robas

Overview

Lundin Mining (OTCPK:LUNMF) (TSX:LUN:CA) is Canadian base metals mining company, with a relatively diversified set of operations. The producing mines are in Chile, Brazil, USA, Portugal, and Sweden, there is also the Josemaria development project in Argentina. The stock is listed in Canada & Sweden, and the reporting currency is U.S. Dollars.

Figure 1 – Source: Company Website

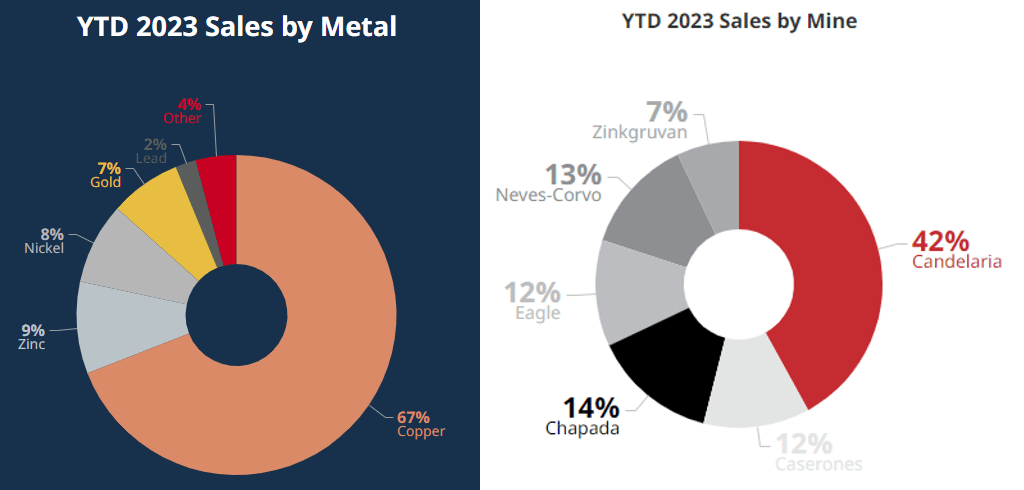

The company gets most of its revenues from copper production, but also produces more material amounts of zinc, nickel, and gold, together with minor amounts of other metals. Broken down by mine, 54% of 2023 revenues came from Chile and an additional 14% from Brazil. So, the company has almost 70% of revenues coming from South America and an even higher percentage of copper revenues.

Figure 2 – Source: Company Website

Financials

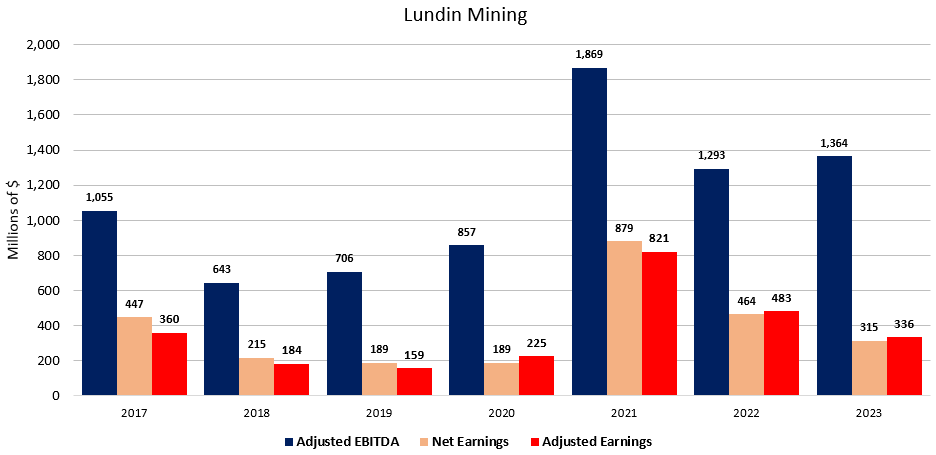

Lundin Mining is an impressive mining company which has generated consistent earnings over the years. 2021 was a particularly good year due to the elevated commodity prices, but we can in the figures below see that the company has generated reasonably good earnings even during years with less accommodative commodity prices. Adjusted EBITDA was $1,364M in 2023 and adjusted earnings were $336M.

