cruphoto

China Concerns

For readers following our writing, you may recall that we rated Rio Tinto (NYSE:RIO) as Buy for price levels below $70 in the past 1~2 years. And that is also the price range where we accumulated our shares. Now, we are thinking about selling our shares and we are contemplating a target price in the same price range (say $70 to $75). It’s been a pretty bad call considering how much the overall market has appreciated over this period. The saving grace is the generous dividends that we’ve collected during our holding period (more on this in the next sector).

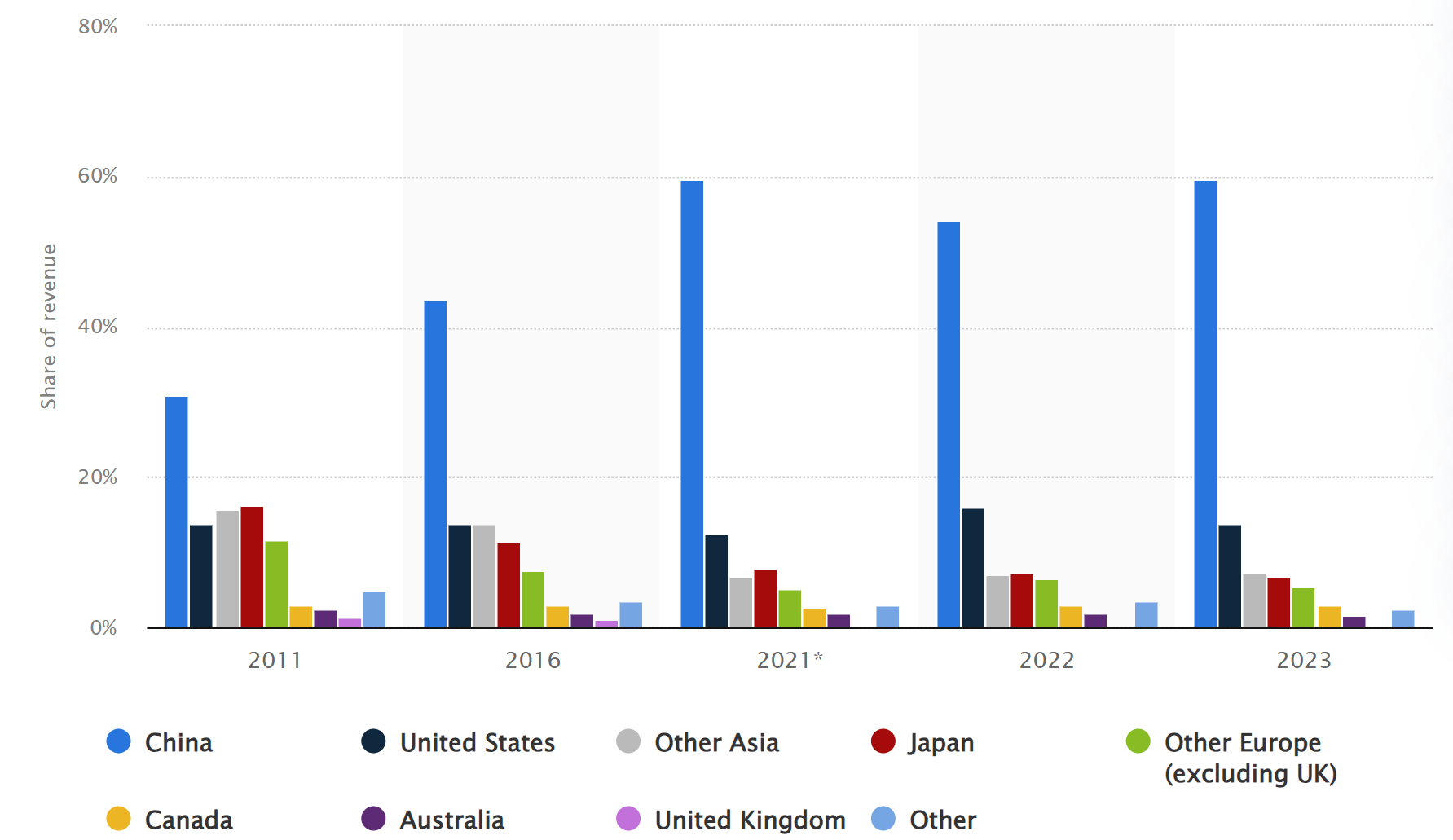

The main factor that caused our change of thesis is China. China is a major market for RIO’s ores as you can see from the chart below. For 2023 in particular, 59.6% percent of its sales revenues are from China, far ahead of its second-largest market (United States), which accounted for “only” 13.9% of revenue generation that year. The real estate and infrastructure market in China kept struggling and its recent stimulus policy seems to have limited effect in my eyes so far in my eyes so far. We are still concerned about China’s trouble in the real-estate sector, a large consumer of raw materials. We are seeing signs that these troubles are far from over, including slumping new home sales, potential default risks for heavy-weight developers, and hidden bad loan problems.

