David Ramos/Getty Images News

Aena S.M.E., S.A. (OTCPK:ANYYY) is the largest airport operator by passenger volume in the world with most of its traffic based in Spain. The Spanish government owns 51% of the company and retains majority voting control.

I last wrote about Aena in the article, Aena: Growing Demand As Passenger Traffic Recovery Continues.

In the article, I took a bullish opinion on Aena as I thought the airport operator would benefit from the beginning of normalization of interest rates and had an opportunity with vertiports in the future. I also noted that passenger traffic through Aena’s Spanish airports improved steadily in 2023 as of Q3 2023 and wrote that the stock had upside if passenger traffic continued to strengthen.

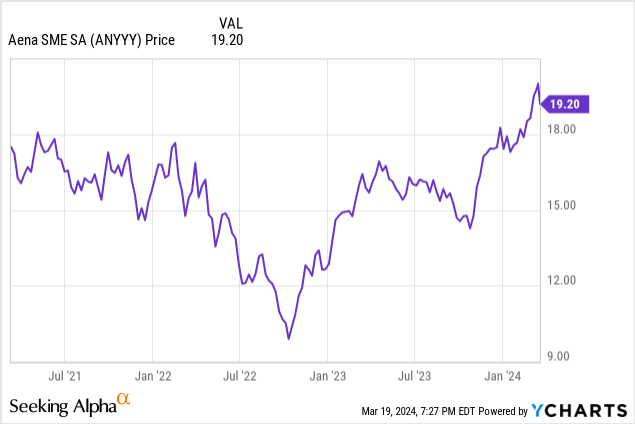

Shares of Aena largely declined from 2020 into the middle of 2022 given headwinds such as eight straight quarters of losses since the first quarter of 2020 as a result of the pandemic.

During the beginning of the pandemic, Aena’s passenger traffic through its Spanish airports declined in 2020 to 27.6% of largely pre-pandemic 2019 levels. In 2021, Aena’s passenger traffic through its Spanish airports amounted to only 43.6% of 2019 levels.

In recent years, however, Aena’s passenger traffic has strengthened as passenger traffic through the company’s Spanish airports in 2023 rebounded to 102.9% of 2019 levels. With stronger passenger traffic and a more optimistic future, Aena’s stock has done relatively well in 2023 and the beginning of 2024.

Since I wrote my last article, Aena reported full year 2023 results on February 28, and the company also presented its updated strategic plan 2022-2026 on March 7, 2024 that reflected continued strength and optimism in passenger traffic growth into 2026.

Full Year 2023

For 2023, Aena’s passenger traffic rebound continued and its financial results strengthened as a result.

