fergregory/iStock via Getty Images

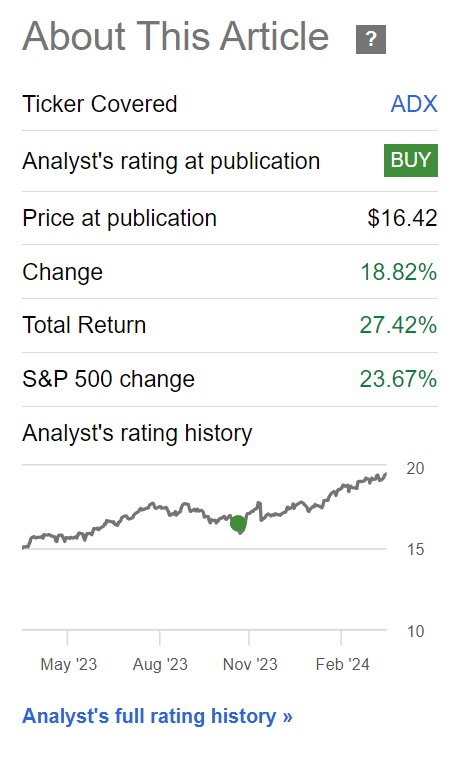

In October, I re-iterated my buy rating on the Adams Diversified Equity Fund (NYSE:ADX). In my opinion, ADX is one of the most impressive growth-oriented closed-end fund (“CEF”) in the market, with a long track record of strong performance. ADX was also well positioned, with large weights in the ‘Magnificent 7’ stocks that were driving market performance. Since my update, the ADX fund has done extremely well, returning over 27% (Figure 1).

Figure 1 – ADX has returned over 27% since October (Seeking Alpha)

In my October article, I also wrote that investors in ADX should be on the look out for a sizeable year-end distribution, since the fund pays a minimum 6% annual distribution and it had only paid three $0.05 distributions up to October. My estimate, based on October YTD performance, was for an ~$0.80 / share special distribution.

In fact, due to the fund’s strong rally into year-end, the ADX fund ended up paying a $1.15 / share year-end special distribution. This was a welcome bonus for investors in the ADX fund.

However, with the ADX fund up over 25% since October, am I still as bullish on the prospects for the ADX fund?

