gorodenkoff

Investment Thesis

Cadence Design Systems (NASDAQ:CDNS) is part of the EDA market (Electronic Design and Automation) which I believe is running quite hot at the moment. The foundation of my belief is that since AI proliferated, especially over the past 12–15 months, enterprises have doubled down on their spending and investments in key strategic priorities, which puts them in a position to become secular beneficiaries of the AI wave. And Cadence benefits from these strategic spending shifts as more enterprises ramp up usage of Cadence’s computer-aided design products and solutions to design & develop highly complex electronic systems.

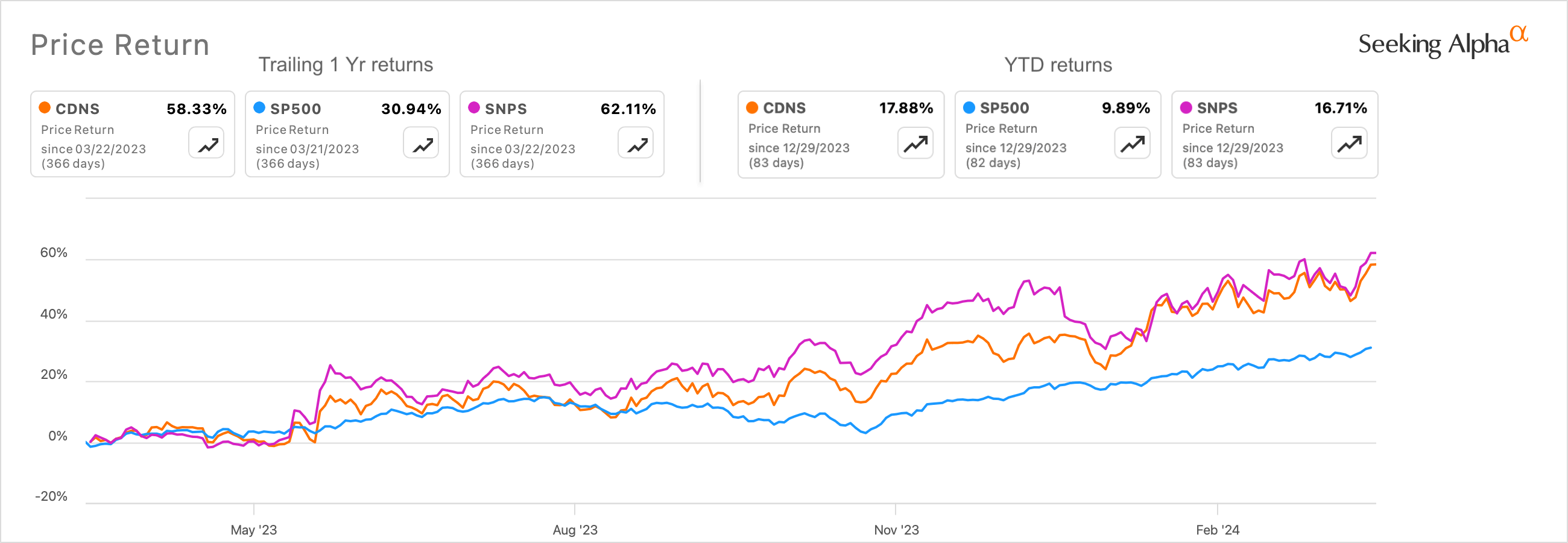

Cadence Design, along with its direct competitor, Synopsys, are actively engaged in growing their market share and expanding their portfolios by making acquisitions in the last few months, heating this up in the EDA market. Both stocks have also performed well on a trailing 1-year and YTD basis.

Cadence Design Systems performance on the markets vs its peer, Synopsys and the S&P 500 Index (SA)

While there is no doubt that there are some strong long-term secular forces that will continue to lift Cadence over an extended period of time, I believe a pullback is needed in this stock as expectations get ahead.

