DSM_Sergiy/iStock via Getty Images

We are updating our coverage of DSM-Firmenich (OTC:DSFIY)(OTC:DSMFF) after the company delivered full-year 2023 financial results, and made some additional announcements like the planned separation of their Animal Nutrition & Health business. In our last article, we gave the company a “Neutral” rating given its strong competitive moat, balanced with shares being fully valued and challenges in the vitamin market.

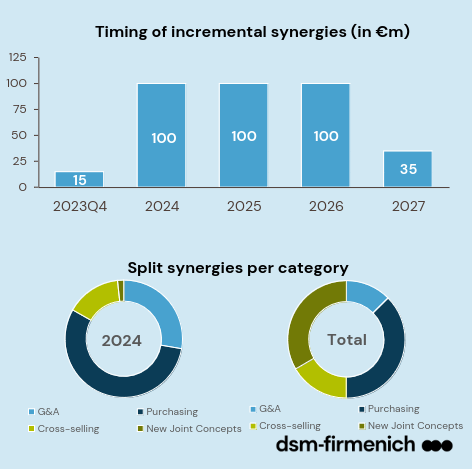

As a reminder, DSM-Firmenich is the result of the merger of DSM (OTC:KDSKF), which is a leader in nutrition, health, and bio-sciences, with private Swiss company Firmenich, which specializes in flavors and fragrances. The combination created a bio-sciences giant that competes with the likes of Givaudan (OTCPK:GVDNY), Symrise (OTCPK:SYIEY), International Flavors & Fragrances (IFF), and Novonesis (OTCPK:NVZMY). There is no doubt this merger created a powerhouse in this industry, which is highly attractive given the high customer switching costs and proprietary IP. This makes it difficult for customers to source these ingredients from others. Still, part of the merger rationale was based on cost and revenue synergies, and so far we are disappointed with what the company has delivered. The company reported having captured only €15 million in synergies during Q4, a pace we consider slow. It is projecting €100 million per year in incremental synergies from 2024 to 2026, and a small additional benefit in 2027.

DSM-Firmenich Investor Presentation

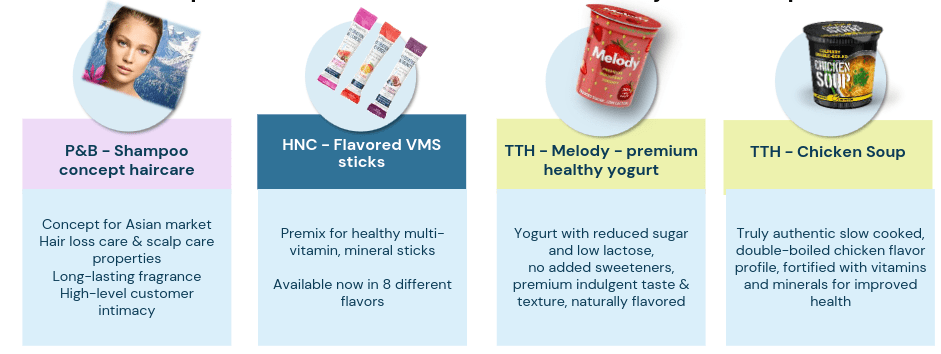

We have always been more skeptical of revenue synergies compared to cost synergies, as they are more difficult to demonstrate and it is easy to overestimate cross-selling opportunities. Still, the company has shared a few product launches that were the result of using combined IP and R&D efforts. The slide below shows some of the new joint concepts that the company is preparing for market introduction.

DSM-Firmenich Investor Presentation

The Vitamin Problem Persists

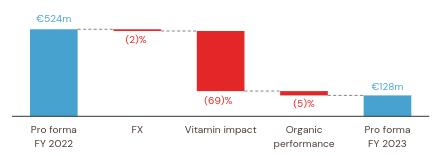

Despite mitigation efforts by the company to reduce the impact of a challenging vitamin market, results remain underwhelming. The company had previously announced a €200m cost reduction program, which it reports is well underway with closures of Vitamin B6 and Vitamin C plants and employee count reductions.

This helped deliver the first €10 million in savings in Q4 2023 but was not enough to compensate for the weak organic sales. The company saw decreases in volumes and prices, and continued reduction of inventories by its distributors. This had a massive impact on the Animal Nutrition & Health business segment.