Brief Fund Overview

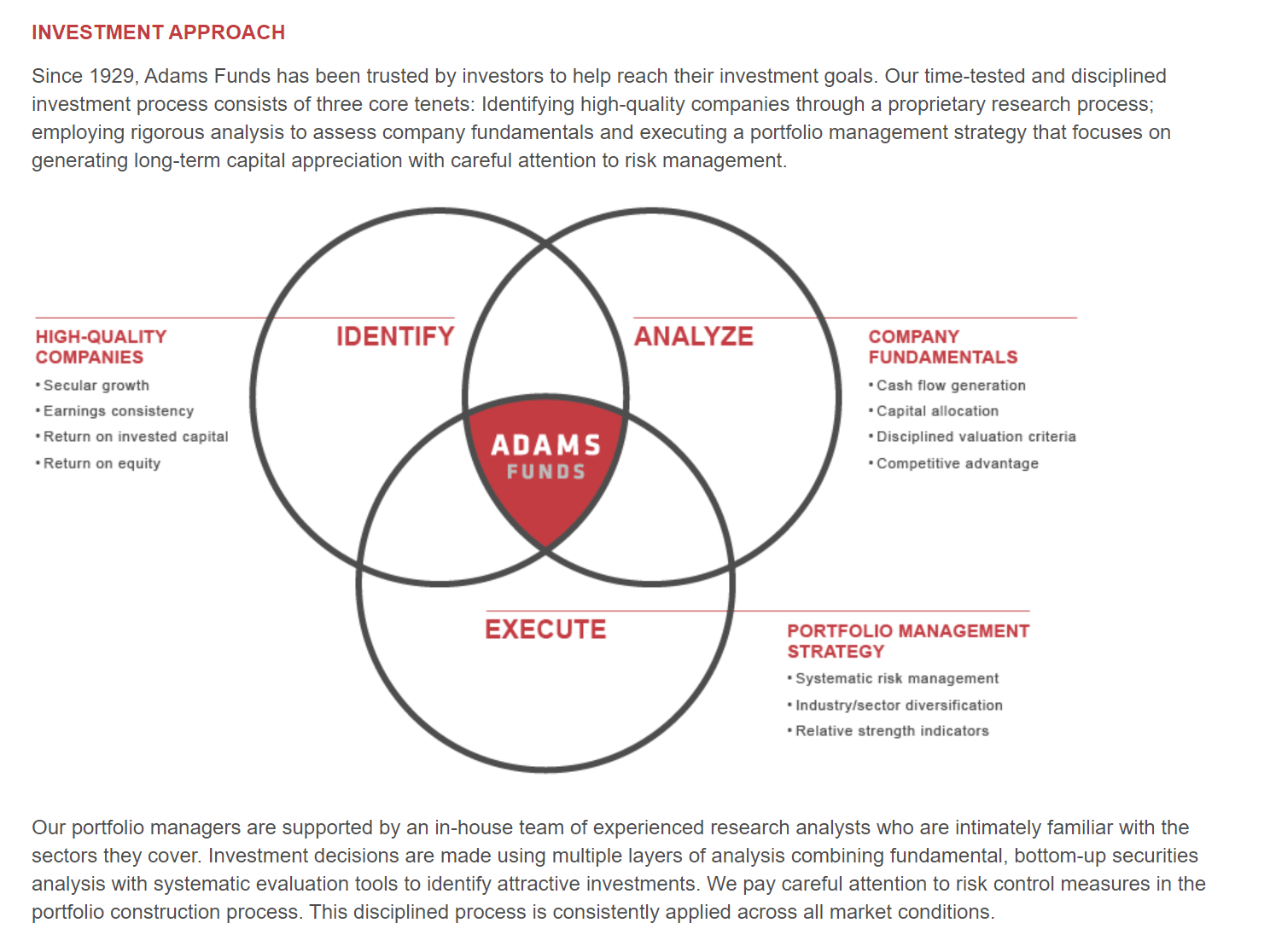

First, for those new to the ADX story, the Adams Diversified Equity Fund is one of the longest-running CEF with operations dating back to 1929. The ADX fund invests in a broadly diversified portfolio of high-quality large-cap equities using a time-tested investment process that looks at secular growth drivers to find companies with consistent earnings growth and returns on capital (Figure 2).

Figure 2 – ADX investment process (adamsfunds.com)

