ansonsaw

Now’s a great time to be an income investor, especially considering that most of the market is now focused on chasing speculative growth. Adding to that is the practice of index investing, which perpetuates the high valuations of companies like Tesla (TSLA) and Nvidia (NVDA) due to their mega-market caps and outsized influence over the S&P 500 (SPY) compared to most other companies.

That’s why I prefer to tune out the noise and focus on growing my income streams from undervalued dividend-paying stocks with long track records of shareholder returns.

Such I find the case to be with NNN REIT (NYSE:NNN), which I last covered in December with a ‘Buy’ rating, highlighting its high occupancy and conservatively leveraged balance sheet. The stock been flat since then (0.35% rise in price and 1.7% total return including dividends) as market optimism around the pace of rate cuts have faded since December.

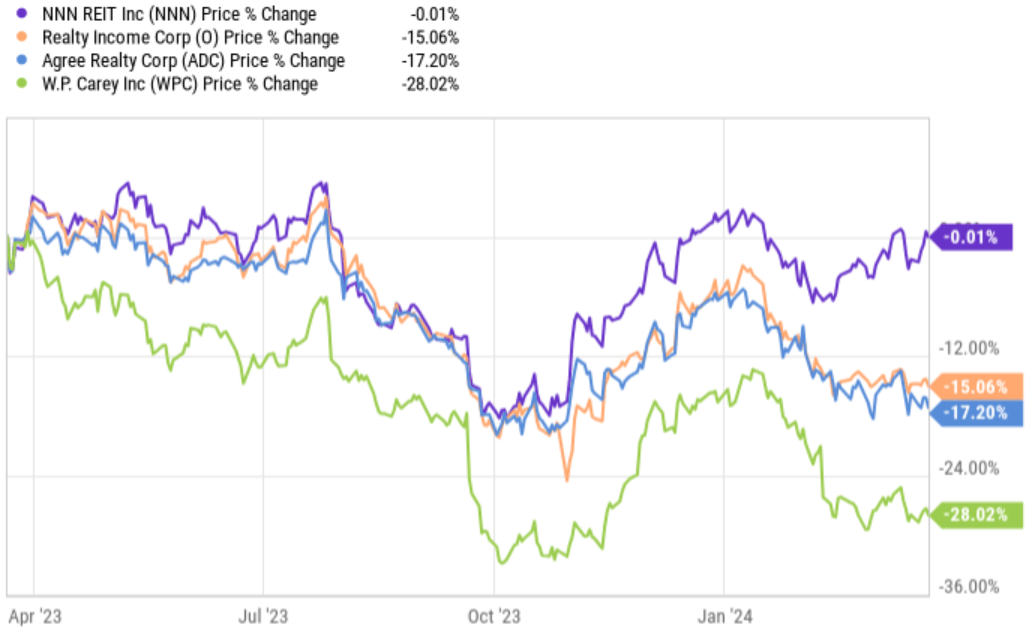

NNN’s performance over the past year has been better than that of peers Realty Income (O), Agree Realty (ADC), and W.P. Carey (WPC) due in part to NNN’s lower valuation than O and ADC to start with, and its avoidance of troubled property sectors like the Office segment, which has plagued peer WPC and resulted in a spin-off and dividend cut.

NNN vs. Peers 1-Yr Price Change (YCharts)

In this article, I revisit NNN and discuss why market uncertainty around the stock makes it a great time to buy this solid dividend-paying name, so let’s get started!

Why NNN?

NNN REIT is a net lease REIT that has a longer dividend growth track record than Realty Income Corp., with 34 years of consecutive annual dividend raises under its belt. At present, it has 3,532 properties spread across 49 U.S. states with long average remaining lease term of 10.1 years.

