Andreus

When one thinks of a small cap company that delves into the space, data and AI sectors, profits are generally not something that comes to mind. An exception to that rule may be Spire Global, Inc. (NYSE:SPIR). The stock has been on an absolute tear, with a chart similar to NVIDIA Corporation (NVDA) and all of the other AI hangers-on during the extreme sector bull run over the past several months. It was an announcement of a collaboration with NVDA that took the stock to meme-level oversold territory last week. The company promptly announced a financing at $14.00, which may have temporarily halted the stock’s run. However, I believe that Friday’s close at around $12.00 represents an ideal level to buy in as it’s a 14% discount to the financing, likely a discount created by momentum traders exiting at a loss.

As the impact of climate change becomes more apparent, the value of the data collected from SPIR for climate and weather patterns will only become more valuable. However, there have been two articles on Seeking Alpha on the company within the last month. If readers want a general overview of the company, they can read those two pieces. My analysis will focus on the capital raise and the positive impact this will have on the stock’s valuation going forward. While those other two authors gave a hold rating on SPIR, the recent pullback and the improved balance sheet has me believing the stock is worthy of a strong buy rating.

The financing and its future impact on the financials

Spire announced a registered direct offering of 2,142,858 shares of Class A common stock at a purchase price of $14.00 per share, raising gross proceeds of approximately $30 million. The financing also comes with 2,142,858 warrants that expire on July 3, 2024 at a strike price of $14.50. If exercised, the warrants would bring in an additional $31 million. This is a rather unusual deal, as warrants generally have a term of a year or more. The fact that it is structured with such a close expiration date leads me to believe that whoever wanted to invest in the company at these terms believes that SPIR will be well above $14.50 in the coming three months in order to exercise the warrants. Otherwise they would require a much longer date to expiry.