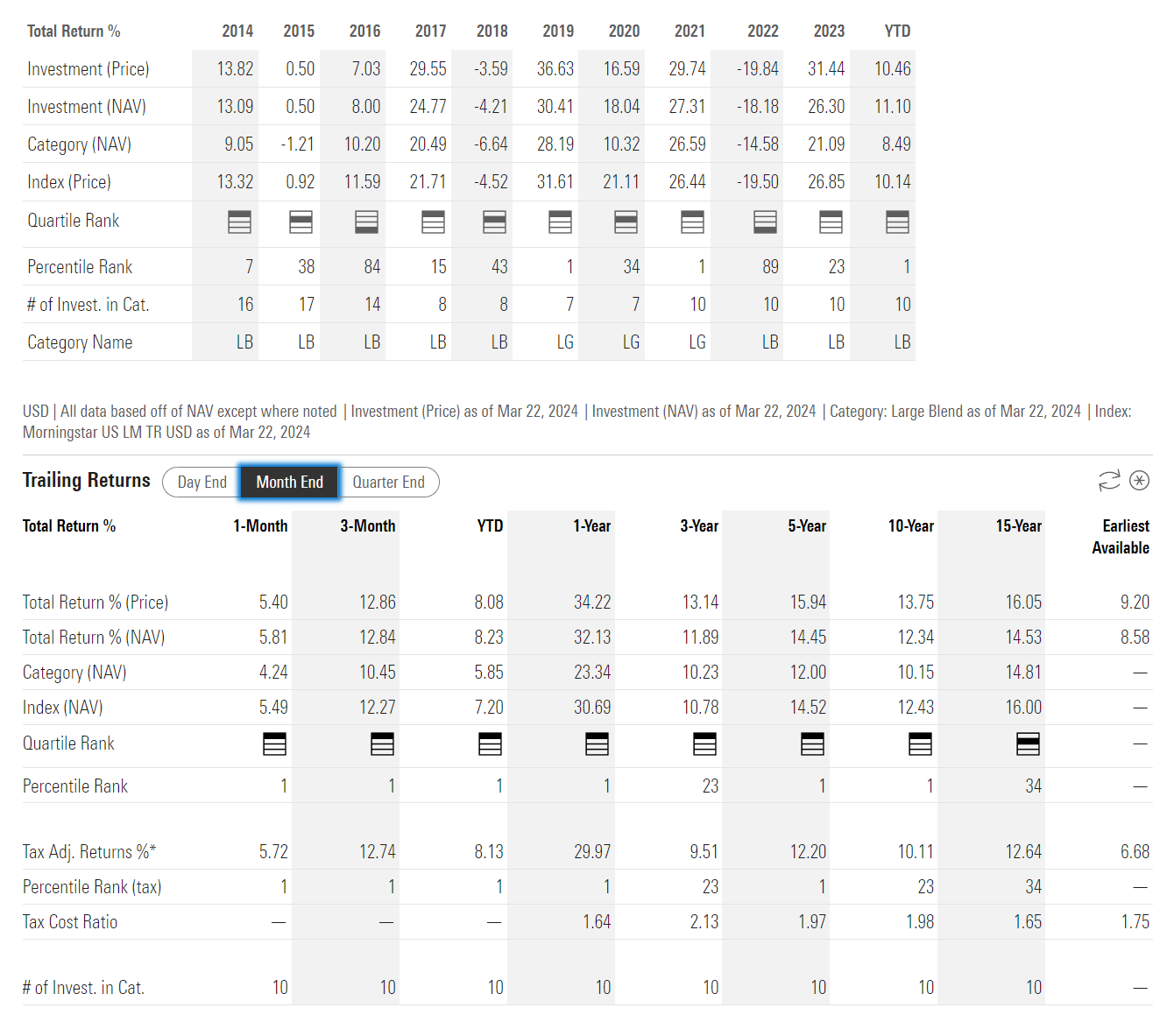

The ADX fund’s long-term performance is nearly unmatched, with an impressive 3/5/10/15 year performance of 11.9%/14.5%/12.3%/14.5% respectively to February 29, 2024 (Figure 3).

Figure 3 – ADX historical performance (morningstar.com)

While the ADX fund lags that of the S&P 500 Index by ~50-100 bps, it compensates for lower returns with its 6% minimum distribution, which is nearly 4x that of the market.

