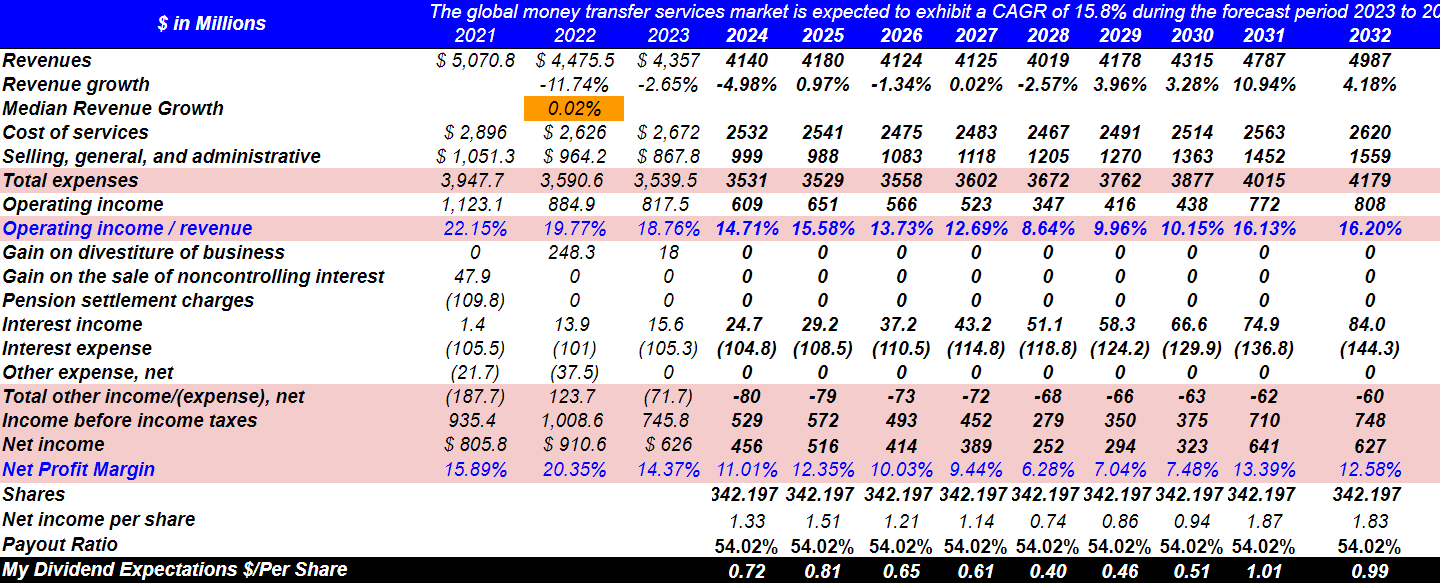

Under my base case scenario is based on my previous assumptions. I included 2032 revenues of about $7390 million, with revenue growth close to 7.26%. Median revenue growth was assumed to be close to 7.2%, which I believe is a conservative figure. I also took a look at the figures reported by other analysts, previous net sales growth, and inorganic growth.

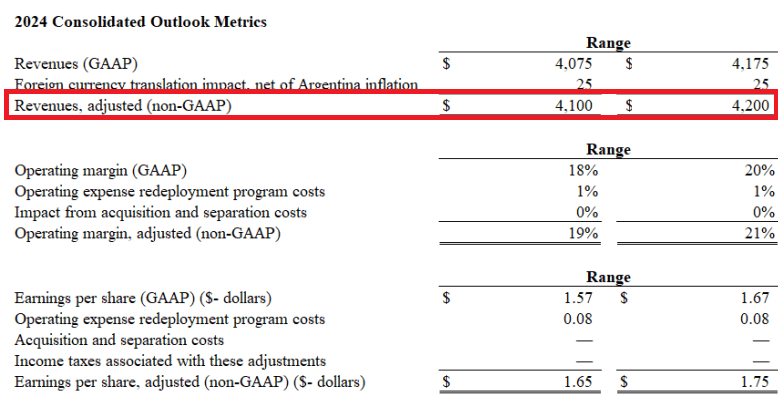

I believe that it is worth having a look at the beneficial 2024 outlook given in the last quarterly presentation. Revenue GAAP is expected to be close to $4.17 billion, with an operating margin GAAP of around 18%-20% and EPS of close to $1.65-$1.75. My numbers are not that far from WU’s expectations.

