Pixelimage

Trinity Capital (NASDAQ:TRIN) is a well-managed BDC that despite net realized losses in 2023 enjoyed substantial portfolio growth in the last year. The BDC also out-earned its dividend with net investment income as well as fully earned its special dividends paid last year.

Trinity Capital is floating-rate positioned BDC, meaning the BDC should profit from the latest inflation update which showed that inflation is not substantially receding.

I think that Trinity Capital has potential to keep raising its dividend in 2023 and return excess portfolio income to shareholders. With a covered 13% yield, I think the premium valuation is deserved.

My Rating History

After I completed my due diligence last year I acquired Trinity Capital’s stock in October 2023 due to the availability of a low-risk yield of 14% that was covered by net investment income.

The yield has since compressed a bit, but the BDC remains a compelling choice for passive income investors, not least because of its solid fourth quarter results and multiple dividend raises since October.

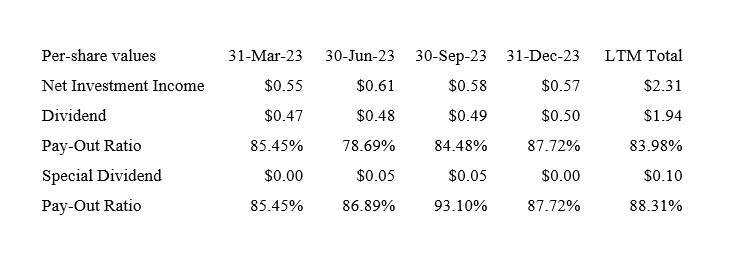

Trinity Capital’s dividend pay-out ratio fell 5 percentage points in the last quarter due to strong net investment income growth related to the BDC’s floating-rate investment portfolio.

Portfolio Review

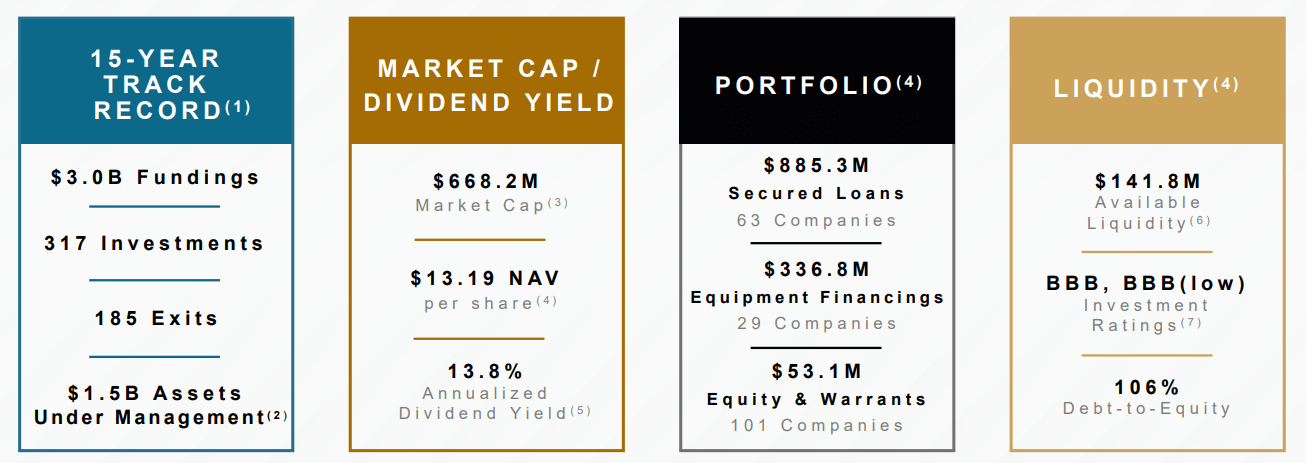

Trinity Capital is an internally-managed, closed-end investment company that is regulated as a BDC. As such, the BDC is required pay at least 90% of its taxable income to stockholders.

Trinity Capital is mainly focused on business loans in the middle-market segment and the provision of capital for the purchase of equipment (machines etc).

Portfolio Overview (Trinity Capital)

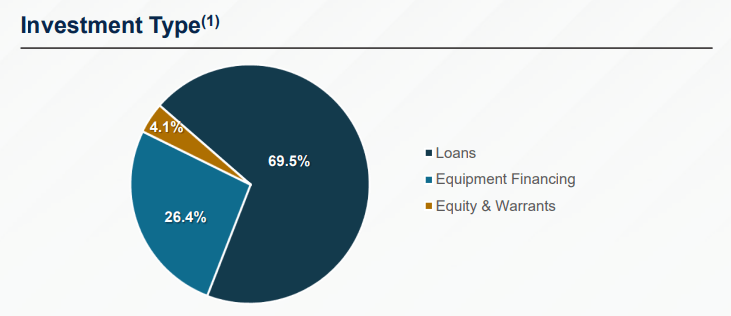

The BDC had secured loans totaling $885.3 million in 4Q-23 which accounted for 70% of investments. Equipment financing, which are unique loans specifically handed out to companies for the acquisition of machines, for instance, accounted for $336.8 million of investments, or 26% of the portfolio total.

