Ultima_Gaina

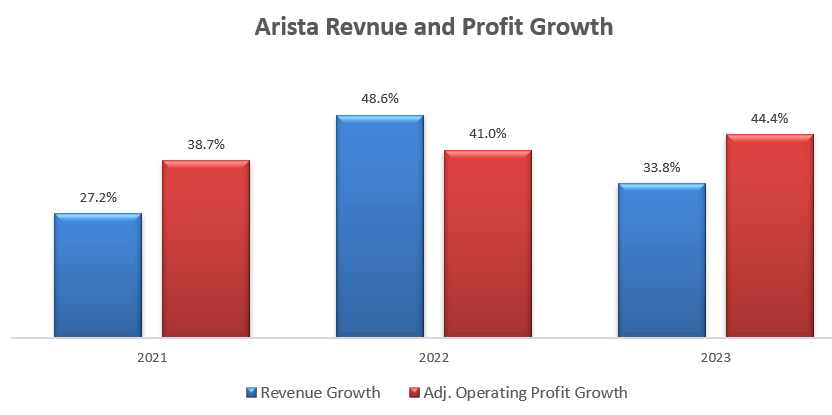

When I initiated my bullish view on Arista Networks (NYSE:ANET) in January 2015, their stock price was only $16.32. Since I published the second piece in June 2023, their stock price has surged by another 94.8%. The company has been gradually appreciated by investors, as evidenced by their rising stock price. They completed the year with 33.8% revenue growth and 51% net income growth in FY23. I remain optimistic about their long-term growth potential in the data center ethernet switch market. I upgrade to ‘Strong Buy’ rating with a one-year target price of $380 per share.

Explosive Growth Driven by Cloud Computing and AI

Arista has been experiencing explosive growth over the past few years, primarily driven by cloud computing and AI workloads, as depicted in the chart below. As emphasized in my previous article, Arista has been gaining tremendous market share from legacy switch vendors such as Cisco (CSCO).

Arista 10Ks

I attribute their outstanding growth to the following reasons:

Arista offers scalable and affordable hardware to hyperscale data centers with unique Extensible Operating System (EOS). Legacy players like Cisco and Juniper Networks (JNPR) offers proprietary hardware at considerably high prices. In contrast, Arista provides a very flexible solutions for these data center operators. Specifically, customers can choose to combine Arista’s EOS system with cheap white box hardware for less mission-critical networks. In mission-critical applications, customers can opt for integrated switching solutions, including Arista’s EOS and proprietary hardware. As data centers require massive cloud computing power, enterprises and hyperscalers prefer choosing affordable solutions for their ethernet switching technologies, in my view. Consequently, I believe Arista’s switching products and EOS are the perfect solutions for enterprise and hyperscalers.

