winhorse/iStock Unreleased via Getty Images

AIA Group (OTCPK:AAIGF) has come down significantly since my first coverage of it in June 2023 when it shouldn’t have. Despite the Group’s strong financial performance, the market has been wary of its Chinese exposure. These “exogenous factors”, however, never had much of an impact on the fundamentals of the business which at present look as sound as ever.

Financial update

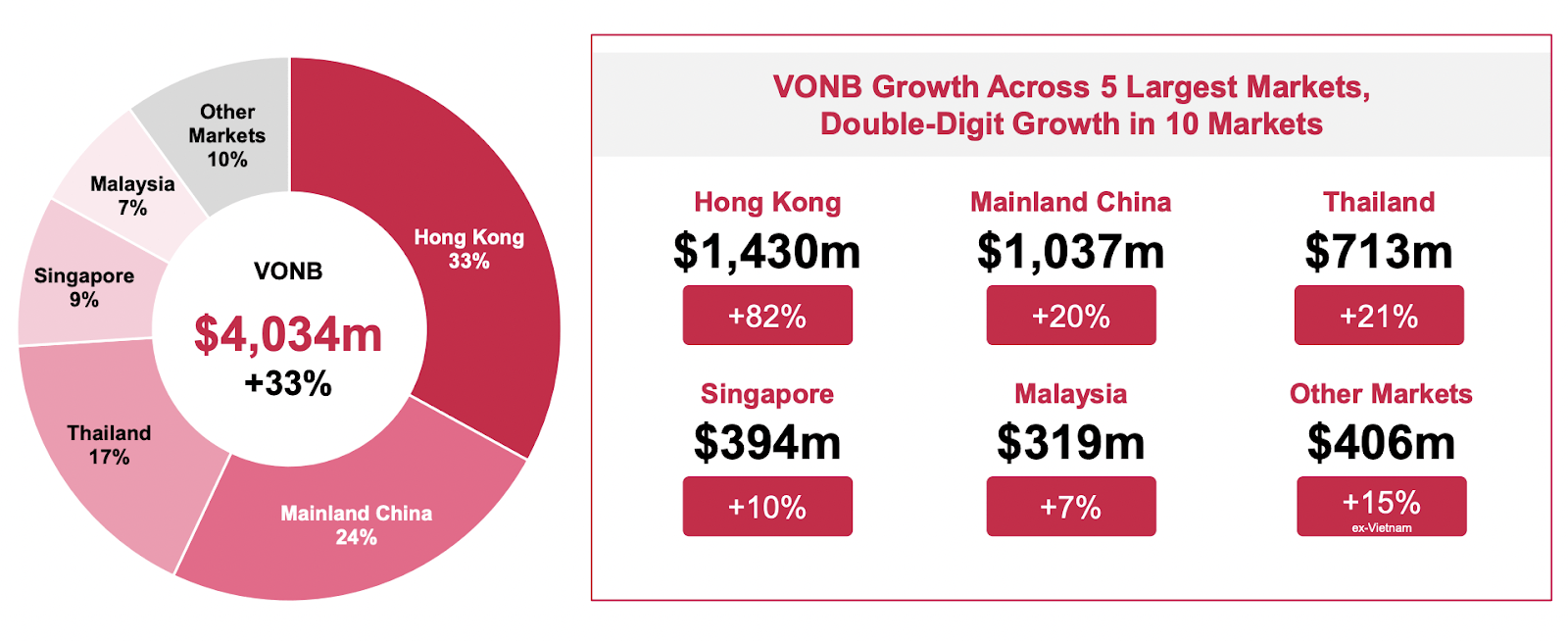

AIA Group reported its financial results for the year ended 31 December 2023 on March 14th. The results were decisively positive, particularly growth-wise. Value of new business (VONB), a key performance metric, hit US$4,034m, finally nearing the pre-pandemic high of $4,154m reached in 2019. In fact, Annualized New Premiums (ANP), another growth metric, added 45% and reached a record high of US$7,650m. For context, the highest before COVID-19 was US$6,585m recorded in 2019. VONB margin, a measure of profitability, came to 52%.