Investment Type (Trinity Capital)

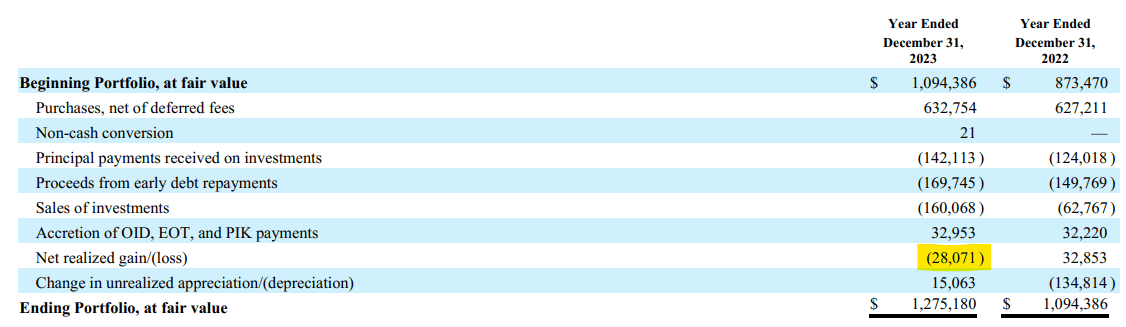

Trinity Capital’s portfolio grew in 2023, despite high interest rates that led to a higher number of loan repayments compared to the prior year. Trinity Capital’s portfolio in 2023 was worth $1.28 billion, up 17% YoY due to robust demand for loan originations.

However, Trinity Capital did see a higher amount of net realized losses in its portfolio in 2023 as well, reducing portfolio value by $28.1 million, compared to a gain of $32.9 million in the prior year.

Net Realized Losses (Trinity Capital)

Trinity Capital experienced robust net investment income tailwinds as 2023 was a good year for business development companies in general, but particularly for those that made at least some floating-rate loan investments.

As of December 31, 2023, 69% of Trinity Capital’s loans, based on principal amount, were floating-rate which obviously helps the BDC in a rising-rate environment, or in an environment in which short-term interest rates remain elevated.

Inflation data for the most recent month showed that consumer prices are still rising, they were up 3.2% YoY in February, which pushes back the central bank’s timeline for rate cuts in 2024. Thus, Trinity Capital should be able to earn a level of net investment income in the short-term that is comparable to the fourth quarter of 2023.

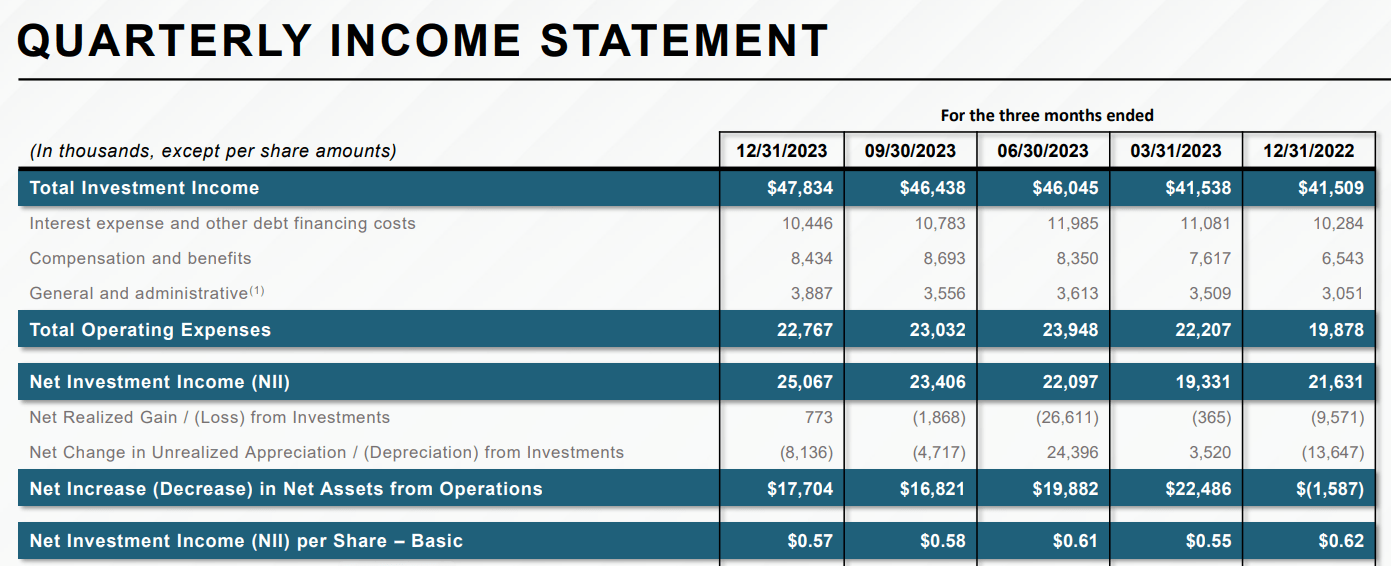

In the fourth quarter, Trinity Capital earned $47.8 million in investment income, up 15% YoY while net investment income (which is total investment income minus the BDC’s operating expenses) was $25.1 million, up 16% YoY.

