NoDerog/iStock Unreleased via Getty Images

Introduction

Per my April 2023 article, Monster’s (NASDAQ:MNST) gross margin has fallen substantially from the 60% level of 2019. Some of this is transitory due to the company’s covid philosophy of emphasizing product availability over economics. However, some of it is permanent seeing as growth is high in segments where the gross margins are less attractive than the US energy drink market; the alcohol segment and the international segment are examples where gross margins are not as good. Co-CEO Hilton Schlosberg repeated his emphasis on dollars over margins in the 2Q23 call (emphasis added):

We went into alcohol with our eyes wide open, we knew the margins that were in alcohol would be lower than the margins in the energy drink category. So we look at margin, I’ve always said this on calls, I say we bank dollars, we don’t bank percentages. And I’ve always encouraged analysts to just think, likewise, that we don’t bank percentages, we bank dollars.

Net income has gone up 47% from $1.1 billion in 2019 to $1.6 billion in 2023. Free cash flow (“FCF”) dollars have gone up nicely as well from $1 billion in 2019 to $1.5 billion in 2023. However, the increase in sales has been better on a relative basis as we’ve gone up almost 70% from $4.2 billion in 2019 to $7.1 billion in 2023 ($ in millions except Basic EPS):

|

*Basic EPS |

Net income |

Net Margin |

FCF |

Operating income |

Gross profit |

Gross Margin |

Net sales |

|

|

2019 |

$1.02 |

$1,108 |

26.4% |

$1,012 |

$1,403 |

$2,519 |

60.0% |

$4,201 |

|

2020 |

$1.33 |

$1,410 |

30.7% |

$1,315 |

$1,633 |

$2,724 |

59.2% |

$4,599 |

|

2021 |

$1.30 |

$1,377 |

24.9% |

$1,113 |

$1,797 |

$3,109 |

56.1% |

$5,541 |

|

2022 |

$1.13 |

$1,192 |

18.9% |

$700 |

$1,585 |

$3,175 |

50.3% |

$6,311 |

|

2023 |

$1.56 |

$1,631 |

22.8% |

$1,500 |

$1,953 |

$3,794 |

53.1% |

$7,140 |

*Basic EPS above is adjusted for the stock split for 2022 and earlier years.

FCF growth above has been impressive despite the decline in gross margin and FCF is what matters most to me in terms of valuing a company.

Celsius (CELH) has been growing rapidly in the US and some investors who are long Celsius might be tempted to short Monster. My thesis is that investors should think twice about betting against Monster. The energy drink business is a wonderful one and I think there is a good chance business will continue to thrive in the future for Red Bull, Monster, and Celsius. Of course, we have to separate the businesses from the stocks because even a good business can be a bad investment if the stock price is out of line.

High Margin US Convenience And Gas Channel

The Nielsen numbers for the overall US market are important but there are limitations such as

Costco not being included. An August 2023 Beverage Digest interview says 60% of the US energy business is in the convenience channel (emphasis added):

If you look at categories and channels, about 15 to 20% of carbonated soft drink business is in the convenience store channel. Conversely, about 60% of the energy drink business is in the convenience channel.

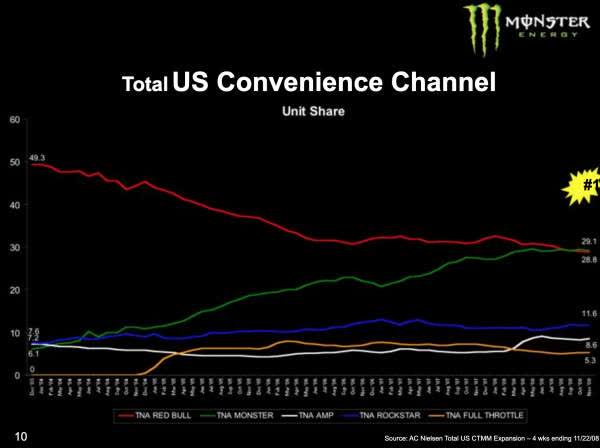

Looking at a slide from the December 2008 Investor Presentation, we see the green line for Monster rising prodigiously from December 2003 when they had less unit share than competitors like Rockstar (PEP) and Amp. By November 2008 Monster had solidified their leadership position with Red Bull:

Monster US Convenience Channel Unit Share (December 2008 Investor Presentation)