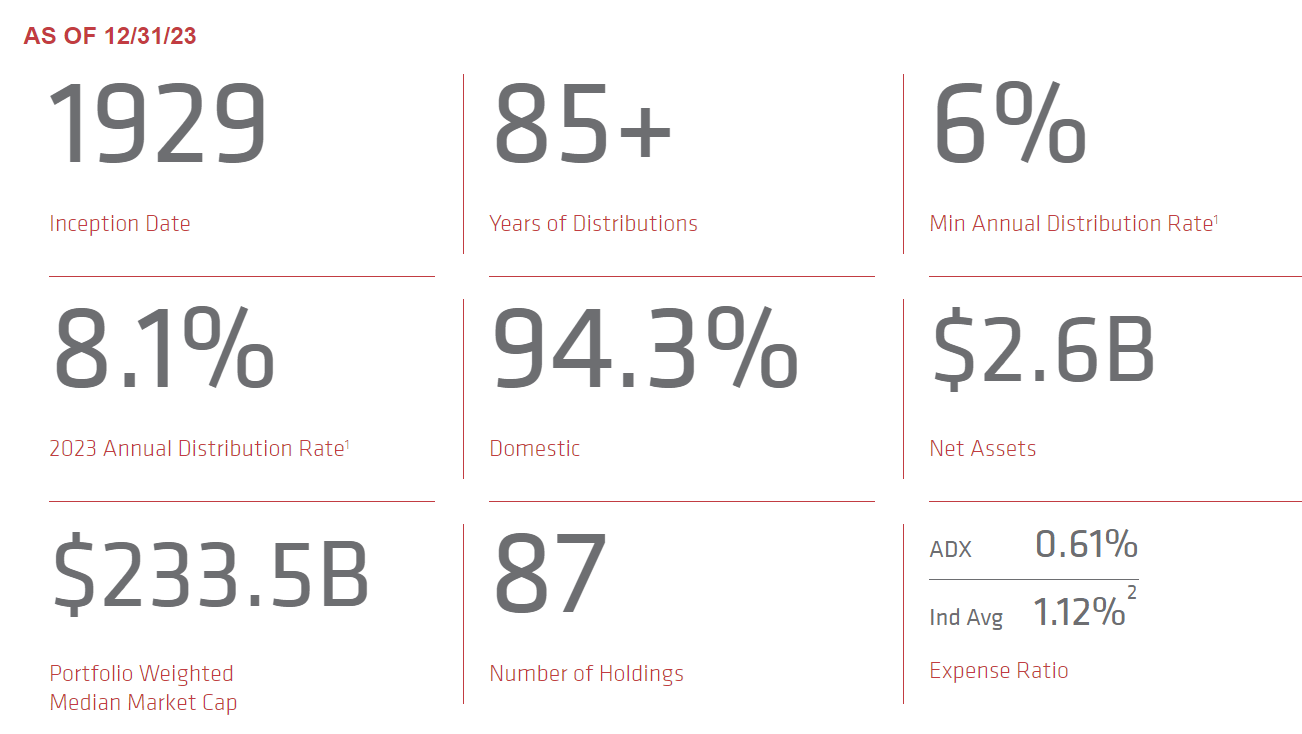

All-in-all, the ADX fund is an extremely impressive equity CEF that is well loved by investors, with $2.6 billion in net assets (Figure 4).

Figure 4 – ADX overview (adamsfunds.com)

Too Far Too Fast?

