Boy Wirat

I cautioned investors in leading net-lease REIT W. P. Carey Inc. (NYSE:WPC) to be cautious about adding more shares in mid-January 2024, highlighting a much less attractive risk/reward profile. I urged investors to watch out for profit-taking possibilities in WPC, intensifying downside volatility. Accordingly, WPC has declined more than 16% since my caution, significantly underperforming the S&P 500 (SPX) (SPY). With WPC’s valuation dropping back into undervalued levels, I assessed it timely to reconsider whether WPC buyers should return and buy its recent steep pullback.

At a recent March conference, W. P. Carey management highlighted that the market “overreacted” to the WPC’s fourth-quarter earnings call. However, astute investors who observed WPC’s price action would have gleaned that WPC topped out in early January 2024, well before W. P. Carey’s earnings conference in early February 2024. Moreover, dip buyers have returned to defend WPC at the mid-$50s levels, corroborating W. P. Carey’s argument of a “favorable entry point.”

WPC investors should recall that the market justifiably de-rated WPC heading into its FQ4 release. WPC posted forward guidance below analysts’ estimates. W. P. Carey management emphasized that 2024 is designated to be a “transition” year as the company divests its office portfolio, refocusing its attention on industrial and retail properties. The divestment is expected to be completed by the first half of 2024, as the office properties segment accounted for less than 3% of its annualized base rent.

However, the market was likely concerned with ongoing restructuring in W. P. Carey’s portfolio, heightening execution risks even as it looks to move on from its office exposure. Furthermore, its downgraded forward outlook will put more pressure on W. P. Carey management to source suitable growth assets to lift WPC’s AFFO before the REIT can improve its dividend payouts subsequently.

W. P. Carey guided for a 2024 AFFO outlook of between $4.65 and $4.75, with a midpoint metric of $4.7. This aligns with analysts’ estimates of $4.7, projecting a decline of 9.3%. Management also highlighted that the targeted payout ratio will be reduced to the “low to mid-70% range” as W. P. Carey looks to reinvest to generate dividend growth moving forward.

W. P. Carey anticipates an investment volume of about $1.75B at the midpoint for FY24. The company updated in early March that $200M in deals had been “completed through the earnings release” in February. In addition, W. P. Carey has also allocated another $100M to fund new other projects, indicating a $300M pipeline visibility.

With the Fed expected to cut interest rates three times in 2024, it should alleviate the bid/ask spread between buyers and sellers, as spreads are expected to normalize. Moreover, the ongoing dislocation in the capital markets should provide W. P. Carey opportunities to leverage sale and leaseback transactions, providing much-needed liquidity to the market. With W. P. Carey supported by $1B in cash on hand bolstering its balance sheet, the company looks well-primed to capitalize on improved market sentiments as REITs look to emerge from their long-term bottom.

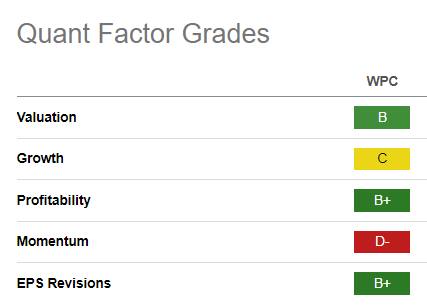

WPC Quant Grades (Seeking Alpha)

WPC’s valuation looks more favorable at the current levels, and it was assigned a “B” valuation grade by Seeking Alpha Quant. Its forward dividend yield of 6.2% looks relatively attractive compared to its 10Y average of 5.9%.

However, WPC’s “D-” momentum grade suggests buying sentiments remain tepid, suggesting the market is likely awaiting an improved investment cadence before potentially re-rating WPC.