All four main markets — Mainland China, Hong Kong, ASEAN, and India (i.e., TATA AIA Life) — delivered double-digit VONB growth numbers in 2023. ASEAN, the largest market overall comprising Thailand, Singapore, and Malaysia (this time sans Vietnam where the insurance industry is reeling from a trust crisis)— was up 14% and brought ⅓ of the Group VONB, equivalent to about US$1.5b. The original AIA Hong Kong recorded the highest growth figure of all, 82%, adding US$1.4b. Mainland China ended up at plus 20% and US$1b.

AIA Group

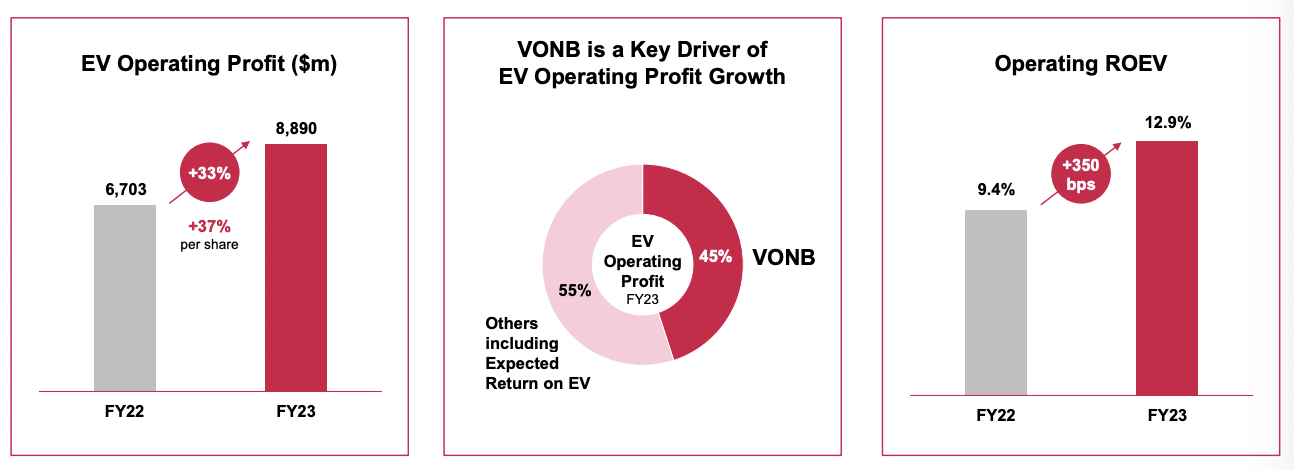

Earnings, as a result, rose too. Especially those based on embedded value (EV), an insurance-specific measurement of total shareholder value: EV operating profit was up by 37% per share to US$8,890m. Return on EV operating profit increased from 9.4% to 12.9%. Though conventionally reported operating profit after tax at US$6,213m stayed flattish, plus 2% per share, due to higher medical claims during the year.

AIA Group

The AIA difference

The Group added over 1.5m new customers in 2023, 10% more than last year. The most common factor cited for driving growth is greater productivity from both agency and bancassurance, across markets.

Even in China, where most other insurers have lost agents, AIA claims to have augmented its workforce instead. AIA China increased new recruits by 59% last year, with agent productivity twice the peer average. Elsewhere too, the group-wide focus is on raising the professionalism of agents while supporting them with digital solutions — exactly where the industry is supposed to be moving. Bancassurance is growing briskly, led by ASEAN.

“We have the world’s most professional agency that has been number one MDRT globally for the last nine years. We are also individually the number one in Mainland China, Hong Kong, ASEAN and India. And we have grown MDRT qualifiers by a further 20% in 2023, proving the success of our high quality model.”

