AndreyPopov

The large-cap pharmaceutical group has lagged the stock market badly over the past year, relative to the S&P 500 jump of +25% or high-flying NASDAQ 100 index spike of +40%. So, I consider this sector a good hunting ground for bargains. Since late summer, I have written bullish views on Pfizer (PFE) here and Bristol-Myers Squibb (BMY) here, but neither has been able to get out their funk, as investors fret over the negative long-term effects of Medicare negotiations on future pricing/profitability and major drug-patent expirations at each.

Another Big Pharma name with equally sound valuations, but the added support of earnings growth kickers approaching in 2025, is Sanofi (NASDAQ:SNY), based in Paris with nearly 60% of sales taking place outside America. Each U.S. ADR creation represents 1/2 of an ordinary share for Sanofi (OTCPK:SNYNF) traded in Europe (generally priced in Euros).

The company is best known for the wonder drug Dupixent [co-developed with Regeneron (REGN)], which generates about 25% of total company revenue currently. According to the 2023 20-F Annual Report,

DUPIXENT (dupilumab) is a fully human monoclonal antibody that inhibits the signaling of the interleukin-4 (IL-4) and interleukin-13 (IL-13) pathways and is not an immunosuppressant. Dupilumab is jointly developed by Sanofi and Regeneron under a global collaboration agreement. To date, dupilumab has been studied across more than 60 clinical trials involving more than 10,000 patients with various chronic diseases driven in part by type 2 inflammation. The dupilumab development program has shown significant clinical benefit and a decrease in type 2 inflammation in Phase 3 trials, establishing that IL-4 and IL-13 are key and central drivers of the type 2 inflammation that plays a major role in multiple inflammatory diseases, such as atopic dermatitis (AD), asthma, chronic rhinosinusitis with nasal polyposis, eosinophilic esophagitis and prurigo nodularis. DUPIXENT comes in either a pre-filled syringe for use in a clinic or at home by self-administration as a subcutaneous injection or in a prefilled pen for at-home administration, providing patients with a more convenient option. DUPIXENT is available in all major markets including the US (since April 2017), most European Union countries (the first launch was in Germany in December 2017), Japan (since April 2018), and China (since June 2020).

Sanofi is also a major vaccine supplier to the world, which represented almost 20% of net sales in 2023. It is a maker of flu shots and a host of vaccines to protect children/infants across the globe from various diseases.

Sanofi Website – March 22nd, 2024

Management is considering spinning off its Consumer Healthcare division (12% of 2023 sales), to focus on prescription drugs. Allergy, Cold & Sinus, Digestive Wellness, and Pain medicine production and assets (which many of us use each year) could be listed as a new company. Existing shareholders would own shares in both the new consumer health enterprise and legacy Sanofi operations. The brand-name list of OTC items includes Allegra, Xyzal, DulcoLax, IcyHot, Aspercreme, Unisom, Oscal-D, and numerous others.

A robust rebound in operating earnings is projected by Wall Street analysts after a transition year in 2024. Rising sales on popular existing drugs, expected new pharmaceutical approvals, and a cost cutting program targeting €2 billion in reductions by the end of 2025 should each add underlying shareholder value over time.

For forward-looking patient investors, buying shares now may prove an excellent decision. Why? My bullish take is focused on (1) a stable and easily covered 4% dividend rate, (2) a stronger balance sheet than most in the industry, (3) a valuation that is way too low if earnings growth picks up in 2025-26, and (4) buyers appear to be getting the upper hand vs. sellers in March on the technical charts. Let’s quickly review the opportunistic setup.

