Sundry Photography

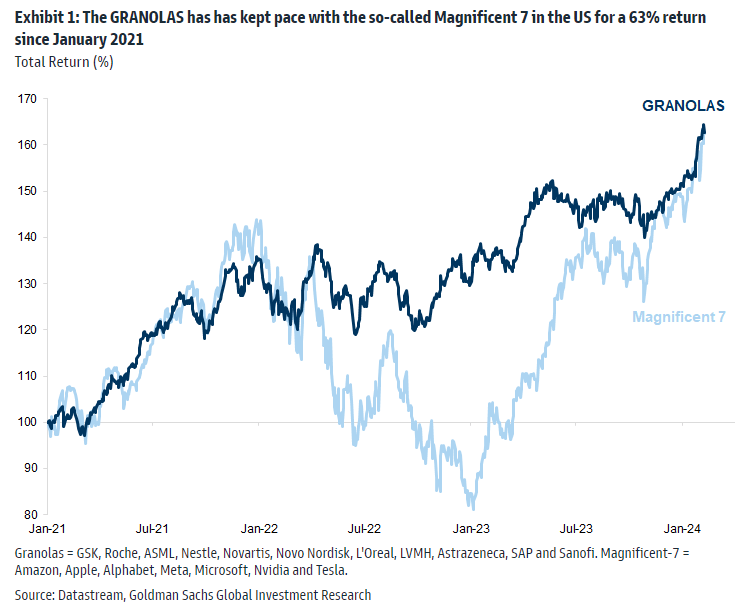

2024 has been another stellar year for semiconductor stocks. But the bullish momentum is not solely focused on chip companies. Firms supplying that AI-fueled niche have taken part in the significant upside so far this year. The broadening global upside trend led analysts at Goldman Sachs to coin “GRANOLAS” stocks (GSK (GSK), Roche (OTCQX:RHHBY)(OTCQX:RHHBF), ASML (NASDAQ:ASML), Nestle (OTCPK:NSRGY)(OTCPK:NSRGF), Novartis (NVS), Novo Nordisk (NVO), L’Oreal (OTCPK:LRLCF)(OTCPK:LRLCY), LVMH (OTCPK:LVMHF)(OTCPK:LVMUY), AstraZeneca (AZN), SAP (SAP), and Sanofi (SNY)), which are all part of high-momentum themes across Europe.

Those equities, along with big domestic players like NVIDIA (NVDA) and Eli Lilly (LLY), are darling names. Today, I’m focusing on ASML (ASML), the third-most valuable company outside the US.

I have a hold rating on the stock. Following a more than 25% return year-to-date through mid-March, the valuation has turned stretched while some technical indicators point to at least a pause in the uptrend.

