matdesign24

The iShares Core High Dividend ETF (NYSEARCA:HDV) is an ETF with more than $10 billion in AUM, and as is typically the case with iShares vehicles, the expense ratio is very low at 0.08%.

At its core, HDV could be considered an income-producing solution for investors who want to capture stable and acceptable levels of dividend streams. The ETF seeks to replicate the investment performance of an index composed of high dividend paying U.S. stocks.

The underlying investment selection process is rather simple as it’s bound by just 75 stocks that have passed financial health and dividend-specific filters:

- Economic moat indicating whether the dividends could be sustained in the long term.

- Distance to default avoiding companies, which carry fundamentals that inherently increase the probability of default.

- Morningstar uncertainty rating reducing exposure to companies with lower margins of safety.

- Qualified dividend income increasing after tax returns.

So, given the above, we also can conclude that HDV is not that passive since it applies different financial assessment levers for including a specific name in the portfolio.

Before we transition into my arguments on why, in my view, HDV is a buy, let’s quickly establish a baseline of the key yield-focused metrics.

Since the inception the average yield of HDV has been in the range of 3.5% – 4%, which coupled with a dividend growth component offers a solid basis for capturing tangible streams of current income.

Currently, HDV yields ~3.6% and over the past five-year period has delivered a dividend CAGR of ~4.7%. It also achieved 12 consecutive years of dividend payments, where 10 of them were characterized with a y-o-y distribution growth element.

Thesis

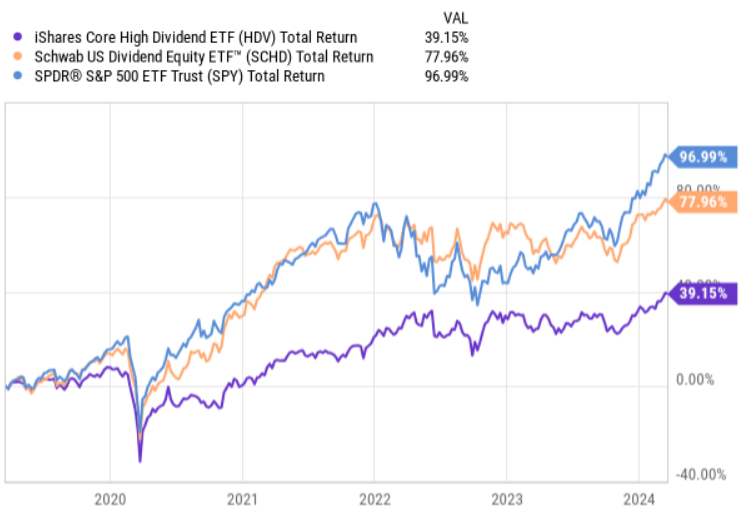

Having said that, while HDV has been rather consistent on dividends, it has massively underperformed the S&P 500 and a commonly preferred yield-generating ETF the Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD).

As we can see in the chart below, since the pandemic years, HDV has lagged behind both the S&P 500 and SCHD in a rather systematic manner. The returns have, however, correlated. But, obviously, the upside participation of HDV has been much shallower.

Ycharts

Granted, this does not send a comforting sign for the bull thesis.

However, I would like to underscore the following aspects which have explained the return divergence, but, in my opinion, are certainly subject to a reversal:

- Growth has outperformed value that (per definition) imposes an unfavorable environment for yield-focused stocks to match the returns of growth companies.

- Growth has been mostly driven by the Magnificent 7 and tech companies, which typically are not included in high-yielding ETFs.

- Value stocks are commonly characterized by capex heavy and duration sensitive factors that in the increasing interest rate environment introduces notable headwinds for free cash flow generation.