Dividend Story

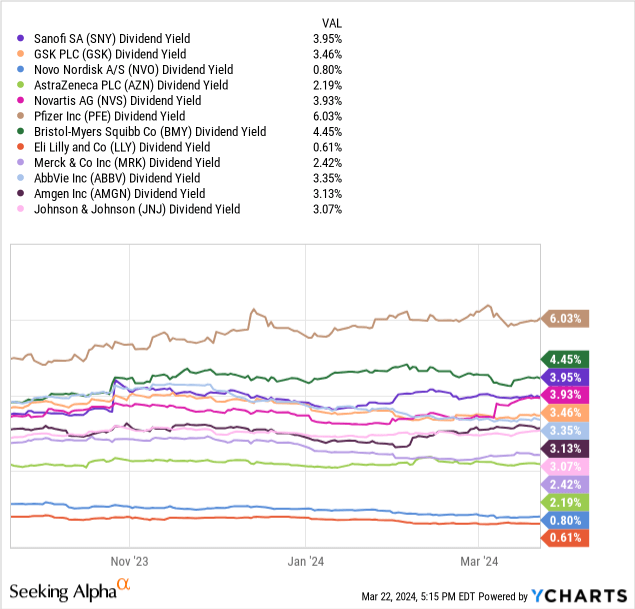

For starters, the income crowd and defensive investors should be attracted to the sound dividend payout at Sanofi. Today’s rough 4% yield for cash distributions is one of the highest in the Big Pharma space. Below I have drawn a 6-month chart comparing Sanofi to yields from peers GSK plc (GSK), Novo Nordisk A/S (NVO), AstraZeneca PLC (AZN), Novartis AG (NVS), Pfizer, Bristol-Myers Squibb, Eli Lilly (LLY), Merck (MRK), AbbVie (ABBV), Amgen (AMGN), and Johnson & Johnson (JNJ).

YCharts – Sanofi vs. Big Pharma, Dividend Yield, 6 Months

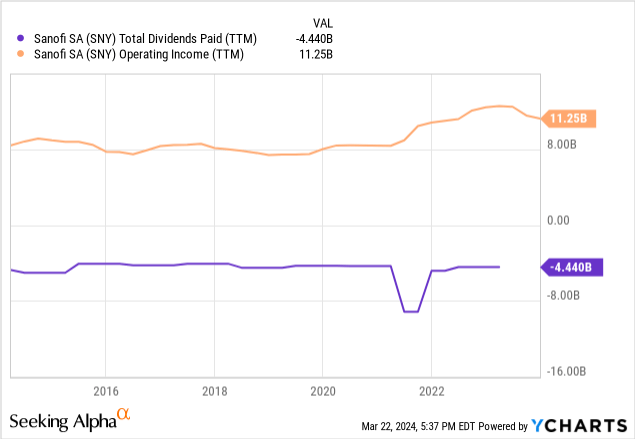

And, the 2x coverage from operating income in 2020 has risen to 2.5x in 2023-24. Essentially, the dividend yield has the strongest coverage in over a decade and is better covered than the vast majority of Big Pharma names. So, the odds of a dividend cut are quite limited, while the opportunity for dividend payout growth is uniquely high.

YCharts – Sanofi, Dividend Coverage from Operating Income, 10 Years

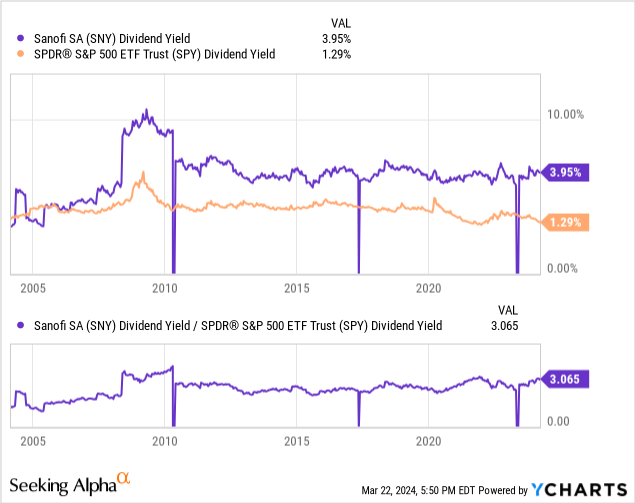

Lastly, the Sanofi yield is sitting at the best “relative” rate to the S&P 500 index since 2010. On the chart below, you can review how the trailing 3.95% yield is substantially higher than the SPDR S&P 500 ETF (SPY) equivalent number of just 1.29% today. For income investors looking for safety, Sanofi’s dividend is 3x the level of regular U.S. blue chips!

