Anna Moneymaker/Getty Images News

The FOMC meeting this week surprised many when it was revealed that the Fed still intended to cut rates three times in 2024. It seemed that given the back-to-back, hotter CPI inflation report to start the year and rising inflation expectations, the Fed would begin to push back against the easing of financial conditions witnessed since early November.

However, the Fed may be sending the wrong message at this point, seeming too eager to lower rates. This could be a giant mistake, especially if the trends of the past two months persist and if the inflation swaps market is correct about inflation over the next few months. Additionally, the recent easing of financial conditions means that commodities like oil and gasoline could see further upside, fueling headline inflation even further.

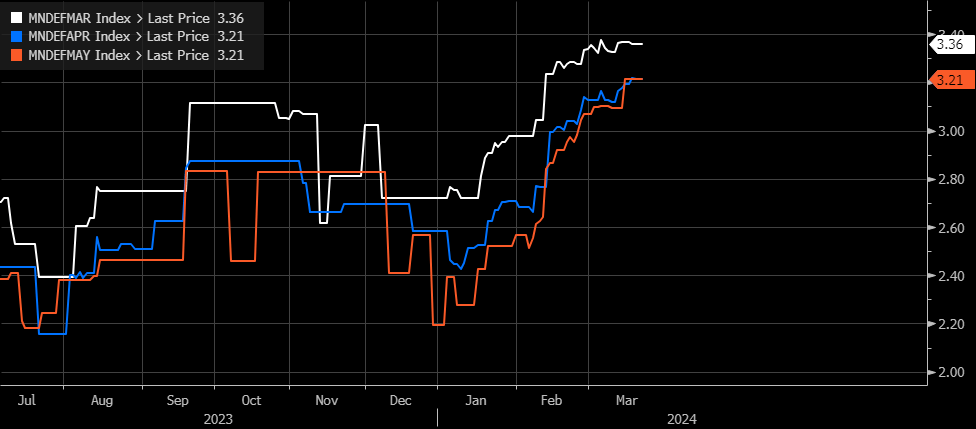

The Market Doesn’t See Inflation Falling Further, Not Yet

Currently, swaps are priced in CPI at 3.4% year-over-year in March and at 3.2% in both April and May. So, at least based on these estimates, it would seem to suggest that the bump in the inflation rate we saw in January and February may have been due to more than just seasonal effects.

Bloomberg

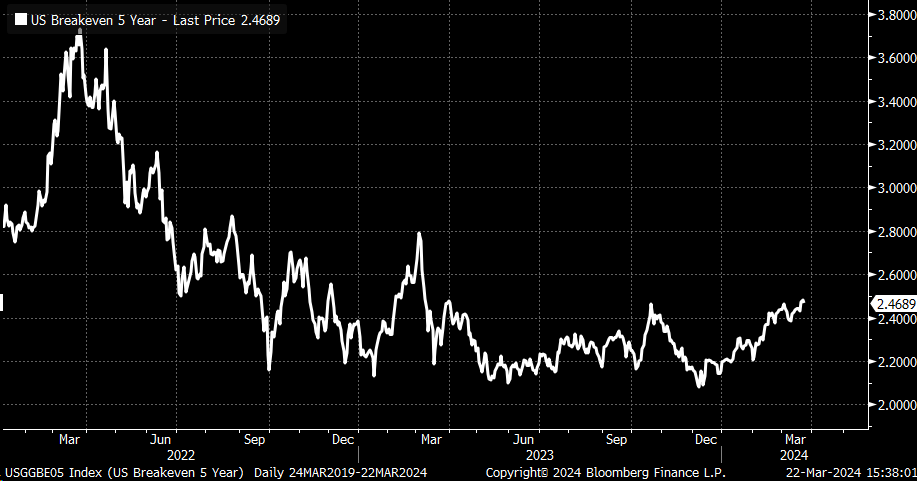

Additionally, this week, 5-year inflation breakevens rose to 2.47%, their highest level since March 2023, after turning higher since the middle of December. This change in inflation breakevens came around the same time the Fed announced it would start cutting rates in 2024.