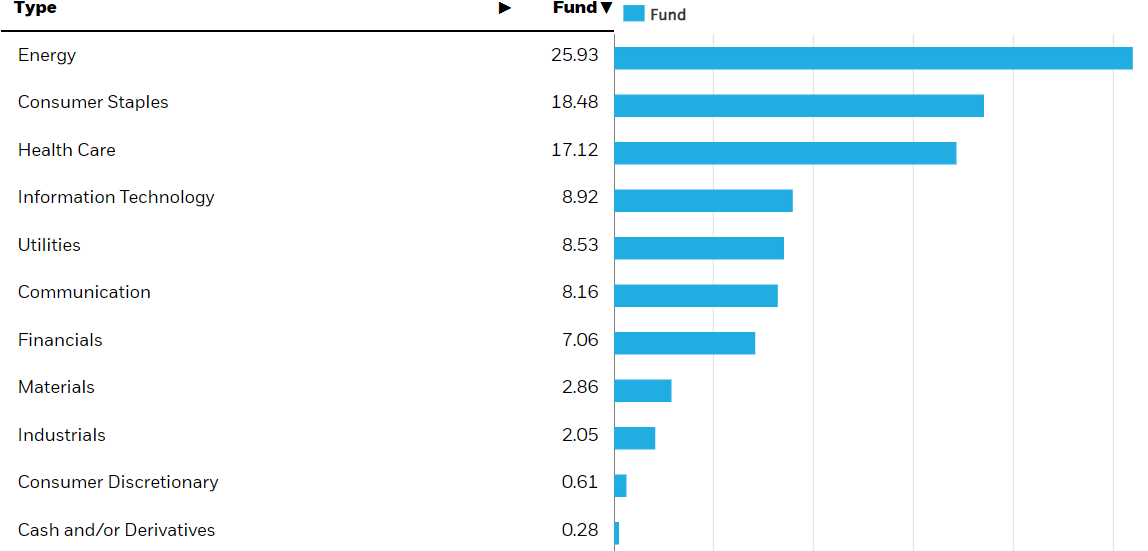

The current sector breakdown of HDV captures this story nicely. The lion’s share of HDV’s portfolio is comprised of value-tilted and interest rate sensitive sectors such as energy, consumer staples, healthcare, utilities and communication.

BlackRock, Inc

Similarly, the breakdown of top 10 holdings confirm such conclusion.

BlackRock, Inc

Let me provide some details on the top 5 largest positions (together explaining above 30% of the portfolio):

Exxon Mobil (NYSE:XOM) – dividend yield of 3.8%, payout ratio of 39% and dividend growth history of 25 years.

Johnson & Johnson (NYSE:JNJ) – dividend yield of 3%, payout ratio of 45% and dividend growth history of 61 years.

Chevron (NYSE:CVX) – dividend yield of 4.2%, payout ratio of 46% and dividend growth history of 36 years.

AbbVie (NYSE:ABBV) – dividend yield of 3.5%, payout ratio of 54% and dividend growth history of 10 years.

Verizon Communications (NYSE:VZ) – dividend yield of 6.6%, payout ratio of 56% and dividend growth history of 19 years.

Given the aforementioned, it would be fair to say that the underlying dividend is safe just as what one could imply from HDV’s stock selection screen. Moreover, the stocks with highest concentration in HDV’s portfolio carry the necessary characteristics to provide solid yield going forward – i.e., relatively acceptable dividend yield, conservative payout ratio and strong track record of dividend growth.

Also, the fact that HDV has managed to deliver a tangible five-year dividend growth CAGR, which includes the period of extremely unfavorable conditions for HDV companies (e.g., elevated SOFR) sends a great signal of notable upside potential once the conditions become more favorable for value.

The bottom line

HDV yielding 3.6%, where the underlying cash flows are underpinned by robust businesses and well-covered dividends that are clearly subject to further growth could be nicely placed into yield-seeking investor portfolios.

The risk (which happens to also be an advantage) is HDV’s tilt toward value. Historically, and especially since the outbreak of COVID-19, the value bias has imposed serious drag on HDV’s performance leading to a significant return gap from the relevant benchmark levels.

Going forward if the Magnificent 7 and growth in general continue to register alpha, HDV will still most likely underperform on a total return basis. Yet, here’s the thing, sooner or later the value should come back into vogue, where the decreasing SOFR could act as a catalyst lifting more capex intensive and traditional businesses higher than growth-oriented companies. In such a case, HDV also will benefit from price appreciation component, and not only from gradually growing dividends.

For me HDV is a buy.

Q2 2024 Earnings Call Transcript")