halbergman

Co-authored by Treading Softly.

Finding a home is an important step for every person. The ability to find a place to live is essential to be able to establish a home base that you then operate from, whether you’re going to work, whether it’s a place to simply cook a meal or to lay your head at night in sleep. The issue that so much of the housing market is seeing right now is that there’s a massive majority of homeowners who are locked in at extremely low interest rates that occurred during the COVID crisis. Now interest rates are significantly higher and homeowners are disinclined to sell because they’re not interested in paying the currently higher interest rates. This creates an affordability issue where the homes that are coming to market are largely unable to be afforded by the average person because they’re priced too high or interest rates are making the mortgage too expensive.

Because of this, it is creating an environment where people want homes, but there aren’t homes available. And the people who want homes aren’t always able to afford what is available because of the interest rates that are pressing down on them and the inflation-rising costs of everything in their lives. When it comes to the market, housing affordability isn’t as big of an issue for the average investor as it is for the average person. However, some companies allow you to benefit from this tension that exists currently.

Today, I want to look at two different ways that you can invest and receive strong income from those who are currently deciding to stay put in their home and simply pay their mortgage and from those who need an affordable place to live by the companies that are meeting those needs head-on.

Let’s dive in!

Pick #1: NLY – Yield 13.3%

Annaly Capital Management, Inc. (NLY) positively surprised the market with Earnings Available for Distribution at $0.68, up from $0.66 the prior quarter. Book value rose to $19.44, and in the earnings call management disclosed that book value was up approximately 2% in January, putting current book value somewhere around $19.80. NLY is trading at roughly a 5% discount to tangible book value.

In Q4, NLY focused on rotating up in coupon and has focused primarily on 30-year mortgages. Source.