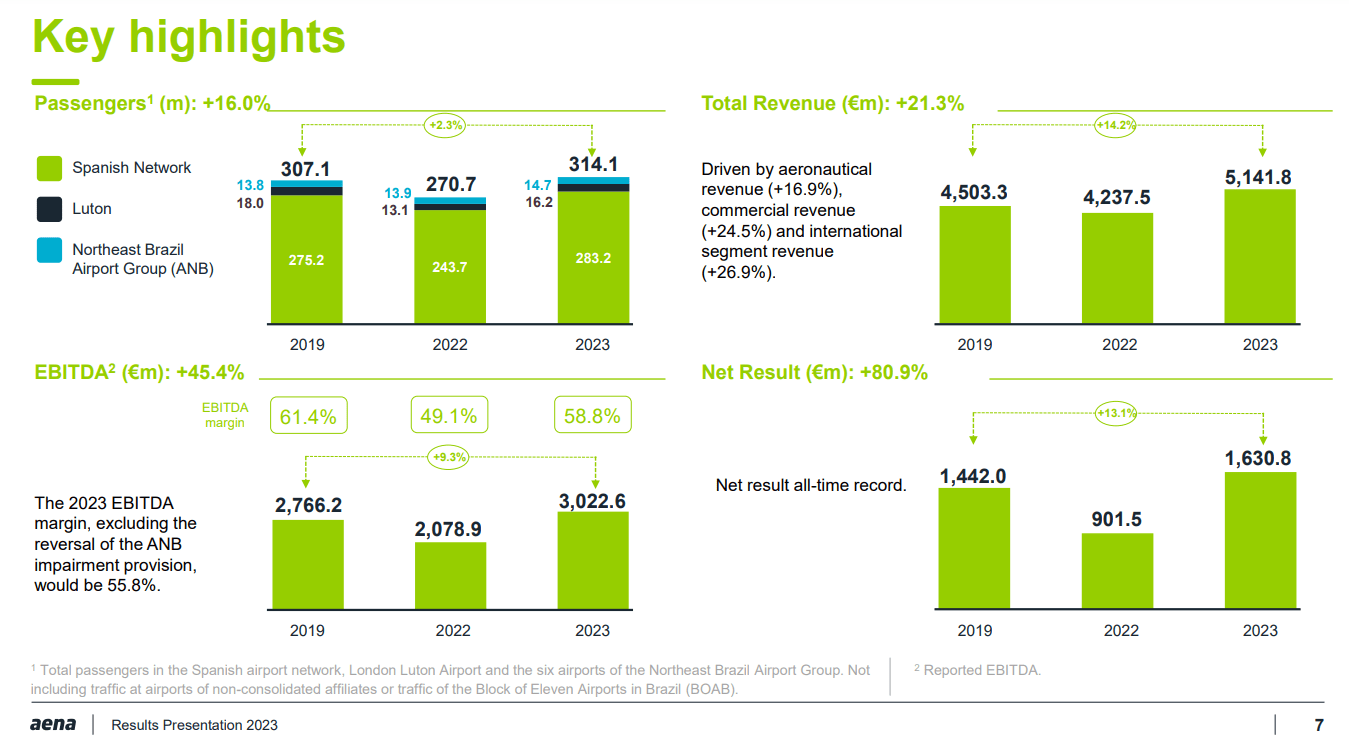

For the year, passenger traffic for the Aena Group, which includes Spain, London-Luton and the Northeast Brazil airports, rose 16% year over year to 314.1 million passengers, which is around 102.3% of largely pre-pandemic 2019 traffic.

In Spain, Aena’s passenger traffic rose 16.2% year over year to 283.2 million passengers, which is around 102.9% of 2019 traffic.

In terms of financial results, Aena’s revenue rose 21.3% year over year to €5.1418 billion. Annual EBITDA rose 45.4% year over year to €3.0226 billion, and is up 9.3% compared to 2019.

Excluding the reversal of the impairment of the Northeast Brazil Airport Group, Aena’s EBITDA margin would be 55.8%.

Net profit was €1.6308 billion, including extraordinary financial items.

Aena Investor Presentation

With the substantial increase in EBITDA, Aena ended 2023 with a net financial debt to EBITDA ratio of 2.06 compared to 3 at the end of 2022.

As a result of its 80% pay-out policy, Aena will propose to the Ordinary General Shareholders’ Meeting a distribution of a gross dividend of €7.66 per share out of the 2023 profit, up from €4.75 per share in the previous year.

It is important to realize that the Aena S.M.E., S.A. ADR is 1/10 of a regular Aena share so the planned proposal of the annual dividend is really around $0.83 for the Aena S.M.E., S.A. ADR under current exchange prices.

My takeaway is that Aena’s passenger traffic and financials were both pretty strong in 2023.

2024

2024 has been another strong year in terms of passenger traffic growth for Aena’s primary market so far.

For the month of February, which had one more day than February of last year, the airports of the Aena network in Spain received 19,226,616 passengers, up 15.7% year over year, and also transported 95,490 tonnes of cargo, up 18.6% year over year.

Both the number of passengers and the amount of cargo transported through the airports of the Aena network in Spain were all time records for February, and the strength maintained the upward trend of the previous month and most of 2023.

For the year, Aena expects to close 2024 with around 294 million passengers for Aena’s airports in Spain, versus 283 million in 2023. The company further added, “the prospects for the 2024 summer season is looking good with around 7% higher schedule than in 2023.”

In January 2024, the Spanish government also allowed Aena to raise fees it charges airlines who use the company’s airports in Spain by 4.09%.

My takeaway is that passenger traffic in Aena’s primary market is heading in the right direction in 2024 and that this year could be a strong year in terms of traffic growth.

