Pgiam/iStock via Getty Images

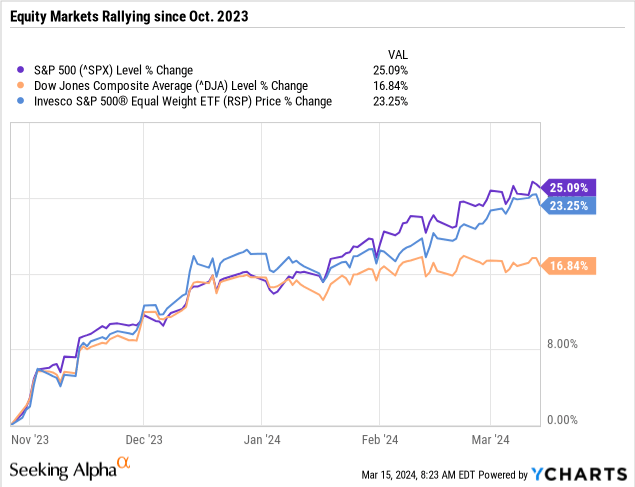

With a strong equity market and all-time highs for the S&P 500 and the Dow Jones Industrial Average, investors are clearly bullish, fueled by growth in the U.S. economy, the prospect for future earnings growth, developments in technology, and the expectation of Fed rate cuts.

However, the equity market rallies could be a double-edged sword, meaning the huge market gains are creating a wealth effect. As a result, the Fed has another reason for keeping rates higher for longer.

The Fed is trying to thread the needle with higher rates to lower inflation without hurting the U.S. economy.

Highlights from the March Fed Meeting

During its March meeting, the Fed changed some of its forecasts and outlook for 2024.