DSM-Firmenich Investor Presentation

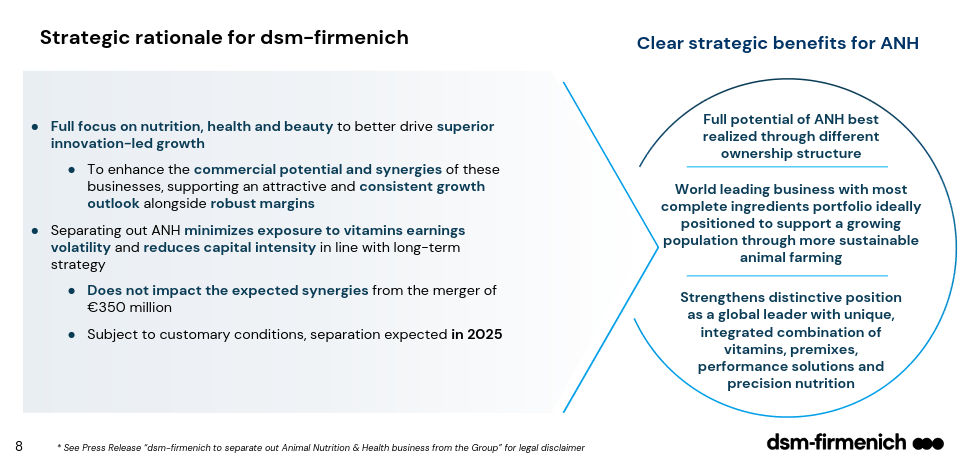

As a result, the company is eager to get out of this business, and it announced plans to separate it in 2025. The company argues that the segment’s potential can be “best realized through a different ownership structure”. We are not fully convinced with this argument and would prefer that management fix the business first before selling it, in order to maximize value for shareholders.

DSM-Firmenich Investor Presentation

R&D

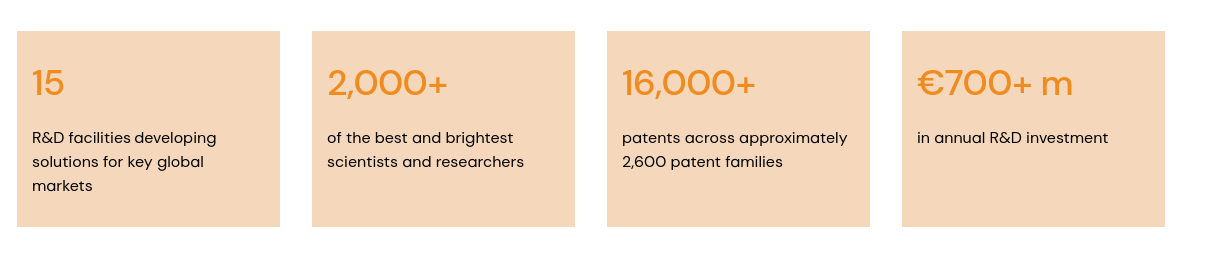

On the positive side, the company continues investing heavily in R&D and so far it seems this will not be an area where the company plans to cut costs significantly. It now reports having 15 R&D centers, with more than two thousand scientists and researchers.

DSM-Firmenich Website

The company shares some of its most recent breakthroughs here, one we found particularly interesting was the creation of a new flavor ingredient developed using AI that gives plant-based meat alternatives a lightly grilled beef taste.

The world’s first-ever flavor created by artificial intelligence: a delicious, lightly grilled beef taste for use in plant-based meat alternatives. High-precision engineering of proteins and strains with sustainability in mind – all in a fraction of the time needed for traditional approaches

Balance Sheet

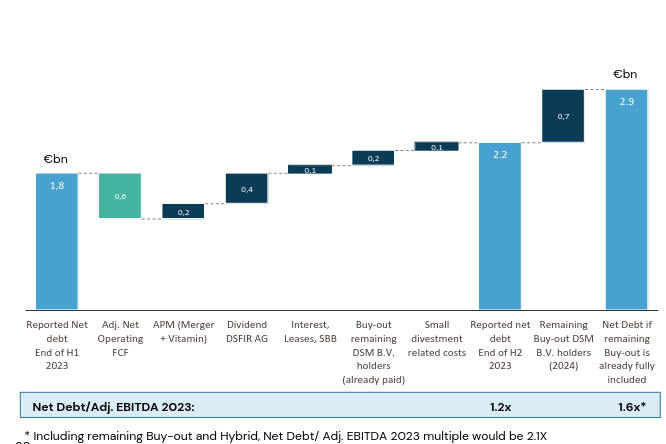

There is now more clarity on the balance sheet situation, given the various transactions that the company was doing at the same time, including the sale of certain businesses, and buying out some shareholders.

The company reported net debt at the end of 2023 of €2.2 billion. However, investors should add an additional €700 million to buy out remaining DSM B.V. (OTC:KDSKF) shareholders plus the €750 million in hybrid notes. When taking all of this into consideration, the total net debt to 2023 adjusted EBITDA would be ~2.1x.

In other words, while there is some leverage, the company’s gearing is quite reasonable. This is also reflected in solid investment grade credit ratings, with Moody’s (MCO) giving the company an ‘A3’ rating, and S&P Global (SPGI) giving the company an ‘A-‘ rating.