Bloomberg

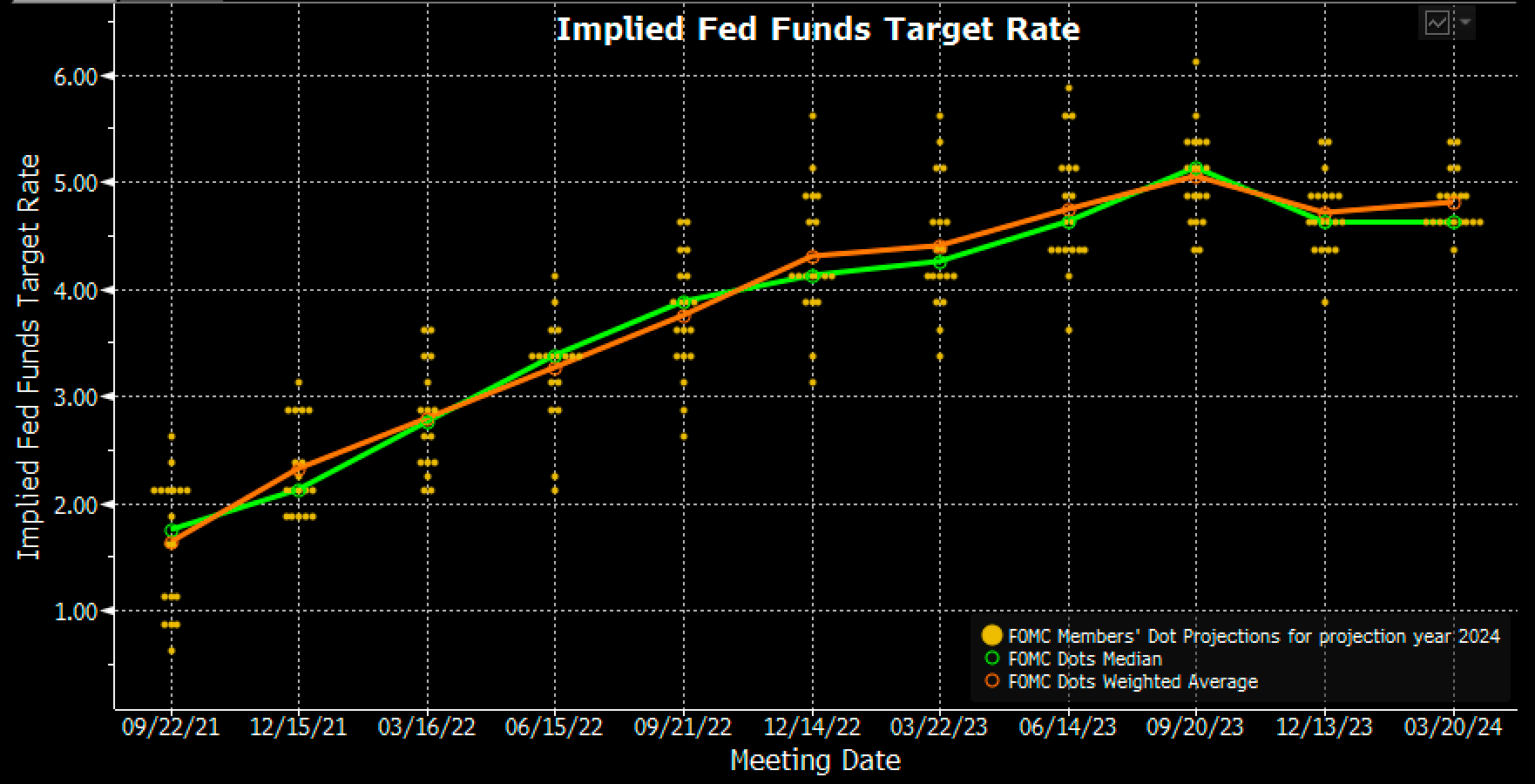

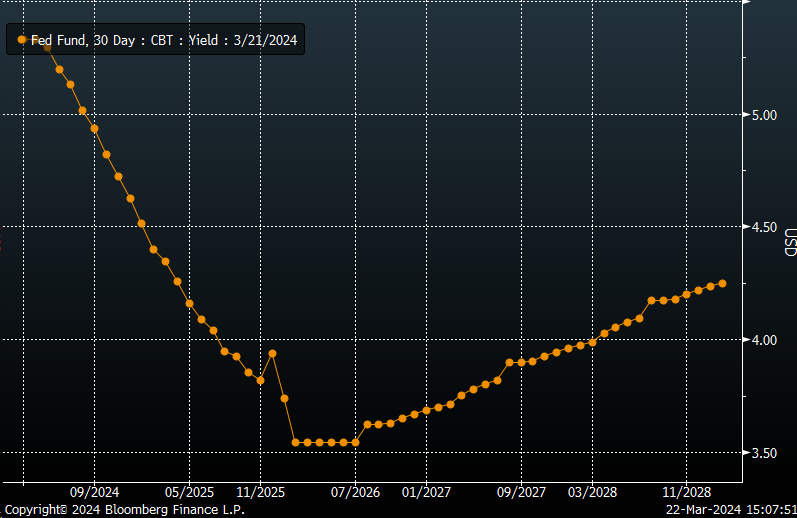

The Fed Is Taking Rate Cuts Away, Higher Neutral Rate

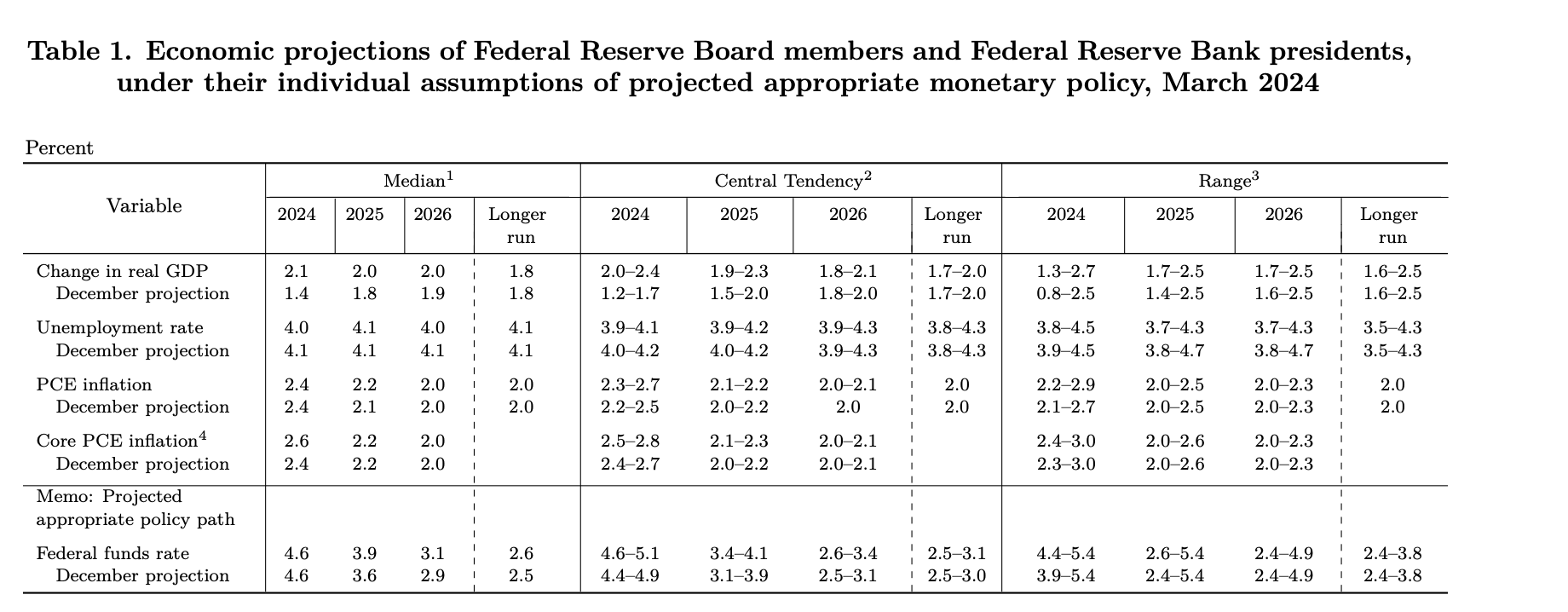

The only solace is that the dot plot shows that while the median dot remained unchanged at 4.6%, the average weighted dot increased by 4.81% in 2024 from 4.70% at the December meeting. Also, the overall positioning of the dots shows that the Fed is coming much closer together, around 2 or 3 rates for this year. So, it is still possible that if the inflation data comes in hotter, the Fed could take away a rate cut or two from this year.