YCharts – Sanofi vs. S&P 500 ETF, Dividend Yield, 20 Years

Conservative Balance Sheet

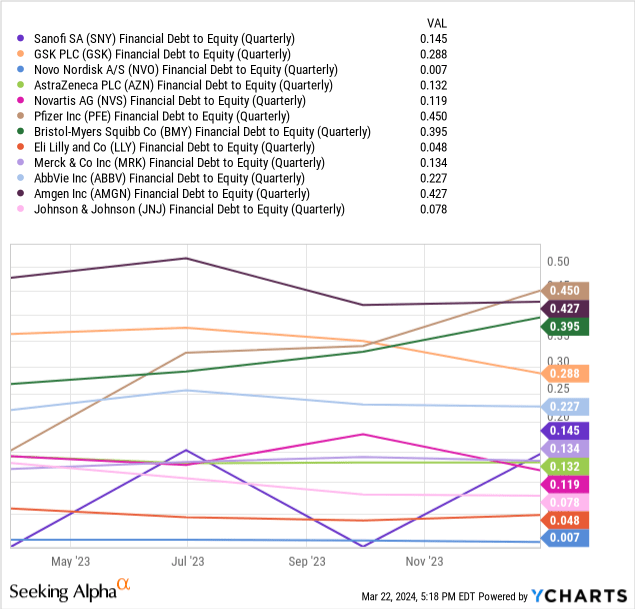

Another idea to contemplate in your buy decision process is Sanofi runs one of the most conservative balance sheets in Big Pharma. Debt to equity is extremely low at 0.14x, in the bottom half of the peer group.

YCharts – Sanofi vs. Big Pharma, Debt to Equity, 1 Year

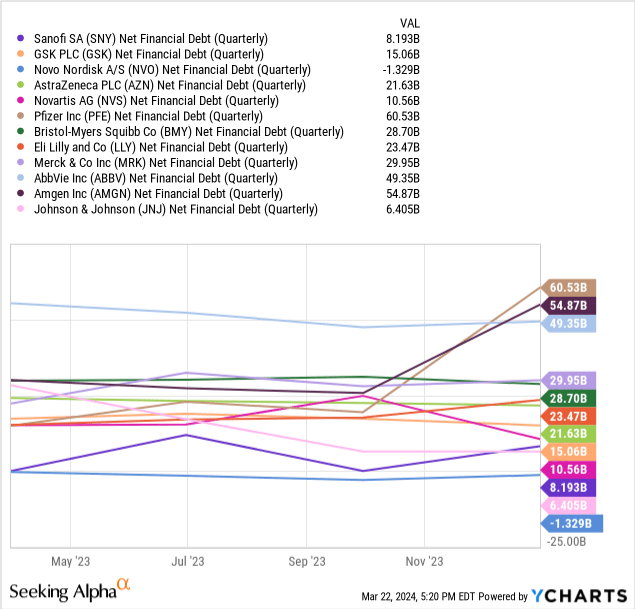

Plus, “net” financial debt (total debt minus cash on hand) is one of the lowest in the group, sitting at a minor US$8.2 billion vs. today’s equity market capitalization of $120 billion.

YCharts – Sanofi vs. Big Pharma, Net Financial Debt, 1 Year

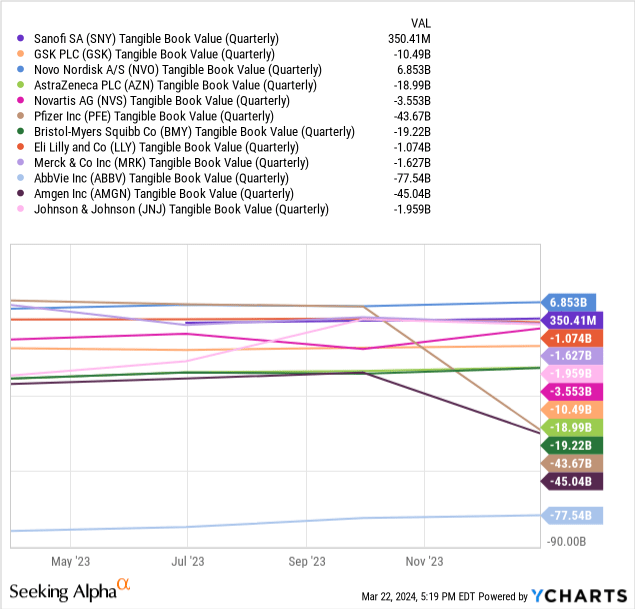

In terms of underlying net asset worth and financial flexibility, the company also has a positive tangible book value number, which is rare for the drug industry. With takeover goodwill accounting and patents structured as intangible assets based on projected future drug sales/income, the biggest pharmaceutical businesses traditionally have NEGATIVE tangible book values. Although US$350 million in TBV sounds light, it is far better than peers.