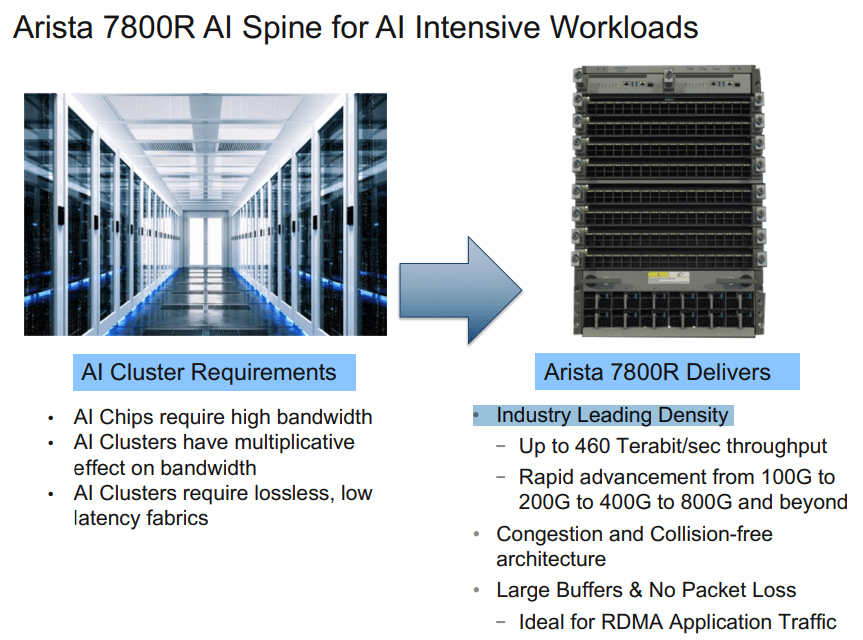

Arista specializes in the high performance data switching market. Their 7000 family of switches is ideally suited for low latency, two-tier, leaf and spine HPC network designs, as described in the white paper. Arista has developed 7800R AI spine and the 7600 Leaf to address the increasing demands on AI networking. Arista 7800R delivers industry leading density, which can up to 460 terabytes/sec throughput. As illustrated in the slide below, the Arista 7800R can meet the high bandwidth requirement for AI clusters. These newly renovated products are designed for high performance computing, and the growth is rising along with the rapid growth of AI computing, in my view.

Arista Investor Presentation

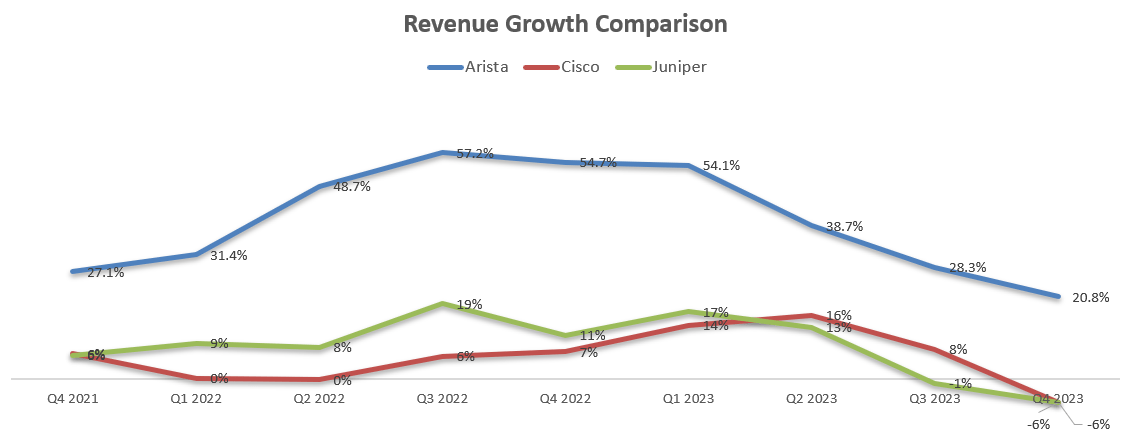

As depicted in the chart below, Arista has been experiencing much stronger revenue growth compared to Cisco and Juniper. It appears to me that Arista is the rising star in the new era of cloud computing and AI networking.

Arista, Cisco, Juniper Quarterly Results

Recent Financial Result and FY24 Outlook

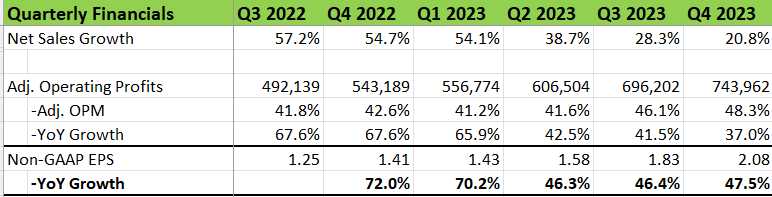

Arista released their Q4 FY23 result on February 12th 2024, with 20.8% revenue growth and 37% adjusted operating profit growth, maintaining their strong growth momentum. In addition, they achieved a record free cash flow of $2 billion, with the majority of cash being reinvested in their own business and only $112 million used for shares repurchase.