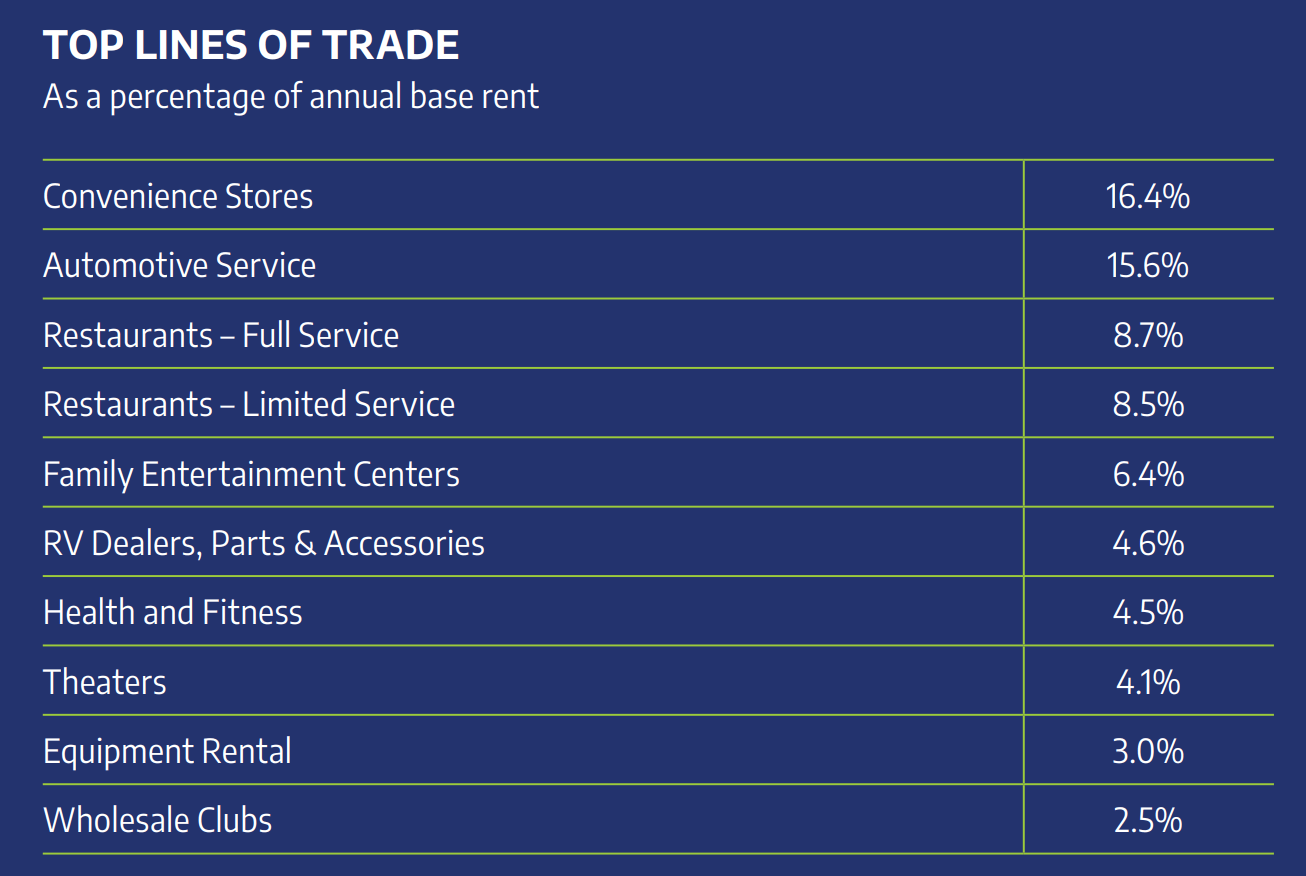

Its tenants are also diversified by over 30 different lines of trade across retail segments that are necessity-based and e-commerce resistant. This is reflected by the following breakout, which shows that Convenience Stores, Automotive Service, Restaurants, and Family Entertainment Centers make up 55.6% of NNN’s annual base rent.

