Michael Vi

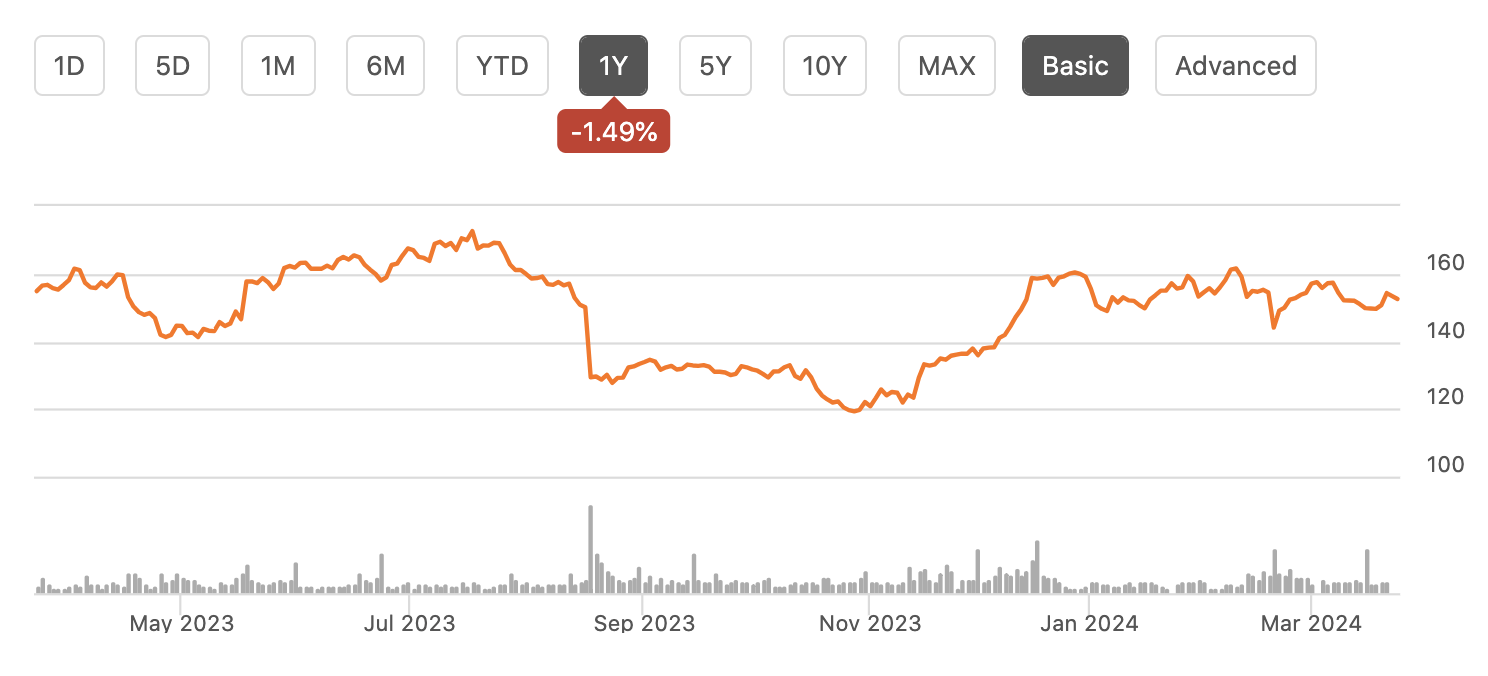

Shares of Keysight Technologies (NYSE:KEYS) have been a poor performer over the past year, trading essentially flat and missing out on a significant rally across the technology sector. The company has struggled with weak orders from wireless carriers and softness in China. Having worked down its backlog, it now faces revenue declines. Since recommending investors sell shares in November given the company’s disappointing performance, KEYS stock has rallied by 11%, which has lagged the S&P 500’s 15% return during that time. With the growth picture increasingly cloudy, investors who have stayed in the stock should use the rally to sell, as I expect it to continue to underperform broad indices.