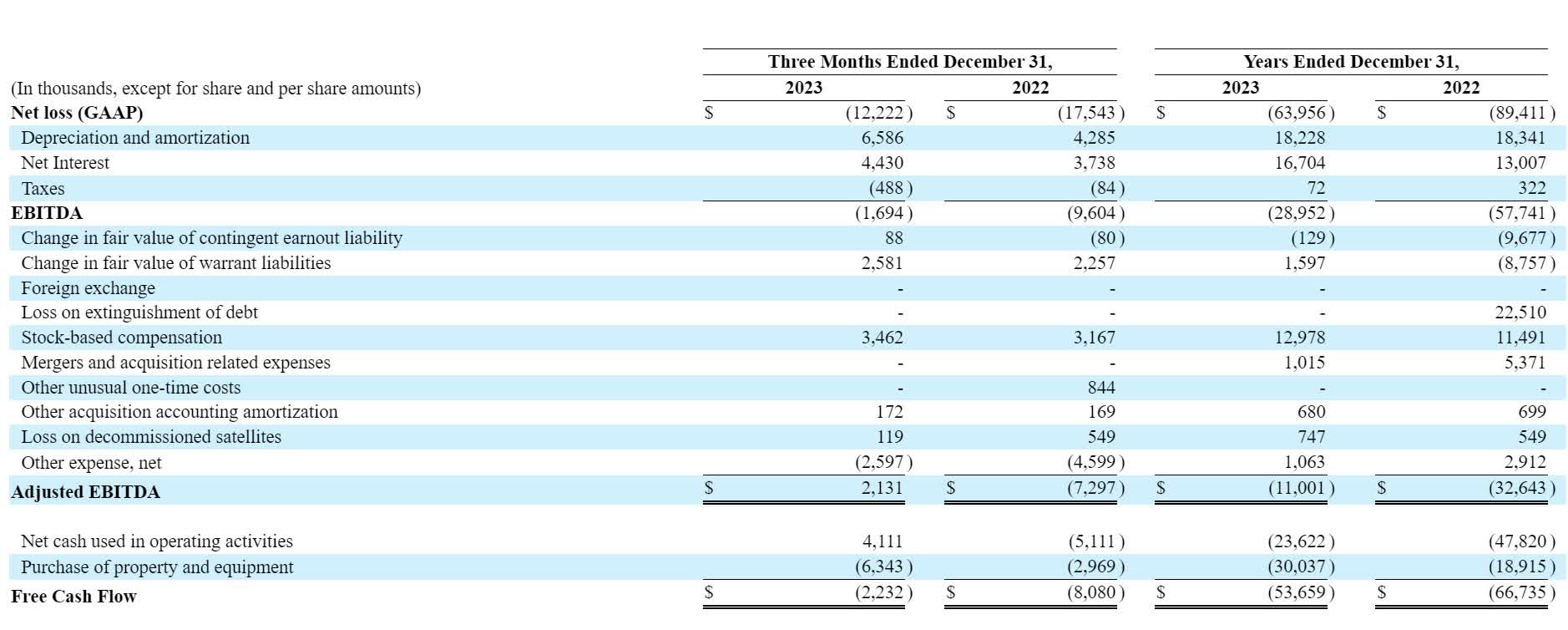

Assuming the warrants get exercised, that will result in the number of shares outstanding growing 19% from 22.1 to 26.4 million. It will also bring in nearly $60 million in cash to the company, net of fees. SPIR has a $118 million loan outstanding from Blue Torch that comes with covenants and a SOFR rate that currently sits north of 13.6%. This has resulted in the company incurring $17 million in net interest expenses for 2023. Reviewing the Q4 financials shows the impact that the interest expense had:

SEC.gov

When a company shows massively negative operations no matter what metric it uses, interest expense is just one line of many charges. At that point in time it’s more important to keep the company solvent than it is to optimize the balance sheet. That’s why SPIR had to settle for the Blue Torch loan in the first place. However, the Q4 numbers paint a different story. Adjusted EBITDA was $2.1 million for Q4, operating cash flow was $4.1 million while free cash flow was -$2.2 million. Had the company not incurred $4.4 million of interest expense, it would have achieved positive FCF for the quarter.

2024 guidance also paints a positive picture:

SEC.gov

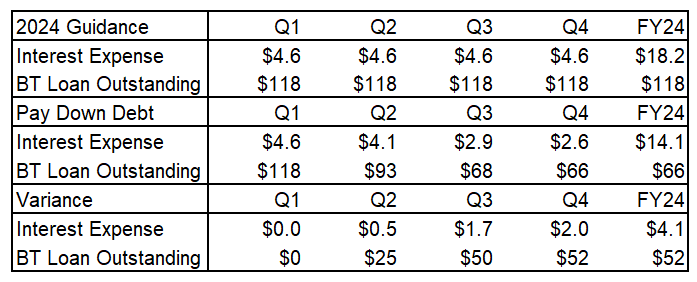

Midpoint revenues for Q1 and the year are $28 million and $143 million, respectively. Midpoint adjusted EBITDA for Q1 and the year are -$1 million and $16 million, respectively. Unfortunately SPIR does not forecast FCF, though on the conference call, management stated that the company anticipates that it will be FCF positive by the summer. Assuming capital purchases align to depreciation, FCF should track reasonably closely to adjusted EBITDA. The main difference between them should be the interest expense. Interest expense is projected to be $18.2 million for 2024, so subtracting this total from the midpoint adjusted EBITDA of $16 million leads to -$2.2 million in FCF for the year. This would align with management’s statement of being FCF positive by the summer. Where Q1 and Q2 are negative, Q3 break even to slightly positive and Q4 positive for an annual number that is just under the breakeven mark.

If SPIR was to use $50 million of the cash injection from the raise to pay down debt, I propose a payment schedule outlined below. Early termination fees are currently 2% of the principal repaid, but that drops to 1% after June 13, 2024.

SPIR 2024 guidance; my own estimate

For Q2, I assumed a $25 million payment at the start of the quarter. Subject to a $500,000 penalty baked into the interest expense line item, the expense would decline to $4.1 million. Assuming the warrants get exercised by the end of June, another $25 million payment could be made at the start of Q3. Q3’s interest expense would decline to $2.9 million, including the $250,000 1% early termination fee.