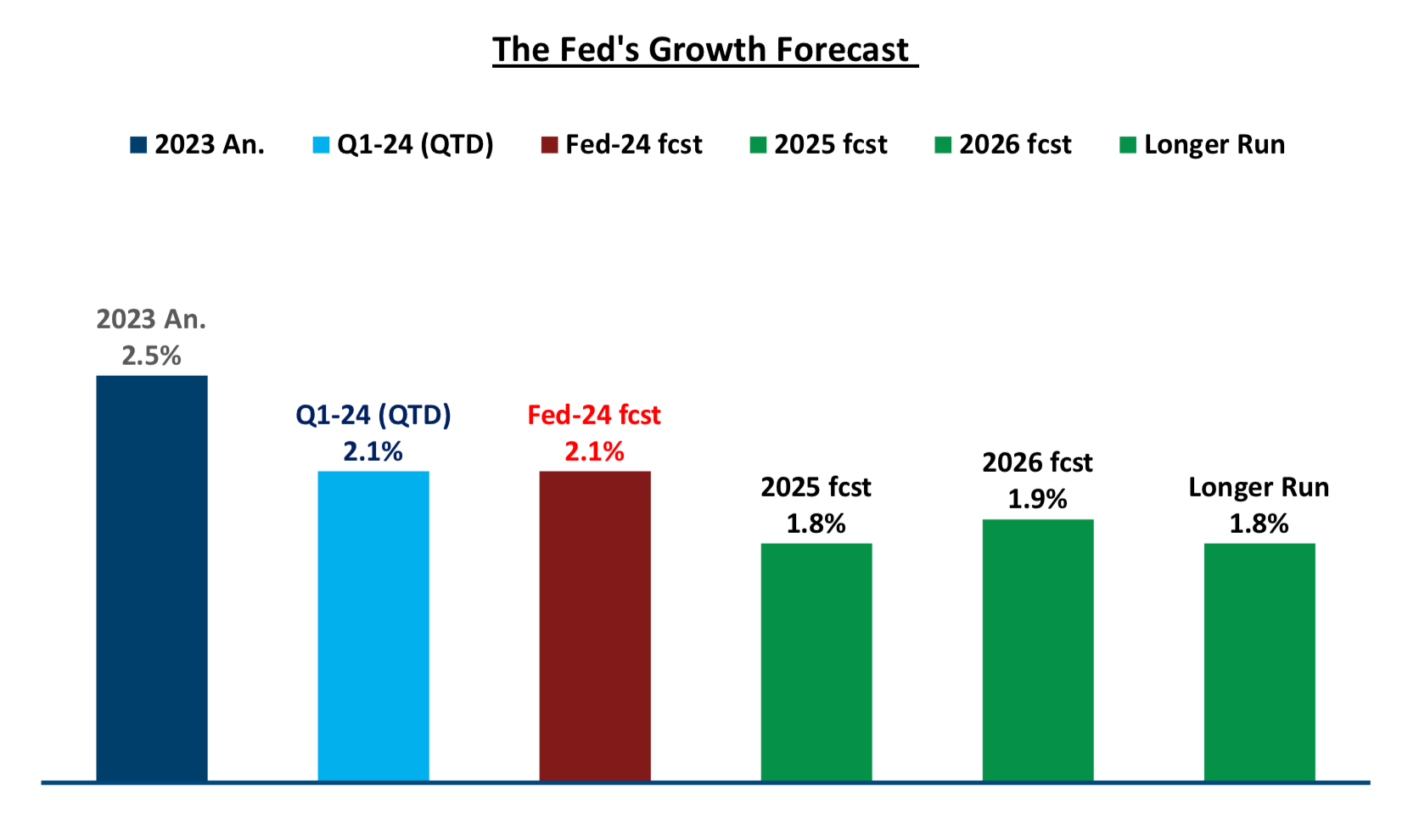

- The Fed increased its 2024 real GDP growth forecast from 1.4% to 2.1%.

- They lowered their unemployment rate forecast from 4.1% to 4.0% for this year.

The Fed left the number of rate cuts at three for 2024 and signaled that the economy is moving into better balance, which includes unemployment, inflation, and growth.

“The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance.” —from the Federal Reserve FOMC statement March 2024.

This is slightly different from the January meeting when they wanted to see the economy move into better balance.

The March meeting did little to change the Fed’s path to cutting interest rates—forecasted to be 75 basis points in 2024. The question remains when the Fed will start cutting, whether it’s during their June or July meetings in time for the summer housing season or later in the year.

The Fed Chair stated during the press conference that they would cut rates sooner if they saw a deterioration in the labor market but offered no details of the exact level of unemployment that would trigger cuts.

Be On Watch

This is why it will be important to watch the data to determine when the Fed will start cutting rates.

Hopefully, we can then learn how this data-dependent Fed will approach rate cuts, particularly the timing and exact number.

Of course, the Fed considers many factors, but in this article, we’ll delve into two of the key factors investors should watch (besides inflation).

Strong Growth

One reason the equity markets have been so resilient is that the U.S. economy is not yet showing signs that the Fed’s higher-for-longer rate policy is damaging the prospects of growth.

Gross domestic product, or GDP, grew at 3.3% in Q4 last year, indicating a solid U.S. economy.

- Last year finished strong with Q3 and Q4, both posting 3%+ growth.

- For the entire year, GDP for 2023 was 2.5%.

