Dilok Klaisataporn

Mid last year, I wrote an article on the JPMorgan Nasdaq Equity Premium Income ETF (NASDAQ:JEPQ) arguing that it is a compelling vehicle through which to strike a balance between high current income and upside potential from the price appreciation perspective.

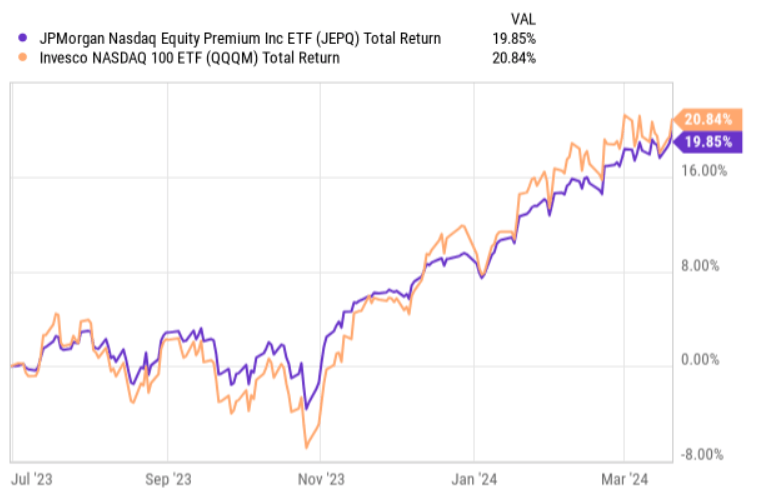

Since then, JEPQ has gone up in a very similar fashion as the underlying index it seeks to replicate (i.e., the Nasdaq 100).

YCharts

Interestingly, from the chart above we can observe two dynamics that I also outlined in my bull thesis on JEPQ:

- During times of downside volatility, the JEPQ has produced better returns relative to the index (e.g., September – November period of 2023).

- In the upward-trending markets, JEPQ has performed quite similar to the index, but with a slight negative alpha given the presence of the options (i.e., the covered call strategy).

All in all, I have to conclude that going long JEPQ was a sound idea as it managed to tick all of the necessary boxes of the bull thesis: delivering solid streams of current income, while on a total return basis generating similar results as the underlying index.

With that being said, in my opinion, now is the right time to deemphasize JEPQ and instead focus on the other opportunities.

Here is why.

Thesis update

There are three distinct reasons why I am downgrading JEPQ from buy to hold.

#1 Subpar yield level

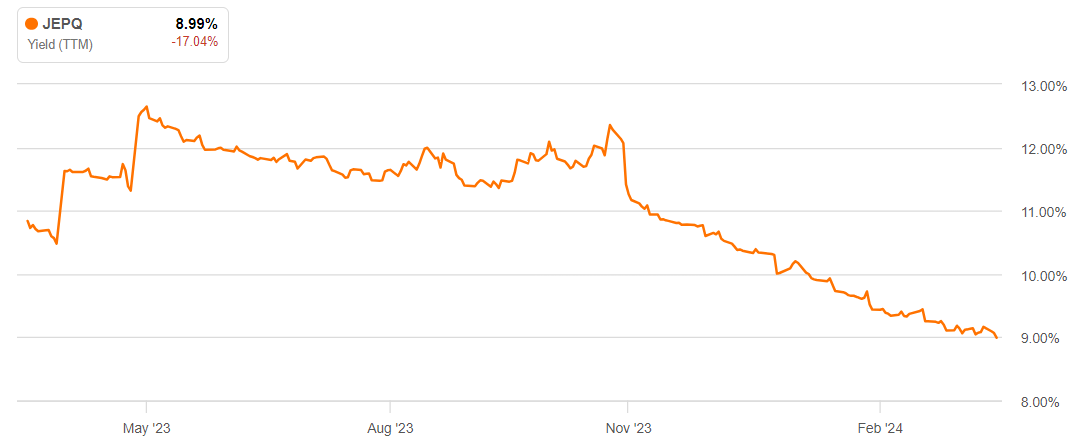

Over the TTM period, JEPQ’s dividend yield has dropped quite materially from ~11% at the time when my first bull thesis was issued to currently 8.9%.

Seeking Alpha

The dividend decrease has been systematic without any meaningful reversals to the upside. In fact, looking at the assumed trajectory and momentum, it seems that it is highly likely that the downwards-sloping trend will continue.

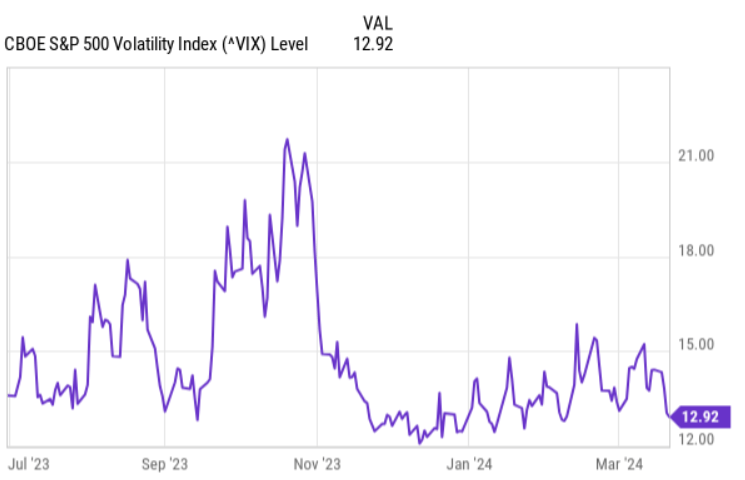

Now, the key driver behind this is the depressed VIX.

