JHVEPhoto

Upstart Holdings (NASDAQ:UPST) wants to disrupt the lending market through its AI platform, but so far the monetization of its customer and partners’ base is not great, raising questions about the sustainability of its business model.

Company Overview

Upstart is a fintech company, combining technological capabilities applied to the financial sector, namely it offers a cloud-based artificial intelligence (AI) lending platform. It was founded in 2021 and has been listed since 2020 on the NASDAQ stock exchange and its market value is about $2.3 billion.

Its core business is the development and offering of its lending platform, which uses machine learning to, theoretically, offer a better credit underwriting experience to banks and credit unions. Its goal is to reduce the risk and cost of lending for banking partners, by using its AI models and applications, to better analyze credit risk and offer mostly a digital experience.

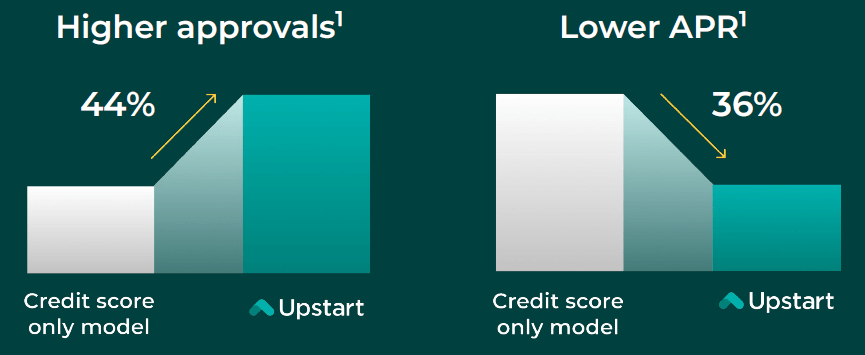

Upstart’s AI models have been trained for more than 10 years, powered nowadays by more than 1,600 variables, while the ‘traditional’ approach in the banking system is to use the FICO score and a limited number of variables to analyze credit risk.

This means Upstart’s models take into account much more variables and a long history of credit prepayments to analyze risk, which theoretically should lead to better underwriting compared to the traditional way. Moreover, as its models integrated more date they should perform better, thus Upstart’s capability of analyzing big data and improving its AI models is expected to be a competitive advantage over the long term.

AI Model (Upstart)

This is something that is not easy to replicate by other technology companies or its customers, which have much less data to analyze, thus by using Upstart’s platform banks and credit unions should have a better credit risk assessment than by doing on its own.

At the end of 2023, it had more than 100 banks and credit unions using its platform, which include personal loans, automotive retail and refinance loans, home equity lines of credit, and small dollar loans.

On the consumer’s side, it has some 2.9 million customers, who benefit from its platform by obtaining lower interest rates, higher approval rates, and a digital lending process. In 2023, about 87% of its loans were fully automated with borrowers having automatic approvals and no documentation to upload. The platform is also interesting for banking and credit unions partners because it enables them to get new customers, have lower fraud and loss rates, plus lower costs to originate loans.

Regarding the funding sources, loans originated through Upstart platform can be retained by the lending partners, purchased by institutional investors, or retained in the company’s balance sheet. In 2023, some 48% of loans were purchased by institutional investors, 32% were retained by its lending partners, 16% were held by Upstart, and 4% were used for a securitization transaction.

Regarding its customer diversification, Upstart is heavily exposed to its top three partners, which together accounted for some 80% of loans originated through its platform during the last year and represented about 62% of Upstart’s revenue. This means Upstart is too much concentrated in a small number of partners, which is not positive over the long term, because if one of these important partners decides to leave the platform, it can have a significant impact on Upstart’s revenues and earnings.

Going forward, Upstart’s growth prospects come from several factors, including the expansion of its partners in its platform, the addition of new products, and potentially the internationalization of its business. In the near term, its growth should come mainly from higher engagement with its current partners, and the expansion to other type of loans, like it has done recently with home equity loans. If the company starts to incorporate small business loans and mortgage loans, I think it can increase significantly loan origination in its platform and reach a broader customer diversification and overall business size over the next few years.

Financial Overview

Regarding its financial performance, its track record has a listed company is mixed given that it reported strong growth during 2020-21 and it was already profitable despite being still in an early-growth phase, but this has changed considerably over the past couple of years as the operating landscape turned much more challenging for start-up companies, due to more tightening funding conditions.