Figure 3 – Source: Lundin Mining Quarterly Reports

The company pays a quarterly dividend, where the dividend yield is 2.7% using the latest share price. The dividend amounts to about $200M in capital distributions to shareholders in a year.

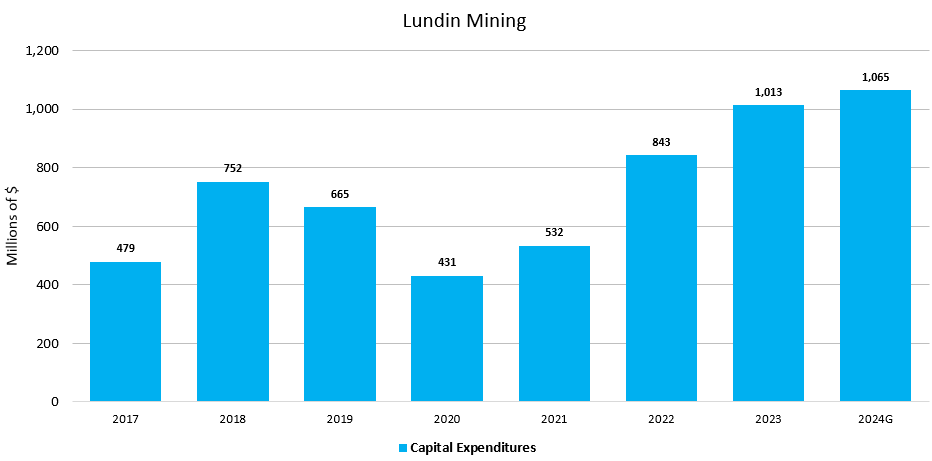

Figure 4 – Source: Lundin Mining Quarterly Reports

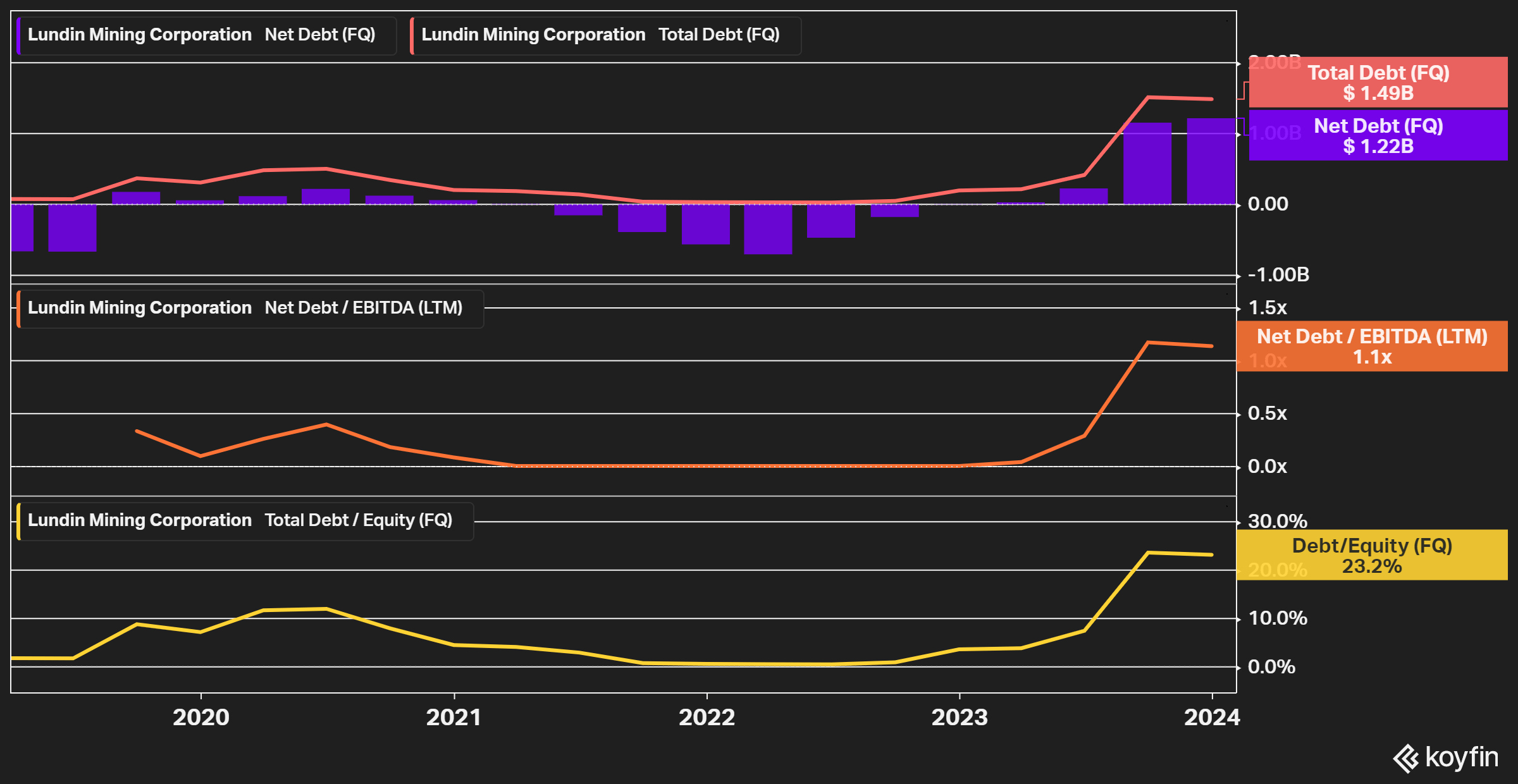

There have also been some substantial capital investments over the last couple of years and the capex guidance for 2024 is at $1,065M. The company has partly funded the capital investments from earnings, but we have also seen the financial leverage increase. The debt-to-equity ratio is now 0.23 and the net debt to last twelve months’ EBITDA is 1.1. These are far from extreme levels, but the