Investor Presentation

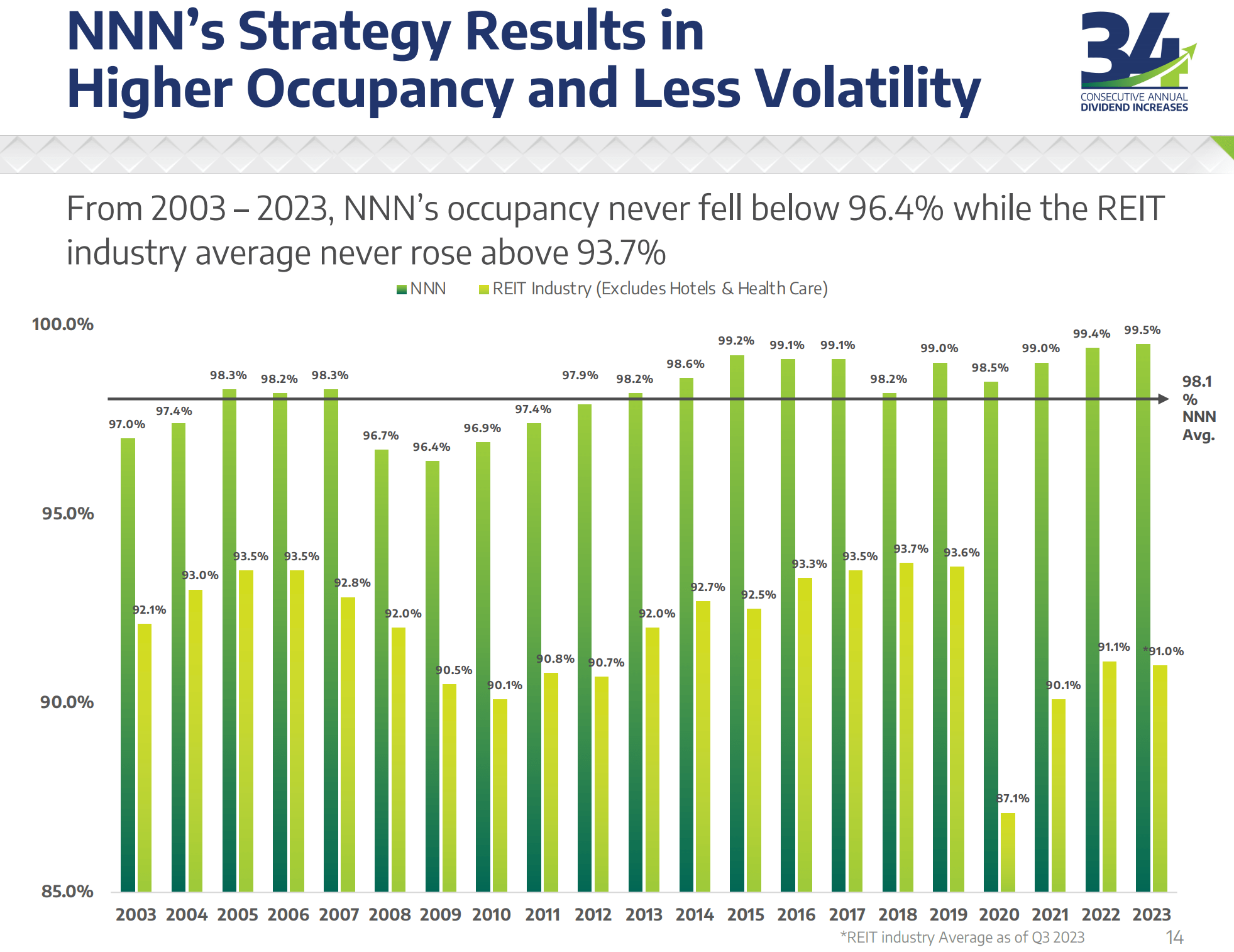

Despite what NNN’s share price performance over the past year may suggest, it continues justify why it remains a solid pick, with full year 2023 FFO per share growing by 4.5% YoY to $3.24. This was driven by healthy internal growth through annual rent escalators and high portfolio occupancy of 99.5%, which rose by 30 basis points on a sequential quarter-on-quarter basis and 10 bps on a YoY basis. As shown below, NNN’s occupancy has never fallen below 96.4% over the past 20 years, while the average across the REIT industry never rose above 93.7%.

Investor Presentation

NNN’s growth is also supported by robust acquisition volume with 165 properties acquired last year totaling $820 million at an initial cash cap rate of 7.3% and a weighted average remaining lease term of 18.8 years, sitting far longer than the 10.1 years portfolio average. This was funded primarily by the issuance of $500 million in 10-year unsecured notes at an attractive interest rate of 5.6%, implying a 170 basis point investment spread (compared to the aforementioned 7.3% cap rate). Additional funding came from $116 million worth of asset dispositions at a lower cap rate of 5.9% implying a 140 bps investment spread, and minimal dilutive equity issuance of just $31 million.

Looking ahead, NNN remains well-positioned from a balance sheet standpoint to source properties should opportunities arise. This includes having a safe net debt-to-EBITDA ratio of 5.5x, sitting under the 6.0x level generally considered to be safe by ratings agencies, and a BBB+ investment grade credit rating from S&P, which comes in handy in the current higher interest rate environment. This can help to ensure that NNN gets financing at favorable rates compared higher leveraged private market players.