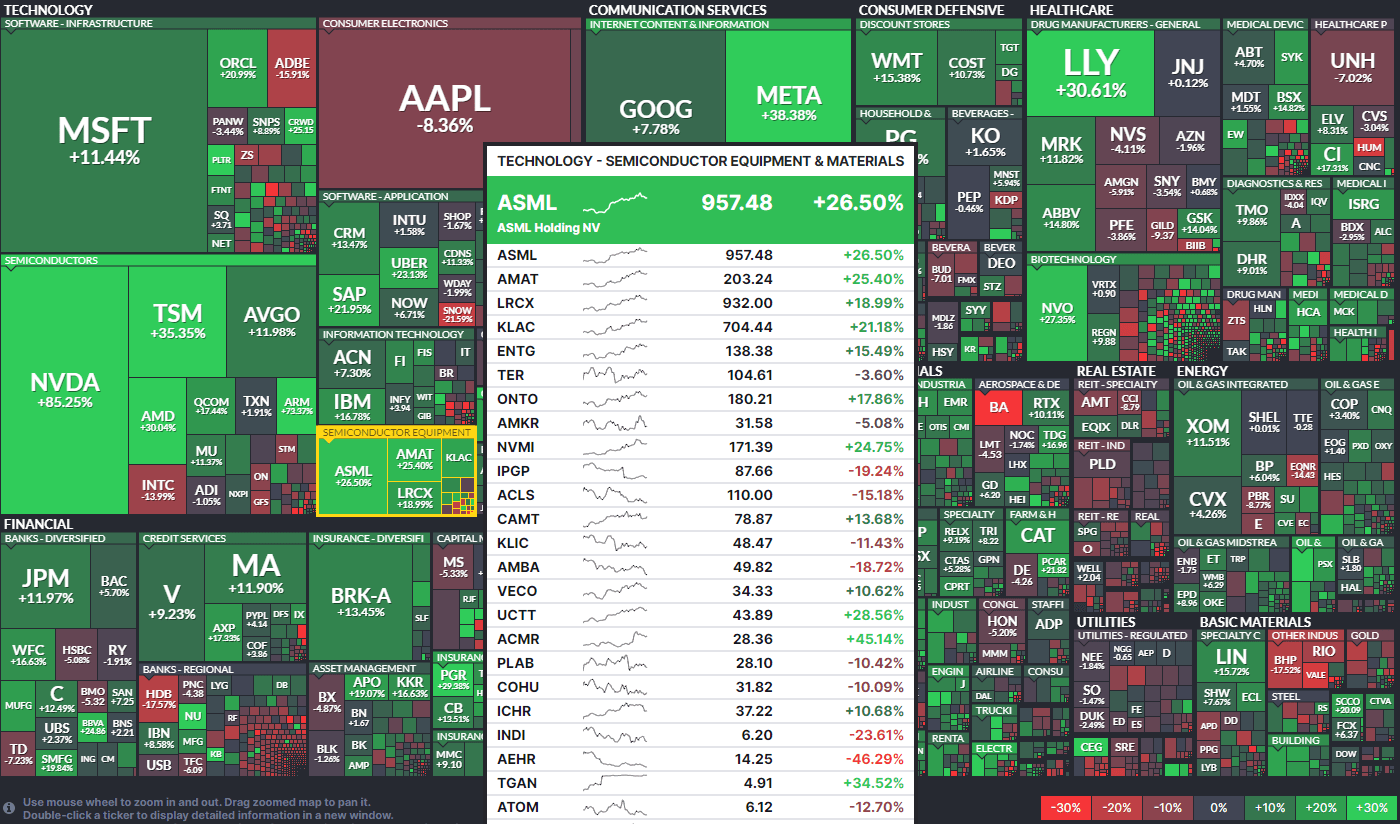

Year-to-Date Global Equity Performance Heat Map: ASML Participates in the Chip Boom

Finviz

European GRANOLAS Stocks Producing Strong Returns

Goldman Sachs

According to Bank of America Global Research, ASML is the market leader in lithography tools, a critical part of the semiconductor manufacturing process enabling ‘Moore’s law’. The company benefits from technological transitions as well as new additions in leading-edge logic and memory chip capacity. ASML currently has a market share of close to 90%, which is a monopoly in next-generation EUV (extreme ultraviolet) lithography.

ASML reported a strong Q4 2023, helping to send the stock to its best one-day gain since 2022. Revenue and EPS verified above forecasts and the company enjoyed strong order intake over the final three months of its fiscal year. EUV orders surged a remarkable 1020% sequentially and were up 65% year-on-year driven by demand for DRAM (Dynamic Random Access Memory) and AI applications.

The management also team confirmed that its order backlog stood at €39 billion at the end of the quarter. That was bullish news, no doubt, but ASML’s guidance was to the soft side, though perhaps the management team was merely trying to temper expectations in a hot industry. The bulls were not concerned as shares rose to all-time highs after the report. Key risks include delays in EUV shipment volume and weaker gross margins as the industry evolves in this upcycle. Any slowdown in global enterprise capex could also hurt the tech company.