higher financial leverage has made the company more exposed if we were to see a retracement in copper prices going forward.

Figure 5 – Source: Koyfin

With that said, there are no near-term liquidity concerns. In the end of 2023, the working capital was $581M and the company also has $1.5B left in its revolving credit facility.

Reserves

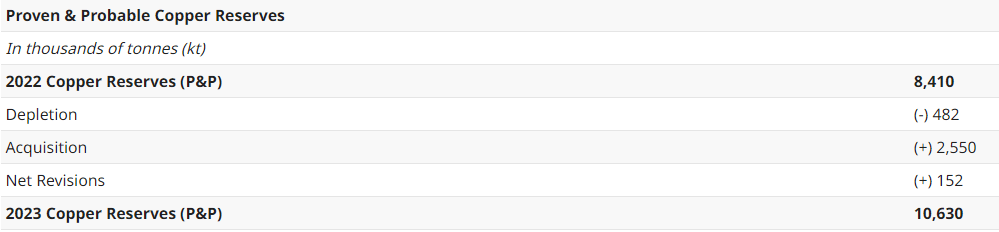

Early February, Lundin Mining provided a reserve update, where overall proven and probable copper reserves grew by 26% on a 100% basis. Most of that growth naturally came from the Caserones acquisition. Regardless, the average mine life is very good with these copper reserves, and I also think it is fair to assume some additional reserve growth from exploration over the coming years.

