fotostorm

Thesis

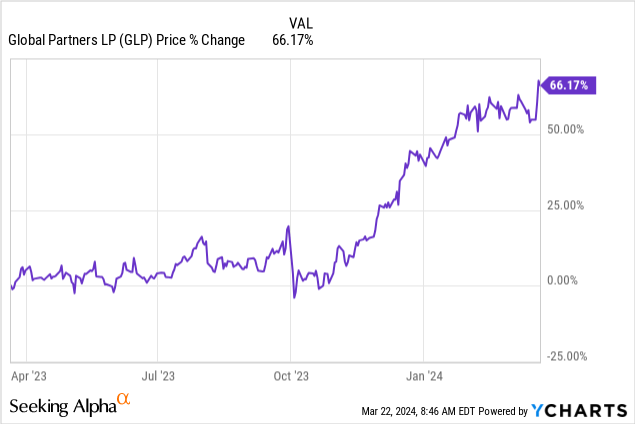

Global Partners (GLP) is a U.S. Master Limited Partnership (‘MLP’) which functions as an owner, supplier and operator of gasoline stations and convenience stores. The MLP has seen its common shares rocket upwards in the past year, on the back of better than expected profitability and expansion plans:

As an MLP, the company runs a large amount of debt, structured as revolving credit lines, debentures and preferred shares. The company currently has two series of preferred shares outstanding, with the Series A set to be retired on April 15, 2024. We covered GLP.PR.A in a separate article here, where we outlined why we were anticipating the debt to be called.

For a retail investor who missed the rally in the common shares, there is only one series of preferred shares outstanding now, namely Series B (NYSE:GLP.PR.B). In this article we are going to have a look at the structure of the preferred shares, their analytics, and the reasons for which we find them attractive from both a company perspective as well as a macro perspective.

MLP preferred shares – what you should look out for

MLPs or Master Limited Partnerships, represent corporates that don’t pay federal income tax, but rather see their profits and losses passed through to investors, who then pay taxes on their share of the earnings. This ‘pass through’ model applies for businesses that generate a steady, predictable stream of income. Thus many MLPs are involved in the energy sector, owning assets like pipelines, storage tanks, and even oil and gas properties.

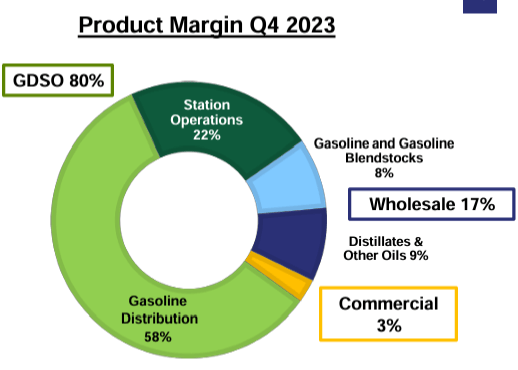

GLP is one of the largest operators of gasoline stations and convenience stores in the U.S. Northeast, and derives most of its product margin from gasoline distribution:

Product Margin (Company Presentation)

The MLP model relies on a steady stream of cash-flow and on relatively high levels of debt. Prior to the Covid crisis many MLPs were running debt/EBITDA ratios in excess of 4x, but those figures have come down after many of the corporates experiencing potential bankruptcy instances.

Preferred shares are categorized as equity on the balance sheet when they are perpetual, and thus are not included in the debt/EBITDA ratio. GLP had issues two series of preferred shares, specifically because they would not affect debt/EBITDA.

The company however has experienced growth, with an increase in EBITDA figures, which has moved its debt ratio to a very conservative level:

Leverage Ratio (Company Presentation)

When investing in MLP preferred shares, an investor needs to be mindful of one large risk factor, namely Chapter 11 restructuring/bankruptcy. Outside of a bankruptcy proceeding, preferred shares can be viewed akin to long duration debentures.

Many MLPs experienced distress during the Covid crisis because the revenue figures decreased, but more importantly because the debt on the balance sheet was not structured properly, with many near term maturities. Companies used to love near term maturities because the cost of funds was cheap. They learned there is a business cost to that during Covid.

New debt issued used to retire preferred shares

GLP is acutely aware of smart balance sheet management, and has $400M of 7.00% senior notes due 2027 outstanding, and $350M 6.875% senior notes due 2029. In addition to the above term debt with maturities above 3 years, the company recently issued in January 2024 $450 million of 8.250% senior unsecured notes due in 2032:

The company said that it intends to use the net proceeds from the offering to repay a portion of the borrowings outstanding under its credit agreement and for general corporate purposes.

While some of the proceeds were used to repay amounts outstanding under the credit facility, a portion of the debenture cash was used to retire the GLP.PR.A preferred shares, given their current yield in excess of 10%.

Please note the attractiveness of the debenture yield, with the company being able to issue 8 year debt at Treasuries+3%. The reason for this issuance is the retirement of expensive funding on the back of a low leverage ratio.