YCharts – Sanofi vs. Big Pharma, Tangible Book Value, 1 Year

Undervalued Growth Proposition

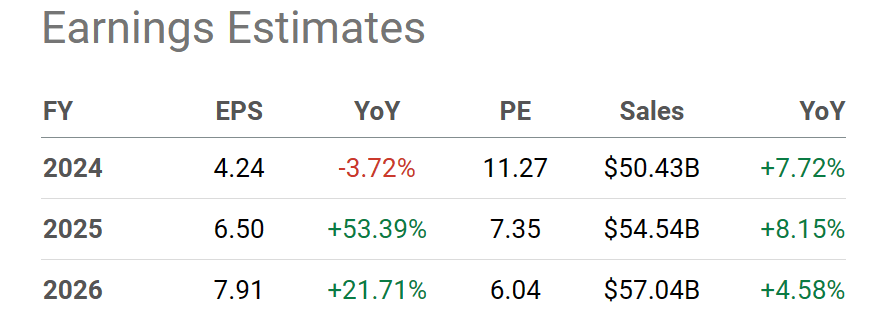

In summary, Sanofi has a terrific dividend story and a rock-solid balance sheet as a foundation for stock gains. But, the truly bullish reason to own the stock is its valuation may not properly discount a bright earnings future starting next year. 2024 is expected by analysts to be a year of restructuring and perhaps a company split. Based on the business setup today, earnings per share of US$6.50 next year and $7.91 in 2026 have yet to be priced into the stock.

Seeking Alpha Table – Sanofi, Analyst Estimates for 2024-26, Made March 21st. 2024

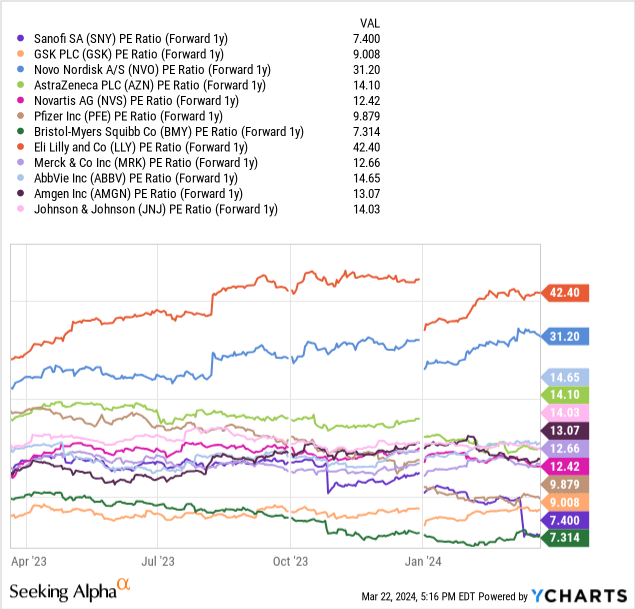

When we look at the peer group and forward 1-year earnings in 2025, only Pfizer matches up with Sanofi at a projected P/E of 7x. And, if you weigh 2026 estimates, Sanofi is far and away the cheapest of this group.