Seeking Alpha

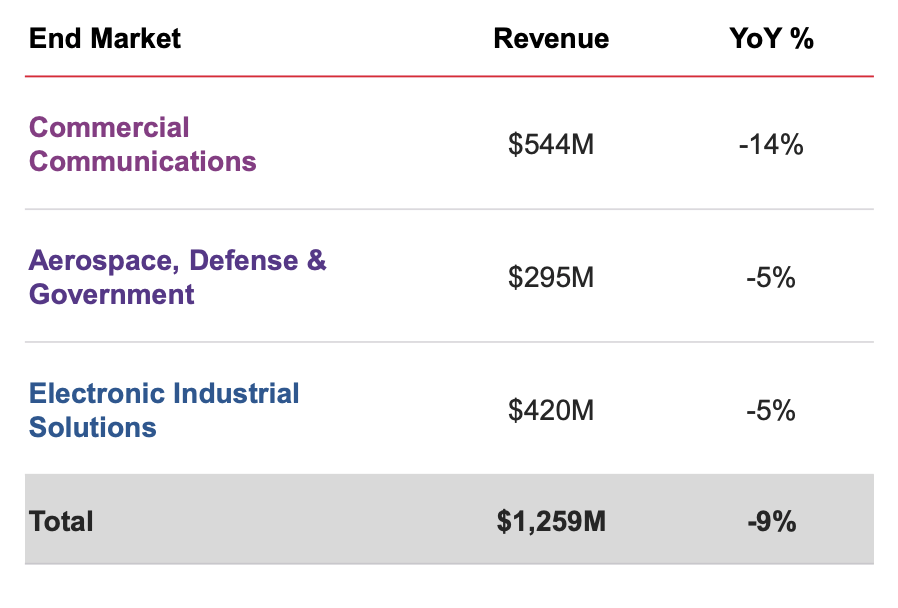

In the company’s fiscal first quarter, Keysight earned $1.63 in adjusted EPS, which beat consensus by $0.04, as revenue declined by 9% to $1.26 billion. KEYS primarily services three end markets: communications, government, aerospace & defense, and industry, like automotives and semiconductors. While these various product lines are experiencing declines of different magnitudes, Keysight is seeing declines across all units, which is leading to falling revenue.

Keysight

Just as KEYS is seeing weakness across products, the company is seeing challenges across geography. Keysight is a fairly global business with the Americas driving 41% of sales; Asia Pacific 39%, and Europe 20%. In the Americas, revenue fell by 8% while Asia was down by 13%. Management has specifically called out the fact that China continues to be weak and “challenging.” Even with recent underperformance here, China is a mid-teens share of revenue.

While China is a clear point of concern, I was also concerned by the performance in Europe. Headline revenue fell by 1%, due to weakness in communications. However, the company has also completed an acquisition of European-based ESI, which will provide $140 million of recurring revenue. Ex-M&A and currency, Europe was down by 21%, a dramatic drop. With much of the global telecom sector facing fierce competition, elevated debt loads, and high dividend payments, cap-ex spending is somewhat constrained, which has reduced demand for KEYS technology, particularly with much of the 5G roll-out having occurred.

The Communication Solutions Group (CSG) is 67% of revenue and posted a 12% decline to $839 million as operating margins compressed by 170tp to 27.0%. The commercial communications environment is cautious, despite growth in AI-related products. Aerospace, defense, and government was down from last year, though orders rose, given increased space and satellite activity.

Its other, smaller unit, Electronic Industrial Solutions (EISG), was down by 5% from a year ago. Delays in fab projects are reducing semiconductor demand. Keysight products are used to help semiconductors quality check and manage production. With expansion projects taking longer to launch, this pushes out revenue. Most notably, Intel has delayed its Ohio factory’s completion date as it has taken more time for CHIPs Act funding to be allocated. Similarly, while electric vehicle solutions spending is rising—there is less spending on products related to actual production. While EVs continue to gain penetration, take-up has been a little slower with Ford having pushed out some EV sales goals, for instance. These developments create a more challenging environment for Keysight.

This decline in activity is also beginning to pressure profit margins even as KEYS has benefitted from easing supply chains and input costs to increase gross margins by 200bp to 67%. Its cost of products fell by about 10.5%, outpacing the decline in revenue. Favorable mix shift has also helped gross margins with core software sales flat from last year while lower-margin hardware declines.

Despite higher gross margins, the company’s core operating margin fell by 230bp to 27%, as the firm has lost operating leverage at a lower sales pace. Most notably, R&D spending rose 2% to $232 million and is now 18.4% of revenue from 16.4% last year. With technology rapidly changing, it is imperative to spend adequately on R&D to maintain competitive positioning, meaning some of this spending is really not discretionary.

Indeed, the company plans to maintain R&D spending around current levels, even in the face of weaker revenue, which is pressuring margins. Now in Q1, SG&A also rose by $24 million to $362 million. However, there were $28 million of restructuring and acquisition costs, as the company seeks to streamline operations with the aim of reducing SG&A spending in the low-to mid-single digits. This may still lead to higher SG&A as a share of revenue, but these declines should help to limit margin compression.