Arista Quarterly Results

My biggest takeaway from the earnings call is that they increased their 400 gig customer base from 600 in FY22 to 800 in FY23, and their management expected to achieve at least $750 million in AI networking revenue by FY25. Arista is expecting trials for 800 gigabytes switching in FY24, with the real production set for FY25. According to Telecom Review, 800-gigabit ethernet switches will experience rapid customer adoption and are projected to surpass 20 million ports in annual shipments within four years, primarily driven by AI networking. I am encouraged to see Arista has been making progress in their 800 gig switching product.

For Q1 FY24, Arista guides approximately 14% revenue growth and an 80bps margin expansion, as detailed below.

Arista Q4 FY23 earnings

For FY24, there are several factors need to be considered:

Mordor Intelligence forecasts that the data center network market will grow a CAGR of 17.85% from 2024 and 2029, driven by cloud computing, VR and AI related workloads. The overall market growth enables Arista to grow their ethernet switch business at a high pace, even without assuming any market share gains.

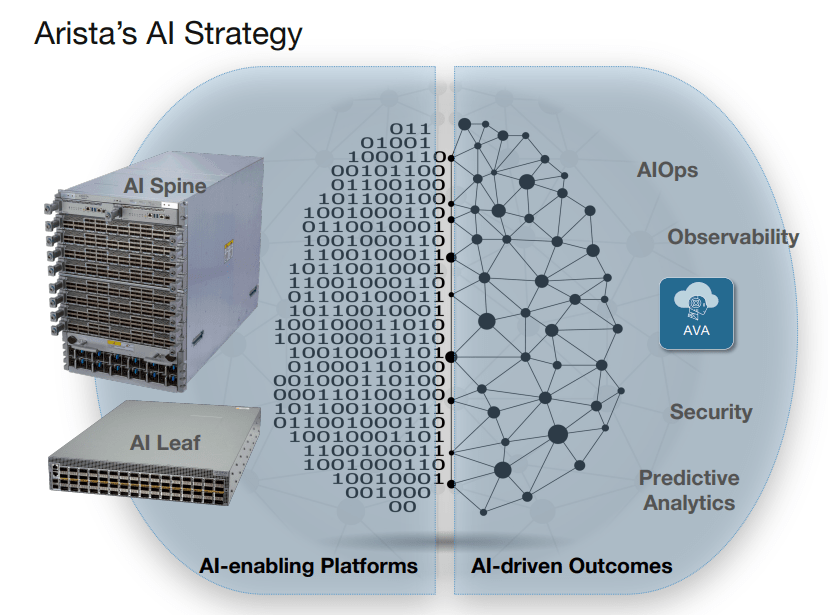

As discussed earlier, Arista’s products are well positioned for AI spine and leaf edge, as illustrated in the slide below. In addition to the switching platform, Arista has been expanding their other services including AIOps, observabilities, security and data analytics. In March 2024, Arista announced their new network observability software, offering workload and infrastructure monitoring across data center, campus, and wide area networks. There are some existing players in the observability market such as Datadog (DDOG) and Dynatrace (DT); however, the observability market is a relatively new market, and I anticipate all players will enjoy market expansion growth over the next few years.

Arista Investor Presentation

Lastly, Arista has experienced strong growth in their campus networking market over the past few years, with the campus and routing adjacencies contributing around 19% of total revenue at present. As indicated over the earnings call, Arista has been investing in cognitive wired and wireless, zero-trust networks, and network identity features to better meet the requirements of campus networking.

Taking into account all these factors, I assume Arista will continue their high-growth momentum, delivering 22% organic revenue growth, reflecting 25% revenue growth in data center market and 10% revenue growth in campus and other adjacencies.

Valuation Revision

As discussed, I assume Arista will deliver 22% organic revenue growth over the next few years, after which the growth rate will begin to moderate to 15% year-over-year growth. It worth nothing that the assumptions are quite conservative compared to their historical growth rate, and essentially the underlying assumption is that Arista just needs to grow in line with the market growth rate, maintaining their current market share.

