Joe Hendrickson/iStock Editorial via Getty Images

Dear readers/followers,

Brown Forman (NYSE:BF.B) is one of those companies that I did not expect to really ever become “cheap”. Nor is it, in fact, “cheap” now – let me be clear about that. I am not calling the company cheap here. It’s “Less expensive than it once was”.

Brown Forman Corporation now, as I am writing this article, trades at around $52/share. This is the lowest it has been since COVID-19. It’s still high if we view it from a 20-year trading average, and if you had bought the company a number of years ago you could have bought it at 20x P/E, and generated annualized RoR of almost 11% here, beating the market. That is a good investment because BF.B is actually a business with an A-rating in terms of credit, a market capitalization of more than $25.3B, and with less long-term debt/cap than 41%.

This company is actually one of the largest in America when it comes to the spirits and wine business segments, and it’s based in Louisville, KY, owning some of the most storied and famous brands out here.

This includes brands such as Jack Daniel’s, Old Forester, Woodford, GlenDronach, BenRiach, Glenglassaugh, Herradura, Korbel, and Chambord – and the company also has been the owner of Southern Comfort and Tuaca, but these are sold off.

Let’s look at what this company can offer you in terms of upside.

Brown Forman – Plenty to like about quality spirits

So, first off, and important to get out of the way, you do not nor is it likely that you will ever control any significant voting share of Brown Forman – this goes for “the market” as well. That is because BF.B is a family-owned business, with the dozens of members of the Brown Family owning 67% of the shares of the company. This is not a dealbreaker in any way – I own plenty of businesses that are family-owned, and that are great investments.

However, these businesses typically have very low yields – and BF.B is a great example of such a business. Even dropping as much as this, the company’s yield is no more than 1.66% in a context where 3-4% from a savings account is commonplace. It makes any argument for investing here a “tough” one, at least from a yield perspective.

The company has some of the best spirit brands in the entire world.

BF.B IR (BF.B IR)

What’s more, if you look at the company fundamentals, you will find that the company is a very profitable business on a peer comparison. In fact, it’s not an exaggeration to say that Brown Forman manages the 90th percentile or above in almost every KPI that matters. The company has LVMH (OTCPK:LVMUY)-level profits, with 60%+ gross margins, a 31%+ operating margin and over 22% net margin. Very few brands manage this, and that is even taking into consideration that these margins, as of the last 12 months, have been dropping quite significantly. Brown Forman has a storied history of profitability and margin expansion.

We’ll go into valuation later, but as of the last few months, the company has traded at a 14-day RSI (relative strength index), which is extremely favorable (Source: GuruFocus).

More on quality. The company’s products are well-loved by both consumers and reviewers. JD above all, keeps winning awards and has won #1 Whisky of the Year more than once.

BF.B IR (BF.B IR)