Statista

Dividends In Focus

Given these issues, we also began to be concerned about the dividend, a key motivation for us in the first place. In our experience, commodity stocks tend to move in tandem with the overall stock market, but at a lower magnitude because global GDP growth is a key driver of sales of these stocks. Many metals and ores RIO produces are used in almost every industry throughout the world.

Given the slower price appreciation, the dividend yield was the main attraction for us. As you can see from the chart below, the company’s yield was below 4% 10 years ago. Today, the yield is close to 7%. And when we bought our shares, the yield was even higher, around 8%.

Seeking Alpha

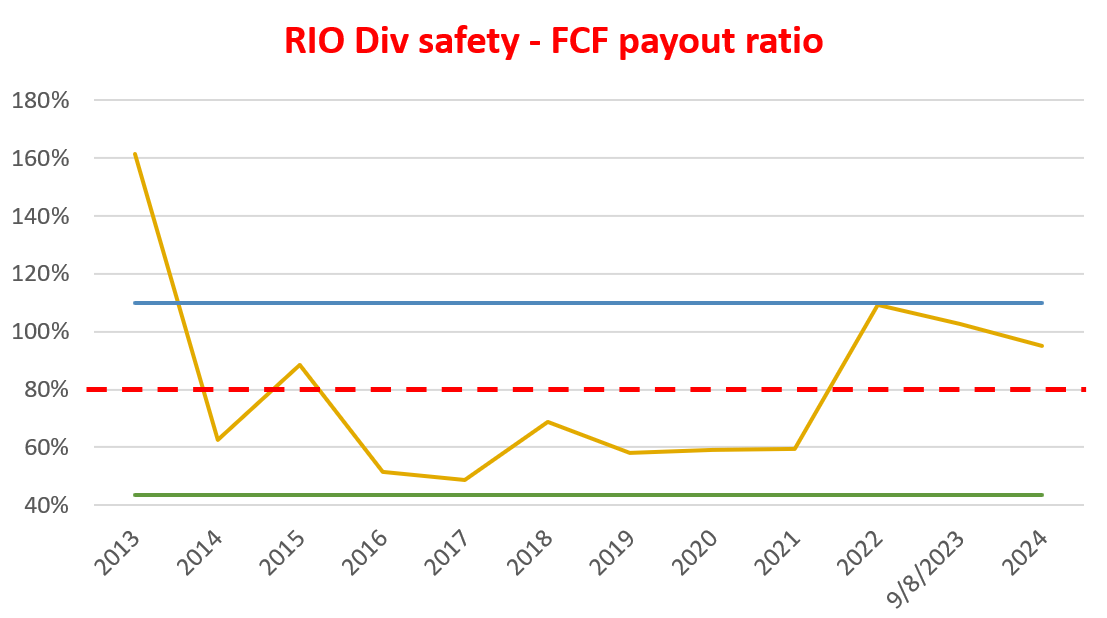

Going forward, we don’t see much change in Rio’s overall capital allocation strategy, and we envision the dividend payout ratios to continue. As such, there are good reasons for investors who need current income (with a good degree of safety) to consider RIO shares. However, we are seeing limited potential for RIO’s dividend to increase in the next few years. As seen in the following chart, our projection shows that RIO’s free cash payout ratio (on an FWD basis) is hovering around 100%. It is not only in limiting dividend increases in an absolute sense but also towards the upper end of its historical range.

