jetcityimage/iStock Editorial via Getty Images

Petco Health and Wellness Company (NASDAQ:WOOF) operates over 1500 pet care centers in the United States, Mexico, and Puerto Rico, as well as pet veterinary hospitals, under the Petco brand. The company also has the Petco mobile app, providing information on pet care and a convenient way to order products and services. Petco also offers its own pet products with brands such as WholeHearted, Reddy, and Well & Good.

The company did an opportunistic IPO in early 2021, as the stock has since lost nearly all of its value with pressured profitability and concerningly high debt. While the stock’s significant fall could represent an attractive buying opportunity to some, I am not very optimistic yet. Petco’s high debt makes the investment case volatile, and the valuation doesn’t provide enough upside to justify a great risk-to-reward in my eyes.

Stock Chart From IPO (Seeking Alpha)

Financials: A FY2023 Profitability Slump Amid Modest Growth

Petco has achieved modest growth in the company’s past years, mainly with a FY2020 growth of 11.0% and an FY2021 growth of 18.0% during the Covid pandemic; in other years, the growth has only amounted to low single-digit percentages with FY2023 revenues growing by 3.6%. With a good part of the pandemic growth likely caused by inflation, I believe that Petco’s sustainable growth level is very modest, below the reported CAGR of 7.3% from FY2018 to FY2023.

Some growth in the future is still to be expected; Petco managed to grow veterinarians by 9% year-over-year in Q4, as told in the quarter’s presentation. In addition to service growth enabled by a growing number of veterinarians, digital sales continue to grow providing some room for wider revenues in the future. Still, I believe that the overall growth story should be modest; in Q4, services only accounted for 15.2% of revenues. Petco is also expanding its offering with pet insurance, as announced in January.

Author’s Calculation Using Seeking Alpha Data

The company has historically had quite thin profitability with an average operating margin of 3.9% from FY2018 to FY2022. As such, any fluctuation in Petco’s operations can be seen volatilely in earnings, with FY2023 being a great example. Petco’s operating margin decreased to 0.7% in the fiscal year mostly due to a lower gross margin than usual, decreasing operating income by -81.5%. The management relates the weak profitability to investments in bringing value brands into consumables and discretionary headwinds in the Q4 earnings call, explaining a 3.5 percentage point decrease year-over-year in Q4 and a 2.6 percentage point decrease in FY2023 compared to FY2022.

Petco didn’t publish an FY2024 guidance due to the recent change in CEO but did provide a Q1 outlook with the Q4/FY2023 report. The company expects revenues of $1.5 billion, around 10.4% lower than the reported prior quarter’s revenues and 3.6% lower than Q1/FY2023 revenues. The company sees weakness in consumer sentiment resulting in weak Q4 comparable sales, seemingly continuing into FY2024; the weak profitability isn’t going to get better yet.

I believe that an eventual margin recovery into prior years’ level is quite likely, but upcoming quarters seem likely to show worse figures for at least the first half of FY2024 as Petco’s Q1 guidance points toward continued weakness. Pet care centers’ operations should be stable on a long-term basis, though, as pets require constant care, and I don’t see any signs of Petco’s brand fundamentally weakening, so I consider the pressure in gross margins highly likely temporary. Petco’s management also still seems confident in the company’s long-term future with favorable megatrends and a strong brand, at least in the Q4 earnings call.

Worryingly High Debt

Petco has an extremely leveraged balance sheet. The company currently holds almost $1.6 billion in long-term debt, around three times Petco’s market capitalization of $535 million at the time of writing. With Petco’s historical cash flows, paying off a significant amount of the overleveraged balance sheet requires a lot of time with FCF of -$10 million in FY2023 and $68 million in FY2022. Petco managed to pay down debt by $75 million in FY2023.

The high debt makes Petco’s earnings even more volatile – currently, as margins have compressed in FY2023, interest expenses are well above Petco’s operating earnings at $150.9 million in FY2023 compared to an operating income of $42.2 million. Even on a more normalized earnings level in FY2022, operating income was $227.8 million, of which the FY2023 interest expenses cover the majority. The company shouldn’t necessarily have liquidity issues with available revolving credit left, though.