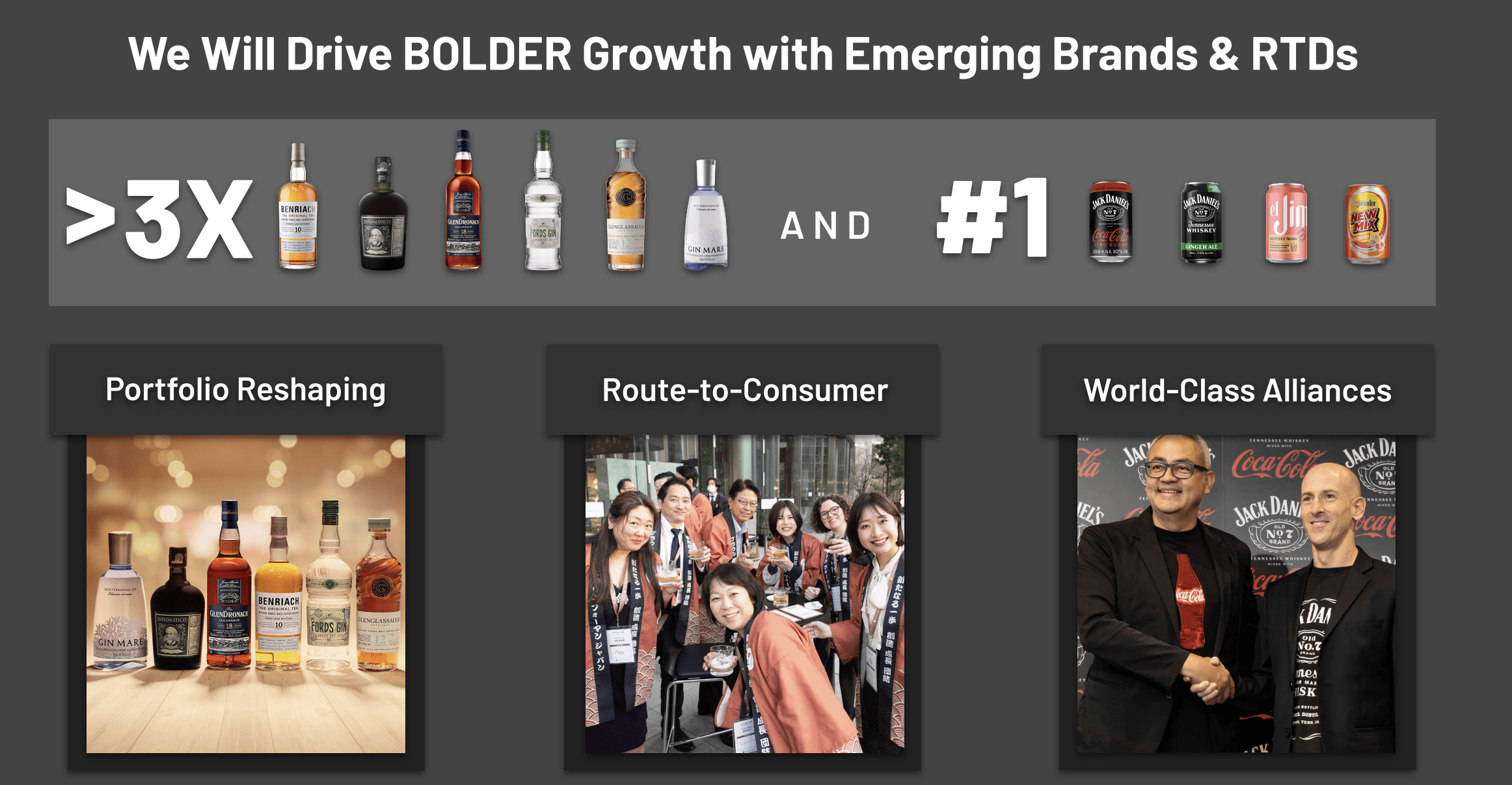

Woodford and the other aforementioned brands keep the company growing as well, with Woodford seeing international expansion not only in Europe, but in New Zealand, China, and Japan. The company also works the Tequila angle, with the company’s brands some of the quickest-growing, super-premium products out there.

BF.B IR (BF.B IR)

The company’s strategy over the past few years has been to carefully reposition its portfolio for growth and excellence, with the introduction of new products in 2014-2022, and the latest push in 2023 being mixed Coke/JD drinks being sold. This also comes with investments into superb alliances, including things like Coca-Cola (KO) with headlines being that yes, Coca-Cola is now putting Jack & Coke in a can, and ready-mixed drinks such as the JD Southern Peach.

BF.B IR (BF.B IR)

This company has been able to drive impressive TSR for a very long time, thanks to increased premiumization for the company’s valuation. However, this is where things are now slowly but surely deflating. The fault that many analysts and services seem to be making, as I see it, is that they view BF.B as able to continue to trade at 33-37x P/E, despite only growing at 3-4% per year.

Even with an A-rating in terms of credit, that is, as I see it, not even remotely close to justified here. All you really need to do is look at where the company has been trading before, to see how “out of bounds” things have gone here.

I would view the company as a company with a very wide moat, based on its market leadership and over 150 years of tradition of Tennessee Whiskey and Kentucky Bourbon. Growth, as I see it, seems likely here – but the levels of growth are unlikely to be as positive as they were before. There will likely be some growth captured from the collaboration with strong brands like Coca-Cola, and new categories like Gin and Rum as a result of super-premium acquisitions in the various spaces here.

