koto_feja

The AI trend has lifted almost every stock that has a whiff of artificial intelligence capabilities in the market this year. But what generalist investors have to be wary of is that AI is a very broad category, and certainly not all companies are of comparable quality.

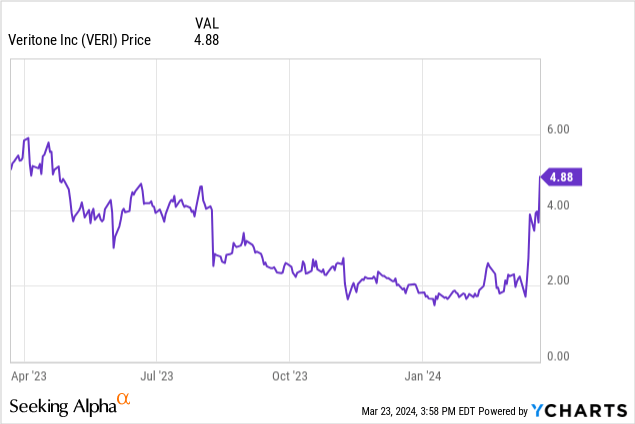

This year’s rally seems to have lifted all boats, including Veritone (NASDAQ:VERI), a company founded about ten years ago that has made very little incremental progress. Year to date, the stock has nearly tripled, recouping much of last year’s losses as financials deteriorated. Don’t trust this phantom rally: it’s likely to be short-lived.

I last wrote a bearish article on Veritone last May, when the company was trading just shy of $4 per share. The stock had been sleepily trading downward until just recently when the company announced Q4 results as well as a restructuring plan that aims to cut out at least 15% of annual operating expenses.

That, in and of itself, should be the first red flag. AI is having a watershed moment this year, and most AI companies are investing in growth while the time is ripe: but Veritone is contracting. There’s no doubt, of course, that this move is quite necessary for Veritone (we’ll get into the company’s shrinking balance sheet later in this article). But the point still stands: Veritone is certainly not thriving, even if its stock price rally this year suggests that it is.

Red flags abound here, actually. The company continues to see precipitous y/y drops in revenue, and new software bookings are coming in lower than last year’s levels. We note as well that not all of Veritone’s revenue is software-driven; it still generates roughly half of its revenue from “managed services,” or essentially its legacy ad-tech/media management services business.

The question here is survivability: in my view, Veritone will find it difficult to deliver on its promise of returning to growth and profitability this year. I remain solidly bearish on this name and advise investors to invest elsewhere.

Sharp contraction in the top line: where’s the AI advantage?

A similar narrative has played out across most software companies that deliver AI products this year: enterprise adoption is surging as mainstream interest has picked up in ChatGPT, helping these software companies buck the broader macro challenges and achieve high levels of new bookings.