Trinity Capital grew its portfolio-derived income due to new loans/equipment finances as well as floating-rate tailwinds in 2023. For 2024, I anticipate resilient net investment income as the inflation update suggests the central bank won’t move its position on interest rates for at least a couple of more months, in my view.

Quarterly Income Statement (Trinity Capital)

Dividend Coverage Improved 5 Percentage Points In 4Q-23

Trinity Capital earned $0.57 per share in net investment income in the fourth quarter which compares against a $0.50 per share dividend pay-out. Trinity Capital raised its regular dividend every quarter in 2023 by $0.01 per share and paid special dividends amounting to $0.10 per share (the BDC paid special dividends twice in 2023 in the mount of $0.05 per share for 2Q-23 and 3Q-23).

This leads us to a dividend pay-out ratio of 88% in the fourth quarter. In 2023, Trinity Capital paid out 84% of its net investment income excluding special dividends and 88% including special dividends.

Dividend (Author Created Table Using BDC Information)

Trinity Capital: Quality Has Its Price

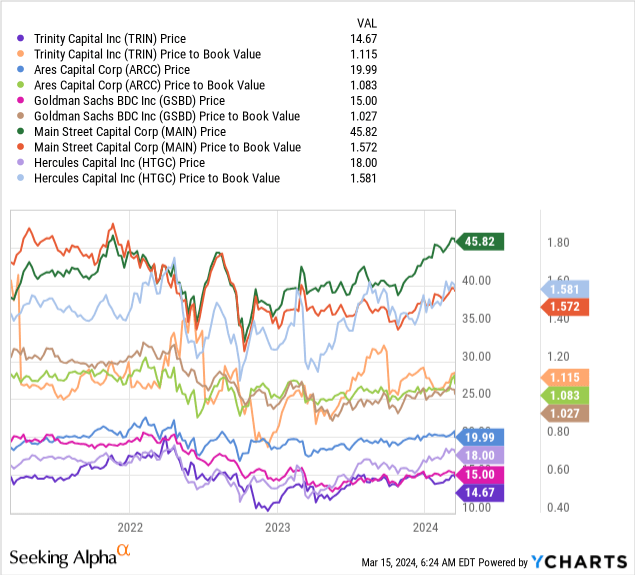

Business development companies that have sufficient net investment income to hike the dividend every quarter in 2023 and that still have a high degree of excess dividend coverage are not surprisingly selling at a premium to net asset value. Trinity Capital’s net asset value as of December 31, 2023 was $13.19 per share, up $0.04 compared to 2022, which means that the BDC’s stock is selling for 1.13x NAV, thus implying a 13% NAV premium.

Only the best-of-breed BDCs get premiums to net asset value including Ares Capital (ARCC), Main Street Capital (MAIN) and Hercules Capital (HTGC). All three BDCs have produced reliable business results for stockholders in the last few years which has resulted in passive income investors rewarding this consistency with a premium valuation.

I think Trinity Capital’s premium NAV is deserved given its multiple dividend raises in the last year. With net investment income tailwinds not yet tailing off, I think we could see a new round of dividend hikes in 2024.

Why The Investment Thesis Might Fail

Trinity Capital has built a moderate floating-rate posture which obviously leads to net investment income tailwinds as long as short-term interest rates stay where they are. A reversal in the central bank’s attitude on interest rates should make the BDC’s prospects for NII gains less compelling in a low-rate environment.

Furthermore, Trinity Capital’s excess dividend coverage may soften in the latter half of 2024, if the central bank starts to slash rates, limiting, potentially, the outlook for incremental dividend raises.

My Conclusion

Trinity Capital is a well-managed BDC and its floating-rate posture and strong originations have paid dividends for the BDC, literally.

The most recent inflation update for February shows surprisingly resilient inflation, with inflation stubbornly staying above 3%, which should turn out to be a tailwind for Trinity Capital’s large floating-rate senior secured investment portfolio.

The degree of excess dividend coverage is also something that I think has a lot of value for passive income investors in 2024 and it could point to more dividend hikes in 2024.

Trinity Capital is selling at a premium to net asset value, presently 13%, but the premium might be worth it if Trinity Capital continues to raise its dividend pay-out this year.

Quality always has its price and Trinity Capital definitely fits the mold.

Q2 2024 Earnings Call Transcript")