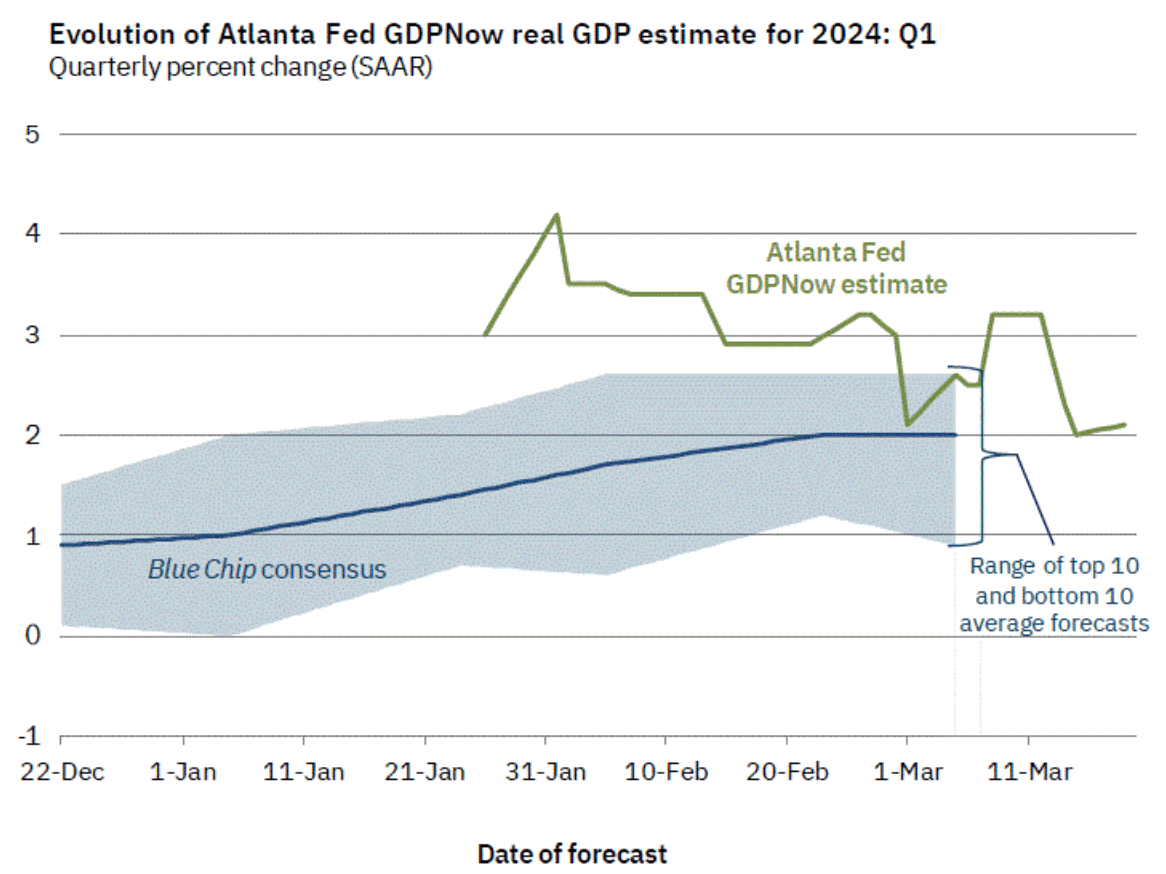

- Current growth is 2.1% as of March 19, 2024, according to Fed Atlanta’s forecast model, GDPNow.

GDP Now Forecast Q1 2024 from the Fed Atlanta (The Federal Reserve Bank of Atlanta)

- If you remember, the Fed had conditions for rate cuts that growth would moderate.

- The Fed has changed its forecasted real GDP growth rate from 1.4% to 2.1% year-on-year in 2024.

Putting it all together, the graph below shows GDP for 2023, current QTD growth (blue), and the Fed’s forecast (red and green).

The Fed’s GDP Growth Forecasts (Data from the Federal Reserve Bank and the Bureau of Economic Analysis)

Takeaways:

For the Fed to cut rates, they may want GDP growth to be lower than current levels or, at the very least, they may not want growth much higher.

What if GDP growth =

- 2.5% in Q1 2024

- 3.5% in Q2

- = 1st half GDP of 3%

What does the Fed do if the US economy averages a 3% growth rate for the first half of this year?

If growth is really strong, why wouldn’t the Fed wait, assuming that using its higher-for-longer policy isn’t hurting the economy?

In my opinion, the stronger the growth rate going into June or July, the more FOMC participants are going to favor cutting rates later this year versus by the summer.

For these reasons, GDP growth is one key factor investors should watch to determine when the Fed cuts rates this year.

The Job Market

Another key component that the Fed is watching is the labor market, including new payrolls and unemployment. The U.S. job market has been really strong.