An impressive growth story so far aided by secular catalysts

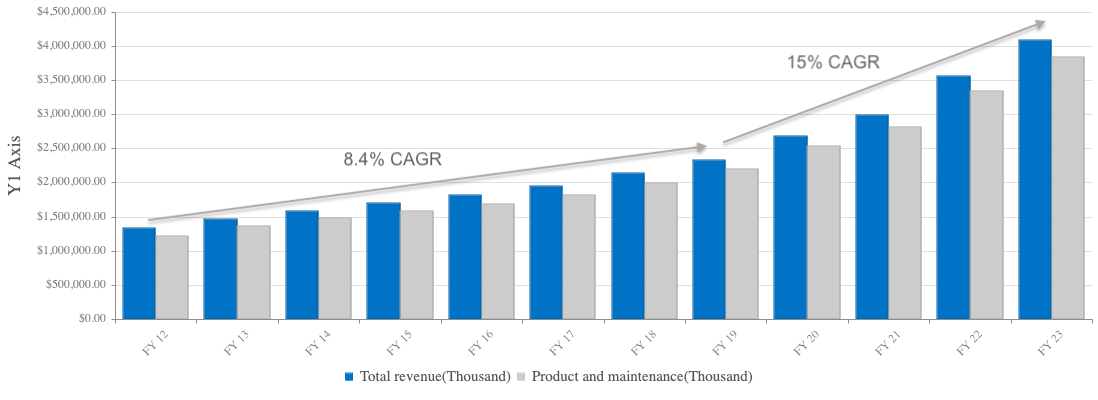

Per its full-year FY23 earnings report published last month, Cadence’s annualized revenue grew 15% in FY23 to $4.09 billion, at the high end of their guidance of $4.06–$4.1 billion issued in Q3 FY23. The business continued to see a boom in their semiconductor IP and AI-driven systems analysis. I have added a chart below where I have split the growth rates of the company into two phases. Pre-pandemic compounded growth rates for the company were ~8%, but those compounded growth rates almost doubled to ~15% post-pandemic, and management continues to expect similar growth rates, based on commentary on the recent earnings call.

Cadence Design’s revenue growth rates have almost doubled after the pandemic (Company sources)

Cadence has ramped up its partnership with foundries and chip companies throughout the year, which allows Cadence to provide design software and lead IP. Since the AI boom, I believe chip packaging has become extremely crucial in designing complex chips and SoCs (System-On-Chips) that help accelerate high-performance computing (HPC), AI, and mobile computing design spaces for Cadence’s own customers as well as Cadence’s partner’s customers. Partnerships with Intel (INTC), Arm (ARM), and NVIDIA (NVDA). In fact, Nvidia highlighted its partnership with Cadence and peer Synopsys while explaining how the company’s design software can be used in conjunction with Nvidia’s chips for efficient system design.

In addition, the company also highlighted another growth area of their business, System Design and Analysis (SD&A), which “continued its strong momentum, delivering 18% year-over-year growth in Q4 and 22% growth for the year.” I believe the company’s SD&A business will continue to be a core part of its Intelligent Systems Design growth strategy as it benefits from demand for a seamless platform solution across design, packaging, simulation, and analysis.

How Cadence lines up to competition

The EDA market is largely oligopolistic, and Cadence competes for market share with its two direct peers, Synopsys and Siemens EDA. The market also has several other smaller players, such as Keysight Technologies (KEYS), Schrödinger (SDGR), CEVA (CEVA), and Altium Limited (OTCPK:ALMFF). However, most of Cadence’s smaller competitors compete for a far smaller market share via a combination of services and solutions that include providing technical/computational software or electronics design, consulting companies, etc. That makes Synopsys a key competitor, really, with Synopsys and Cadence running head-head in this horse race for dominance in the EDA and SD&A markets which can also be noted in a Trendforce report market research report.

According to the Trendforce report on the EDA market, Cadence is the second-largest player in this market, accounting for 30% of the market share. This is followed by Siemens EDA further out, at 13% market share. But Cadence’s larger direct peer, Synopsys, holds a 32% market share.

In fact, the market is so hot at the moment that Cadence and Synopsys have been very busy in the M&A space. Most recently, Synopsys moved to acquire another large rival, ANSYS (ANSS), two months ago, following Cadence’s acquisition of system design engineering firm Invecas. Cadence also followed this up with another acquisition earlier this month with BETA CAE. To date, Cadence has reportedly made over 60 acquisitions, while Synopsys has made almost 90 acquisitions.