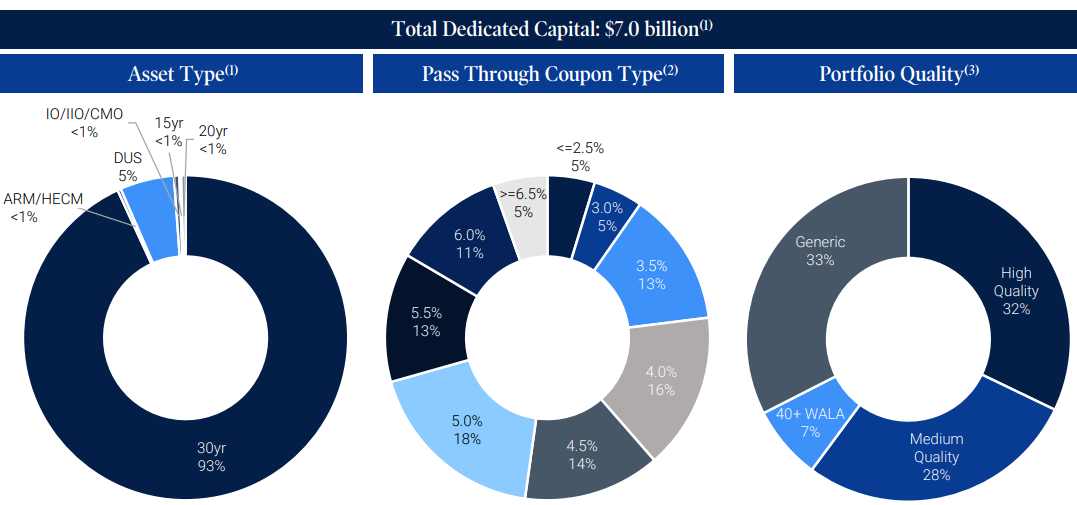

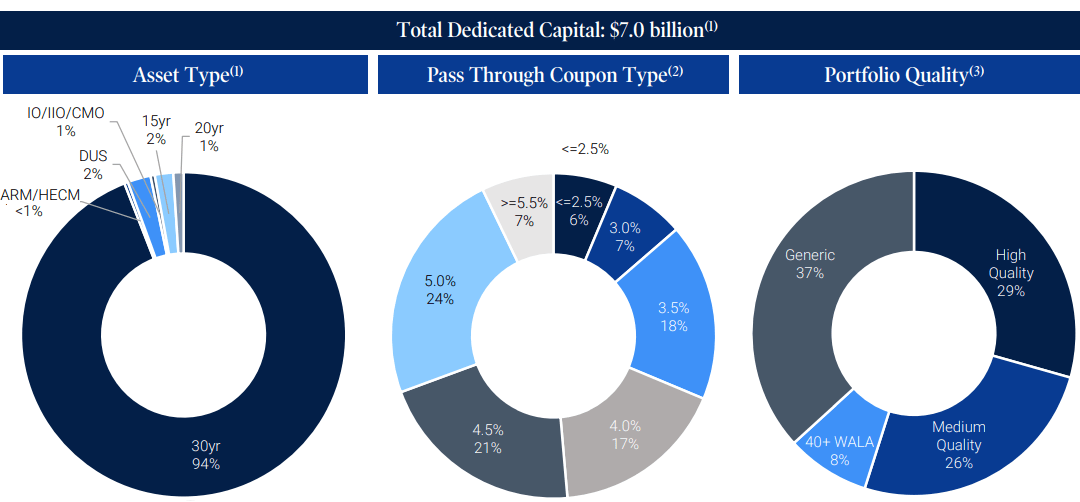

NLY Q4 2023 Investor Presentation

Approximately 47% of its agency MBS has a 5% or higher coupon. When we look year over year, we can see that in 2022 NLY ended with only 37% of its portfolio in 5%+ coupons. Source.

NLY Q4 2022 Investor Presentation

Additionally, there has been a slower migration to higher quality. Note that with agency MBS the “quality” is not measured by default risk, rather buyers can choose between “generic” pools of loans and “specified” pools of loans. The difference is that “specified” pools have characteristics that reduce the likelihood that they are prepaid. NLY wants to get paid the higher coupons for as long as possible. Buying specified pools is usually done at a premium to generic pools.

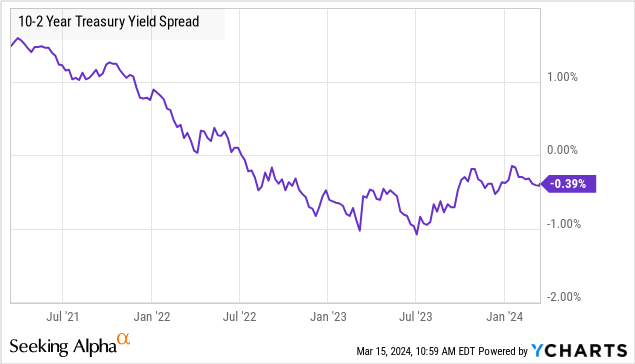

The yield curve is inverted, and it has been inverted for 1.5 years, making this the longest yield curve inversion since the 1980s. This has been a challenge for the agency mREIT business model which is to borrow short term and lend long term.

The inversion has gotten a lot more shallow, but will likely continue until the Fed actually cuts rates:

There are a few methods mREITs can use to hedge against this issue. NLY has chosen to primarily rely on interest-rate swaps. As a result, its financing costs have risen at a slower pace than the coupon it receives. The primary reason NLY’s EAD has declined over the past year has been interest rate swaps ending and coming off the books driving up interest expense.