Valuation

With Petco’s highly volatile earnings, I believe that the EV/EBITDA ratio is the most fit multiple to look at when comparing the company’s historical valuation. Currently, Petco trades at a forward EV/EBITDA of 10.1, up from a low of 7.9 but still below the historical average of 12.1.

Historical Forward EV/EBITDA (TIKR)

To estimate a rough fair value for the stock, I constructed a discounted cash flow model. In the DCF model, I estimate a revenue fall of -3% for FY2024 in light of the weak Q1 guidance. Afterward, I estimate modest growth with service revenue growth contributing to the estimated 4.5% in FY2025. With the gradual growth slowdown afterward, the DCF model’s total revenue growth estimates represent a CAGR of 2.1% from FY2023 to FY2033, with a perpetual growth rate of 2% afterward.

I estimate the EBIT margin to see benefits from a recovering consumer sentiment from FY2025 forward, eventually recovering into a margin of 3.5% from FY2027 forward. The estimated margin represents Petco’s average operating margin prior to the pandemic in FY2018-FY2019. Petco has a fairly large amount in investments worsening the cash flow conversion, and I estimate quite a modest conversion going forward.

With the mentioned estimates along with a cost of capital of 8.45%, the DCF model estimates Petco’s fair value at $2.14, around 8% above the stock price at the time of writing. While the DCF model estimates upside, I don’t think that the investment case currently has a very good risk-to-reward in terms of valuation – the model takes an EBIT margin of 3.5% as granted and estimates no liquidity issues despite Petco’s large amount of debt.

DCF Model (Author’s Calculation)

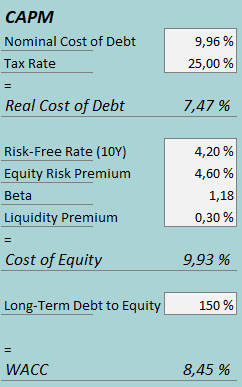

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q4, Petco had $39.7 million in interest expenses. With the company’s current amount of interest-bearing debt, Petco’s annualized interest rate comes up to 9.96%. As already said, Petco leverages a worryingly high amount of debt in financing – I estimate a long-term debt-to-equity ratio of 150% as paying off the debt should take a very long time with Petco’s cash flows. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.20%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates Petco’s beta at a figure of 1.18. Finally, I add a small liquidity premium of 0.3%, creating a cost of equity of 9.93% and a WACC of 8.45%.

As the equity valuation has gone down significantly since Petco’s IPO, I don’t believe the beta of 1.18 is necessarily a fair beta estimate for Petco at the moment – with current financials, the company is now more leveraged than ever before, making a fair beta likely much higher. I didn’t modify the beta in the CAPM, but I believe that investors should require a higher expected return for the investment as Petco is highly leveraged.

How I’d Change My View

For the time being, I am neutral on the stock. The investment case is likely to be volatile, though, and there are many factors that could alter the stock’s attractiveness.

On the upside, Petco’s profitability improvements could be a significant positive value driver, if the margin trajectory is proven to be better than I anticipate. With historically thin operating margins, even slight improvements in the margin could be a major catalyst in creating shareholder value, easily raising the fair value estimate.

Petco’s growth initiatives could also provide operating leverage in a scenario where growth is faster than I anticipate, also being a driver for higher margins. The expansion into insurance could provide marginal earnings to Petco, but with the current margin profile, any added earnings are highly valuable to the bottom line.

Continued weakness could make the stock fall further, though, making even a neutral rating too optimistic. The high debt can easily start to add up with weaker earnings, making the stock essentially worthless.

Takeaway

Petco’s post-IPO performance hasn’t been up to par with expectations; the current revenue growth trajectory seems very modest, and the company’s profitability has suffered massively from weakened discretionary spending, pressuring the operating margin very low from already thin levels. The company’s extremely leveraged balance sheet doesn’t improve the situation, making earnings fluctuations even more leveraged for shareholders. While I expect the profitability to start improving at some point with an improving consumer sentiment, the investment case doesn’t seem too great – investors take on large risks from debt, and the assumption of a margin recovery, for quite little upside as my DCF model only estimates very slight upside in the mentioned scenario. For the time being, I have a hold rating for the stock.

Q2 2024 Earnings Call Transcript")