YCharts

We can see here that as VIX has plunged from the November highs, the JEPQ’s dividend has dropped accordingly.

At the core, it is fully explained by the embedded covered call program, which captures premium from sold options. When the implied volatility is low (i.e., the market has become less fearful), the option premiums tend to go down. As a result, by selling cheaper options, JEPQ pockets smaller option premiums that in turn negatively impacts the dividend distribution capacity.

#2 Unfavorable entry point

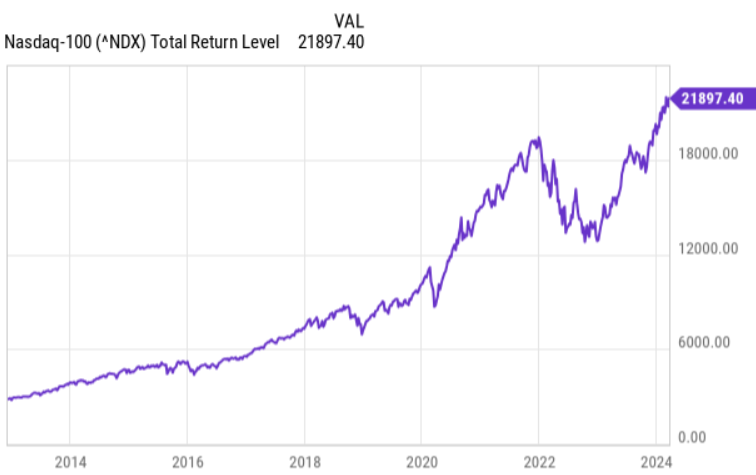

If we zoom back and take a look at the market capitalization levels, it is clear that currently we are at or very close to all time highs.

YCharts

Granted, everyone who has bet against the market and assumed a bearish stance just because the market is trading at peak levels has suffered a huge opportunity cost by foregoing the amazing returns that have been generated by the major large cap indices.

It really boils down to investing style and conviction of where the market will be going from here.

For me, the fact that the market trades at record levels, while the overall economic context seems to be weakening and becoming increasingly unclear makes me uncomfortable in opening notable exposure against the index.

In fact, we have to remember that the index, which JEPQ tracks is largely driven by the magnificent 7 names, which introduces a notable concentration risk here.

While JEPQ follows a covered call strategy, it is still heavily correlated with the Nasdaq 100. So, if the market goes down due to a major price / valuation correction, JEPQ will follow.

#3 Aggressive SOFR expectations

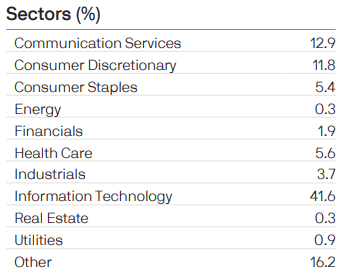

As of now, JEPQ is considerably exposed to tech and communication services stocks all of which are extremely sensitive to the interest rate dynamics. For example, the tech businesses tend to carry a back-end loaded cash generation profile that is driven by the inherent growth expectations. In such cases, the interest rate swings tend to affect the valuations more than, say, for more value-focused stocks that are already now reached or is close to their full cash generation potential.

JPMorgan Chase & Co

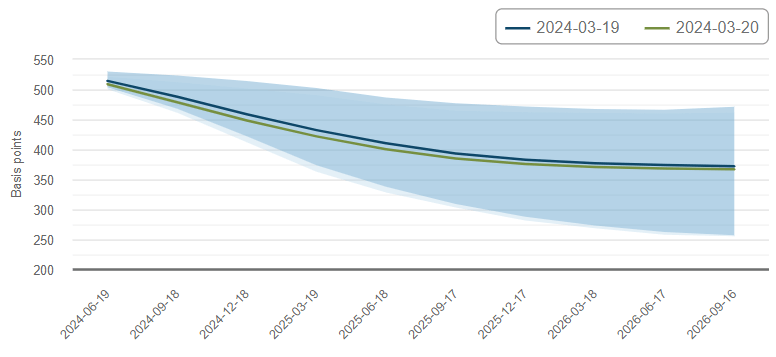

Before I issued my previous article on JEPQ, it was still unclear how the FED would approach the normalization of SOFR. Since then, we have realized that SOFR has already reached its peak level and is very likely to get cut several times this year.

The Federal Reserve Bank of Atlanta

What this does is it automatically forces the market to reprice the stocks accordingly driving up the valuations of most of JEPQ’s underlying constituents.

Again, different people have different opinions as to whether the FED will actually manage to make three cuts this year, but it is clear that we are not talking about four cut, but rather potentially two or even less.

Any recalibration to the downside (i.e., higher for longer) will inevitably trigger a notable share price correction of the same companies that have skyrocketed lately due to more positive SOFR news.

The bottom line

The reasons why I am downgrading JEPQ from buy to hold is related to an unfavorable timing, where three distinct factors have formed a tough basis from which to continue generating decent returns:

- Dividend yield is relatively low due to depressed implied vol levels.

- The underlying constituents of JEPQ are at all time highs.

- The optimistic case of SOFR trajectory has been baked into the cake.

So, really from the risk and reward perspective, JEPQ has become less attractive.

Finally, I still consider JEPQ a superior choice over an investment in pure-play tech driven index such as the Nasdaq 100 or the S&P 500. The reason for this is simple: the embedded covered call strategy offers some downside protection and smaller correlation levels in the case of downwards trending market that against the backdrop of the three aforementioned factors comes in handy.

Q2 2024 Earnings Call Transcript")