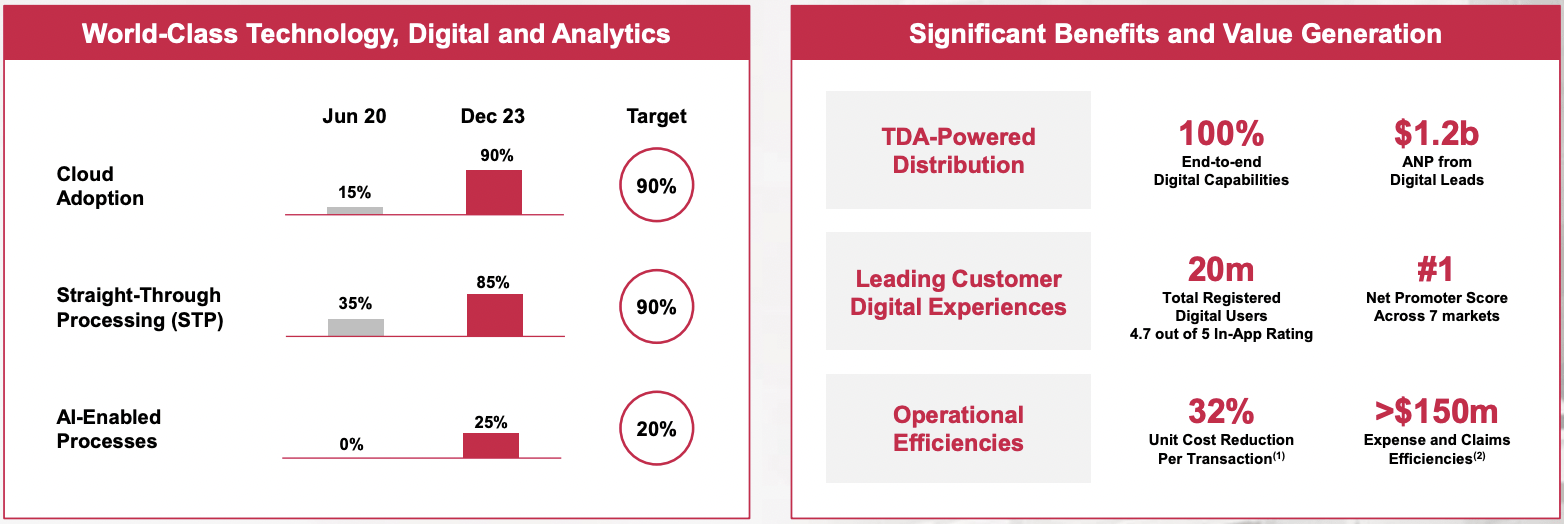

Another strategy at the center of AIA is extensive application of technology, digital (solutions) and analytics (TDA). More than US$800m invested over the past three years has elevated lead generation, customer experience, and operational efficiency. AI is being leveraged for both agency and customer management, leading to greater productivity and hence higher sales.

11 markets out of 18 in total have been fully digitized, with products becoming available online and agents being able to reach customers on digital platforms. AIA’s lead in TDA is helping it win over younger digitally savvy customers, to acquire them and get them to stick around. (To that I can attest as a customer myself.)

AIA Group

Valuation

After losing 31% (30% with dividends) over the past year and 41% (38%) in the last three years (AAIGF returned -25% and -39% in total in the same periods), SEHK:1299 is the cheapest in five years, at a Price/EVPS of 1.41. The consensus price target is high, with 12-month forecast at HK$96.80, more than 70% up from HK$55.95 as of March 23.

|

SEHK:1299 |

FY2023 |

FY2022 |

FY2021 |

FY2020 |

FY2019 |

|

Price |

HK$68.5 |

HK$86.8 |

HK$78.6 |

HK$95.0 |

HK$82.2 |

|

EV per share |

US$6.26 |

US$5.87 |

US$6.03 |

US$5.41 |

US$5.14 |

|

Price/EV per share |

1.41 |

1.89 |

1.68 |

2.27 |

2.06 |

Source: Annual reports 2020 and 2022, financial results 2023

Dividend

At 2.9%, the yield is not much for a Hong Kong stock but payments have been growing consistently, by about 14% per year since 2014. The dividend policy is stable, and since earnings (and cash flows) cover payments comfortably, the yield can be expected to keep growing.

Risks

The main concern on everyone’s mind is China. It is geopolitics, really an indelible part of investing in China and/or Hong Kong. It is also the debt situation and underwhelming economic recovery so far — issues that might take longer to resolve. It is worth remembering though that AIA is as diversified throughout Asia as can be, and China (where it owns just 1% of the market) is not its largest territory by value contribution.

Conclusion

I believe the performance momentum AIA has built since the end of COVID-19 will continue. The AIA advantage in agents and TDA may prove to be the right combination for continued growth in Asia’s dynamic insurance markets. Things will not be perfect given the inherent complications of operating in China, but other markets, ASEAN in particular, can easily pick up the slack. (And the smaller base in China could help sustain AIA’s growth numbers in the long term.) Overall, AIA is a solid growth income stock with a positive outlook.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")