Updated Strategic Plan 2022-2026

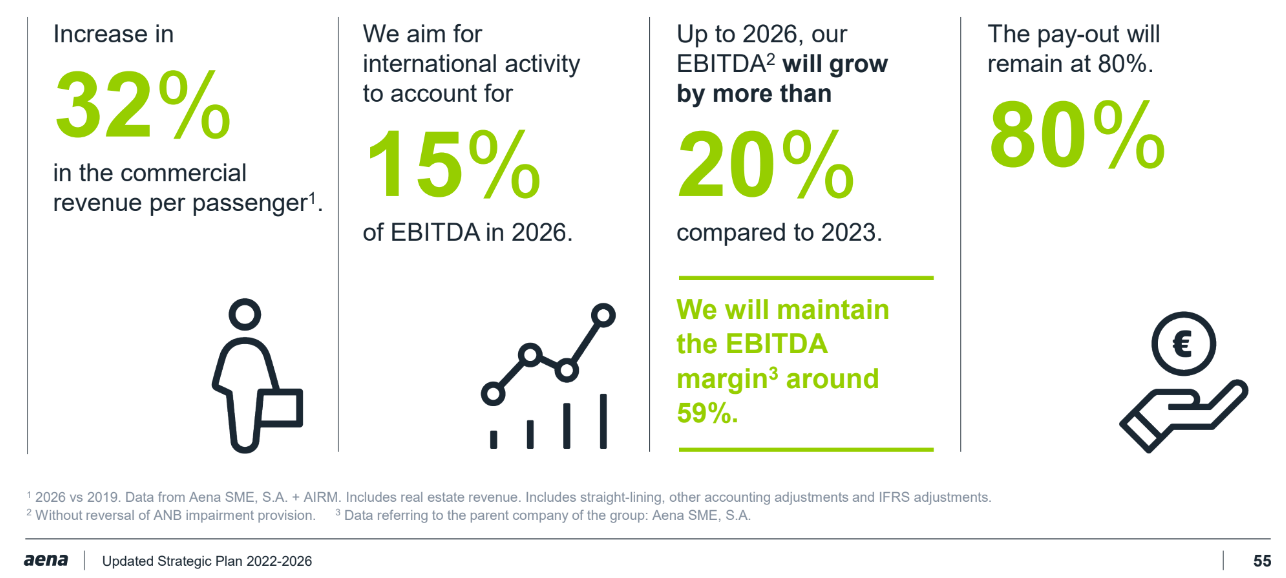

For the Updated Strategic Plan 2022-2026, Aena sees continued growth in passenger traffic. Management, in particular, expects the number of passengers in Spain to be around 294 million passengers for 2024, around 300 million passengers in 2025, and around 310 million passengers in 2026.

When including Aena’s airports outside of Spain, Aena expects to handle over one million passengers a day globally in 2026. Besides Spain, the company has considerable market share in Brazil as Aena now handles around 20% of Brazil’s passenger traffic.

In terms of financial results, Aena expects EBITDA margin of around 59% in 2026, and for international business to account for around 15% of EBITDA in 2026.

Aena also expects EBITDA in 2026 to grow over 20% compared to 2023 without reversal of ANB impairment provision.

Management also confirms its 80% pay-out dividend policy.

Aena Investor Presentation

Further in the future, Aena says it will propose investments that will at least double those committed in previous regulatory periods, with stronger traffic being a primary reason.

To put the number into perspective, Aena plans to invest a total of €3 billion in the current regulatory period of 2022-2026.

My takeaway is that Aena expects continued growth in its primary market given its guidance in terms of its number of passengers in Spain into 2026. Further out, management seems to think there will be more investment opportunities given stronger traffic potential. The company is also diversifying more internationally, which could be an opportunity for further growth.

Risks

If economic conditions weaken or flight demand isn’t strong for any number of reasons, passenger traffic might not be as strong as expected.

If passenger traffic is not strong, Aena could face headwinds in terms of its profitability and its stock. The company had 8 straight quarters of losses as a result of decreases in passenger traffic due to the pandemic, for instance.

Given the Spanish government owns 51% of Aena, the airport operator might sometimes operate in the interests of Spain rather than shareholders.

Aena might not adjust successfully to vertiports.

Valuation

In terms of earnings estimates for Aena S.M.E., S.A. ADR which is 1/10 of a regular Aena share, analysts see earnings growing.

In terms of expectations, analysts on average estimate Aena S.M.E., S.A. ADR to make $1.36 per share for 2024 and $1.44 per share for 2025. As of March 19, that gives the company a forward PE ratio of 13.99 for 2024, and 13.24 for 2025, which is an attractive valuation in my opinion.

Seeking Alpha

In terms of expectations, I think Aena could meet average analyst earnings estimates if it meets its passenger traffic growth guidance, which I think the company can achieve assuming air travel isn’t disrupted by any significant negative events.

As a result, I continue to rate Aena as a ‘Buy’ and I would hold it as ‘equal weight’ in a diversified portfolio that includes the Magnificent Seven.

I think that Aena could trade for a potential 2024 PE ratio of 16 or higher in the next year if passenger traffic continues to strengthen and interest rates begin to normalize. That gives me an upside of 14.3%+ as of March 19 levels.

I would not own too much of Aena however as air travel can change substantially in a short amount of time as the pandemic has illustrated.

In terms of passenger traffic, some tailwinds could be a stronger Euro Area economy. According to the IMF in January 2024, they expect real GDP rising in the Euro Area by 0.9% in 2024, and 1.7% in 2025 versus 0.5% in 2023.

Another potential tailwind could be the beginning of lower interest rates, which I think could happen this year. In terms of interest rates, I think they will normalize in a year or two.

In terms of things I’d follow, I would foremost follow passenger traffic trends principally in Spain but also internationally and make sure they’re going in the right direction long term.

I would also follow interest rates. I think if interest rates begin to decline, Aena would have further tailwind as that could help make its annual dividend more attractive.

I would keep an eye on what management does with vertiports as that could be a growth market in the future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")