Figure 6 – Source: Company Press Release

Guidance & Valuation

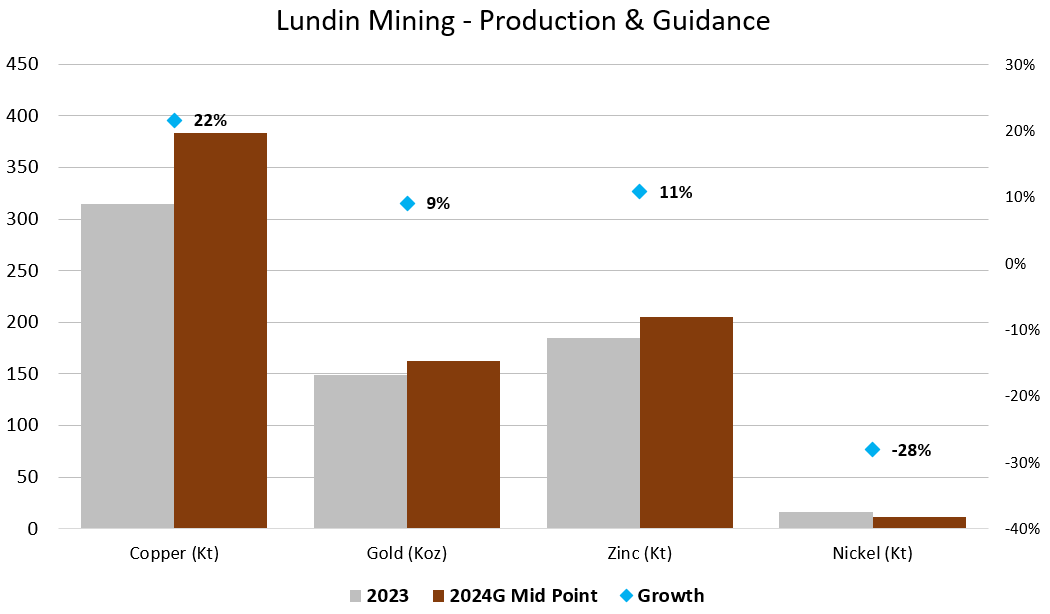

The production guidance for 2024 is very positive, where the production of copper, zinc, and gold production is expected to increase compared to 2023. The growth in copper production following the Caserones acquisition is particularly impressive. Nickel production is expected to decrease materially, but the overall impact to total revenues from this decline will be small. The cost guidance for 2024 is also very competitive.

From 2025 and onwards, production is expected to be more stable or possibly decline slightly, but that will also depend more on the timing of various near-term growth projects.

Figure 7 – Source: Data from Lundin Mining Presentation

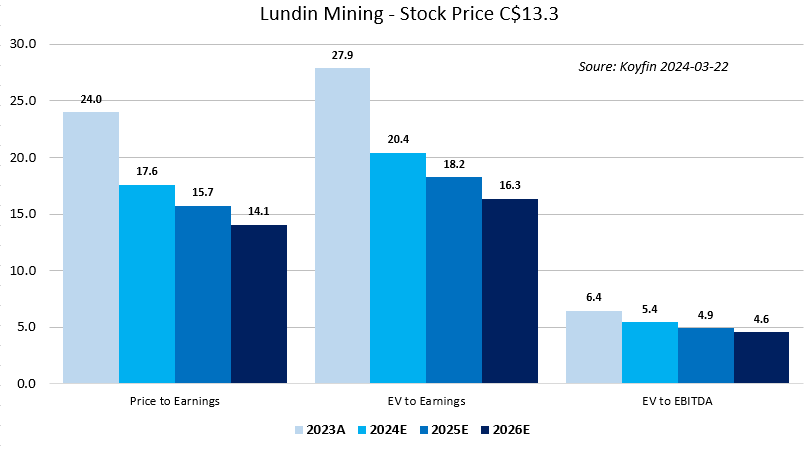

If we use the latest share price, net debt, and share count from Q4 2023, the company is trading with a market cap of $7.6B and an enterprise value of $8.8B. The estimates below are from Koyfin, where we haven’t seen that many upward revisions lately, despite a strong copper price. So, if the current copper price holds going forward, the estimates are likely slightly conservative.

Figure 8 – Source: Koyfin

Based on the latest estimates, we are looking at an EV to Earnings around 20 for 2024 and the multiple is expected to decline slightly over the coming years. That is not overly expensive, but far from dirt cheap.

Conclusion

While there is a lot to like about Lundin Mining, there are also some risks to consider. The increased financial leverage together with a larger capex budget for 2024 means the company is more dependent on higher copper prices than some of its peers or what the company has been in the past. So, the downside protection has decreased lately.

The exposure to Chile and Argentina is relatively high and it will increase more when the Josemaria project reaches production in a few years. There are no doubt synergies operating a few mines within proximity of each other, which can put downside pressure on operating costs. However, the concentrated exposure also means regional geopolitical risks could more substantially impact the company.