Non-Farm Payrolls

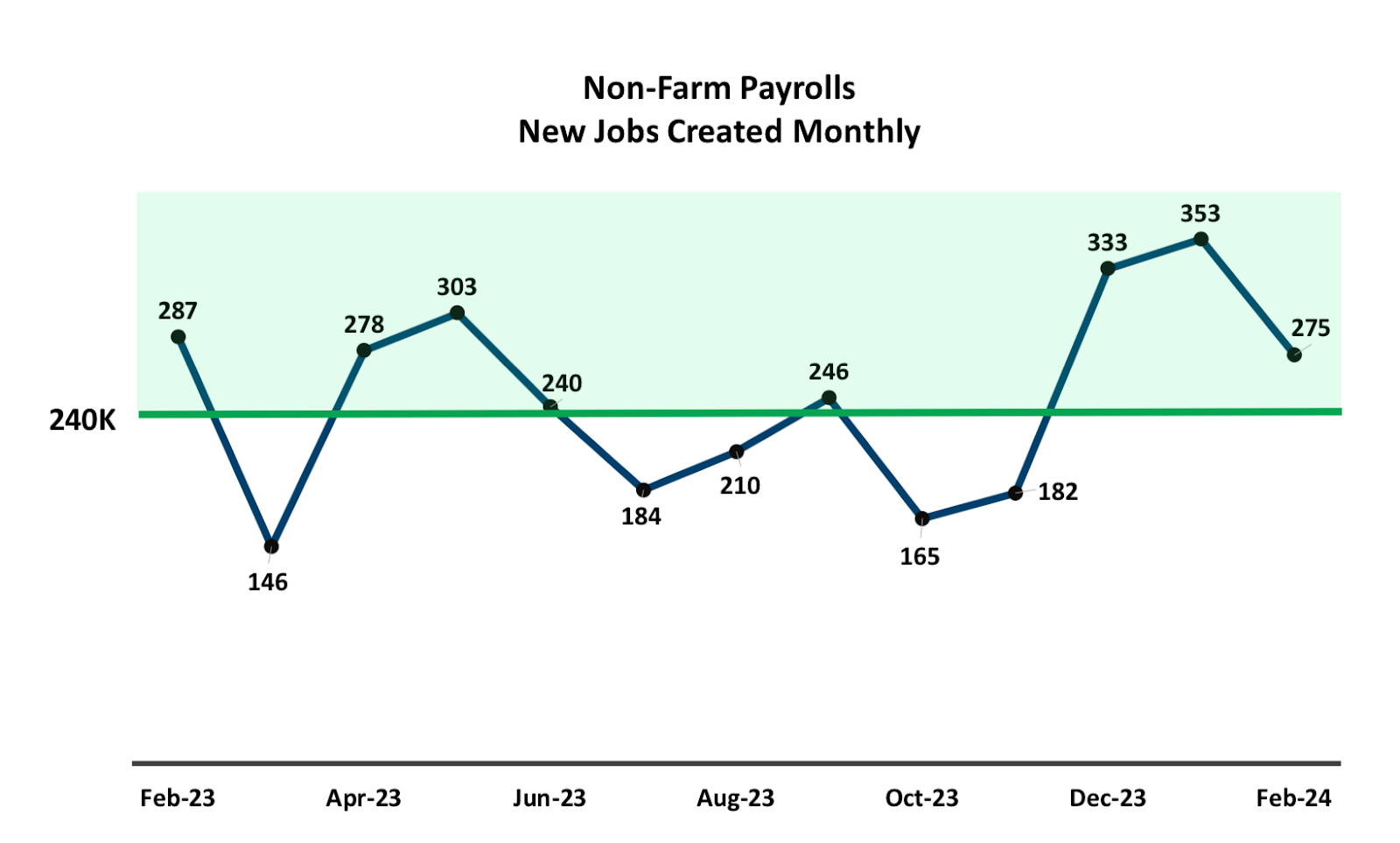

The monthly new jobs data (called nonfarm payroll employment) increased by 275,000 in February, with industries like healthcare, government, food services, and transportation leading the pack.

December of last year posted 333K, and January 2024 put up similar numbers (353K). That’s three months in a row with over 250K new jobs.

In total, the U.S. has created more than 3 million new jobs since Jan. 2023 — for an average of 230,000 per month.

- In the graph below, shown in green, are the number of months that NFP has come in above 240,000 or 8 months since Jan. 2023.

Nonfarm payroll monthly gains from Jan. 2023 to Feb. 2024 ( U.S. Bureau of Labor Statistics (BLS).)

NFP Chart by Chris B Murphy. Data from the

U.S. Bureau of Labor Statistics (BLS).

Some critics have argued that many of the new jobs are part-time, while others argue that companies can’t afford full-time, because of the cost or can’t find enough full-time workers.

Regardless of your position, it’s a tight labor market, which can lead to higher wages, which the Fed considers inflationary. That tightness is shown in the unemployment rate.