Source: Investor Presentation

With market experts noting that the global money transfer services market could grow at close to 15.8% CAGR from now to 2032, I believe that the sales growth included in this scenario makes sense.

The global money transfer services market is estimated to be valued at USD 110.8 billion by 2032 from USD 26.5 billion in 2022. It is expected to exhibit a CAGR of 15.8% during the forecast period 2023 to 2032. Source: Marketresearch

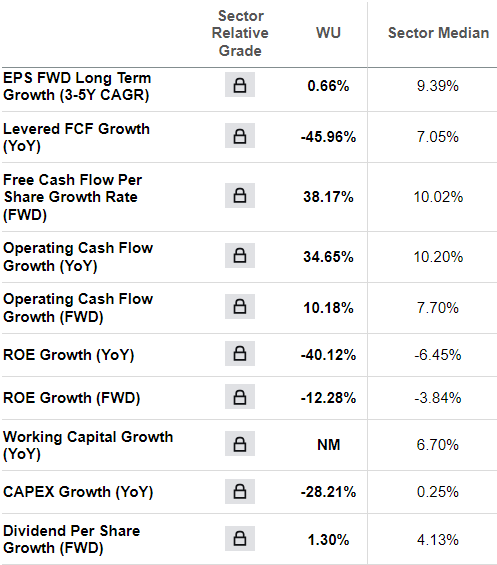

For the assessment of the income statement, I also took into account the growth statistics, the profitability grade, and underlying metrics offered by Seeking Alpha.

Source: Seeking Alpha

With the previous assumptions, I also included cost of services of $3918 million, selling, general, and administrative costs of about $2029 million, and total expenses close to $5947 million. Finally, 2032 operating income would stand at close to $1442 million. Note that the ratio of operating income / revenue stands at close to 19%, which is close to the figure reported in 2023 and 2022.

With gain on divestiture of business and no gain on the sale of non-controlling interest or pension settlement charges, I did include interest income worth $105 million, with interest expense of about -$204 million. Finally, 2032 net income would stand at close to $1128 million.

If we assume a share count of close to 342 million, net income per share would stand at $3. If we also assume a payout ratio of 54%, which is in line with the previous payout ratio reported, my dividend expectations would be close to $1.78 per share.

Source: My Expectations

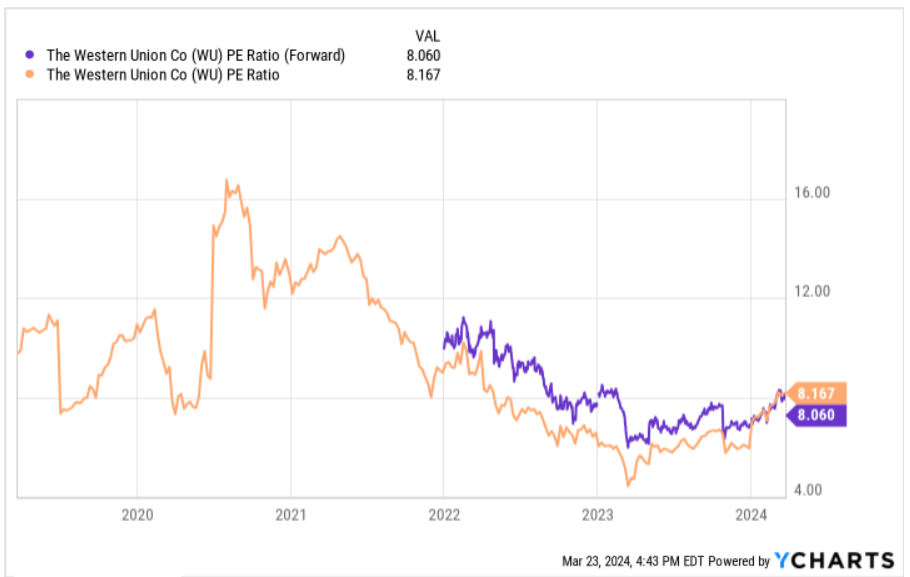

Using a dividend discount model with cost of capital of about 8.6%, I also used a 2032 PE ratio of 9x, which I believe is conservative. Note that the PE ratio in the past was close to 16x and 4x. I do believe that WU is trading a bit cheap these days at close to 8x earnings. In my worst case scenario, I assumed a valuation of 7.5x earnings.