The main challenge to the company’s operations, as I see them, is that future growth is unlikely to be as easy to capture as historical growth. The entries into emerging markets are likely to be fraught with more regulatory and tax headwinds than entries into western markets – as we can see with peer problems in geographies if you look for instance at Pernod Ricard (OTCPK:PRNDY) and their issues in China.

In the end, the addition of the new categories of drinks and spirits will add more breadth to the company’s lineup, while internationalization should improve the mix and quality of its results as well as its international market positioning.

Risks do exist for the company – and they are as follows.

Brown Forman – Risks & Upside to the company at this time

The main risks to the company are its concentration and the entry of smaller players onto the field. To the first, the company is less diversified than two of the major rivals I own shares in – talking here about Diageo (DEO) and Pernod Ricard. Its concentration makes it far more susceptible to swings in the market and downturns, which makes the former two better investments from a mixed perspective.

Not only that, both of these investments trade at far lower multiples than BF.B. DEO trades at no higher than 18-19x P/E normalized with a yield that is more than double that of BF.B and the native RI ticker for Pernod trades at 17.5x, with a yield of almost 3.2%. It goes to show you that once you open your eyes to the international markets, you can find great deals.

For that reason, I would view the risks as elevated here, and move onto valuation and show you exactly what you would be investing in, when it comes to BF.B.

Brown Forman – Good company, but too high a valuation

So, this is a great business – a good company to invest in. But like any business, it actually needs to be bought at an attractive valuation. Brown Forman isn’t at an attractive valuation at this time. What makes me say that is the fact that it trades, despite dropping down for the past few months, at no less than 27x P/E, which is well above both of the peers I consider to be valid on the European side of things here.