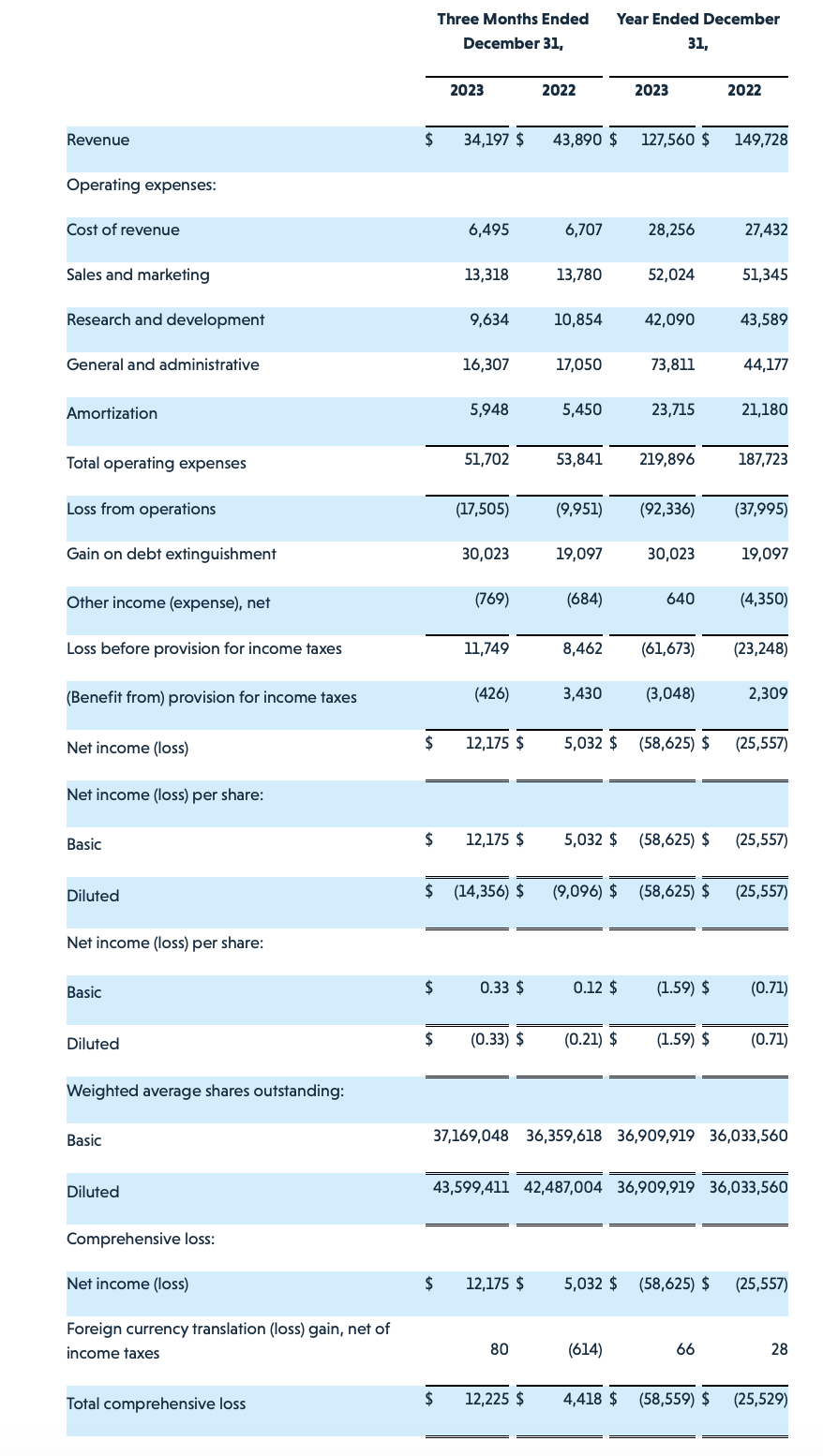

This is not the case for Veritone. Take a look at its Q4 results below:

Veritone Q4 results (Veritone Q4 earnings release)

Revenue declined -22% y/y to just $34.2 million (note here: Veritone is at an incredibly small scale vis-a-vis other publicly traded software companies). Note as well here that software revenue (which is what investors who are banking on the AI trend should care about) fell -28% y/y to $19.8 million, while managed services saw a milder -11% y/y decline.