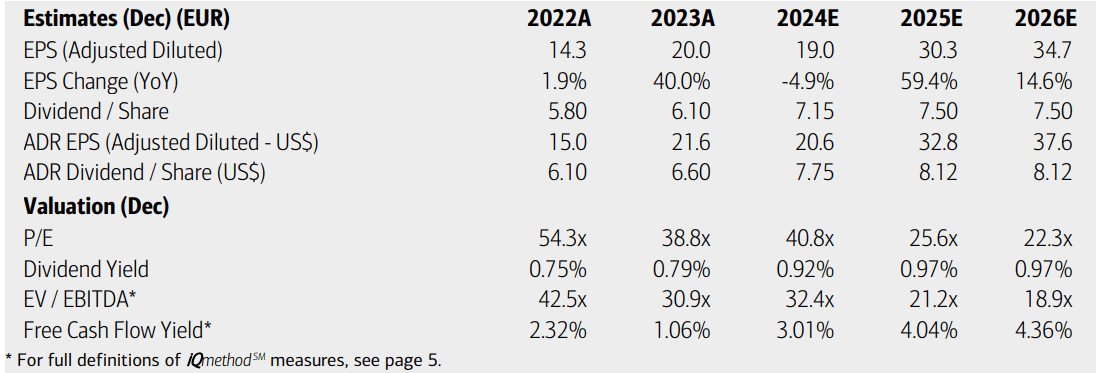

On valuation, analysts at BofA see earnings actually falling fractionally this year before EPS growth is seen as rising sharply in FY 2025. Per-share operating earnings are then expected to continue higher through 2026. The Seeking Alpha consensus forecast shows slightly less than $21 of EPS in ‘24 and $30 in the out year while top-line growth is set to soar in 2025. Dividends, meanwhile, are forecast to remain low – the $367 billion market cap Dutch company pays less than 1% in yield on ADR shares. ASML has a very low free cash flow yield and EV/EBITDA ratio that is currently about 2x that of the S&P 500.

ASML: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

BofA Global Research

If we assume $23 of forward earnings, about the current consensus forecast, and apply the stock’s lofty 38.6 forward P/E multiple, then shares should trade near $890. We can take a PEG ratio approach, too. As it stands, the forward non-GAAP PEG is at a 17% premium to its long-run average. As a whole, valuation metrics appear stretched on this high-momentum ex-US stock.

ASML: Valuation Metrics Stretched Despite Strong 2025 Growth Ahead

Seeking Alpha

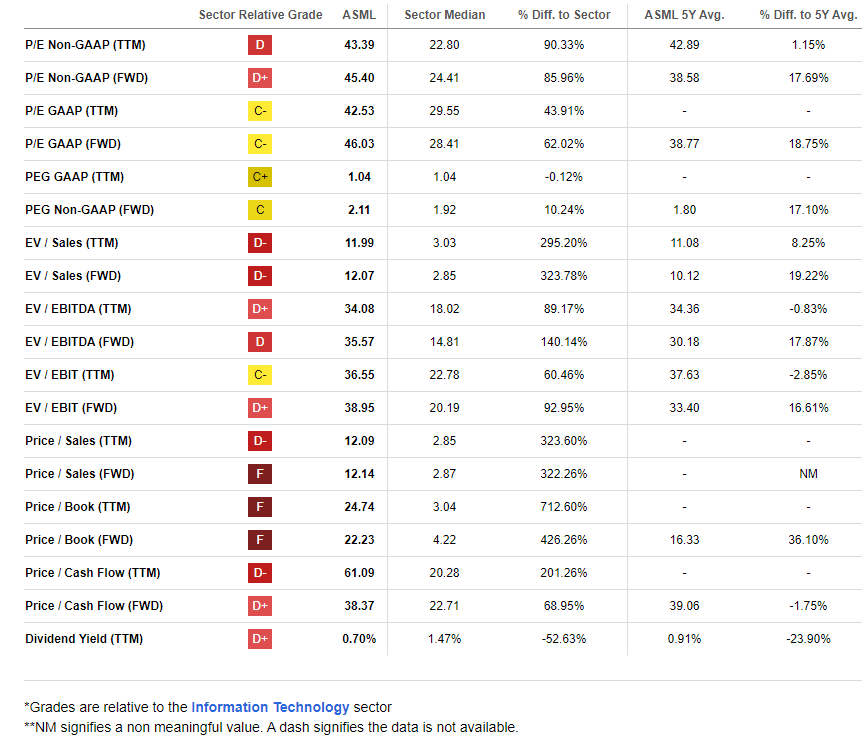

Compared to its peers, ASML features a weak valuation grade, but we must consider high growth prospects over the quarters ahead. If ASML can achieve, say, $36 of EPS in 2026, then it trades with a mere mid-20s P/E. Given that sanguine growth expectation and strong current profitability trends, shares could still be a decent candidate for growth investors.