Bloomberg

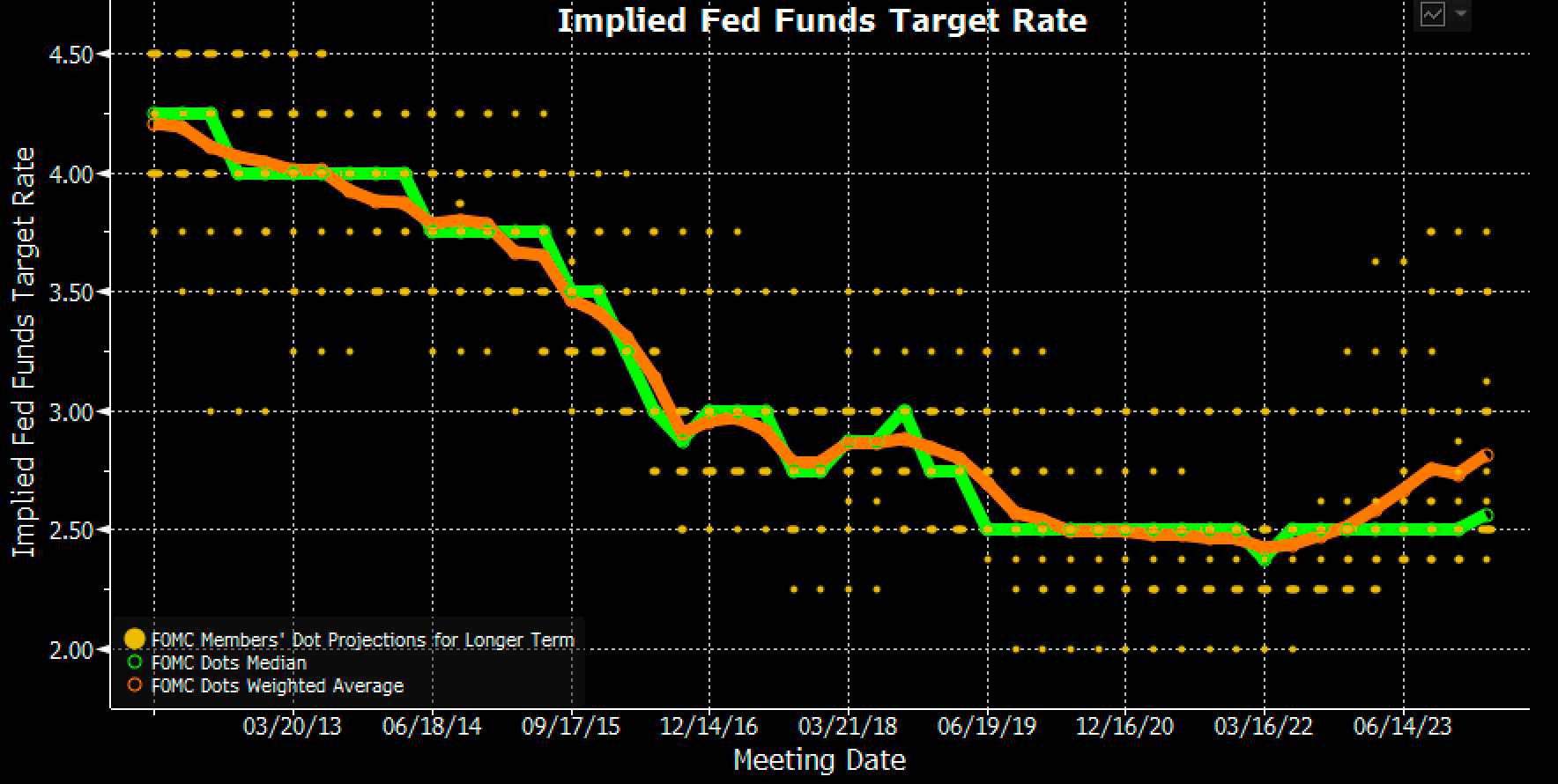

Additionally, rate cuts for 2025 were removed from the forecast, with the median now at 3.88%, up from 3.62% in December. Meanwhile, the forecast for 2026 went up 3.12% from 2.875%. Also rather important is that the Fed is starting to come around to the neutral rate being higher than previously thought, with the longer-run rate rising to 2.56% from 2.5%, while the median average weight rose to 2.81% from 2.72%.

What is odd about this longer-run project rate is that inflation is hotter than in the past decade, unemployment seems lower, and growth feels stronger. Yet, the Fed sees the longer-run rate as lower than it is even as late as 2019. This could suggest a longer-run rate that is going higher.

Bloomberg

While none of this for now indicates that rates are going higher, it is an acknowledgement that the economy is more robust than expected and that days of ultra-low interest rates are probably behind us. Fed Fund futures currently see the neutral rate of the economy higher than the Fed, with rates bottoming at 3.6% in 2026 and then rising again. Still assuming a 2% headline PCE rate, it would suggest a real interest rate of 1.6%, not the current Fed projection of 0.6%. This could also suggest that policy is not as tight as the Fed thinks and is possibly another reason why 5-year breakeven inflation expectations are rising.

Bloomberg

More Tolerant

Additionally, based on the dots, it seems the Fed will tolerate hotter inflation, with core PCE now expected at 2.6% in 2024, up from 2.4%. Meanwhile, headline PCE was revised higher in 2025 to 2.2% from 2.1%. Additionally, growth is expected to be stronger, with GDP in 2024, 2025, and 2026. This means that nominal GDP growth will run hotter, too, when adding the real GDP with the PCE projections together.

FOMC

The problem is that if the Fed is tolerant of hotter inflation and still intends to cut, it could mean that it is about to make a similar mistake it made the last time: waiting too long to raise rates.

This is not to say that the Fed should raise rates from here; the Fed should be more careful about cutting rates and signaling its eagerness for those cuts at this point. Right now, the Fed seems to be giving the impression it wants to cut no matter what, and that may be the wrong impression to give at this point in the game, especially if the swaps market turns out to be correct.

Q2 2024 Earnings Call Transcript")