Suphanat Khumsap/iStock via Getty Images

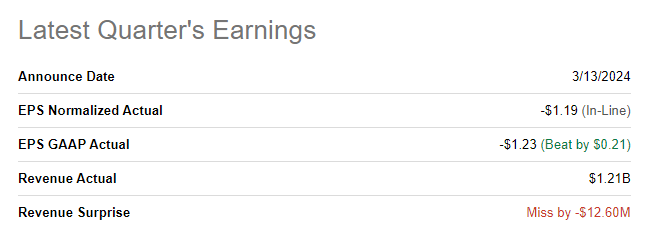

Shipping logistics provider ZIM Integrated Shipping Services (NYSE:ZIM) reported earnings for the fourth quarter last week that met average investor expectations in terms of adjusted earnings. The company also expectedly reported a large net loss for FY 2023 as the global shipping industry is going through a correction and has suffered, throughout the year, a precipitous decline in cargo freight rates. Although ZIM Integrated Shipping Services is suffering from challenging market conditions, I believe that the recent rebound in shipping rates is a very favorable development that could help the company report stronger earnings and free cash flow in the short term. ZIM is cheap based off of free cash flow and could easily double if the shipping market stabilizes and recent freight rate gains can be sustained!

Previous rating

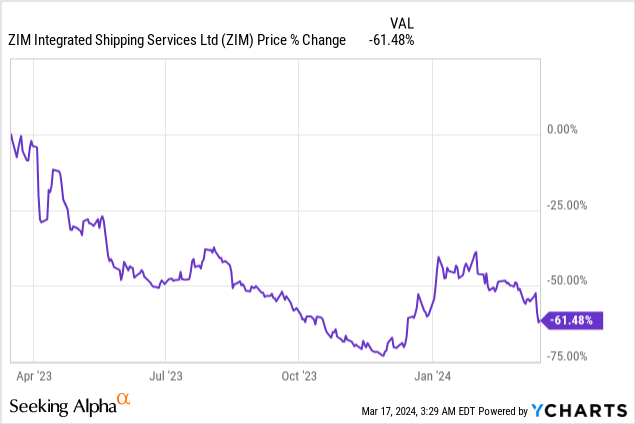

Despite escalating attacks on shipping routes in the Red Sea, I upgraded ZIM Integrated Shipping Services in December to buy due to the company’s significant short squeeze potential. After ZIM Integrated Shipping Services eliminated its dividend in FY 2023, the market has turned noticeably bearish on the shipping company. Shares soared in December and January, reflecting an improvement in the pricing environment, but have recently fallen back below $10 again… which translates to a favorable risk profile, in my opinion.

Rebound in shipping rates could change the game for ZIM in 2024

ZIM Integrated Shipping Services reported results for the fourth quarter last week that largely met average investor expectations. The shipping company achieved revenues of $1.21B, showing a year-over-year decline of 45%. However, revenues came in only slightly ($12.6M) below consensus expectations. In terms of adjusted earnings, the company met expectations and reported a loss of $1.19 per share.

Seeking Alpha

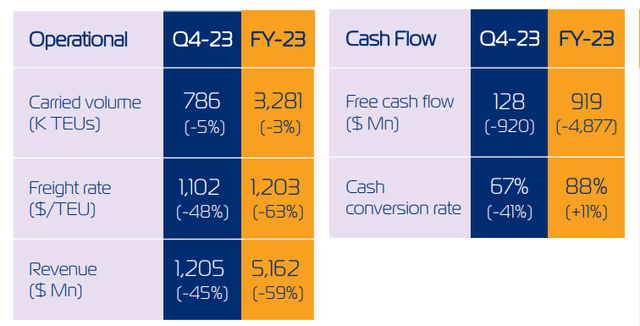

ZIM Integrated Shipping Services has suffered from a steep decline in freight rates in the last year which caused a major revenue contraction as well as a significant drop-off in earnings and free cash flow. The firm’s average freight rate per twenty-foot container in Q4’23 was $1,102, showing a year-over-year decline of 48%. The decline in shipping rates due to slowing demand for shipping logistics providers in a post-pandemic world has been a major headache for companies like ZIM Integrated Shipping Services.

ZIM Integrated Shipping Services generated a $147M net loss in Q4’23 and a full-year net loss of a massive $2.8B. The firm’s free cash flow accomplishments didn’t look much better: ZIM’s free cash flow declined by $920M year over year in Q4’23 and fell to only $128M. Total FY 2023 free cash flow was $919M, still positive, but also showing a Y/Y drop-off of $4.9B.

ZIM Integrated Shipping Services

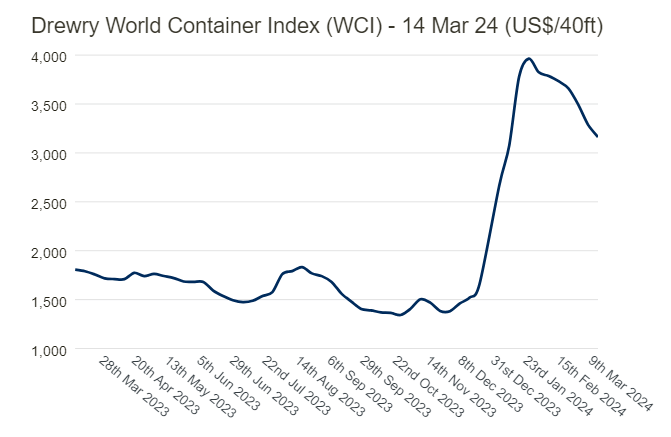

One favorable development in the fourth quarter, and one reason why I am still bullish on the shipping logistics provider is that shipping rates started to climb sharply higher at the end of Q4’23. This uptick in shipping rates is directly related to Houthi attacks on container shipping lanes in the Red Sea. A number of container companies, including Maersk (OTCPK:AMKBF), said that they would reroute their container ships in response to a changing risk matrix in the Red Sea. The longer time required for certain transits as well as higher costs associated with longer transit times have led to a surge in freight pricing.