YCharts – Sanofi vs. Big Pharma, P/E Ratio on Projected 2025 Results, 1 Year

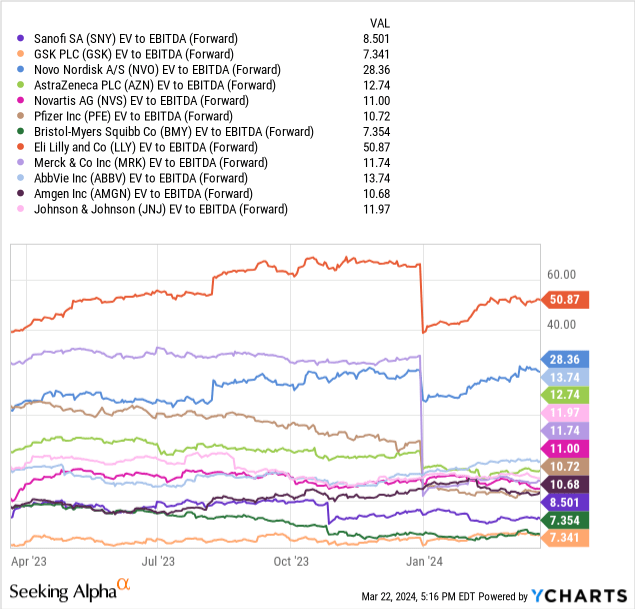

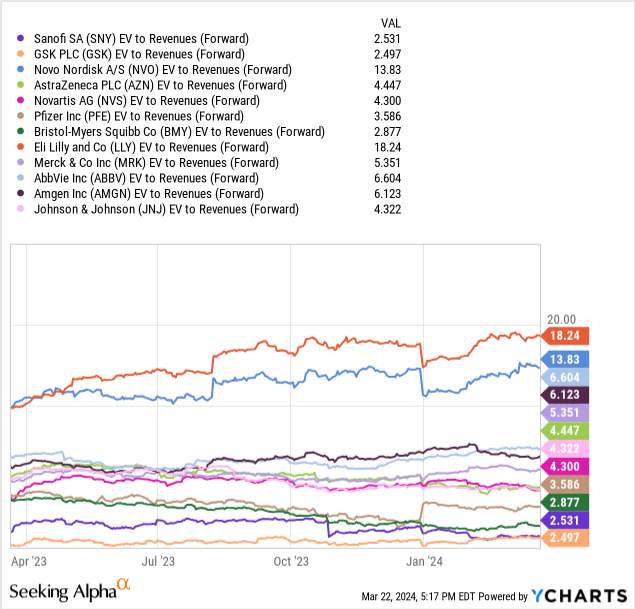

Further, when we take into account the company’s low level of net debt, enterprise valuations on forward estimated EBITDA (8.5x) and revenues (2.5x) scream SNY is absolutely a bargain vs. industry competitors. Note: the sector growth leaders of Eli Lilly and Novo Nordisk are valued richly on their weight-loss GLP-1 drug prospects.

YCharts – Sanofi vs. Big Pharma, EV to EBITDA on Projected 2024 Results, 1 Year YCharts – Sanofi vs. Big Pharma, EV to Sales on Projected 2024 Results, 1 Year

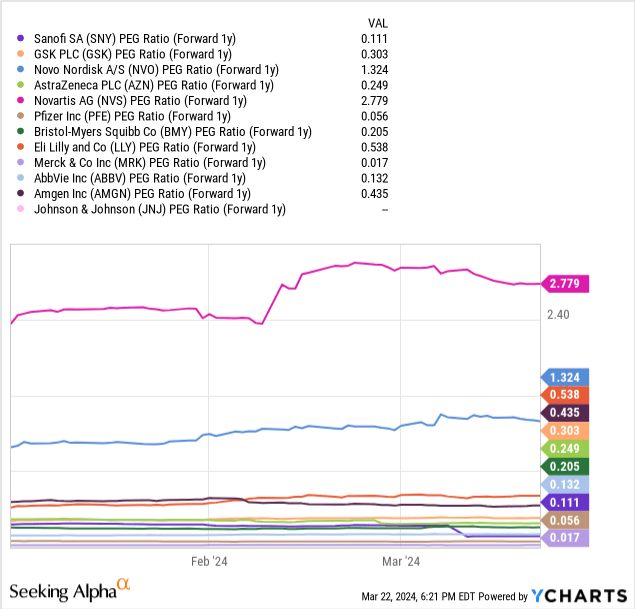

When you cross projected earnings growth rates vs. current P/Es, the PEG valuation for Sanofi is extremely bullish today. Honestly, most Big Pharma names appear to be worthwhile buy ideas on this metric.