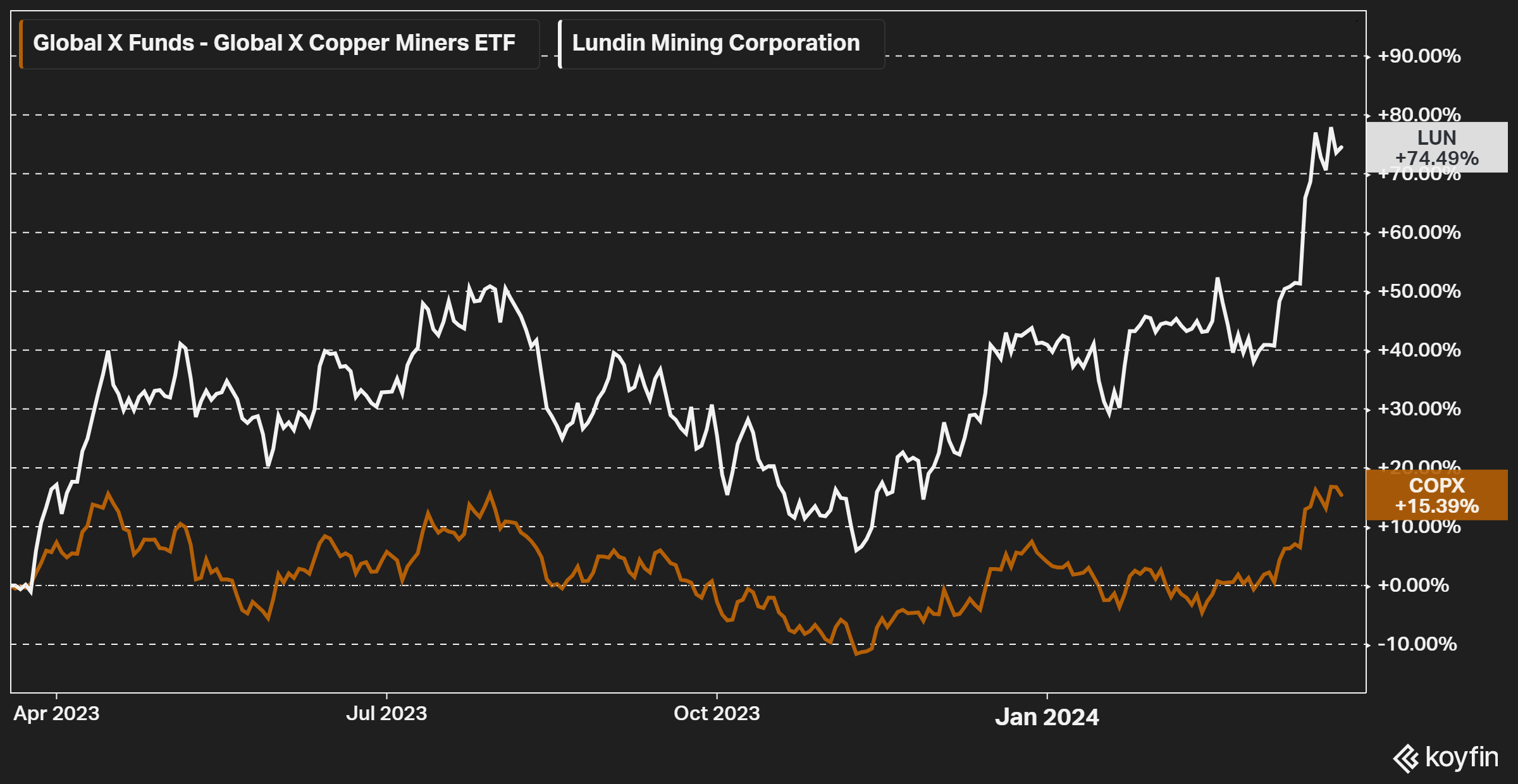

Figure 9 – Source: Koyfin

Overall, I think Lundin Mining is a quality copper mining company which has managed to grow its production profitably over the years. On the valuation side, I consider the company somewhat fairly valued after a strong stock price performance over the last year, so I am neutral on the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")