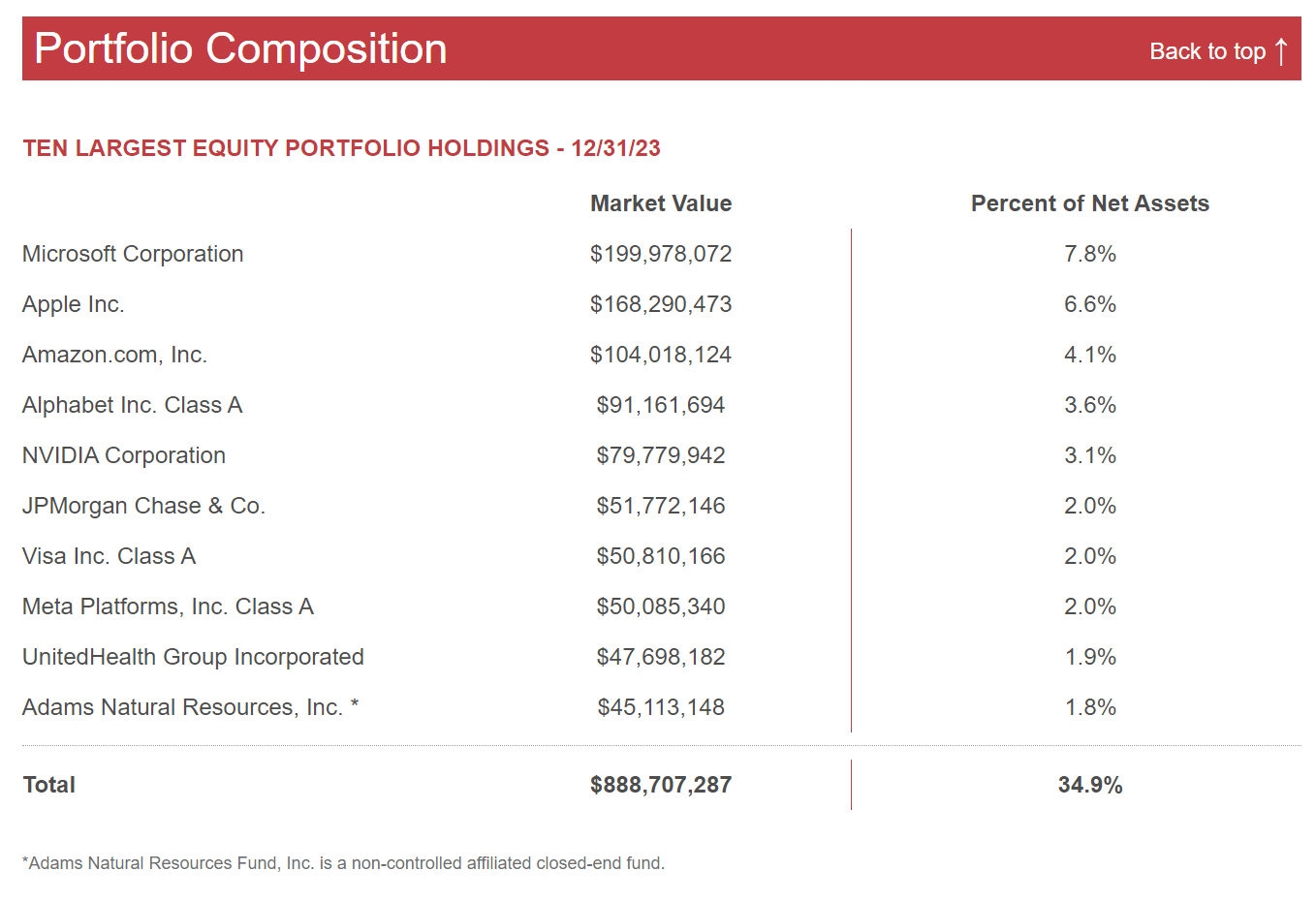

With respect to the ADX fund’s future performance, I am starting to get concerned, as I believe growth stocks have simply run too much, too quickly, with markets narrowly led by artificial intelligence (“AI”) stocks. For example, if we look at ADX’s top 10 holdings, we can see that the ADX fund’s largest holdings are mostly concentrated in the ‘Magnificent 7’ stocks, as I mentioned in my prior article (Figure 5).

Figure 5 – ADX top 10 holdings (adamsfunds.com)

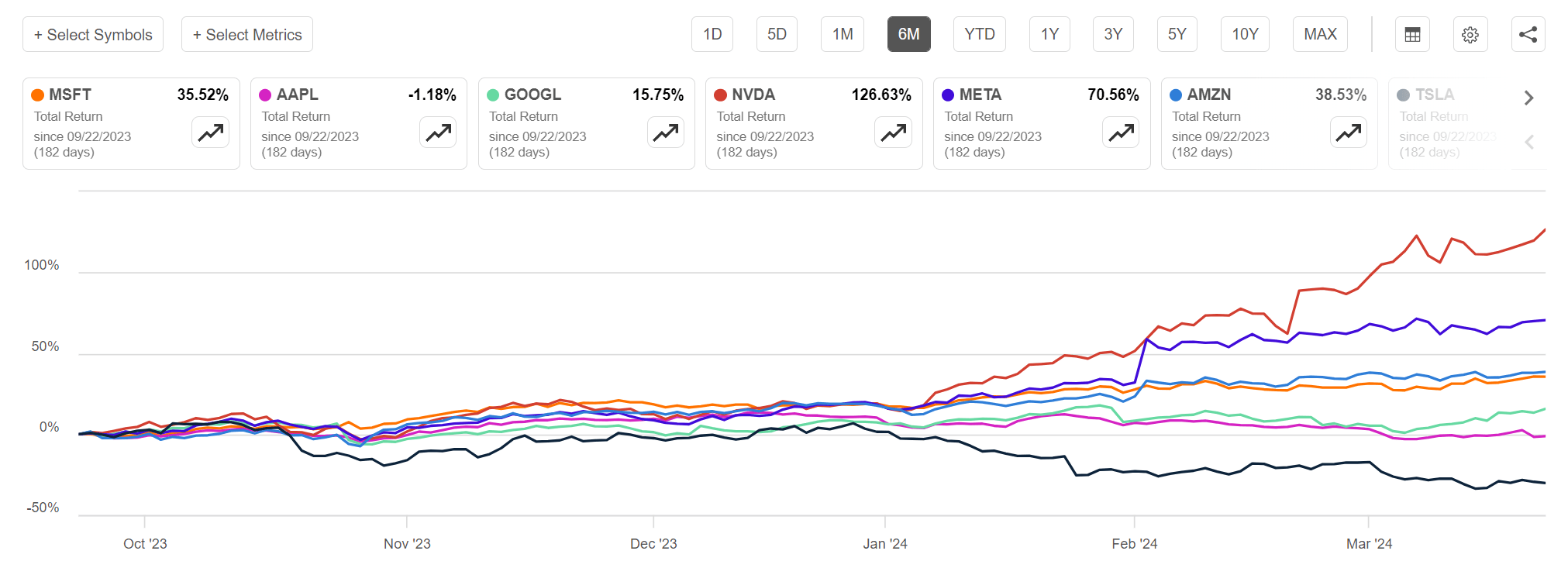

However, even within the ‘Magnificent 7’, leadership is narrowing, with Apple and Tesla exhibiting negative total returns in the past 6 months and Nvidia and Meta being the clear winners (Figure 6). Continued narrowing of market performance is not a healthy sign, as it increases the risk of a single company’s earnings or catalysts triggering a market-wide drawdown.