Since Q3 is expected to be FCF positive according to management, the $1.7 million savings in interest expense could be used to further pay off debt in Q4, reducing the loan outstanding by another $2 million. The end result being a savings of $4.1 million in interest expense and a paydown of the loan of $52 million throughout the year.

Going back to full year projections, the company expects a non-GAAP operating performance between a $5.5 million loss and a $2.5 million gain. This leads to a non-GAAP EPS ranging between -$0.24 and +$0.11 based on 22.5 million weighted average shares outstanding for the year. Saving $4.1 million in interest expense would lead to an improved operating performance range between a $1.4 million loss and $6.6 million gain. With the financing, warrant exercise and any potential stock compensation, assume 25 million weighted average shares outstanding for the year. This would lead to a non-GAAP EPS ranging between -$0.06 and +$0.26.

Should the company plan to use the bulk of the cash raised from the financing for debt repayment, the 19% dilution on the stock has the potential to practically eliminate the risk of an operating loss for the year while more than doubling the upside EPS. The Blue Torch loan outstanding would be $66 million instead of $118 million by the end of the year. The $2 million per quarter delta in interest expense between Q1 and Q4 2024 would lead to an $8 million increase in FCF for 2025 compared to the base case scenario, further enabling SPIR to pay more of the debt quicker. The company would be in a position to refinance the remainder at a much lower rate and on more favorable terms as the balance sheet and likely its credit rating will have been greatly improved.

There is a possibility that SPIR raised the cash with no intent to pay down the debt. However, just by how the timing of the expiry date on the warrants aligns with the 1% reduction in the termination fee, it really appears to me that this raise was primarily for the purpose of paying down the debt. The investor likely invested the amount they did with this in mind. Knowing that their cash injection will help improve the balance sheet and therefore increase the value of their investment through a reduction in insolvency risk.

Conclusion: SPIR is a strong buy at $12.00

Unlike my colleagues on Seeking Alpha who put a hold rating on the stock, at $12 and after the financing announcement, I feel this is a good level for a strong buy rating. First, the financing deal at $14 indicates that the investor laying down the $30 million at that price is bullish. Even when assigning a value of $1.40 for the $14.50 warrants expiring at the start of July (estimated based on extrapolation of price data for $14 and $15 call options on SPIR for May and August), that would still leave a net cost of $12.60 solely for the shares for the investor. And presumably they didn’t buy in just to break even.

Second, despite having the potential to dilute the shares by 19%, if the company uses the bulk of the net proceeds to pay down debt, it actually has a significant anti-dilutive impact on 2024 EPS numbers. On March 7th, the day following the release of the financials and guidance, it rose 9% from $12.50 to $13.62. Clearly the market liked the guidance and this raise sets the company up to easily beat the top end of the non-GAAP EPS estimate.

Third, the act of paying down the debt, which is essentially toxic debt given to nanocap stocks in desperate shape, would vastly improve SPIR’s balance sheet risk. The perception of the company would improve, making it palatable to a wider range of institutional investors.

The main negative impact of the dilution will be that revenue per share and price to sales metrics will take a hit. Considering the midpoint guidance of $143 million in revenue for 2024, the revenue multiple with 26.4 million shares outstanding at a $15 stock price is just 2.8x. Not exactly a stretched figure for a company that has been growing in excess of 30% per year in an industry that is expected to see heavy growth for the foreseeable future.

In the longer term, one could argue that the company forever diluted itself by 19% when it may not have had to. But if this dilution enables it to get to larger FCF figures faster, that means it can always enact a share buyback to offset it. Let’s not pretend that 19% is a horrible level of dilution for a stock with a market cap less than $500 million. Companies of this size and especially in speculative and prospective sectors like AI, data and space satellites tend to dilute at far higher rates than this as they are running deeply negative operations. It appears that those days are behind SPIR. With the capital raise, the timeline to prosperity has been accelerated.

I bought shares and call options in SPIR last week.

Q2 2024 Earnings Call Transcript")