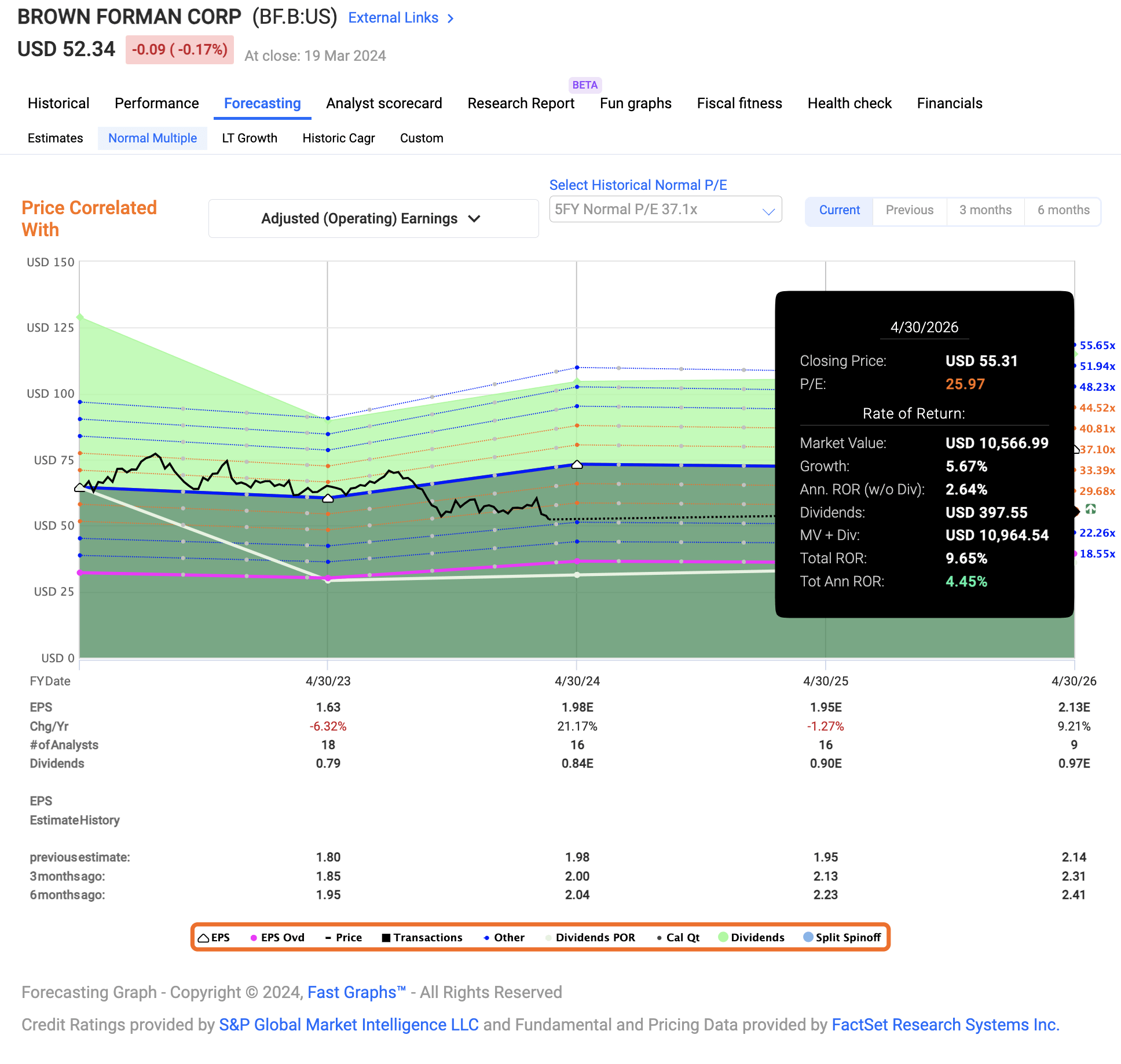

That 27x P/E isn’t justified for a company, that over the next 3 years and inclusive of the 2023A period is expected to grow less than 5% per year (Source: F.A.S.T Graphs). If the company maintains its 27x P/e, that means you’re only getting single-digit annualized RoR.

In fact, if this company manages to trade at 26x P/E, this is roughly the returns you’ll have – and 26x P/E is more than both Diageo and Pernod, both of which have higher yield and an equal sort of fundamentals and safeties, and far better sales mix.

BF.B Upside (F.A.S.T graphs)

To be quite frank, I do not understand the premiumization this company seems to command in the eyes of some. It’s a great business, it has JD and some really good brands – but there are many good spirits brands out there, and you don’t really need to pay over 25x P/E for the other ones.

Looking at analysts, there is some sense of premiumization to an average PT of around $58/share, but it’s also declined since about a year ago, when the level was around $80/share. 20 analysts follow the company, and only two consider the company a “BUY”, with most analysts, over 14, at a “HOLD”, “SELL” or similar rating. (Source: S&P Global).

In short, analysts do not consider this company all that great a “BUY”, and I agree with them here. Morningstar allows for the company to trade higher, with an FV above $60/share (Source: Morningstar). I do not agree with this assessment, based on where peers in this company which I view as superior in mix and dividends trade.

For that reason, I will assign the company an introductory rating of “HOLD” here. I view Diageo and Pernod as superior investments, and I own significant stakes in both. I would be interested in buying BF.B if I could get it at a 15% annualized upside to a valuation that makes sense on a peer average basis – where those peers included the European companies that I speak of.

So for the time being, that means the following thesis is relevant for Brown Forman.

Thesis

- Brown Forman is an interesting company, but it plays in a segment where other companies, namely Diageo and Pernod, are currently far more attractively priced. So while Brown Forman is cheaper than it has been for quite some time, I would still not call it massively attractive from a valuation perspective. This also includes the dividend, where the aforementioned two other companies are far more attractively priced.

- It comes down to a relational upside for this company versus other companies in the same or similar sector – and that is where Brown Forman simply does not come out on top. Even at a relatively high valuation, the company does not produce an annualized RoR in excess of 15% easily, which is what I am looking for.

- I am unwilling at this time to forecast the company higher than a 30x P/E, which comes to around $64/share on a forward basis – however, that is with a significant growth rate in earnings for the 2024E period. For now, I would rate the company a “HOLD”. There are better alternatives to this one on the market today.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is not cheap, and because I believe other companies have better upside and diversification in this very field, I would view this company as a “HOLD” here.

Q2 2024 Earnings Call Transcript")