Figure 6 – Even Magnificent 7 leadership is narrowing (Seeking Alpha)

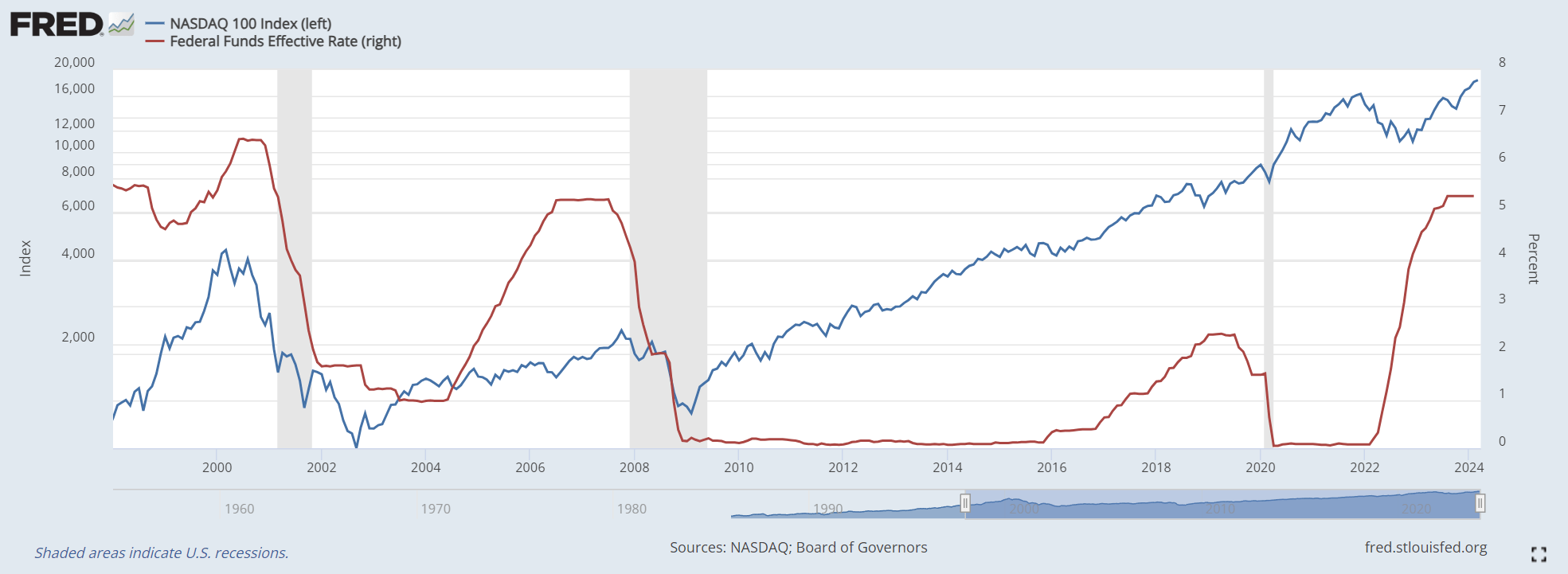

Recall in my prior article, I warned of a blow-off top rally, as macro conditions were very similar to 1999/2000, with “AI” replacing “dot-com” (Figure 7). That analogy continues to play out in real time.

Figure 7 – Analogy to 1999/2000 (Author created with price chart from St. Louis Fed)

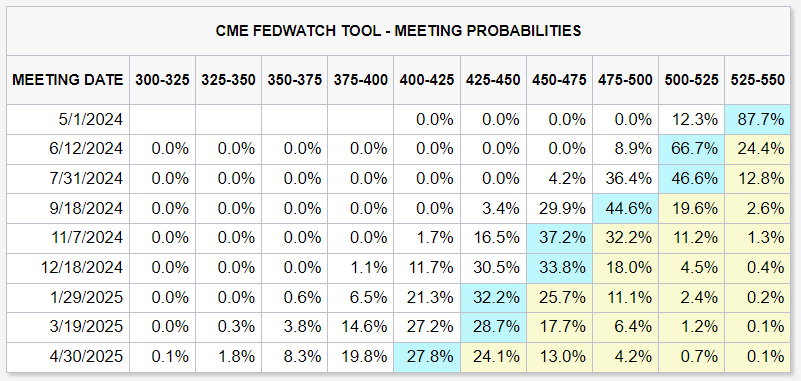

My main worry is that historically, equity bubbles ‘burst’ when the Fed cuts Fed Funds rates (to respond to prevalent economic challenges). As we near the expected date of the Fed’s rate cuts, I fear we may also be nearing the popping of this cycle’s equity bubble (Figure 8).

Figure 8 – Fed cut expected in June (CME)

Higher Interest Rates May A Hidden The Issue

With equity markets are making daily new highs and credit spreads nearing all-time lows, readers may question my caution, as everything appears to be smooth sailing.