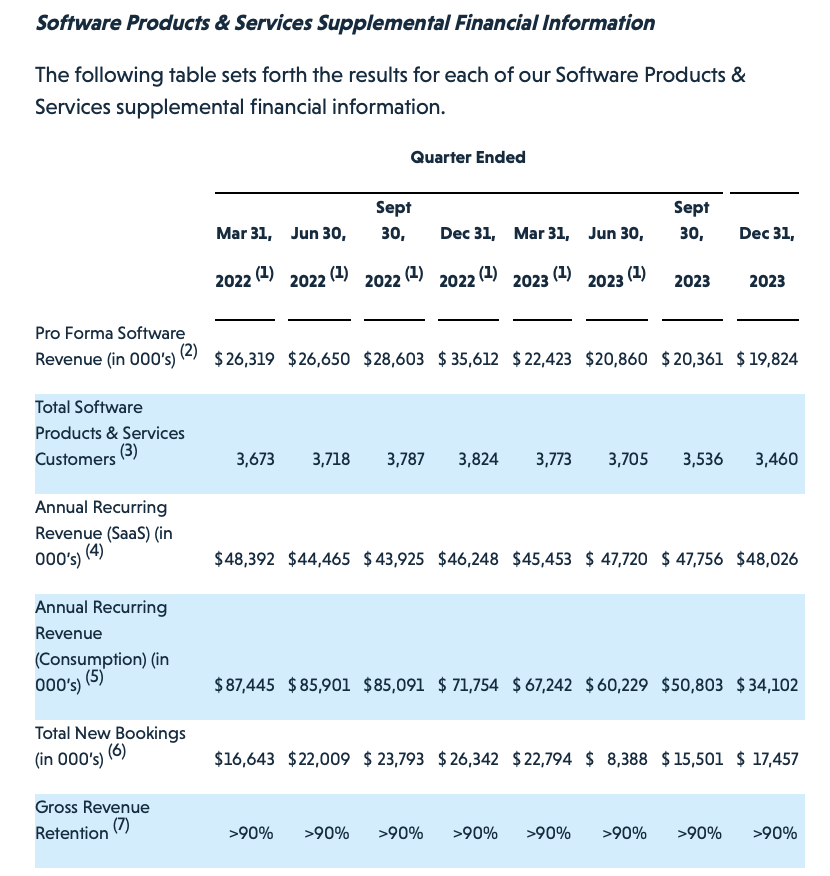

Here’s the other warning sign to be cognizant about: new software bookings also declined -34% y/y to just $17.5 million in the fourth quarter:

Veritone key metrics (Veritone Q4 earnings release)

The company attributed the y/y bookings decline to reduced engagement from Amazon (AMZN), previously one of its largest customers. Going forward, it expects Amazon to contribute to less than 5% of overall revenue. But that doesn’t mean the risk is concentrated to Amazon only. Meanwhile, the company’s count of software customers declined by 76 customers quarter-over-quarter to 3,460. This is the fourth straight quarter of customer declines since peaking in the December quarter of 2022.

As a reminder, Veritone’s core AI product is called aiWare. This is essentially a PaaS (platform-as-a-service) offering that gives companies the ability to embed AI features such as transcription and process automation into internally built applications. A good chunk of Veritone’s software clients sits in the public sector, working with customers such as local police forces.

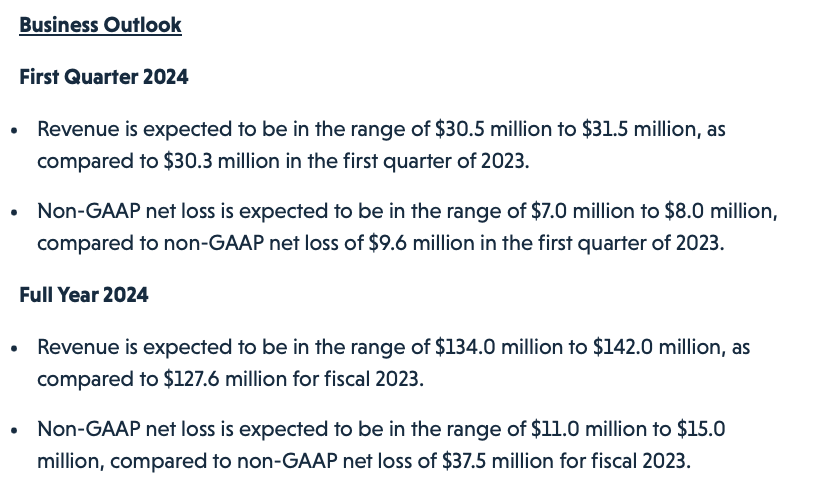

Veritone is projecting to return to total revenue growth by the first quarter of FY24, and for the full year FY24 to grow at a 5-11% y/y clip, as shown in the chart below:

Veritone outlook (Veritone Q4 earnings release)

To me, we’ve seen no evidence of a path back to growth, especially with new software bookings declining in Q4: so we should treat this outlook with a heaping grain of salt.

Even with layoffs, can Veritone remain solvent?