One modest positive is that Keysight is one of the few nonfinancial companies that enjoys positive net interest income, running about $4 million a quarter. The company carries $1.75 billion of cash against $1.2 billion of long-term debt. Because cash interest rates are higher today than the fixed yields KEYS issued debt at, its interest revenue actually exceeds its expenses. Its balance sheet is a significant source of strength that provides ample capacity to manage downturns even far more severe than the company is experiencing. Indeed, it still bought back $93 million of stock in Q1.

The current environment has been difficult, and unfortunately, I do not see signs of acceleration. Orders declined to $1.22 billion from $1.3 billion last year. This resulted in a book-to-bill ratio of about 0.97x. Core orders fell by 12% from a year ago. With orders running below revenue, that points to weak future demand, which makes sequential revenue growth more difficult. Keysight has a $2.3 billion backlog, which provides about 6 months of revenue. However, I would note that historically just 2% of orders were “long-term,” but that figure is now about 8%. In other words, it will take longer for KEYS to convert backlog to revenue, creating the risk of further revenue slippage.

In perhaps another sign of soft demand, inventory rose about $40 million sequentially to $1.02 billion. With inventories higher even as sales, its working capital position is less efficient, and it takes Keysight longer to move product. This does create a risk that recent gross margin gains are reversed. This inventory rise is not substantial to be a major risk, but rather, it is a minor headwind and adds to the evidence demand has undershot expectations.

Along these lines, management isn’t “assuming a strong revenue recovery” in the second half of the fiscal year. Activity is expected to decelerate further this quarter with revenue expected to be $1.19-$1.21 billion, leading to $1.34-$1.40 in EPS. Management expects revenue to be flat sequentially in Q3 and up mid-single-digits in Q4, which would just get KEYS back to Q1 levels. More optimistically, it expects some increase in orders, creating the potential for revenue growth in 2025, though off such a low base, revenue may not return to peak levels before 2026.

In the first half, KEYS will earn about $3.00, and its guidance implies a similar run-rate in revenues in H2 vs H1. Considering there is a 3-6 month lag between orders and revenue, the ~$1.2 billion in orders is consistent with Q2 guidance and a similar level of revenue in Q3. Given an economic recession appears unlikely, a further material drop should not be the base case. There is scope for modest growth in some segments like government, given the US is raising defense spending by 3%. This should support Keysight sales for satellite and space work. If Boeing (BA) is able to increase production, that would support its aerospace unit, though I hesitate to assume much improvement. All of this points to a second half that is similar to the first half on the revenue front.

Holding margins flat, this would lead to about $3 in EPS in H2 2024. At a 5% reduction in SG&A, earnings could push towards $3.20 as margins improve. As such, I am looking for $6-$6.20 in full year earnings. This puts the $6.15 consensus toward the higher end of my 2024 earnings forecast, creating some downside risk.

I also view earnings as likelier to come in toward $6 than $6.20, as a 5% SG&A cut may prove larger than the company can generate, and R&D spending stays elevated. Additionally, with inventories rising, some gross margin momentum may be lost. Its China business also remains weak, and given the geopolitical dynamics, there may be an effort to diversify away from US technology companies, reducing demand for Keysight products more structurally. While KEYS exposure to China has fallen, a mid-teens share of revenue is still significant; ongoing weakness here just makes it more difficult to grow the company. Analysts are forecasting a 21% growth rate in 2025, which seems optimistic with Q4 revenue unlikely to be much better than Q1 and orders activity that shows little momentum.

Shares are trading 25x 2024 earnings, and over 20x 2025 earnings. This is a lofty multiple for a company seeing negative revenue growth and facing a constrained demand environment that does not appear to be abating. By contrast, the entire S&P 500 is at 20.9x forward earnings and about 18.6x 2025 earnings with consensus of 11% growth in 2024 and 13% in 2025. KEYS is trading at a significant premium to the market even as it has a slower growth profile. While its balance sheet provides Keysight with durability, the ability to grow into these premium multiples is unclear, and the market appears to already be pricing in a recovery, which may not materialize as quickly as hoped.

As such, with shares having rallied (though less than the market), investors have an opportunity to exit shares at an attractive level in my view. Given its strong balance sheet and the fact earnings should bottom this year, I believe a multiple of up to 20x can be justified, or about $125. That creates nearly 20% downside, which may be realized if market lose confidence in such a strong 2025 recovery. I would sell shares before future earnings report shows the weak momentum in the business persists.

Q2 2024 Earnings Call Transcript")