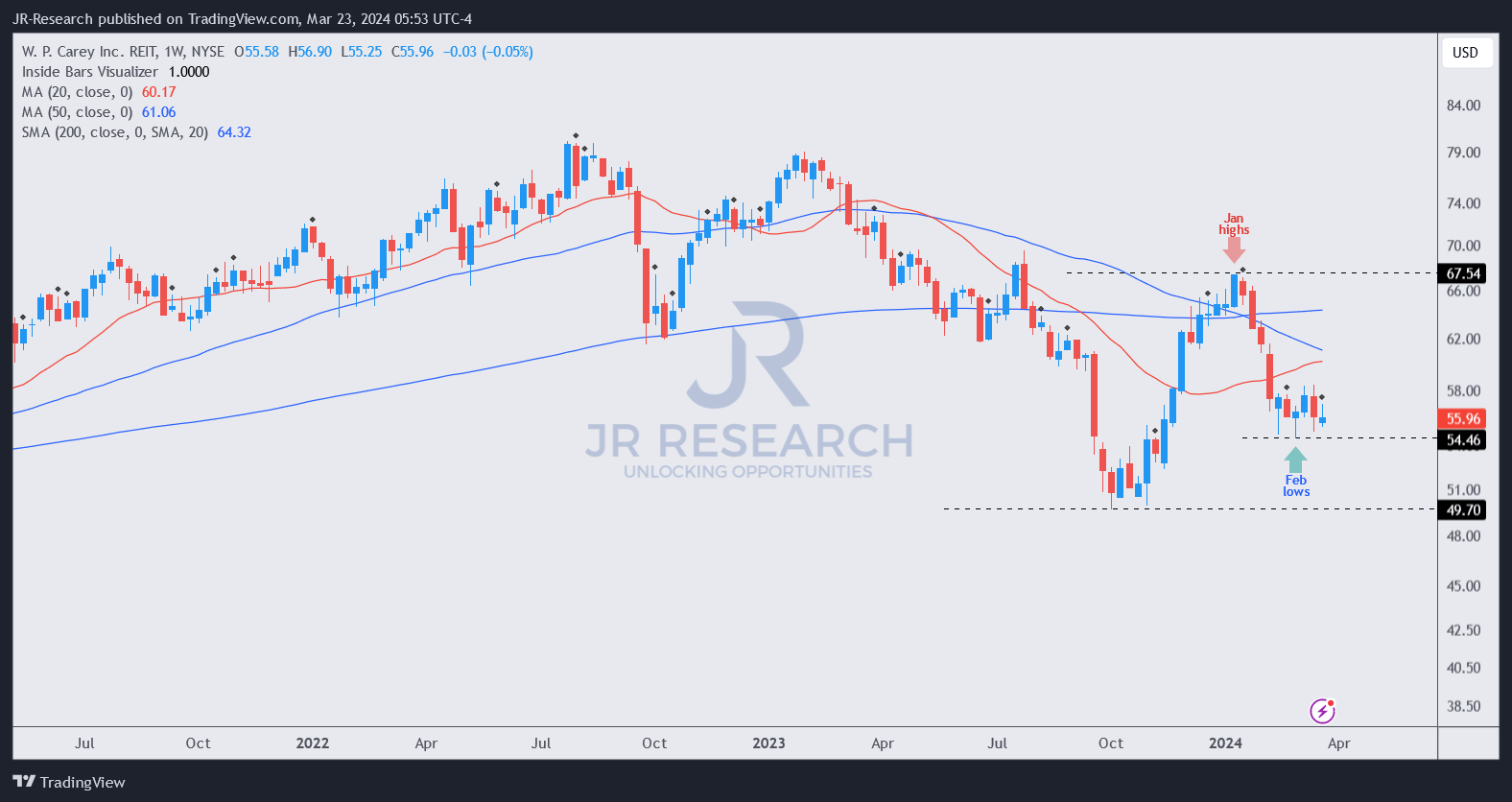

WPC price chart (weekly, medium-term, adjusted for dividends) (TradingView)

As seen above, WPC buyers have returned to defend the mid-$50s levels, helping the stock to consolidate over the past six weeks. It has also remained well above its October 2023 lows at the low-$50s levels, corroborating well for WPC’s ongoing recovery.

With the interest rate headwinds expected to be less hawkish in 2024, it should improve W. P. Carey’s growth opportunities to recover its AFFO post-office exit.

Bolstered by a constructive valuation, I assessed the current levels as an opportune moment for WPC buyers to add exposure.

Rating: Upgrade to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Q2 2024 Earnings Call Transcript")