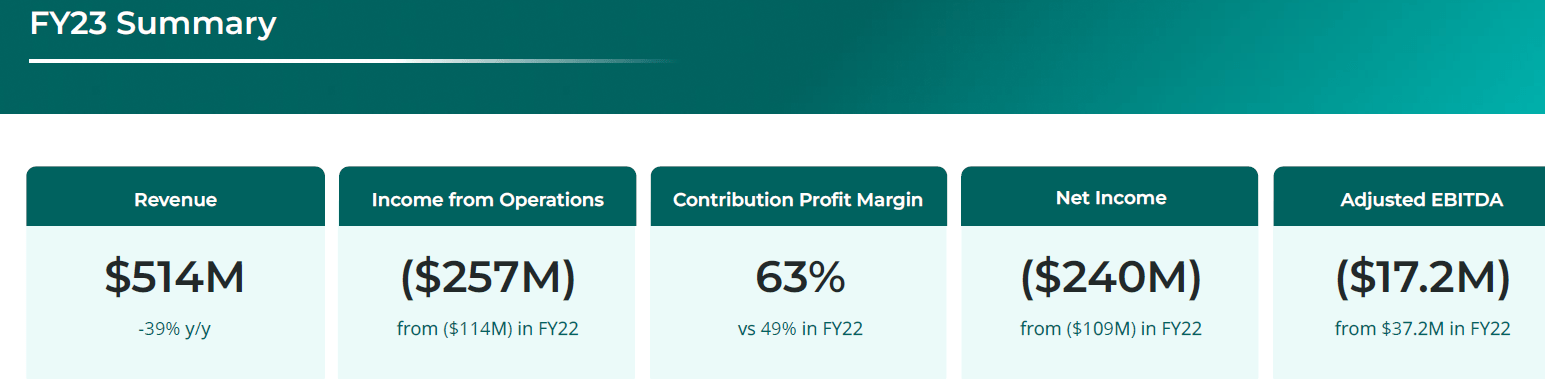

Indeed, in 2023, its revenues amounted to $514 million, a decrease of 39% YoY, and the company reported operating losses, given that both its adjusted EBITDA and net income were negative last year.

2023 KPIs (Upstart)

This negative operating performance is justified by a more challenging macroeconomic environment over the past couple of years, with higher interest rates making also loans less accessible for customers, while on the lending side tighter funding conditions from institutional investors and bank partners led to several lenders and credit investors to stop or reduce their investments in Upstart’s originated loans.

Due to this more challenging backdrop, Upstart’s loan originations declined considerably in 2023, both by number of loans and volumes, as shown in the next table.

Volumes (Upstart)

This shows that despite Upstart’s business model being more focused on technology and not directly providing loans, its business is still very exposed to economic and funding cycles, being directly affected by credit conditions in the marketplace.

Nevertheless, its strategy is to continue to operate as a capital-light operation, retaining loans on a discretionary basis and not evolving its business model into a specialized finance company. I think this makes sense over the long term, but until Upstart reaches a larger size and diversifies further its banking and credit union partners, and also geographically, its business will continue to be cyclical.

Ultimately, I think its business can evolve into a similar profile in the financial industry that Uber Technologies (UBER) or Airbnb (ABNB) have successfully built in other sectors, of providing technology services and not owning the ‘underlying’ asset, but so far Upstart has not been able to leverage its AI platform into this type of business model.

This means that Upstart is likely to retain loans in its balance sheet for some time, which exposes it to potential credit losses ahead, making its business being a mix of fees more related to volumes and credit risk.

Over the long term, I would like also to see more revenue coming from a subscription type of business, in which banking partners would pay a fee for being in Upstart’s platform, which would provide the company with a more recurring revenue stream and be less exposed to loan volumes.

Regarding its outlook, Upstart provided guidance for Q1 2024 that was below expectations, expecting to generate some $125 million in revenue and report a net loss of about $75 million, which means its operating momentum is not expected to improve much in the short term. Furthermore, this backdrop is likely to remain difficult until the Federal Reserve starts to cut interest rates, which can happen in the second half of this year, and potentially ease credit conditions and lead to a rebound on Upstart’s operating momentum.

This seems to be somewhat expected by the street considering that current consensus is for the company to report revenues of $575 million in 2024 and a net loss of about $224 million, which is a small improvement from the previous year. In the following years, it’s expected to have higher revenues and smaller losses, but I think investors should take these estimates with caution as Upstart business is quite cyclical and medium-term estimates can be wrong by a significant margin.

Regarding its valuation, given that Upstart is reporting operating losses and is not expected to report a positive bottom-line over the next few years, the best measure to use is the EV-to-sales multiple, which is currently at more than 5x forward revenue, which is not particularly a bargain for a company that is reporting losses and its growth ahead is not expected to be fantastic.

Conclusion

Upstart has an interesting business proposition through its AI lending platform, which can be a disruptor of the credit space over the long run. However, its expansion in recent years has been modest, both from a partners perspective and product diversification. This makes me wary that is business is scalable and sustainable over the long-term. I think Upstart is still quite risk, and see SoFi Technologies (SOFI), which I’ve covered recently here, as a better long-term investment in the fintech sector.

Q2 2024 Earnings Call Transcript")