Author

Valuation

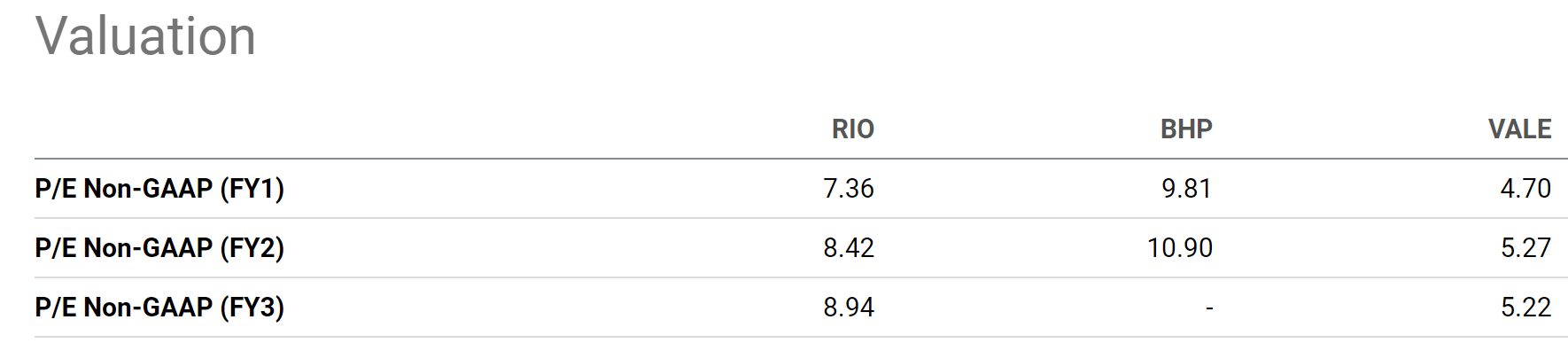

Although on the positive side, RIO is attractively priced with a P/E in the single digits as you can see from the chart below. To wit, it is trading at 7.36x P/E on an FY1 and non-GAAP basis, a fraction of the overall market’s valuation multiple only. But note the market expects the earnings to decline in the next 3 years. As a result, its FW P/E is expected to gradually inch up to about 9x in FY3.

However, my view is that RIO’s current P/E is attractive on an absolute basis but close to fair valuation on a relative basis. For example, when compared to its major peers, the picture changes a bit. RIO has a lower P/E ratio than BHP Group (BHP) and a higher P/E than Vale S.A. (VALE). Also, RIO’s median P/E in the long-term (say the past 10 years) is about 9x. And as just mentioned, its FY3 P/E is projected to be about 9x.

Seeking Alpha

Other Risks And Final Thoughts

A few miscellaneous, yet noteworthy, thoughts before I close this article. I assume readers are familiar with the risks common to ore/commodity stocks already, such as commodity price volatility, sensitivity to environmental regulations, and also sensitivity to geopolitical instability as many ore producers (and RIO is no exception) operate in countries with political or social unrest. As such, I will focus on a few less-discussed factors here.

On the negative side, besides the risks mentioned earlier, RIO is also heavily reliant on iron ore compared to other more diversified miners. This makes it more vulnerable to price swings and softened demand for this particular ore.

On the positive side, I expect Rio’s production of other ores, in particular lithium, nickel, copper, and uranium to increase over the next few years (say 3~5 years). And I further anticipate these mineral ores to help its profit growth. These ores are critical in the fabrication of batteries for electric vehicles. They are also used in the production of many renewable energy projects around the world. These new industry sectors are growing quickly and should help with the demand for RIO’s ores. Another positive to consider is RIO’s ex-U.S. exposure, especially for investors whose exposure is mostly concentrated in the U.S., which has become very expensive in our view. RIO’s ex-U.S. exposure, combined with its commodity nature, makes it a good candidate for an all-weather portfolio if you are a believer in Ray Dalio’s approach as we do.

All told, our view (and plan also) is that RIO is no longer a buy under current conditions. We are looking for an exit point near $70, and this target price is largely determined by its near-term trading pattern and price volatility. Its attractive dividend yield offers another motivation to hold, providing a steady stream of income in a very expensive overall market. In the longer term, our growth and price appreciation expectations are quite tempered. To recap, our top concerns are China’s cooling demand for raw materials, a major driver for RIO’s business. Such headwinds could pressure the company’s slow growth potential and limit its flexibility for dividend increases.

Q2 2024 Earnings Call Transcript")