Share-price momentum, meanwhile, is very strong, and I will highlight key price levels to watch following a long-term technical breakout earlier this year. EPS revisions have been mixed over the past 90 days despite a solid top and bottom-line beat reported back on January 24.

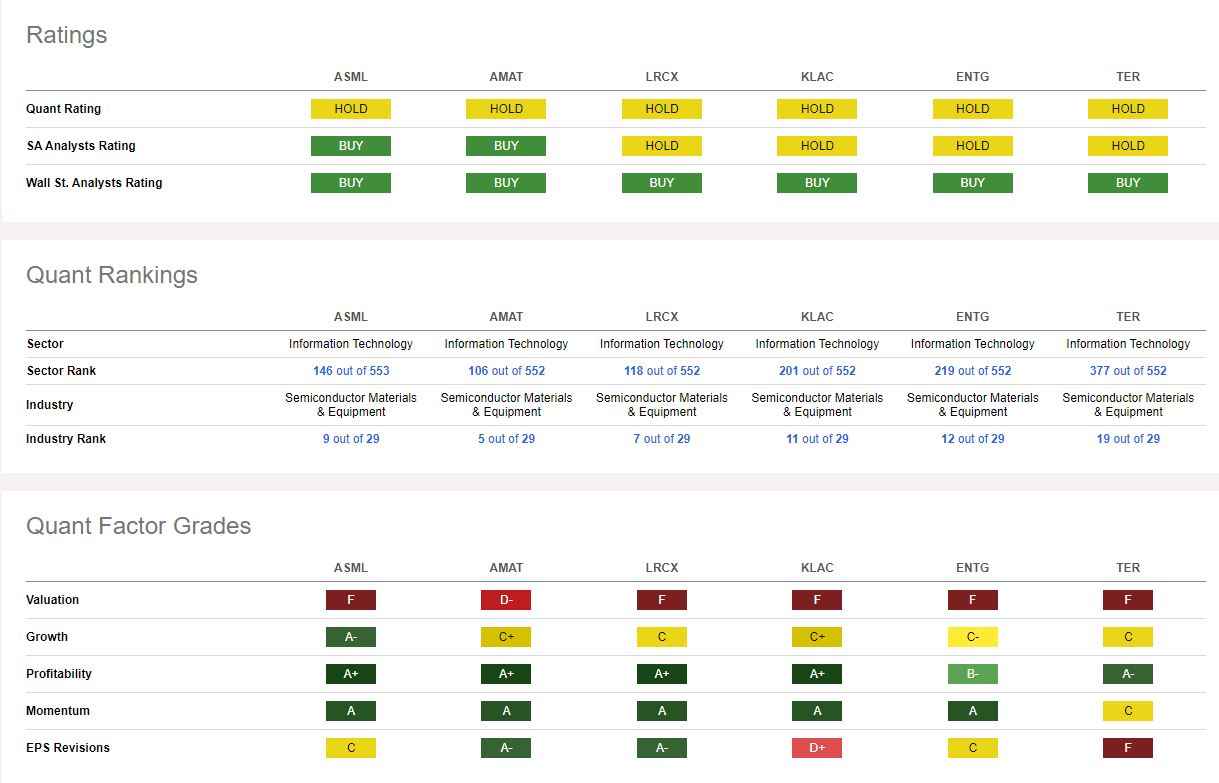

Competitor Analysis

Seeking Alpha

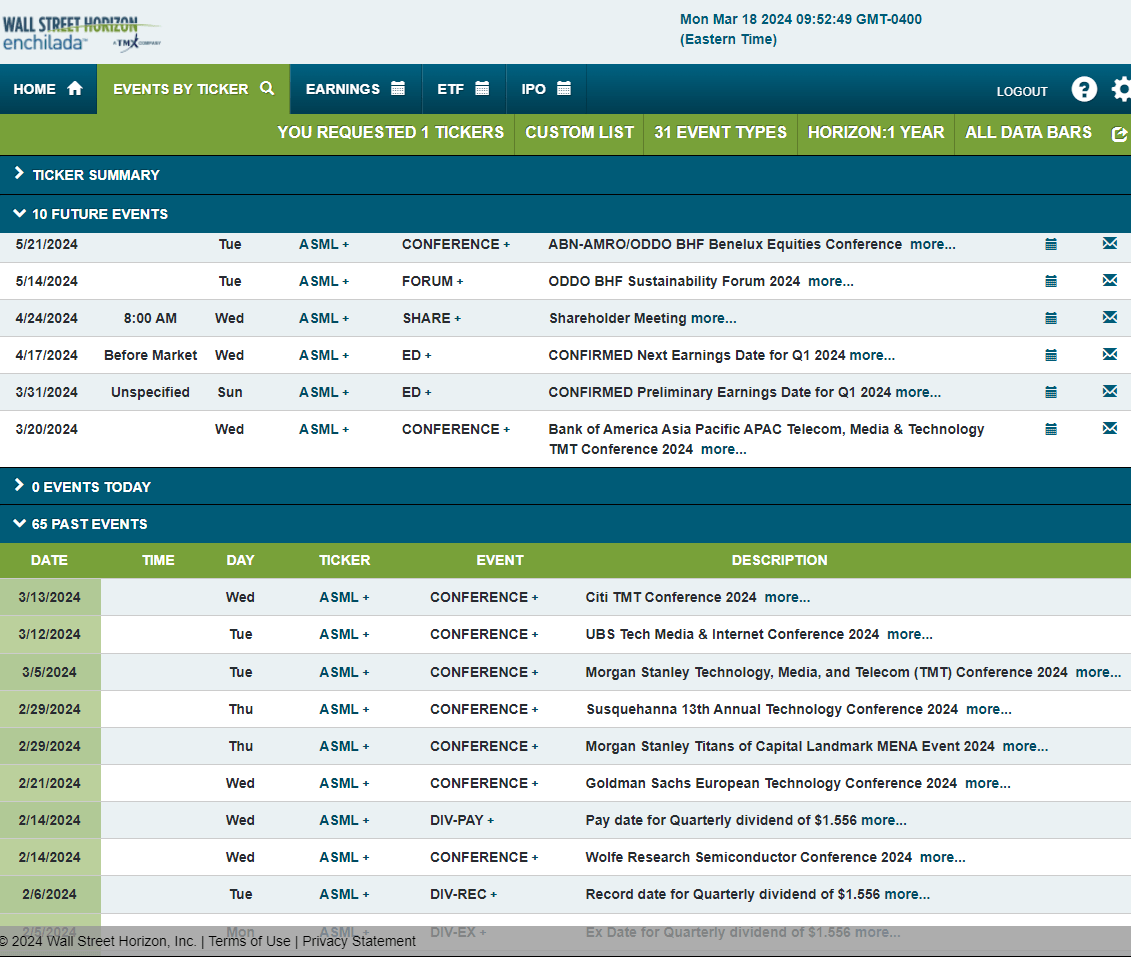

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q1 2024 earnings date of Wednesday, April 17 BMO with a shareholders’ meeting taking place a week later. It is indeed an active event calendar – the firm is slated to present at the Bank of America Asia Pacific APAC Telecom, Media & Technology TMT Conference 2024 in Taiwan this week and a preliminary earnings update should come at the end of Q1.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

