DanielAzocar

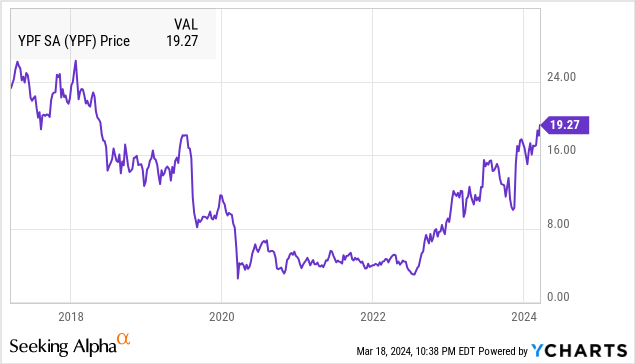

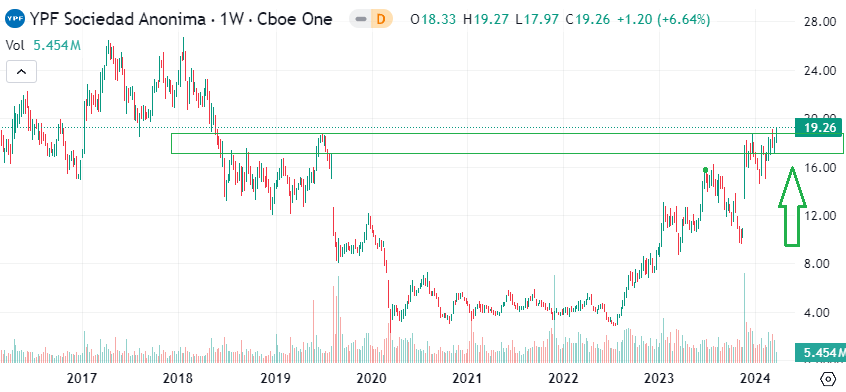

YPF SA (NYSE:YPF) has quietly rallied to a near 6-year high with Argentina’s state-controlled energy company benefiting from a wave of optimism toward the new Javier Milei Presidential administration. A backdrop of market-friendly economic policies including efforts to relax export and pricing restrictions controls are seen as encouraging investments in the country.

Beyond the improving sentiment, the company’s latest quarterly result was highlighted by a jump in crude oil production and firming margins reflecting an ongoing operational and financial turnaround. Plans to significantly increase shale oil output and expand midstream capacity over the next few years support a more positive long-term outlook. We are bullish on YPF with a sense that several tailwinds can push shares higher.

YPF Earnings Recap

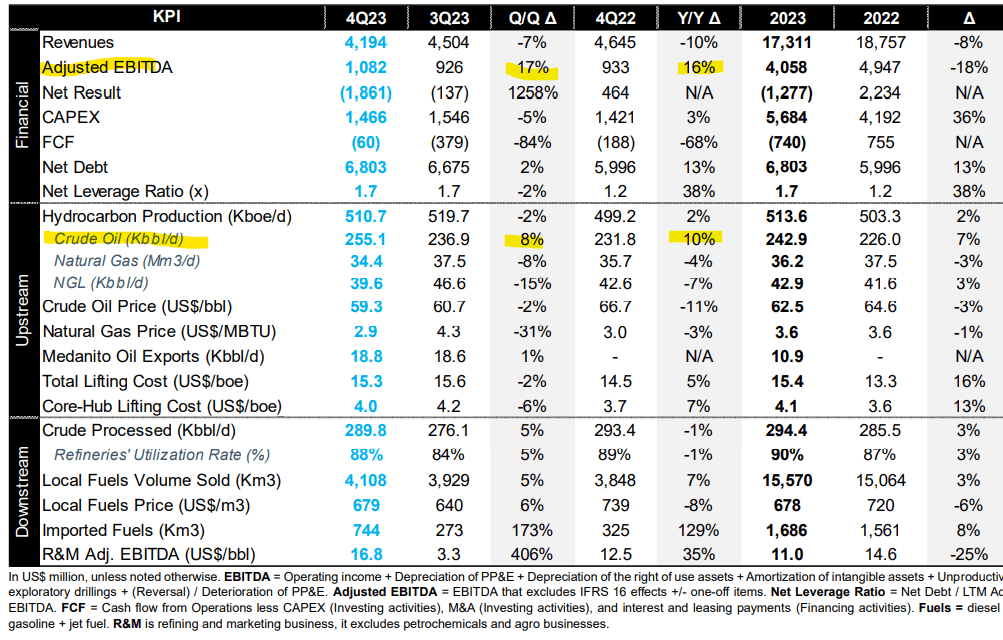

YPF reported a Q4 GAAP net loss of -$1.9 billion although this amount included a large impairment charge related to the disposal of a conventional oil field. Nevertheless, adjusted EBITDA increased by 16% year-over-year to reach $1.1 billion as a better indicator of the underlying financial strength.