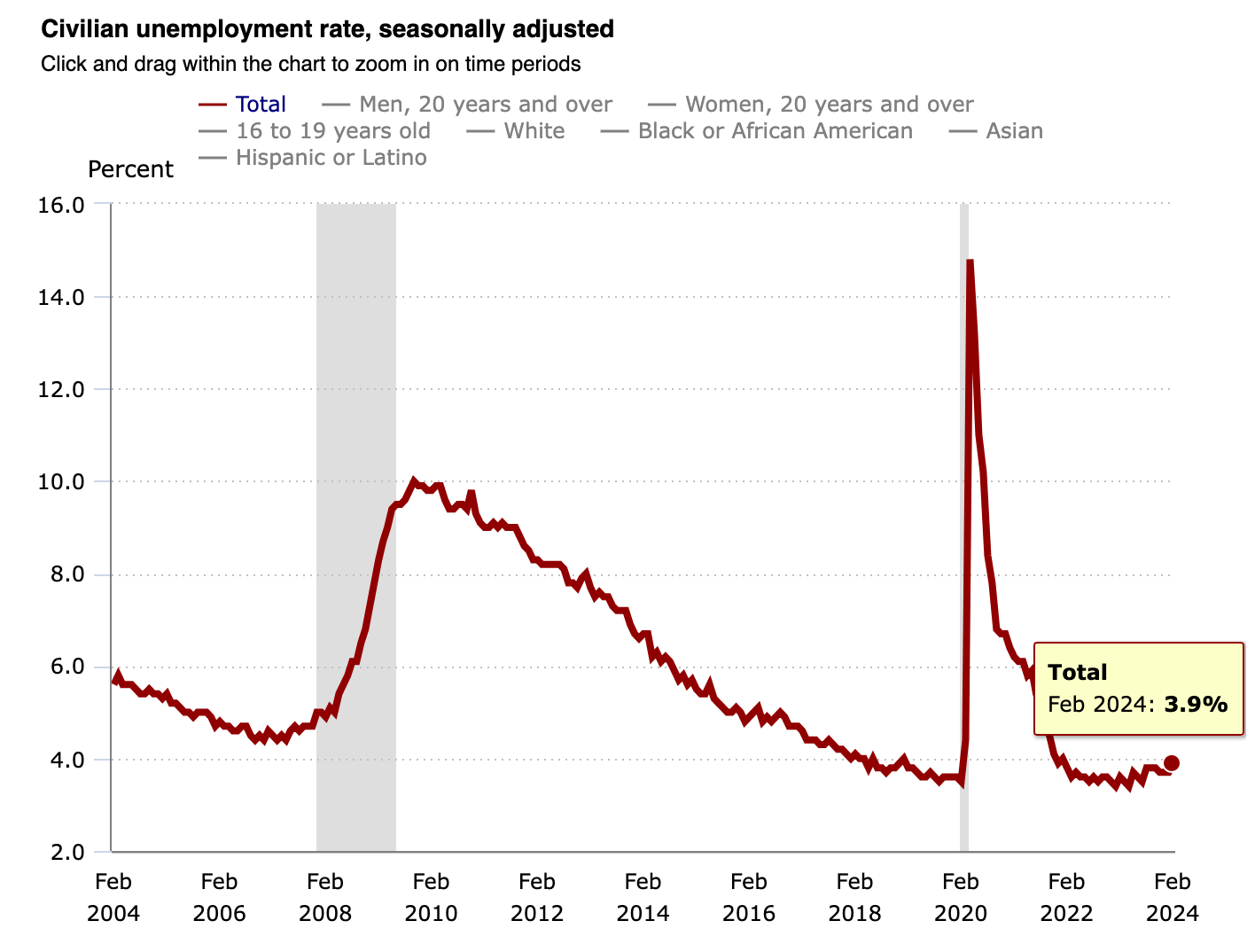

Unemployment: Near 20-Year Lows

Although the Fed doesn’t forecast non-farm payrolls, they do forecast unemployment.

- The Fed’s unemployment forecast is 4.0% for 2024.

- The unemployment rate is 3.9% (as of Feb.) versus 3.7% in January, according to the U.S. Bureau of Labor Statistics (BLS).

Check out the chart below, which shows the U.S. has one of the tightest labor markets in 20 years.

CPI Inflation data. (The Bureau of Labor Statistics (BLS).)

Graph from the

Bureau of Labor Statistics (BLS).

Takeaways:

Fewer monthly job gains via NFP would be ideal for the Fed.

The Fed likely wants non-farm payrolls to come in below 100K to help push up the employment rate. This would reduce labor market tightness while not hurting workers since they’d likely only be unemployed for a few months.

The U.S. economy usually needs ~150K new monthly jobs just to keep pace with the number of new workers coming into the workforce.

Nonetheless, if we continue to see 200K-350K non-farm payroll numbers, the Fed may delay rate cuts.

Wrapping Things Up:

The Fed’s upcoming meetings will be critical in determining whether we see rate cuts in time for the summer housing season.

More Questions than Answers

The more we analyze, the more questions come up and here are a few that investors should consider:

- When will the Fed cut rates and by how much?

- What data is the Fed’s data-dependent policy hinged on?

- Where do growth and employment need to go for rate cuts to happen, or is it strictly an inflation watch?

- What specific metrics would cause a delay in rate cuts until later this year?

- How would the equity markets react to delayed rate cuts?

- How do the equity markets react if the Fed decides to cut only once between now and September or December?

Of course, this is not an exhaustive list of all the factors that influence monetary policy decisions. Inflation, consumer spending and confidence, the savings rate (called M2), business activity, and bank lending are just a few others.

The Fed changed its GDP growth and unemployment forecasts to be more in line with current figures. However, I believe they’ll cut rates anyway in 2024 unless inflation jumps.

However, please monitor any changes in the GDP growth rate and the labor market, as these could delay cuts, putting the equity markets at risk of correction.

Good luck out there.

Q2 2024 Earnings Call Transcript")