Stephen Lovekin/Getty Images Entertainment

Investment action

I recommended a hold rating for Korn Ferry (NYSE:KFY) when I wrote about it the last time, as I awaited further clarity on the Fed’s decision on cutting rates before I took a look at its upcoming performance. Based on my current outlook and analysis, I am upgrading my rating to a buy as the Fed message is very positive for KFY—continue to see rates being cut in 2H24. There are also growing signs of a recovery cycle up ahead that got me positive about the business. Lastly, with the KFY lower cost structure, earnings should grow faster than the top line when the upcycle really comes.

Review

KRY 3Q24 fee revenue came in at $668.7 million, a decline of 1.8% y/y on a reported basis and 2% on a constant currency basis. Revenue in executive search declined 7% y/y on a constant currency basis, dragged down by North America decline of 9%, Europe decline of 3%, APAC decline of 4%, and Latin America decline of 5%. As for consulting, revenue grew 3% y/y on a constant currency basis, supported by digital revenue growth of 6% but offset by an RPO decline of 22%. Lastly, professional search and interim revenue grew 11%. Although revenue growth was negative, EBITDA margins came in at a surprise as they expanded 110 bps to 15.2%, driven by cost efficiencies, and came in above the consensus of 14.8%. As a result, EPS saw $1.07, outperforming consensus expectations of $0.99. For 4Q24, management guided for fee revenue of $675 to $695 million and $1.09 to $1.17 in EPS.

I believe things are going well for KFY for multiple reasons. The obvious one is the Fed’s constant messaging about cutting rates. Although there are some debates about whether the Fed will really cut rates given the housing supply situation, sticky inflation, and strong labor market, I think the constant messaging to cut rates is a positive one. At the micro level, there are also multiple data points that point to an upcycle for KFY ahead. Firstly, management noted stabilizing labor market trends as inflation subsides and organizations have adapted to a high interest rate environment, which means even if the Fed doesn’t cut rates, the hiring environment is not going to get dramatically worse than before. Additionally, there has been a stabilization in the volume of executive and interim searches, as well as a 15% increase in the volume of professional searches, which are all indicators that companies are beginning to ramp up their hiring efforts. The consulting segment also witnessed a similar shift, with KFY reporting structurally higher demand for its digital solutions and consulting services as organizations shift towards a more collaborative, horizontal model, favoring cross-firm collaboration over a traditional, vertical one. The results in 3Q24 are very supportive of these datapoints as well, where new business excluding RPO improved from -4% in 2Q24 to flattish in 3Q24, and new business in Jan’24 grew 5% organically, showing strong momentum that appears to have rolled into Feb’24 as new business performed in line with internal expectations. The outlook for March was also very positive, as it is on track to be a very strong month.

Growth recovery aside, I also think that after multiple quarters of weakness, the business has become structurally stronger as well. KFY now has a much more diversified approach to acquiring businesses, which really helps when times get tough (where they may need to cut their own staff). On a year-to-date [YTD] basis, the cross-line of business referrals now represents a quarter of revenue on a year-to-date basis. Also, the business now has a lower cost profile, which makes its profit less volatile in the downcycle. We can see this from the expansion of EBITDA in 3Q24 and management expectations for productivity gains and operating leverage to drive EBITDA margins to expand from 15% in FY24 to 16–18% over the longer term.

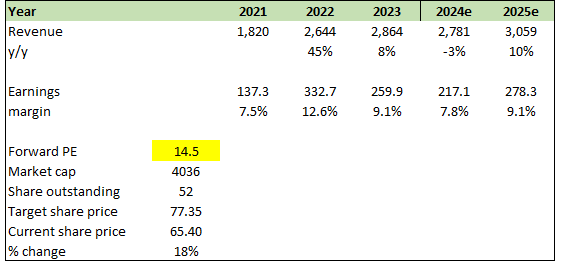

Valuation

Author’s work

I believe KFY can almost certainly grow as guided for FY24, given the guide was given in February and the business fiscal year ends in April (adding the 4Q24 guide to the 9M24 numbers, I got to $2.78 billion in revenue and $217 million in earnings). My view is that the upcycle is here for KFY, and FY24 should see the first year of growth recovery. In estimating this, I looked back at the previous 2 major cycles (post-dot-com and GFC). In both cycles, the first year of growth was incredible; KFY grew 36% in FY05 and ~30% in FY11. Given that the current macro environment is not entirely in a growth mode yet, I assume FY25 growth will be a lot less than in the past and just slightly above the FY23 level, at 10%. FY25 margins should inflect upwards as well. At the onset of a recovery, my view is that KFY should be able to recover margins back to FY23 levels at the bare minimum, given that the revenue base is larger and KFY now has a lower cost structure.

Risk

4Q24 revenue guidance is in the range of $675 to $695 million, implying a 6% y/y decline at the midpoint, and while I am positive, this could be seen as uncertainty in the broader labor markets, which means that my growth estimate is too aggressive.

Final thoughts

My recommendation has been upgraded from hold to buy as the Fed’s message on rate cuts and signs of a recovery cycle paints a positive outlook for the business. In particular, management has noted stabilizing labor markets and rising hiring activity, which both point to a potential upcycle ahead. I also like the fact that KFY has lower cost structure, which should help drive faster earnings growth when topline recovers.

Q2 2024 Earnings Call Transcript")