Revenue of $4.2 billion declined by -10% from Q4 2022, largely reflecting the decline in oil and natural gas prices over the period, despite a 2% increase in total hydrocarbon production. That said, the bigger story was a 10% increase in crude oil output to 232k bbl/day average, leveraging company records for drilling and fracking operational efficiency.

source: company IR

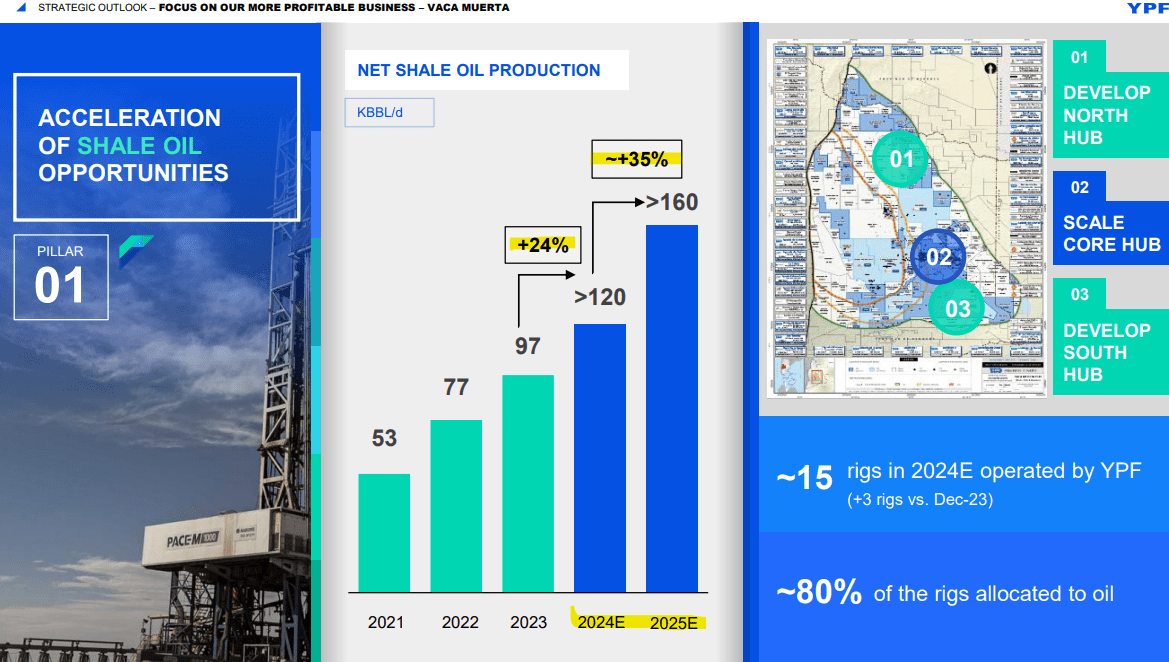

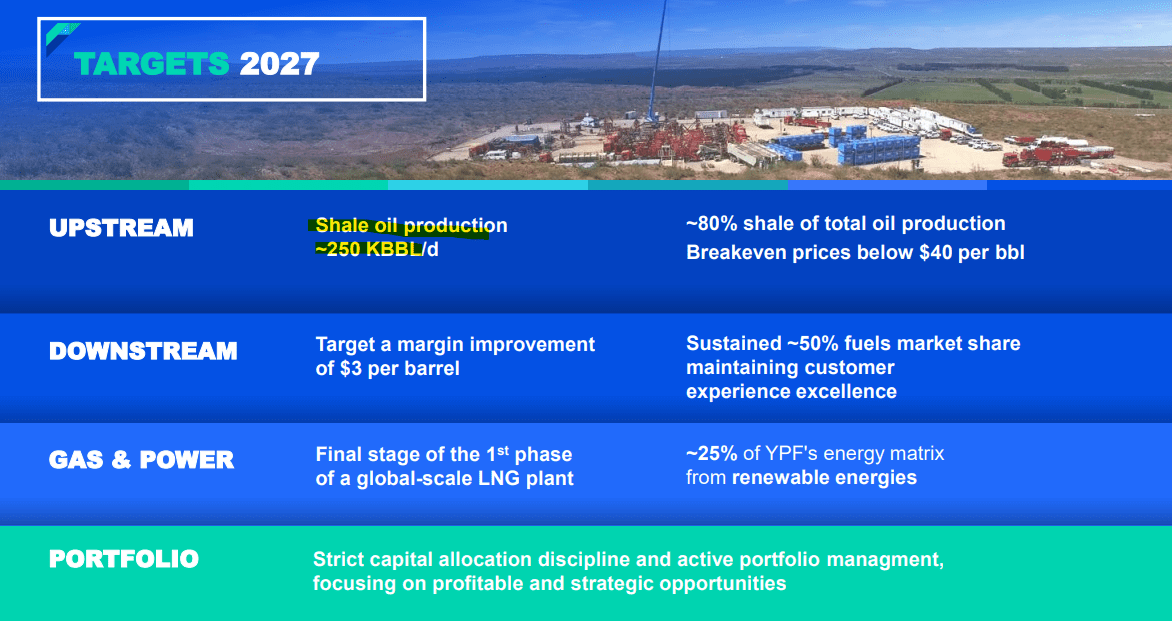

For 2023, net shale oil production at 97k bbl/day climbed by 27% y/y and represents approximately 46% of total hydrocarbon production. Favorably, that side of the operation is seen as helping to lower total lifting costs over time and supporting the positive outlook. This covers