Source: YCharts

The WACC of other competitors stand at close to 13% and 5%, but the median WACC is close to 7.1%. With these figures in mind, I believe that the cost of capital assumed appears conservative.

Source: GuruFocus

With these figures, the implied fair value per share would be close to $22. Given the current valuation of the stock, I believe that there is significant upside potential in the stock price.

Source: My Expectations

Under My Worst Case Scenario The Company’s Recent Initiatives, And My Assumptions May Fail

Under this case scenario, I assumed that the stock repurchases may not bring demand for the stock, and investors may also sell shares. As a result, the WACC would stand at close to 10%. In addition, artificial intelligence, and machine learning may not be as beneficial as expected in the base case scenario. Besides, transformation, and the expense redeployment program may fail, which may lead to lower operating income/revenue, and net income growth than in the base case scenario.

My worst case scenario includes lower net income growth than that in the previous case. Revenue growth is close to 1%. The operating income/revenue assumed is close to 18%-9%, which is not far from the figures reported by WU in the past. In sum, I think that my figures overall are a bit more pessimistic than that in the base case scenario. I do think that they are a bit less likely.

In particular, I assumed 2032 revenues of $4987 million, with 2032 revenue growth of 4%, cost of services of close to $2619 million, and selling, general, and administrative expenses of $1559 million. 2032 operating income would stand at close to $807 million, and the ratio of operating income / revenue would be close to 16%.

Moreover, assuming interest income of about $84 million and interest expense close to -$145 million, 2032 net income would be close to $627 million.

Source: My Expectations

With a cost of capital of about 10%, the NPV of future dividend payments would be close to $4. Now, with an exit multiple of 7.5x earnings, NPV of the terminal value would be close to $5.83, and the implied stock valuation would stand at $10 per share.

Source: My Expectations

Competitors

Western Union once had a large portion of the international money transfer market when digital channels did not exist and the options were limited to shipping methods or banking transactions, but the competitive environment today has changed drastically since there are multiple channels through which two people can generate economic transactions based on the increase in digital offers in this sense. This applies mostly to the retail type of transaction, but not to the transactions of large businesses.

Western Union’s competitors and similar companies include Worldline (OTCPK:WWLNF), Wise, Ebury, Flywire (FLYW), American Express (AXP), PayPal (PYPL) and MoneyGram. Source: Craft

Within this analysis, we included different banking entities as competitors; digital exchange channels either within broker platforms or digital wallets, companies that offer similar services at an international or regional level, and parcel shipping companies such as ATM.

Risks

Of course, the company’s activity is closely related to international economic activity and above all to the migration patterns through which the largest number of retail activities occur, representing a large portion of the total transactions carried out through the company’s platform. This in itself represents a risk that covers possible variations in exchange rates, although it extends to many different currencies.

On the other hand, it must be taken into account that geopolitical tensions at present can lead different countries to generate changes within their regulations regarding economic transactions and sending of parcels. Although this does not represent a major risk for the company, but it could mean complications in terms of majority markets and prevent it from achieving its profit and margin forecasts for 2024.

Considering the total amount of goodwill accumulated, I also believe that goodwill impairments may bring lower net income expectations. As a result, I believe that certain investors may lower their expectations with regard to future dividend payments, which may lower the stock price.

I believe there are also some risks from the recent acquisitions or new M&A activity. Failed integration, goodwill impairments, or lower synergies may lead to lower net sales growth than expected.

Integrating operations could cause an interruption of, or divert resources from, one or more of our businesses and could result in the loss of key personnel. The diversion of management’s attention and any delays or difficulties encountered in connection with an acquisition and the integration of the acquired company’s operations could have an adverse effect on our business, financial condition, results of operations, and cash flows. Source: 10-k

Conclusion

With many analysts out there increasing their EPS expectations, Western Union appears to be under the radar of many individuals in the financial community. I believe that 2024 guidance, the new links with Visa, the stock repurchases, and the use of artificial intelligence may explain the recent optimism about the stock. There are several risks with regard to changes in the interest rates, changes in the geopolitical tensions, lower dividend distributions, or changes in the applicable laws. With that, I believe that Western Union appears quite undervalued at a P/E GAAP TTM of about 8x and 7x forward cash flow.

Q2 2024 Earnings Call Transcript")