However, readers need to remember that financial markets do not always represent the wider economy. With interest rates staying persistently high for more than a year, many parts of the real economy, like commercial real estate and consumer spending, are feeling the pressure.

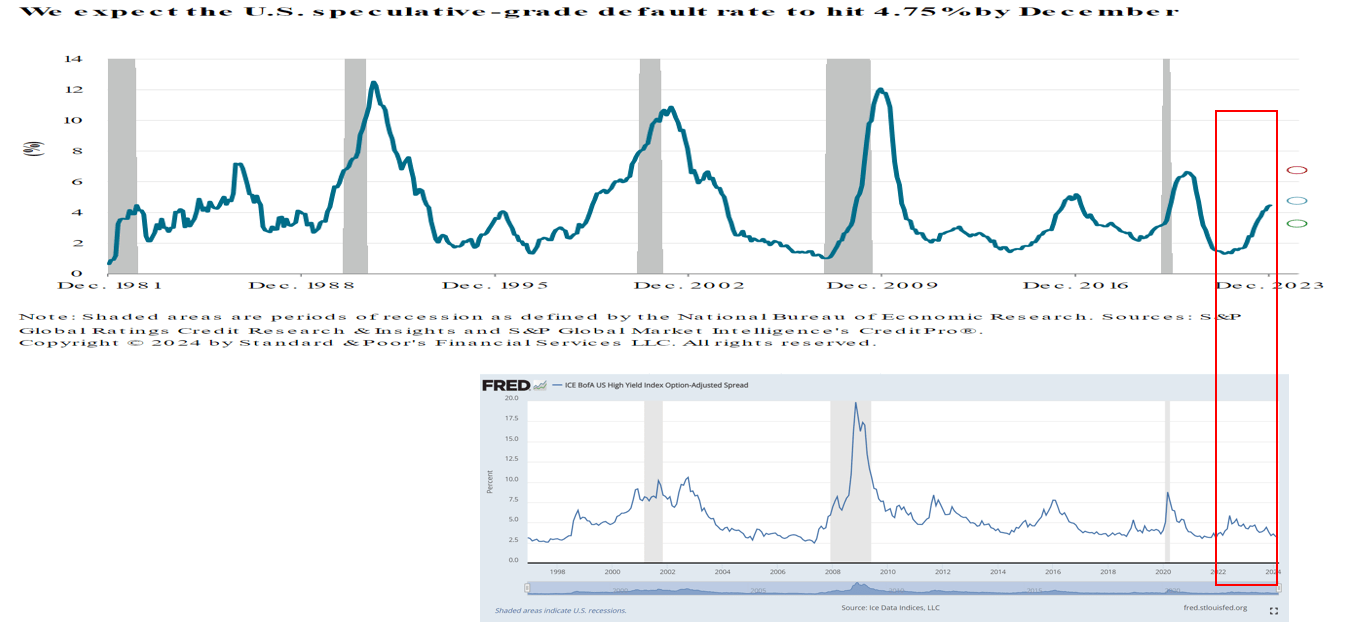

In fact, one warning sign that I have written about recently is a yawning gap between high yield corporate defaults and credit spreads (Figure 9).

Figure 9 – Yawning gap between defaults and credit spreads (Author created with charts from St. Louis Fed and S&P Global)

Basically, financial markets remain blissfully calm while corporate defaults and personal bankruptcies start to pile up.

Beware Equity Bubble Popping For The ADX

For the ADX fund, due to the nature of its investment process, it typically concentrates in the highest momentum growth stocks. This process works until it doesn’t.