the highly profitable “Vaca Muerta” shale formation, recognized as one of the world’s largest active gas and oil reserves in the world.

For 2024, YPF is targeting a 24% increase in shale oil growth to over 120k bbl/day which should re-accelerate again above 160k bbl/day by 2025 by focusing investment efforts to develop this region. From an average total lifting cost of $15.4 billion in 2023, the company sees that measure being reduced by nearly 50% towards $8 by 2025.

source: company IR

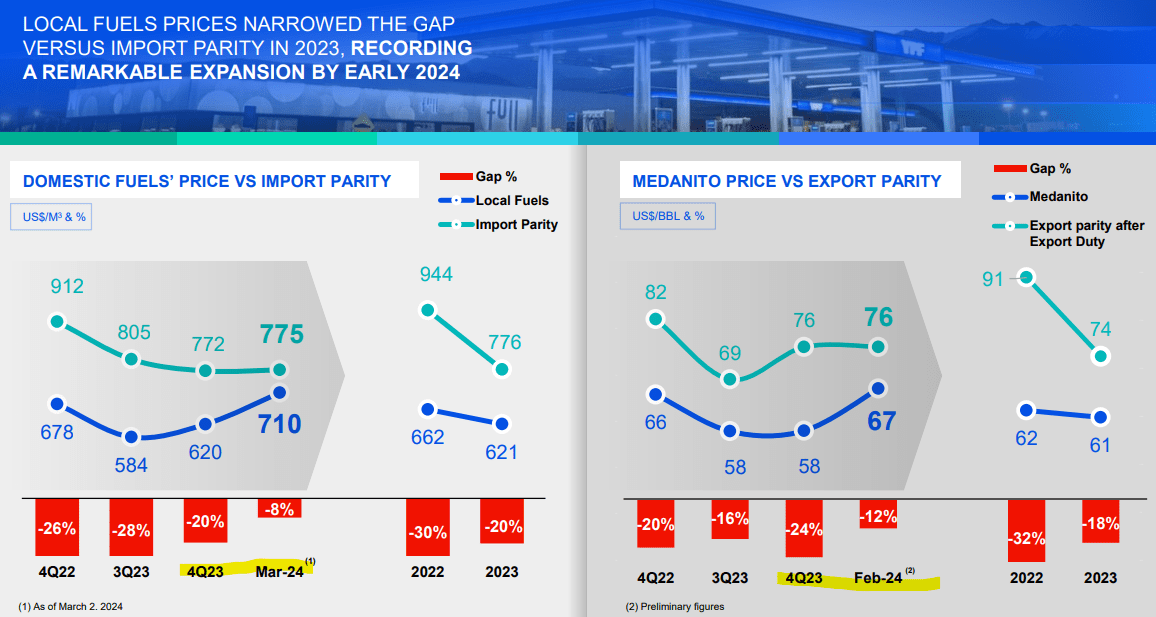

The other major theme here is what the company is calling a “remarkable” narrowing of the pricing gap between local fuel pricing in US dollar terms relative to import parity which has continued into 2024.