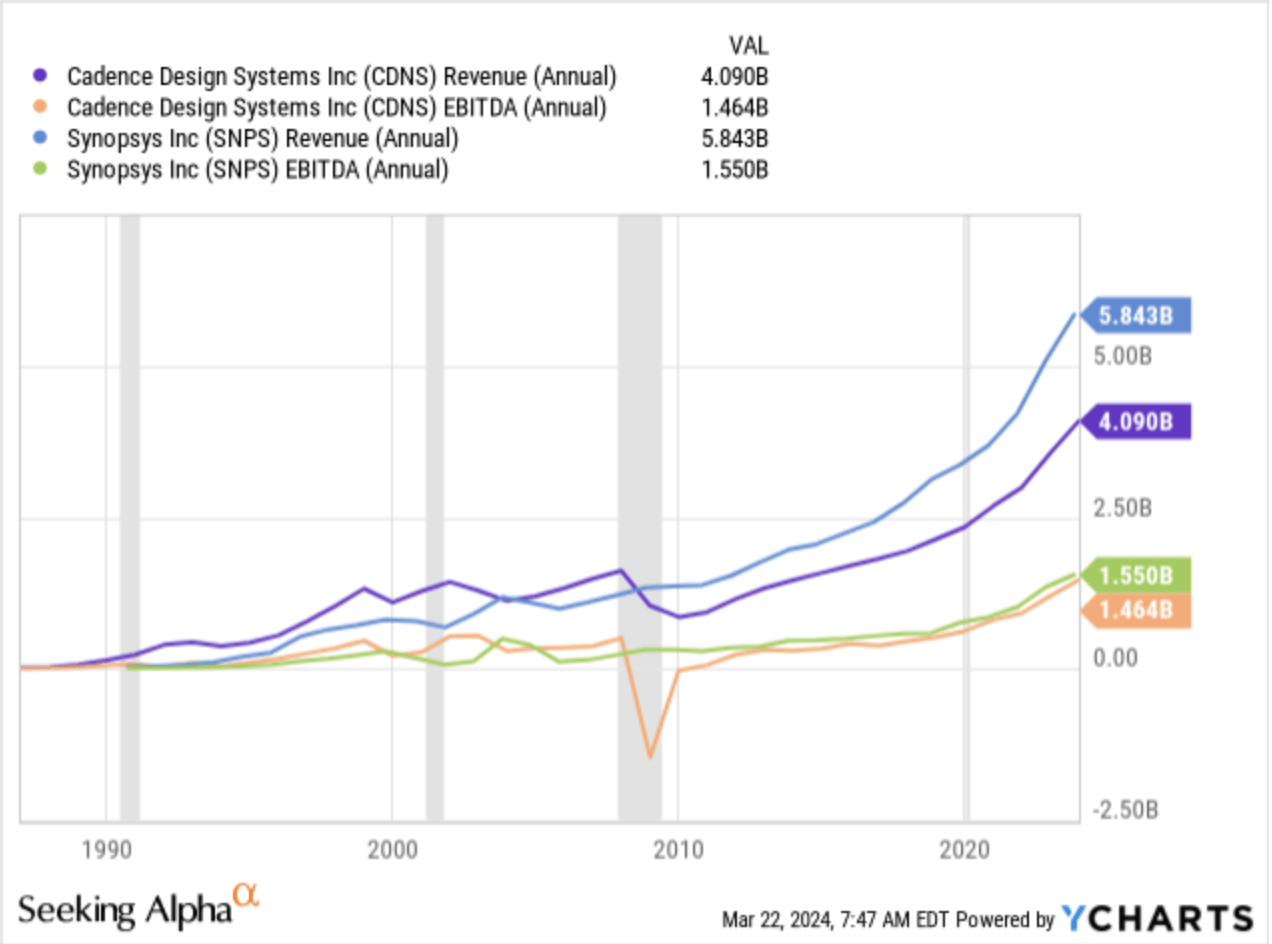

How Cadence’s Revenue and EBITDA compares to Synopsys (YCharts)

From the chart I have added above, on the revenue front, Synopsys is the larger company by revenue but Cadence appears to be the faster growing company of the two, per my analysis. Per Trendforce’s report, while the EDA market is projected to grow at a CAGR of 13.8% between 2020 and 2024, Cadence grew 14.4% on a compounded basis, faster than the CAGR of Synopsys at 13.4% over the same period.