YCharts – Sanofi vs. Big Pharma, Forward PEG Ratio on Projected 2025 Results, 3 Months

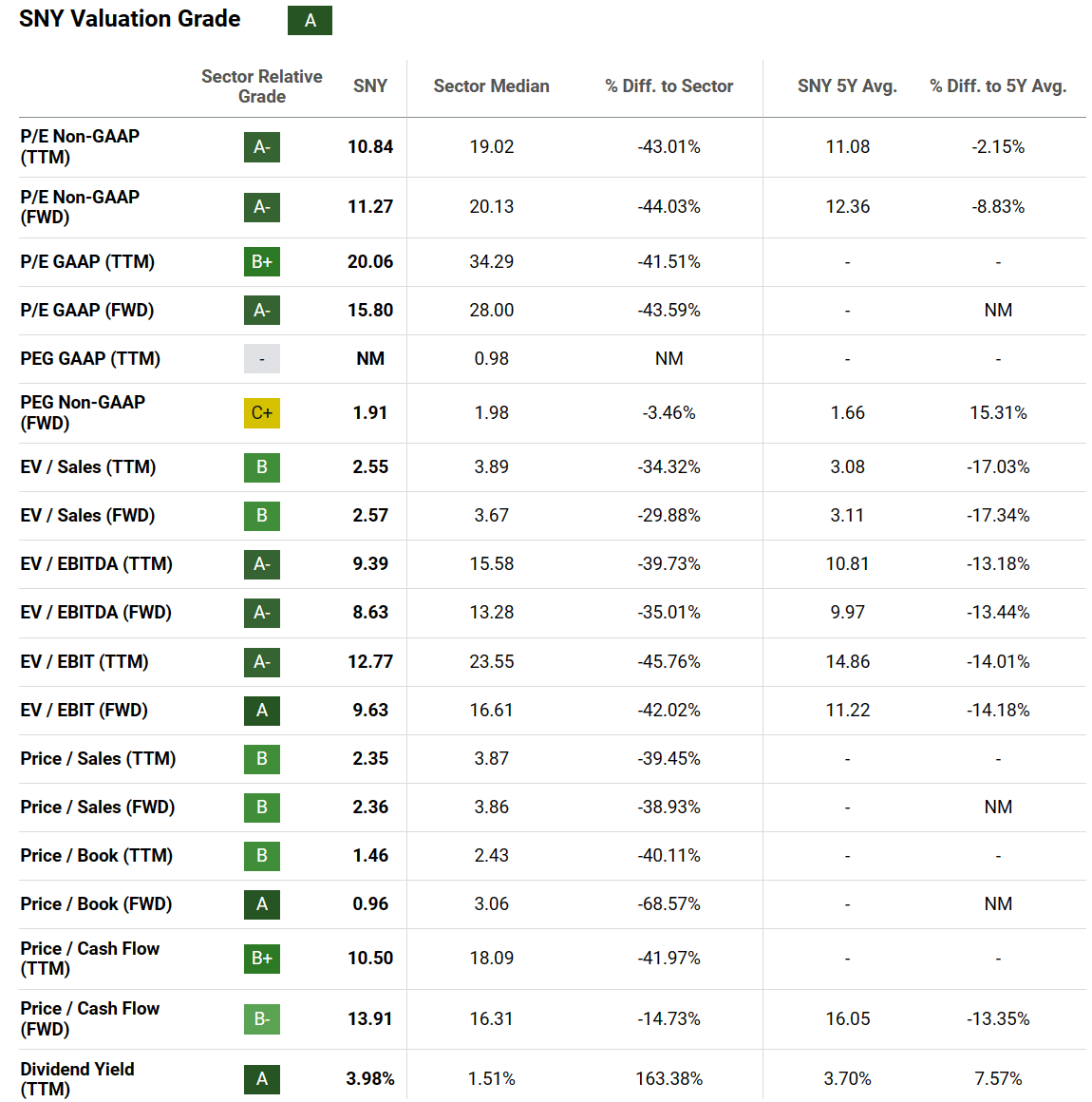

Rounding out my valuation review, Seeking Alpha’s computer-scored Quant Valuation Grade of “A” stands out in the sector. It’s the same positive score as my other two value favorites in the sector: Pfizer and Bristol-Myers Squibb.