Given its conservative balance sheet management, increased growth and long dated debenture maturity profile, we do not expect GLP to issue preferred shares in today’s environment, leaving just GLP.PR.B outstanding.

State of the balance sheet

Retail investors have access to the GLP balance sheet and income statement via the Seeking Alpha platform in the Financials Tab. If one looks at the historic progression for the net debt on the GLP balance sheet they will notice a constant figure of roughly $1.5 billion:

Net Debt (Seeking Alpha)

The above are annual figures, and they have remained fairly constant. What has changed though is EBITDA, which has grown significantly:

EBITDA (Seeking Alpha)

While the debt figure has stayed fairly constant, EBITDA has grown by 40%, thus making the debt coverage ratios for the company much more attractive, and reducing the need for preferred share utilization in the capital structure.

How does GLP.PR.B compare to other preferred shares

Unlike ETFs or CEFs with similar mandates, individual corporates are not fungible, especially in the niche MLP space. We are not aware of another gasoline distributor MLP that would have preferred shares outstanding, thus GLP is a fairly unique company which needs to be assessed on its own risk and rewards. Utilizing transportation MLPs as a comparison would not be correct since pipeline companies have a different revenue stream model when compared to GLP.

At what point we would be less interested in buying GLP.PR.B

As described in the yield analytics section below we expect a 3 year tenor for the preferred shares, which currently values them from a yield perspective at T+4.5%. Given high yield spreads are at 300 bps, the spread pick-up is 150 bps against general high yield collateral. The spread is justified given the capital structure allocation and waterfall of payments in case of a bankruptcy. A spread below 100 bps would be considered too tight for us, so we would not buy GLP.PR.B at current yields below 8.5% in the current spread environment.

Forward-looking expectations for the company

The company has proven to be a savvy operator via its EBITDA expansion, on the back of a constant debt utilization. This growth has been fully reflected in its common equity, as illustrated via its 66% gain in the past year.

For preferred equity holders the company growth is not that important since there is no upside with a call price at $25/share. However, as the article describes the solvency of the entity is what matters. With a debt maturity profile layered out in the future (the first debenture matures in 2027), there is nothing from a balance sheet perspective that can constitute a trip-wire in the near future.

Profitability will be monitored via net income figures as well as debt service coverage ratios and free cash flow operating figures to ensure ample coverage of debt service.

Attractive yield for the Series B preferred shares

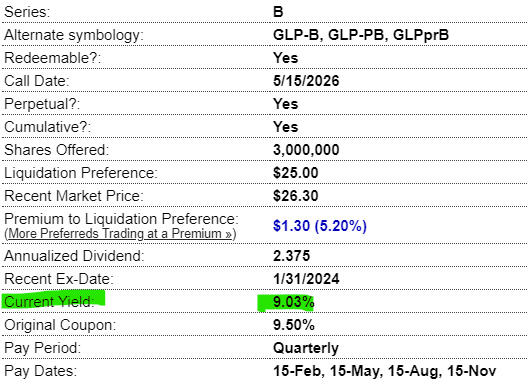

The Series B are fixed rate cumulative preferred units issued at 9.5% coupon but with a 9% current yield:

Yield (PreferredStockChannel)

The series are well set-up for the current macro environment where rate hikes are behind us, with the Fed now discussing when rate cuts will begin exactly in 2024. Fixed rate debt will benefit as the Fed lowers Fed Funds.

It is interesting to note how well the market perceives GLP, given the very narrow spread of around 100 bps between the 2032 debt and the preferred shares. The wider this spread the higher the perceived riskiness of an issuer. Why? Because in a Chapter 11 restructuring debt holders are set for a very high recovery for asset rich companies like GLP, whereas preferred equity is very likely to get completely wiped out.

While common equity embeds growth prospects, and we have seen GLP common shares rally hard, the preferred equity acts like debt for healthy companies. In today’s macro environment picking up 9% yielding preferred shares with an estimated duration of 3 years is an attractive risk/reward proposal. While the first call date is only 2 years away, we do not think GLP will call the series right away, waiting for lower risk free rates, thus we are adding a 1 year tenor to the initial call date.

Conclusion

GLP is an MLP that operates gasoline stations and convenience stores in the U.S. Northeast. The company has experienced EBITDA growth, which has lowered its debt ratios and has boosted its common shares. The company is a very smart balance sheet manager, having termed out its debt, with the latest issuance coming in January 2024. Part of the proceeds from the latest debentures will be used to retire the Series A preferred shares on April 15, 2024. Retail investors having missed the common shares rally can look at the only remaining series of preferred shares, namely GLP.PR.B. The shares yield 9% and have a 2026 first call date, with our base case expectation for an actual 2027 retirement/call. Under the current balance sheet structure we see no risk that would put GLP into a Chapter 11 restructuring until the expected GLP.PR.B redemption, thus making the remaining preferred shares a very attractive risk/reward proposal in today’s macro cycle where rate cuts are expected.

Q2 2024 Earnings Call Transcript")