Cadence’s Valuation and Outlook

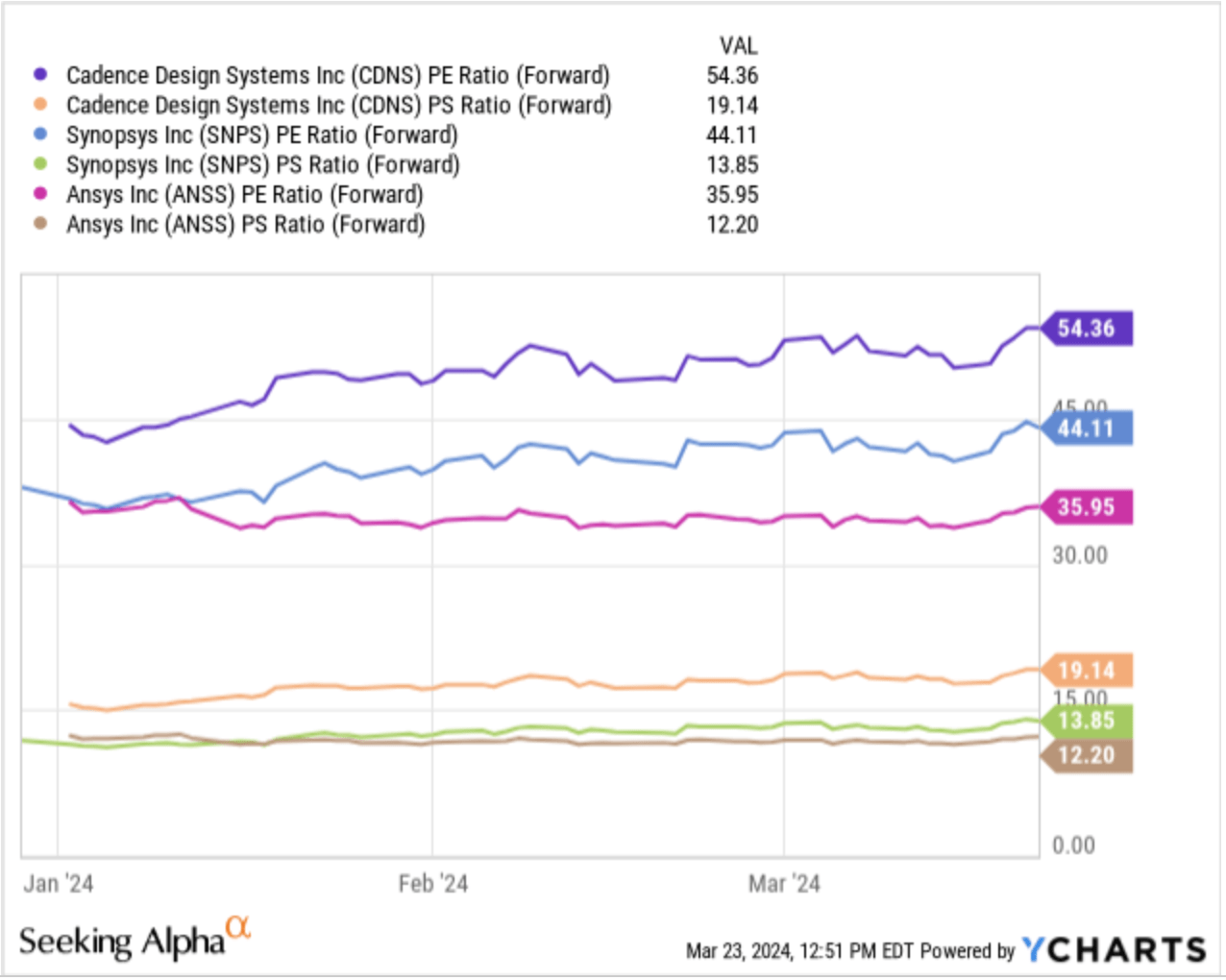

Based on the observations I made at the end of the previous section, it appears that Cadence’s relative premium to invest in the stock is now justified as compared to Synopsys on a trailing basis. Cadence trades at ~21.5 times trailing sales as compared to Synopsys, which trades at 15.3 times trailing sales. At this time, it makes sense to compare and contrast Cadence with its direct larger peer Synopsys which together account for over 60% market share per the Trendforce report. I have added ANSYS below, although ANSYS has now been acquired by Synopsys.

Cadence is richly valued on a relative basis versus its peer, Synopsys (YCharts)

But, consensus estimates project both companies to grow sales at relatively the same growth rates of ~13% between FY23 and FY26, while EPS for Synopsys is estimated to be growing faster at ~21.7% CAGR as compared to Cadence’s compounded EPS growth of 18% over the same period.

Still, as per the chart above, Cadence is trading at a relative premium of 54 times forward earnings compared to Synopsys’s 44 times forward earnings. I do not see why Cadence should trade at a higher premium when its forward-looking top- and bottom-line growth rates are expected to be lower than its peers.

Risks and other factors to look for

I mentioned earlier that competition is a threat to Cadence. So far, Cadence’s target market appears to demonstrate perfect signs of an oligopolistic market, with Synopsys being the only other major threat.

A higher dollar also affects the growth in revenue for Cadence. Volatility in the dollar, as represented by the dollar index (DXY), can present distortions in Cadence’s revenue collected. This is important per my observation of Cadence’s historical trends of international revenue, which always exceeds at least 50% of its overall revenue, and they continue to expect revenue from international operations, which account for a significant portion of the company’s overall revenue.

Takeaway

As discussed, there are some secular forces that will certainly drive Cadence forward. However, the relative premiums that Cadence is currently trading at are not warranted, in my opinion. Longer-term investors would have nothing to do here, but others looking to initiate positions or cost-average into Cadence’s stock would benefit from sitting on the sidelines, as I expect a pullback given the higher relative premiums and the massive runup in the stock so far. I rate Cadence as a Hold for now.

Q2 2024 Earnings Call Transcript")