At the beginning of the year, according to the Drewry World Container Index, shipping rates soared to almost $4,000 for a 40-foot container. Rates have since corrected a bit, as is normal after such a drastic rise in prices in a short period of time, and shipping a standard 40-foot container now costs $3,162, showing a decline of 4% week over week. The massive rebound in shipping rates should help boost profitability for container shipping companies, including ZIM Integrated Shipping Services in FY 2024.

Drewry World Container Index

ZIM Integrated Shipping Services’ valuation

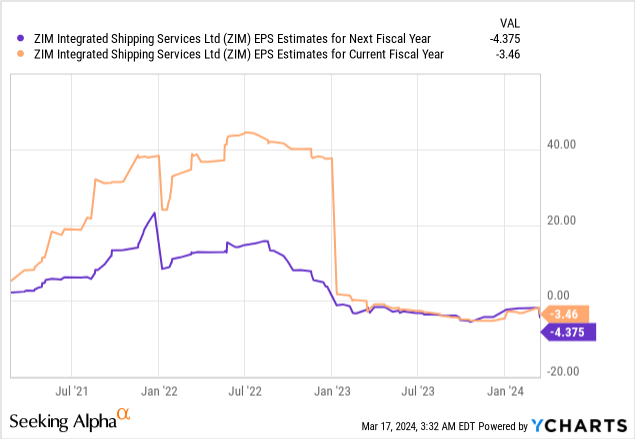

EPS estimates for ZIM Integrated Shipping Services are still negative and indicate that the market appears to expect a recession. The firm’s outlook itself projects an up to $300M adjusted EBIT loss in FY 2024. However, I believe that if the world economy avoids a recession in 2024 and freight rates flatten out at the current level of $3,000/container, ZIM Integrated Shipping Services is facing significantly improved short-term earnings and free cash flow prospects. Currently, analysts expect negative EPS for this year and next year, but the uptrend in freight rates could change this narrative, especially if the price for container shipping remains elevated due to a permanently increased risk profile in the Red Sea.

Although FY 2023 was a challenging year for ZIM, it is a major positive that the shipping company, despite those challenges, managed to generate positive free cash flow.

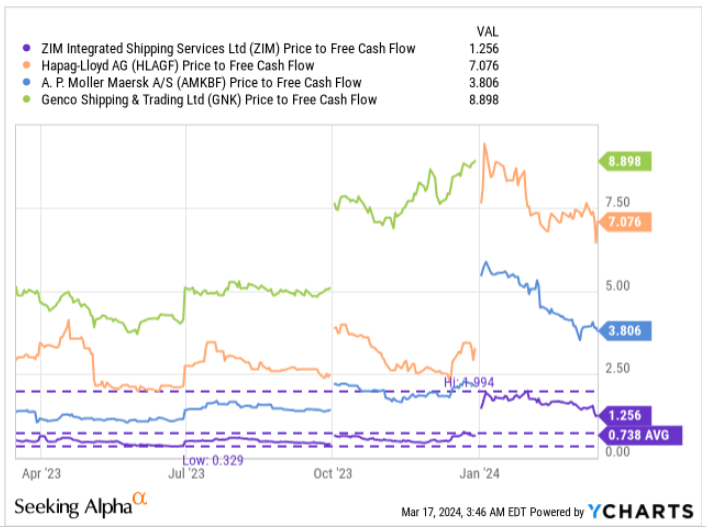

Shares of ZIM Integrated Shipping Services are currently trading at P/FCF ratio of 1.27X, which is above the 1-year average free cash flow multiplier of 0.74X. The low P/FCF average ratio was chiefly driven by overly pessimistic expectations about the shipping industry in FY 2023 which is when freight rates consistently trended lower.

With rates resetting higher to reflect a changed risk matrix, ZIM has considerable revaluation potential in FY 2024, in my opinion. Hapag-Lloyd (OTCPK:HLAGF), Maersk, and Genco Shipping (GNK) all trade at significantly higher P/FCF ratios with the industry group average P/FCF ratio being 5.3X. ZIM is likely trading at a much lower P/FCF ratio relative to rivals due to Houthi rebels specifically targeting Israeli-bound sea traffic.

I believe that even under consideration of a risk discount due to ZIM’s operations being headquartered in the Middle East, shares could easily trade at 2.5-3.0X free cash flow under the condition that shipping rates remain around the $3,000 price level. This implies a potential fair value range of $18.80-22.60 and revaluation potential of up to 139%.

YCharts

Risks in ZIM Integrated Shipping Services

The biggest risk for ZIM Integrated Shipping Services right now is the potential for targeted attacks on Israeli container ships in the Red Sea and in the Middle East. Additionally, the container shipping industry has benefited from an uptick in shipping rates at the beginning of the year. If the pricing situation reversed and the shipping industry had to deal with lower freight rates again, then ZIM’s earnings and free cash flow prospects would obviously deteriorate.

Final thoughts

ZIM Integrated Shipping Services ended a bad year with a bad quarter. The shipping company saw a $4.97B drop-off in free cash flow in FY 2023, which is a stunning sum of money. However, ZIM Integrated Shipping Services still earned positive free cash flow in both Q4 and FY 2023, despite massive macro and pricing headwinds in the industry. The recent uptick in shipping rates for container ships is a positive for ZIM Integrated Shipping Services and one of the reasons, combined with an attractive valuation profile, why I am standing by my buy rating!

Q2 2024 Earnings Call Transcript")