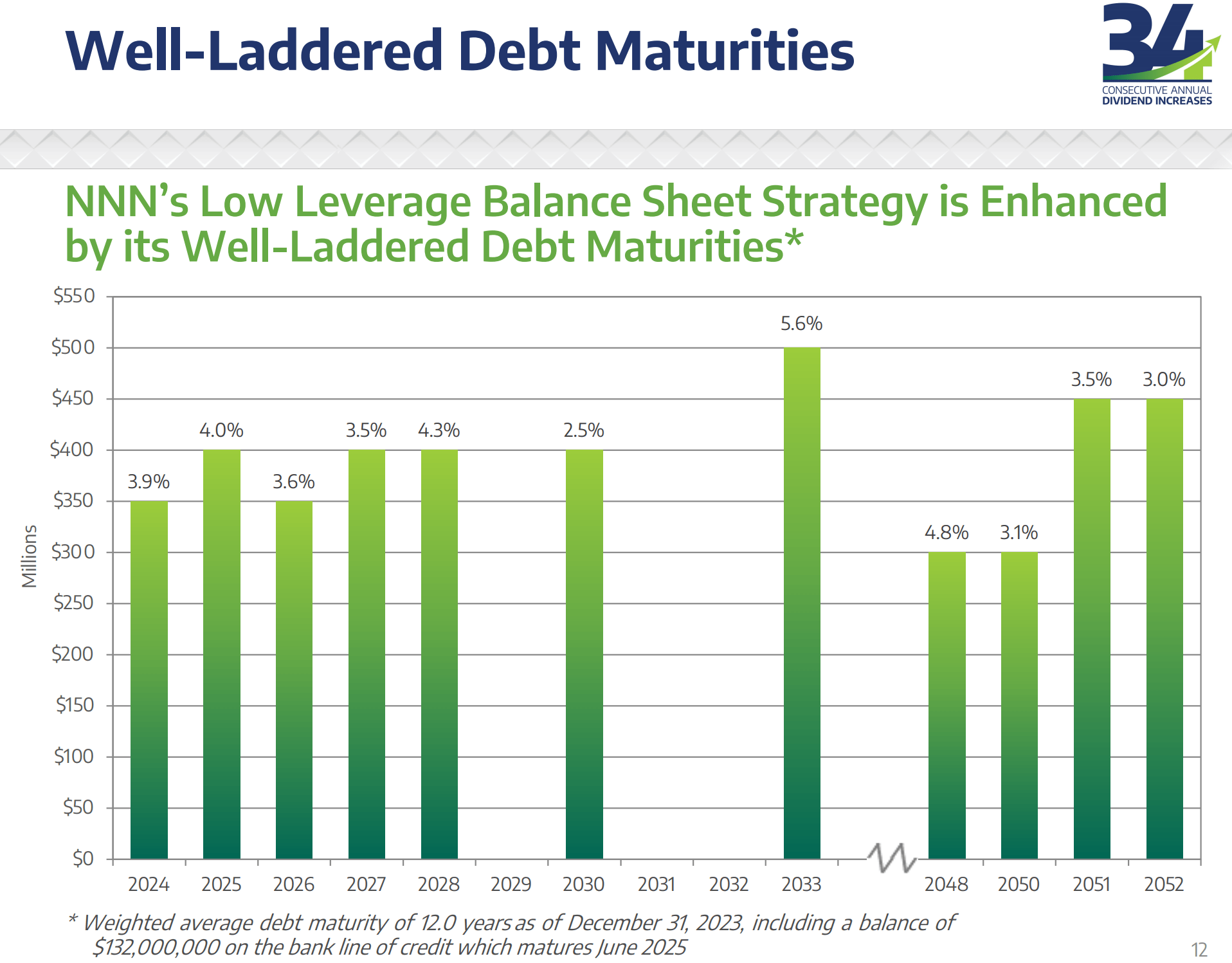

Moreover, NNN carries a strong fixed charge coverage ratio and has a safe unsecured debt-to-gross assets ratio of 42%, sitting under the 50% threshold that I generally consider to be safe for REITs. As shown below, NNN’s debt maturities are also well-laddered with no more than 4.3% of debt maturing between now and the end of this decade.