DSM-Firmenich Investor Presentation

Dividends

The company is proposing a €2.50 dividend per share for the financial year 2023, which puts the forward dividend yield at ~2.3%, considering that the native shares are currently trading at €105.92 in Europe.

Outlook

DSM-Firmenich estimates that in fiscal year 2024, it will deliver an adjusted EBITDA of at least €1.9 billion, which assumes a step-up in adjusted EBITDA of €200 million from synergy deliveries and the measures taken regarding the underperforming vitamins business.

The company will share more details when it presents its Capital Markets Day business plan on June 3rd, 2024. We see the company’s target as achievable, but mostly because we believe the economy is showing signs of resilience and some of the de-stocking issues the company has experienced should start to dissipate. We are skeptical that the company will be able to fully deliver the promised synergies.

Valuation

DSM-Firmenich currently has an enterprise value of around €30 billion, which means the forward EV/EBITDA is around 15x. This is not exactly a cheap valuation, but the industry has generally traded with high multiples given its attractive characteristics.

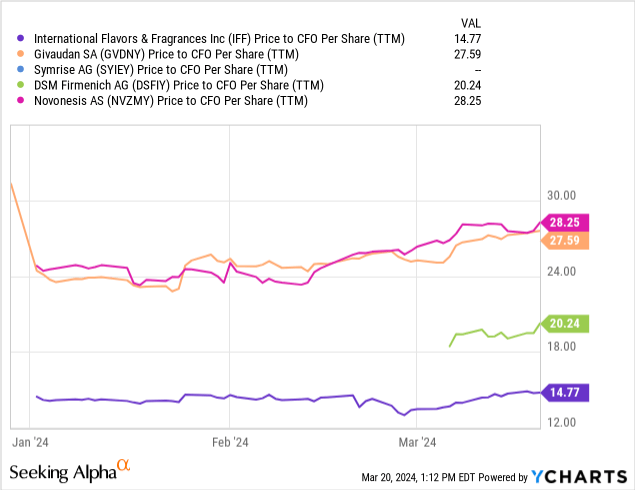

Looking at the Price to Cash-flow from Operations per share, Givaudan and Novonesis clearly trade at a premium, but we would argue they are higher-quality businesses on average. DSM-Firmenich’s Animal Nutrition & Health business certainly dilutes the overall quality of the company, even if its other businesses like Flavors and Fragrances can keep up with these two high-quality competitors.

Compared to International Flavors & Fragrances, the company trades at a significant premium, which is not surprising given the management issues IFF has faced, recently resulting in a dividend reduction of more than half.

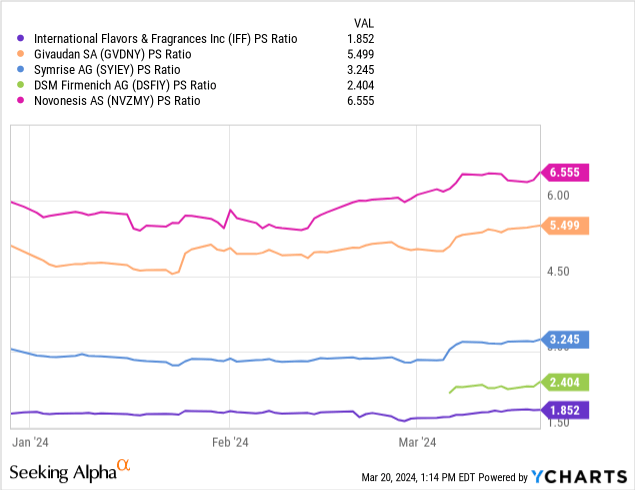

Looking at the Price/Sales ratio we get a similar picture, and while we think the market is correct in giving higher valuation multiples to Novonesis and Givaudan, it has perhaps gone too far. Despite its weak spots like the vitamin business, we think the valuation gap is excessive right now. Not because DSM-Firmenich is currently undervalued, but because Givaudan and Novonesis are overvalued.

Risks

One important risk is that the company is being investigated for price collusion with its competitors, which could result in a significant fine. It also has some exposure to China’s weakening economy, continues to face demand and pricing headwinds in its vitamin business, and de-stocking at some of its suppliers continues being an issue.

Risks are mitigated by the company’s strong balance sheet and elevated profitability, but shares could see valuation multiple compression if the company does not start delivering better revenue growth and the promised merger synergies.

Conclusion

After reviewing recent developments at DSM-Firmenich we continue to rate shares as a “Hold”, but we are getting closer to changing our rating to “Sell” if headwinds persist, or if the company does not start showing more progress on the promised synergies.

We view the €15 million in synergies captured during Q4 as a very slow start. Risks have also increased with the company under investigation for alleged price collusion with competitors, and the company looking to separate the Animal Nutrition & Health business. We worry the company might sell it at a relatively low valuation, instead of putting in the hard work to fix the business.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")