As Arista’s core asset is their EOS operating system software, the company enjoys a relatively high operating margin compared to other hardware companies. Arista delivered 44.4% of adjusted operating margin in FY23, a significant improvement from 37.7% in FY20. The margin expansion is primarily due to their high topline growth and operating leverage. In the model, I forecast their sales and marketing, and G&A expenses will continue to benefit from operating leverage. Based on their historical average, I estimate the sales and marketing as a percentage of total revenue will decrease by 20bps year-over-year, and G&A as a percentage of revenue will reduce by 10bps. Consequently, I expect Arista will deliver a 30bps annual margin expansion in the model.

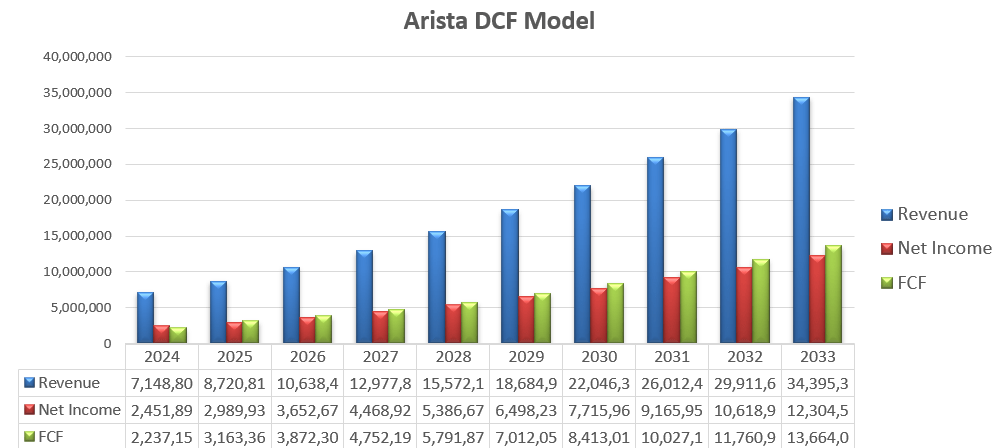

Arista DCF – Author’s Calculation

The model is using 2-stage of FCFE to estimate the 12-month target price. The detailed calculation of free cash flow to equity can be found in the table below:

Arista DCF – Author’s Calculation

The cost of equity is calculated to be 12.9% for Arista, assuming:

-Risk free rate: 4.32%. U.S. 10-year treasury yield

-Beta: 1.23. SA’s 24m Beta

-Equity market risk premium: 7%

Discounting all the FCFE at the discount rate of 12.9%, I arrive at their one-year target price of $380 per share.

Key Risks

For Arista, the potential competition is not coming from legacy players like Cisco and Juniper, as the legacy players are lagging behind in terms of technology in the new cloud computing and AI era. I am more concerned about Nvidia (NVDA) and Broadcom (AVGO) in the AI networking market.

In 2023, Nvidia launched their Spectrum-4, an ASIC 51.2 Tb/s ethernet switch. The product is designed for AI computing by connecting multiple GPU servers together. Nvidia claimed that their Spectrum-X networking can accelerate AI network by 1.6x over traditional ethernet.

In addition, in 2023, Broadcom unveiled their AI switch product: Jericho3-AI ASIC. The product can deliver high-performance switching at port speed up to 800Gbps, and scale up to connect more than 32,000 GPUs.

The 400G and 800G market are still in the infant stage, and Arista has been investing in their 400G and 800G products for several years, as indicated previously. Arista’s investors need to monitor Nvidia and Broadcom’s AI switching business growth and ongoing R&D roadmap.

Conclusion

Arista’s broad ethernet switch products are across 10,25,100,200,400 and future 800 gigabytes, enabling enterprises to deploy AI Spine and AI Leaf computing at a scalable and affordable expense. I believe Arista will continue to gain market share from legacy players like Cisco and Juniper in the data center space. I upgrade to ‘Strong Buy’ rating with a one-year target price of $380 per share.

Q2 2024 Earnings Call Transcript")