Investor Presentation

While interest rates may not come down as quickly as some had originally thought, an eventual decline in rates would be a boon for REITs like NNN that source properties at today’s elevated cap rates. That’s because rents aren’t likely to come down due to annual escalators while interest rates can change. The Federal Open Market Committee will meet 7 more times this year and the Fed has indicated that rates will most likely be cut in 2024 but is waiting for more positive signs from the economy as it relates to inflation.

Risks to NNN include potential for no interest rate cuts or even rate increases should inflation be hard to tame, as that would reset the timeline on when NNN could see accretion from a higher spread between cash yields on investments and lower interest rates from debt refinancing down the road. Other risks include potential for cap rate compression on new property acquisitions, should private market buyers become more accustomed to the new normal and come back to the bidding table after deleveraging their balance sheets.

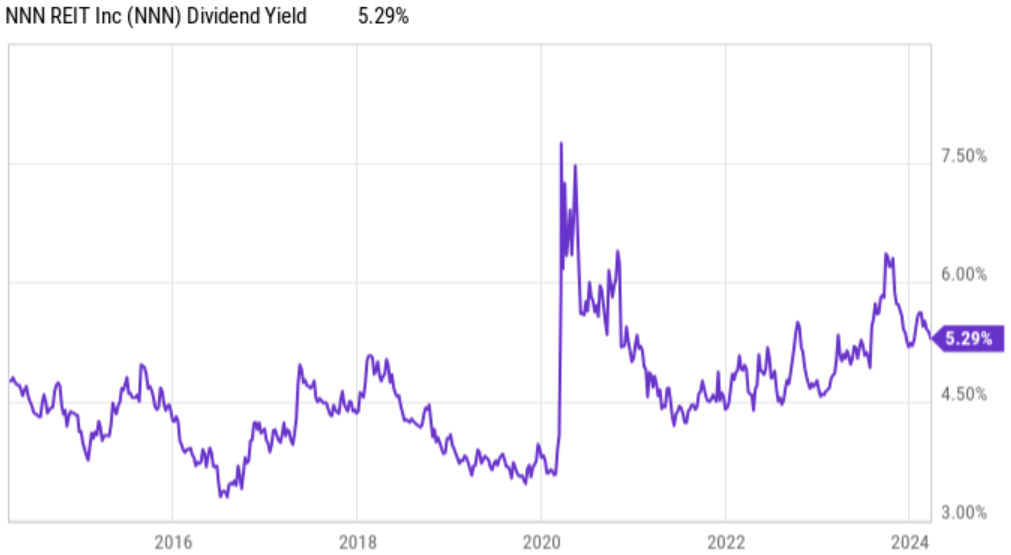

Importantly for income investors, NNN currently sports an appealing 5.5% dividend yield that’s well covered by a 69% payout ratio. It also grew its dividend by 2.7% last year despite interest rate uncertainty and I would expect to see another raise this summer, which would extend its current 34-year track record of consecutive annual raises. To put things into perspective NNN’s dividend yield remains on the high end of its 10-year range excluding outliers such as the early 2020 pandemic-timeframe and interest rate-driven panic sell-off in October of last year, as shown below.