Seeking Alpha Table – Sanofi, Quant Valuation Grade, March 21st, 2024

Technical Pattern

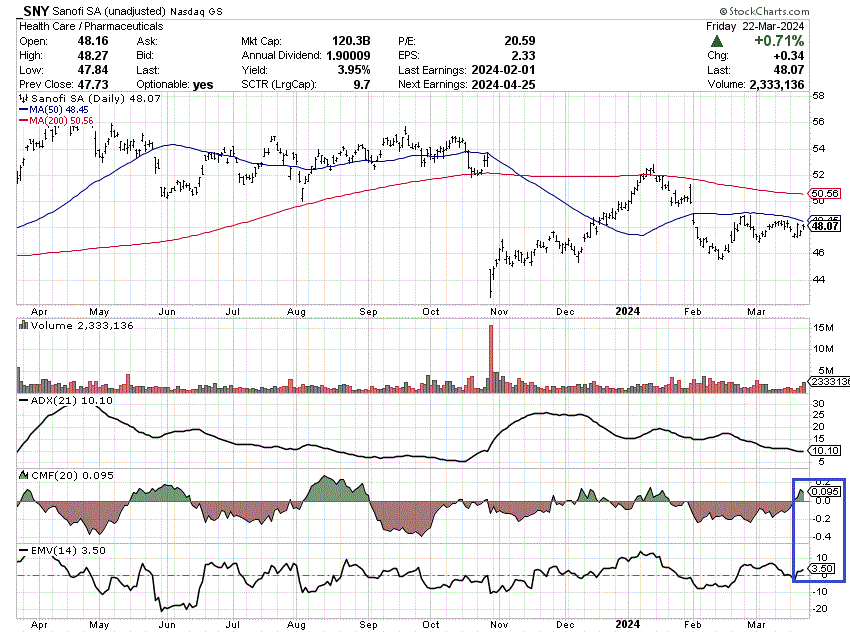

At first glance, there’s nothing exciting to find on the Sanofi chart of daily trading below. Over the past year, price has zigzagged lower, with a large dump in late October on management’s announcement of weaker-than-expected results and its restructuring as a response.

Nevertheless, hints of buying volume inflows overwhelming sellers are starting to appear after a period of consolidating October’s price loss. In fact, in recent days, something of an equilibrium in share supply/demand (indicated by the low 21-day Average Directional Index score of 10) may be witnessing a bullish turn for the better for shareholders. I have boxed in blue the newly positive readings in the 20-day Chaikin Money Flow calculation, alongside the 14-day Ease of Movement reading which has been above zero for weeks already. Note: the expansion of buying highlighted by these two indicators is very different than the net selling of early October.

In my research, when both CMF and EMV are turning higher, share pricing will follow with gains over the next 2-3 weeks about 60% of the time. Yet, when we add the low ADX score into the equation, and factor in the stock’s undervaluation and sizable improvement in business fundamentals coming soon, SNY could be ready for a large upturn in price.

StockCharts.com – Sanofi, 12 Months of Daily Price & Volume Changes, Author Reference Point