In this case, the combination of lower international energy prices while taking steps to adjust prices higher domestically coupled with record demand in Argentina has been positive for the results. Separately, the company is also benefiting from a resumption of Medanito exports to Chile at more favorable prices.

source: company IR

What’s Next For YPF?

YPF isn’t perfect, but the latest trends suggest the company is moving in the right direction. The importance of the expected output ramp-up through 2027 coming from the shale developments is that it opens a path where Argentina can transition from its current position as a net importer of energy products to one of being a net exporter.

The potential there would be a game changer for the company in terms of financial flexibility with the impact on greater profitability. This was a point addressed by management during the latest earnings conference call:

We so far continue to purchase about 20% of the total crude that we processed in our refineries. But clearly, as we continue to expect our oil production to increase in coming months and in coming years, we would expect total purchase volumes to decline over time, while at the same time, we increase our exports.

And so over time, and as we said, probably in five years from now, we are expecting to reach a percentage of about 35% to 40% of our total production to target the export markets while we reduce our net purchases to a level of about 5% to 10% of the total processing volumes.

As it relates to the current Milei administration, reports suggest official policy is taking a hands-off approach to YPF, or at least much less controlling compared to prior regimes. While early rhetoric of moving toward full privatization has been abandoned, the understanding is that the company should benefit from the overall more positive economic backdrop.

An early sign of success in economic reforms has been two consecutive months of a fiscal surplus in the country for the first time in over a decade. The country’s sovereign bonds have also rallied with a lower credit risk this year. In many ways, the rally in YPF captures some of those dynamics.

source: company IR

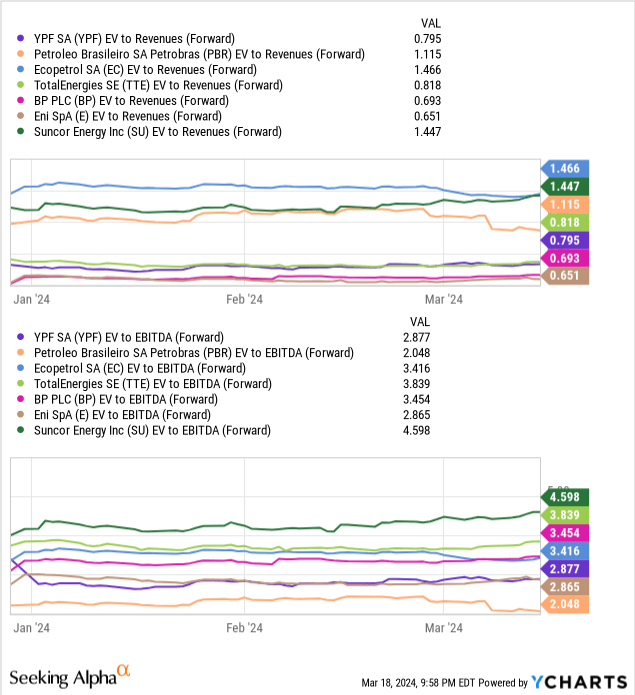

In terms of valuation, at least based on full-year 2024 consensus estimates, YPF with a 1x EV to forward revenue multiple or 3x EV to forward EBITDA is broadly in line with names like Petrobras SA (PBR) and Ecopetrol SA (EC) and other foreign oil names.

That being said, the attraction with YPF is going to be looking into 2025 and beyond when the current production ramp-up reaches scale and the company transforms into a net exporter. The expectation here is that YPF will generate stronger growth over the next several years which could justify a wider valuation premium. With some confidence in the operational targets set by management, we believe YPF is simply undervalued.

The setup we see is for YPF to continue trending higher, particularly in the context of what has been a resurgence of the energy sector with the price of crude oil back above $80bbl. As we see it, YPF works as a proxy not only for the more liberated Argentine energy sector but also representative of improving prospects for one of Latin America’s largest economies.

Seeking Alpha

Final Thoughts

YPF has already surprised a lot of people but it still has a lot to prove. We’re bullish on the stock but also recognize it won’t be a straight line higher and the base case here is to expect volatility going forward.,

When we talk about emerging markets, and Argentina especially, a layer of skepticism and caution is warranted. The country continues to face significant economic challenges and YPF still has a long road ahead to execute its growth and financial strategy.

The risks here to consider extend from the political front to high-level macro themes during the global energy market. The key monitoring points for YPF will be its shale oil output alongside metrics like cash flow and the adjusted EBITDA margin over the next several quarters.

Q2 2024 Earnings Call Transcript")