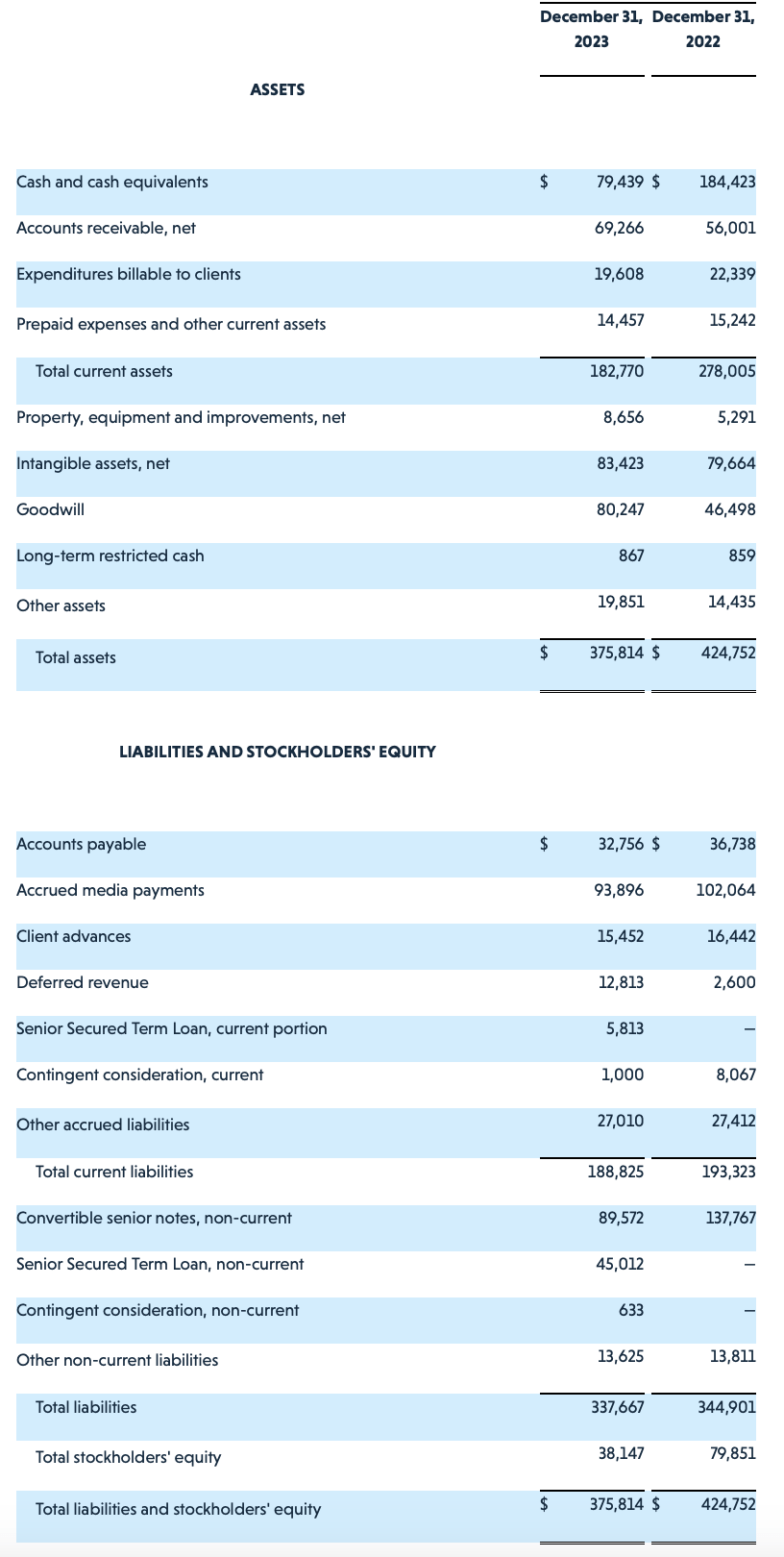

As of the end of the fourth quarter, Veritone only had $79.4 million of cash left on its balance sheet, and it’s actually in a slight net debt position after considering its $50.8 million term loan and $89.6 million of convertible debt.

Veritone balance sheet (Veritone Q4 earnings release)

Meanwhile, operating cash flow in FY23 was -$76.4 million. If Veritone does nothing else, the company would run out of cash by the end of the year.

Of course, management is projecting that it will return to profitability and positive cash flow by the second half of FY24 on the back of its layoff plan. Per CFO Mike Zemetra’s remarks on the Q4 earnings call:

I’m happy to report that as a result of our Q1 2024 restructuring efforts, we executed on over $10 million of additional annualized cost reductions through today, which is included in our full year in Q1 2024 financial guidance, and we are not done. As a result of this phase of reorganization, we expect future synergies, both cost and revenue related to materialize in the latter part of fiscal 2024, particularly across our software products and services lines.

The Q1 restructuring, including organizational realignments within sales engineering and corporate, the result of which was a reduction of approximately 14% of our global workforce.”

All in all, the company expects a 15% savings on operating expenses. FY23 opex was roughly $220 million on a GAAP basis; so 15% would translate to $33 million of annualized savings. All else equal, this isn’t enough to push Veritone’s cash flow back to positive. And that’s not to mention the risk of further software deterioration, as has been the trend over the past few quarters.

Key takeaways

With a very limited balance sheet, declining software revenue, and what to me seems like unrealistic guidance for FY24, Veritone has a number of pitfalls ahead of it this year. Continue to avoid this stock.

Q2 2024 Earnings Call Transcript")