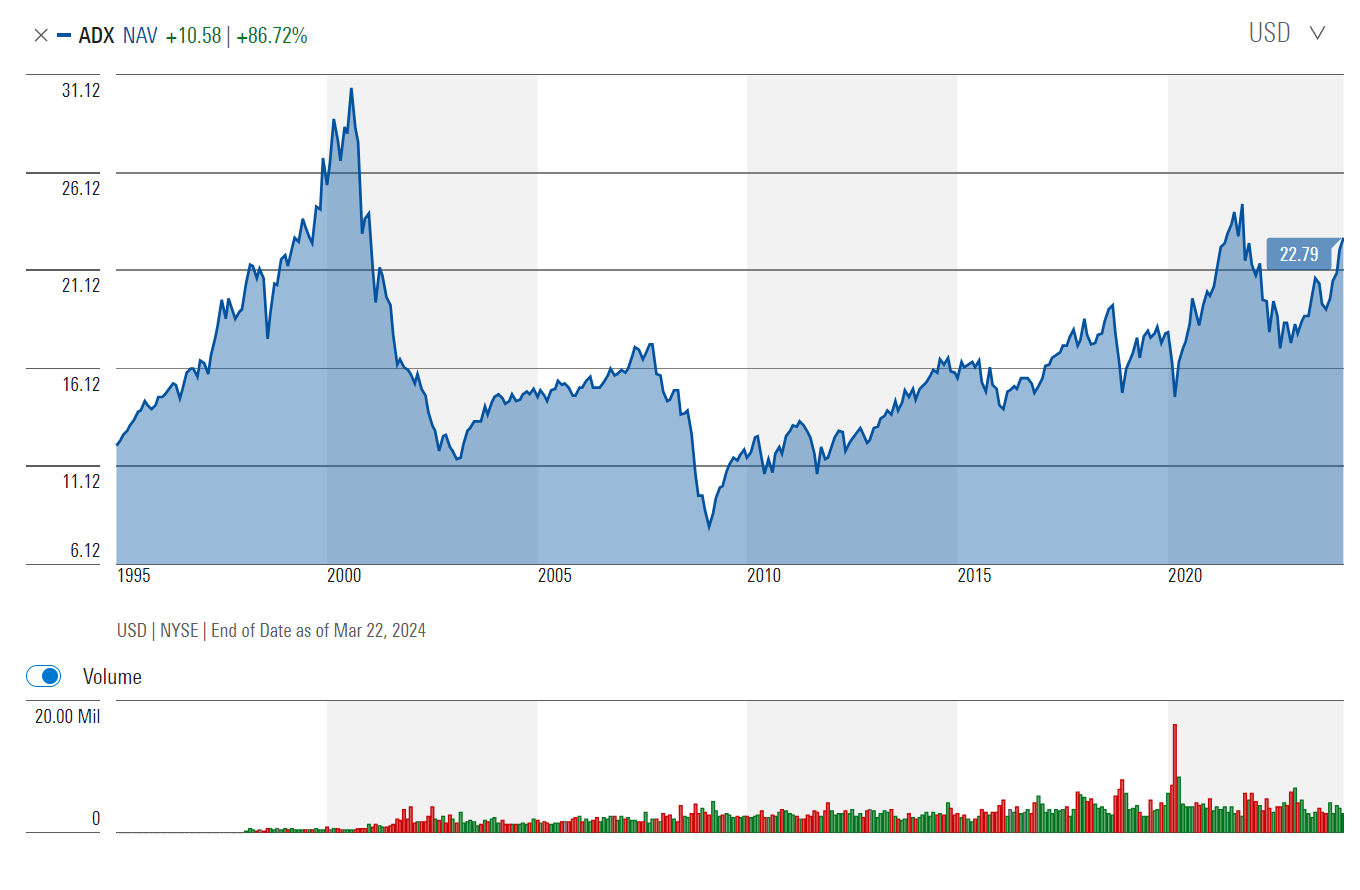

When the bubble popped in 2000, the ADX fund suffered a massive 62% decline in its NAV, and the fund’s NAV still has not recovered to early 2000 levels (Figure 10).

Figure 10 – ADX NAV is still below 2000 level (morningstar.com)

Due to the fund’s concentration in the ‘Magnificent 7’ growth stocks, I fear a similar drawdown may be possible should this “AI” bubble pop, therefore, I recommend investors start to reduce their exposures.

Risk To Being Cautious

Please note that I am not advocating a firesale of the ADX fund. What I am suggesting is that the margin of safety in holding these high-flying growth stocks is reducing, so investors should trim their equity holdings.

Equity markets may very well continue powering higher, led by Nvidia and its promise of AI riches. In fact, while the Fed is expected to begin cutting interest rates in June, it is very possible that the Fed may further delay rate cuts if the U.S. economy continues to surprise to the upside.

Conclusion

The Adams Diversified Equity Fund continues to deliver strong performance, rallying more than 27% since October. I had previously suggested a blow-off top similar to 1999/2000 may be brewing, and recent stock market performance is tracking that analogy.

However, with corporate and personal bankruptcies starting to pile up, I believe they will eventually affect equity performance. The key trigger will be the timing of Fed rate cuts.

With narrowing leadership and reduced margin of safety, I recommend investors start to reduce trim exposures to high growth equities like the ADX fund. I am downgrading ADX to a hold at this time.

Q2 2024 Earnings Call Transcript")