YCharts

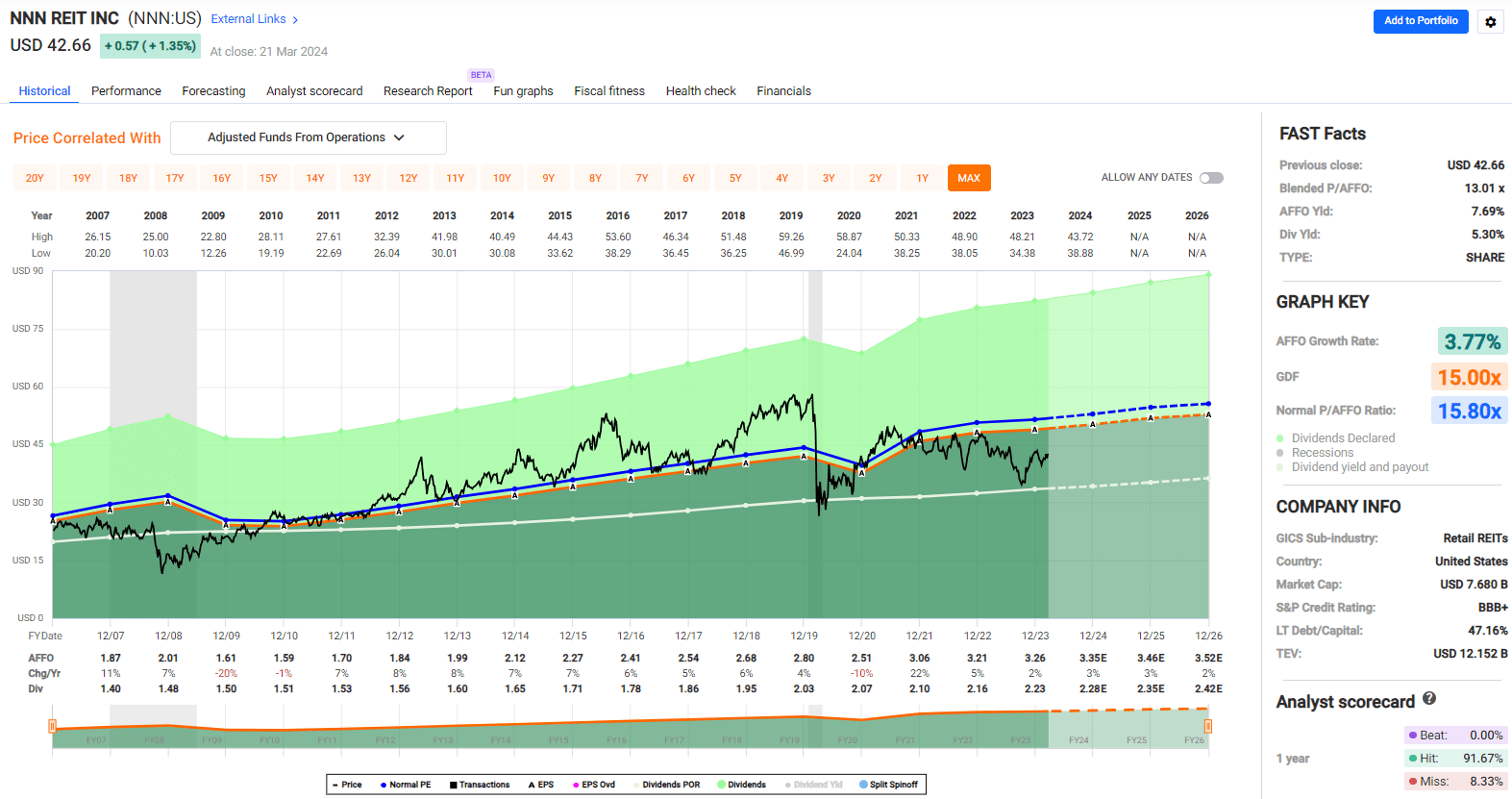

Lastly, I continue to see value in NNN at the current price of $42.43 as of writing, with forward P/FFO of 12.8, sitting well below its normal P/FFO of 15.8. While the market is baking in opportunity cost and risk from the current interest rate environment, I believe it’s also not appreciating the potential long-term benefits from the already realized inflation and properties sourced at high cap rates combined with potential for lower interest rates down the road.

FAST Graphs

Should NNN return to its long-term normal FFO/share growth rate of 5%, that combined with the current 5.3% yield could give investors market-beating returns even without accounting for a share price appreciation to its mean valuation.

Compared to peers, NNN currently trades at a premium to the 12.3x P/FFO of Realty Income and 11.9x of WPC, and at a discount to the 13.7x of Agree Realty. While I currently see Realty Income as being the better value at present, I consider NNN to be a solid alternative due to its similar-quality portfolio that’s purely U.S.-based. In the near to medium-term, I would target a P/FFO in the 14-16x range for NNN should the Fed hold up to its stated goal of 3 rate cuts this year, thereby providing more visibility and stability to interest rates.

Investor Takeaway

NNN is a well-positioned triple net lease REIT with a diversified portfolio of necessity-based retail properties and solid internal and external growth prospects. Its sound balance sheet, investment grade credit rating, and attractive dividend yield make it an appealing option for income investors looking for stability in their portfolio.

While risks do exist, the potential for long-term outperformance due to lower interest rates in the future makes NNN a compelling pick for investors seeking a mix of income and capital appreciation potential. Considering all the above, I maintain a ‘Buy’ rating on NNN with thesis unchanged since I last visited the stock.

Q2 2024 Earnings Call Transcript")