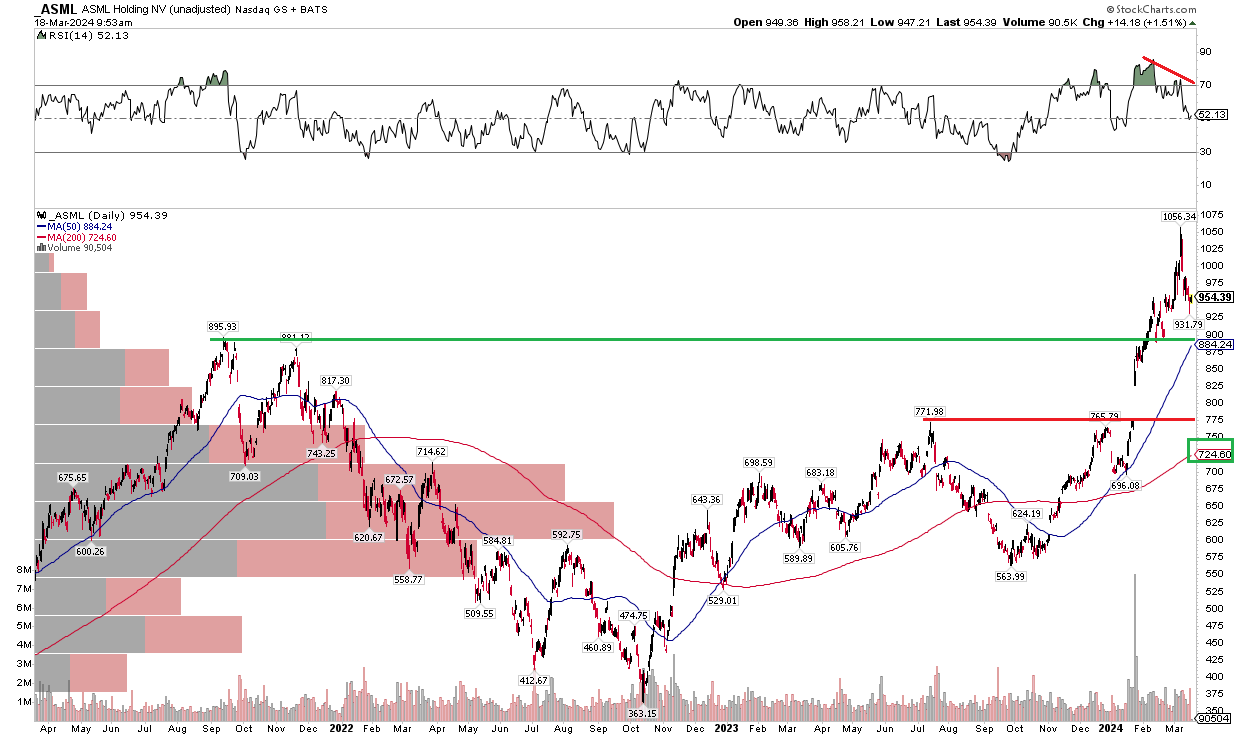

With shares not far from a fair valuation, ASML’s technicals are likewise mixed. Notice in the graph below that a bullish long-term breakout took place immediately after its Q4 2023 earnings date last January. A pronounced rally above the previous all-time high of $896 launched the chip materials & equipment stock to an eventual high above $1050 just a few weeks ago. The last leg of the rally came on relatively weak RSI momentum, however. As price notched fresh highs, the RSI momentum oscillator at the top of the chart made a lower high – otherwise known as bearish divergence.

Also of concern is the earnings-date price gap that lingers just below $800. It’s possible that a correction is underway in the shares, and a pullback to fill that gap could transpire. But that would be an ideal entry point from a technical perspective. With a rising long-term 200-day moving average, and the short-term 50dma well above the 200dma, trend indicators side with the bulls. First support may come about at the 2021 peak just below $900.

Overall, ASML is in an uptrend, but there are cautionary signals as far as the bulls should be concerned.

ASML: ADR Shares Slip Toward Key Support, Bearish RSI Momentum Divergence

Stockcharts.com

The Bottom Line

I have a hold rating on ASML stock. The stock has turned slightly above what I consider to be fair value while technical indicators point to a consolidation over the near term with key support near $800.

Q2 2024 Earnings Call Transcript")