Monster has been dominating the US convenience channel with Red Bull since 2008. In March 2020 Pepsi agreed to acquire Rockstar for nearly $4 billion and the decline of this brand both before and after the acquisition is substantial. 5-hour used to have substantial sales but they are no longer a big factor in this channel and their founder Manoj Bhargava has been named in a Senate Swiss bank tax probe. Bang looked promising for years but they fell apart and Monster acquired them out of bankruptcy for a little under $400 million in July 2023:

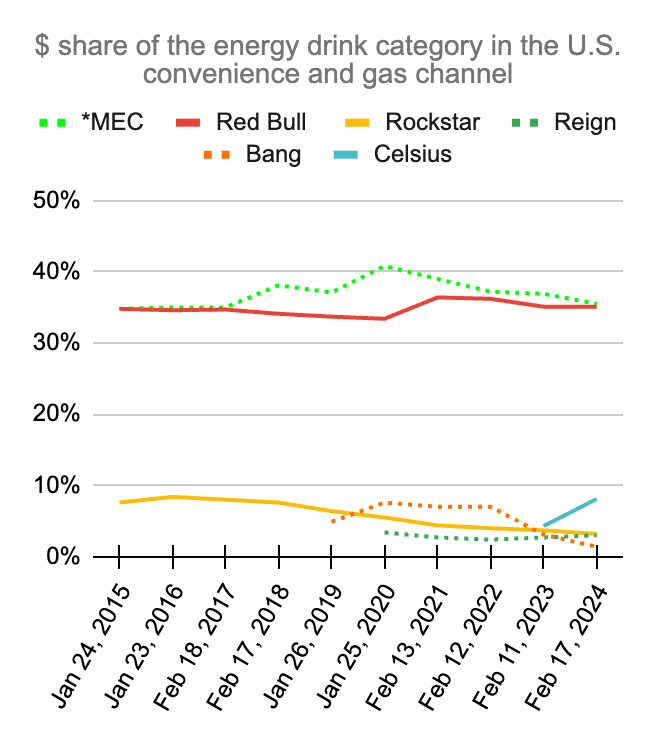

US Convenience/Gas Dollar Share (Author’s spreadsheet)

*Monster Energy Company (“MEC”) above includes their Reign brand but it excludes their newly acquired Bang brand. The above percentages are from 4th quarter calls and the timing varies. In the 4Q18 call, the numbers were from the 4 weeks up to Jan 26, 2019 but in the 4Q23 call, the numbers were from the 4 weeks up to Feb 17, 2024.

Bang and Pepsi reached a distribution agreement in April 2020. However, Bang fell apart after legal battles with Monster. A timely announcement was made in August 2022 about a long-term distribution deal and investment between Pepsi and Celsius such that Celsius slid into much of Bang’s shelf space in the Pepsi ecosystem. Monster bought Bang out of bankruptcy in July 2023 such that Bang is now part of the Coca-Cola (KO) distribution system. An August 2023 Beverage Digest interview with Editor Duane Stanford and Industry Expert John Sicher talks about the performance energy category which includes Monster brands Reign and Bang along with the rising star, Celsius. Industry Expert Sicher says it would be foolish to underestimate Monster in this area. He believes Bang can have some resurgence given the strengths of Monster’s leadership and the Coca-Cola distribution system (emphasis added):

I think one thing that one has to basically take away from what’s happened in the last couple of decades is that one, it would be very foolish to underestimate Rodney Sacks and the Monster management. They are very good at what they do. They’re very focused, they’re very aggressive, and I think that trying to basically manage several brands in the same category is very difficult. I think probably Duane, if anybody can do it, Rodney Sacks and that management team can, so I would think that we’ll see probably over the next year or two at least some resurgence and share for Bang, whether it gets back up to that eight, nine level, I don’t know, but I think Bang is going to be a player again in this category in the next six months or a year.

Per Editor Stanford, Bang forged the performance category and brands like Celsius with a “better for you” marketing angle have now occupied significant shelf space. Of course Monster is now participating heavily in this new space as well. I believe the better-for-you energy space is large enough for both Celsius and one or more of the Monster brands like Reign or Bang to do well:

And still even with all these new entrants, you’ve still got Monster and Red Bull just by far dominating this market and they are not backing down. That’s been so fascinating to watch them really just do everything they can to innovate against these new up and coming brands. For instance, Bang Energy, it came along, Monster created Reign Energy and went toe to toe with them. Now they’ve got a Reign Storm where they’re going toe to toe with some of the natural better-for-you energy drinks. One of the strengths of Monster is not only their ability to drive their brands and really get into the culture, but also to create a platform of brands that really go after all of these different needs states and that also are able to fend off some of these challenges.