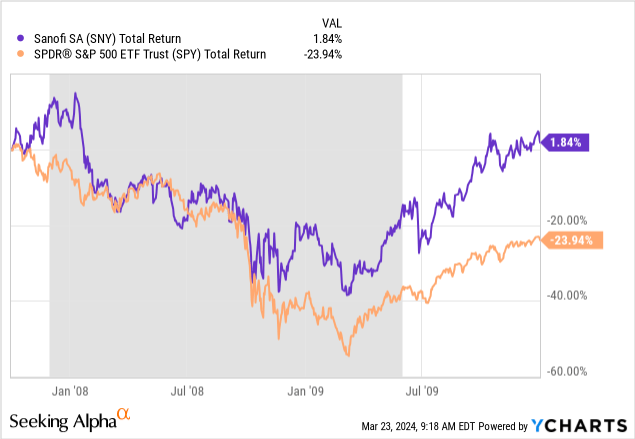

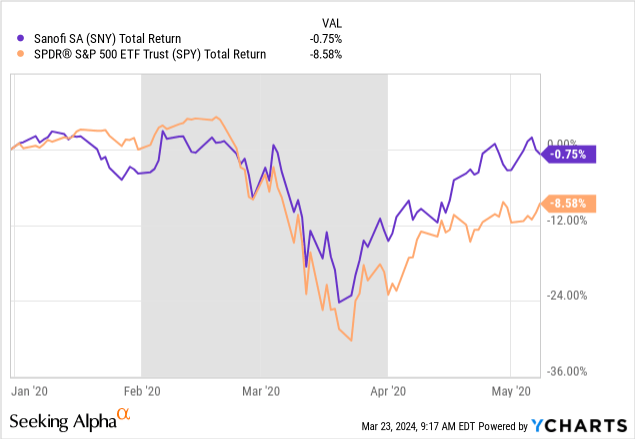

Shares are also an interesting defensive, flight-to-safety pick. Reviewing past recession and bear market performance since 2007, Sanofi has a history of outlining slightly better total returns than the S&P 500, when trouble hits the economy. I am including charts of the 2007-09 Great Recession, first-half 2020 pandemic experience, and 2022 to early 2023 bear market in U.S. equities.

October 2007 to December 2009

YCharts – Sanofi vs. S&P 500 ETF, Total Returns, Recession Shaded, Oct 2007 to Dec 2009

January to May 2020

YCharts – Sanofi vs. S&P 500 ETF, Total Returns, Recession Shaded, Jan to May 2020

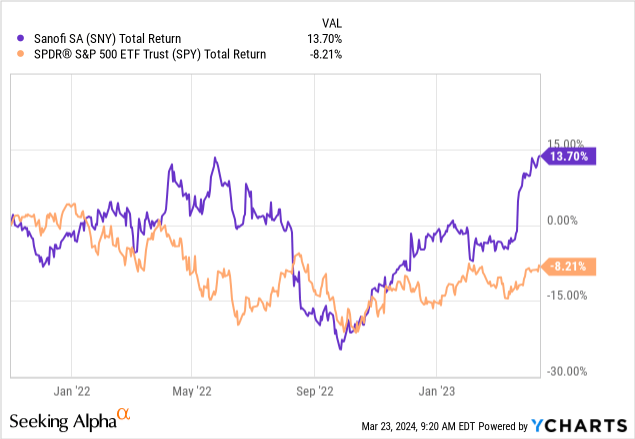

November 2021 to April 2023

YCharts – Sanofi vs. S&P 500 ETF, Total Returns, Nov 2021 to April 2023

Final Thoughts

My investment conclusion is Sanofi may have the best combination of value, growth, and dividend characteristics of all the Big Pharma choices. I believe the stock is a top choice in the growth-at-a-reasonable-price [GARP] area of market research. The major drug companies have a history of defensive total returns in recession and bear markets. In addition, it appears SNY buyers are starting to outnumber sellers in share trading for the first time since early January.

What are the risks to your investment in SNY? A slowdown in Dupixent sales would be risk #1 to ponder, in my view. The company is projecting annual sales of the drug will grow further to 13 billion Euros annually soon (from a little over 10 billion Euros today). If this forecast proves overly optimistic, I doubt analyst income projections will prove accurate.

A general stock market crash scenario would be major risk #2 to weigh in your decision process. While today’s low share valuation should help Sanofi to outperform in regular bear market and recession scenarios, a straight down move in all stocks will affect SNY equally. Don’t laugh but the AI bubble of 2023 and early 2024 has pulled crash odds up to 10% to 20% later in 2024 (most years I would place crash odds well under 5%).

U.S. equity market valuations in particular are quite high in March on (1) modern record price to sales for the S&P 500, (2) total market value vs. GDP output remaining close to 2021’s record high, and (3) nosebleed CAPE ratio scores using long-term trailing P/Es. Incredibly, investors seem to be overlooking still high recession odds, effectively putting sky-high valuations on stocks near a peak in the economic cycle. You have to go back to the original dot-com Tech bubble peak during the year 2000 or the insanity of 1929 to find a similar mismatch setup.

Otherwise, assuming Dupixent sales remain high and a stock market crash is avoided this year, I expect Sanofi to be a successful and productive investment selection over then next year or two. I am placing a Buy rating on SNY, with expectations of nice “outperformance” of the S&P 500 over the next 12-24 months.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")