Asset-Light International Growth

International full service bottler/distributor customers for Monster have climbed from 23% of gross billings in 2014 up to 40% in 2023. More than half the global energy business is outside the US and I think Monster will continue to find success with their global growth efforts:

|

US full service bottlers/distributors |

Intl full service bottlers/distributors |

Club stores & other |

Retail grocery & other |

Alcohol & other |

|

|

2014 |

62% |

23% |

9% |

4% |

2% |

|

2015 |

65% |

23% |

9% |

2% |

1% |

|

2016 |

65% |

25% |

8% |

1% |

1% |

|

2017 |

63% |

28% |

7% |

1% |

1% |

|

2018 |

61% |

31% |

6% |

1% |

1% |

|

2019 |

58% |

33% |

7% |

1% |

1% |

|

2020 |

56% |

34% |

8% |

1% |

1% |

|

2021 |

51% |

39% |

8% |

1% |

1% |

|

2022 |

48% |

39% |

9% |

2% |

2% |

|

2023 |

47% |

40% |

8% |

2% |

3% |

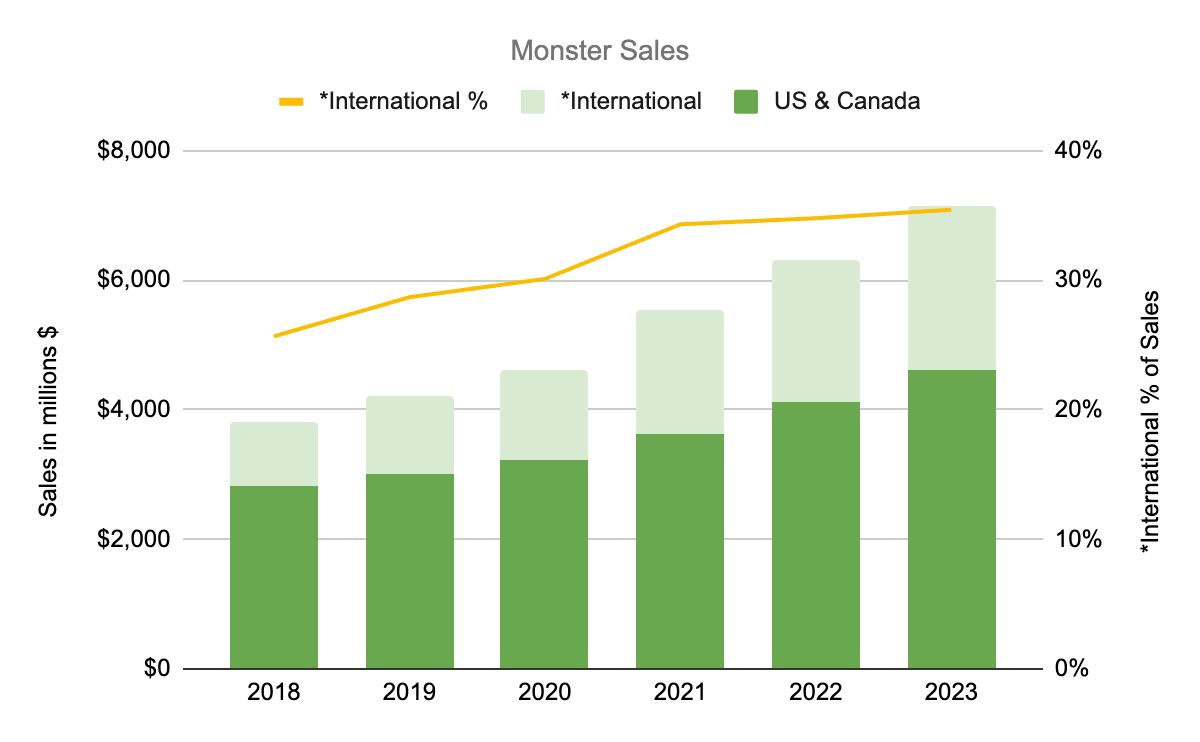

The increase in the rate of international sales should continue to outpace the increase in the rate of US/Canada sales in the years ahead:

Global Sales (Author’s spreadsheet based on 10-K filings)

Valuation

Monster’s 2023 operating income was just shy of $2 billion and I believe the company could be worth 30x this amount +/- $5 billion given management’s track record. As such, I think Monster could be worth $55 to $65 billion.

Per the 2023 10-K, there were 1,040,636,235 shares outstanding as of February 15th. This puts the market cap at about $62 billion based on the March 22nd share price of $59.50. The market cap is in my valuation range and I think the stock is a hold.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Q2 2024 Earnings Call Transcript")