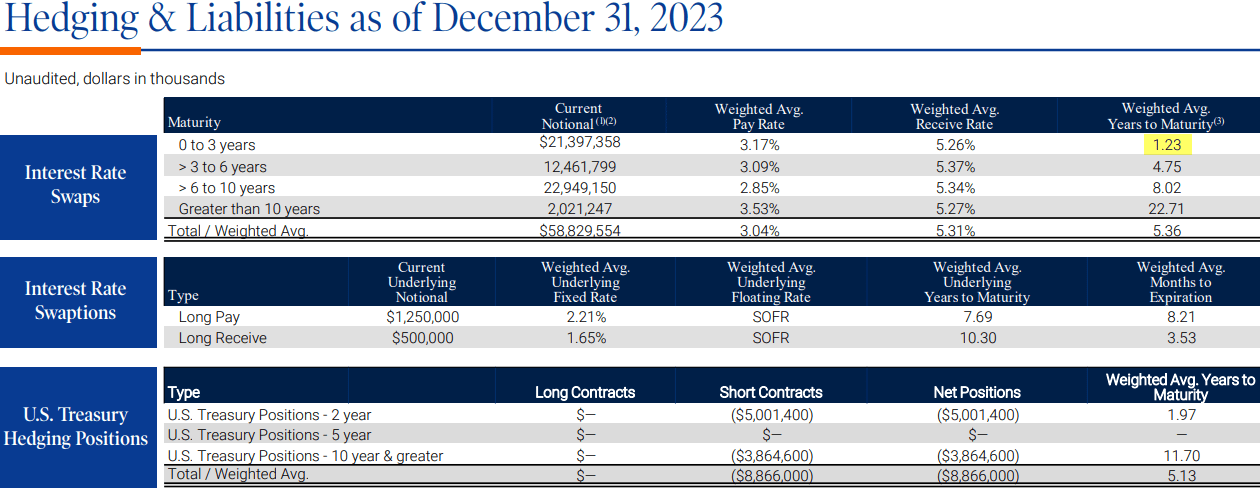

For NLY’s remaining swaps, they have an average life of over 5 years. Source.

NLY Q4 2023 Supplement

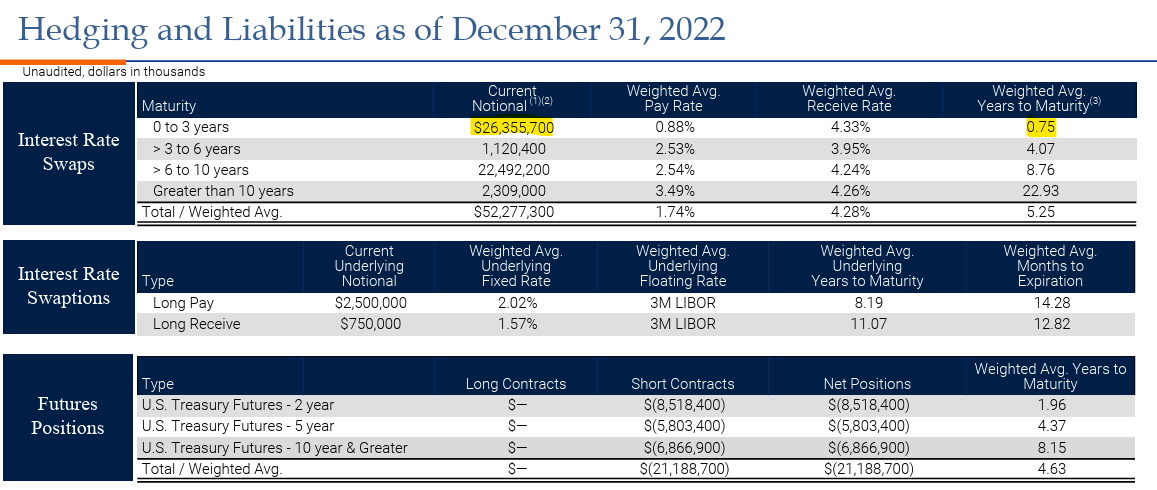

About 36% of them mature within 3 years, and that group on average matures in 1.23 years. This provides a reasonable runway for NLY as the Fed is widely expected to start cutting rates sometime this year. If we go back to December 2022, we can see that NLY had $26 billion in swaps with a weighted maturity of just 0.75 years. Source.

NLY Q4 2022 Supplement

So where we saw a fairly aggressive increase in interest expense for NLY throughout 2023, we can expect that trend to be much more mild in 2024. This will give NLY an opportunity to keep rotating up in coupon, so even as the yield curve might be inverted, NLY’s yield received remains higher than the rate it is paying on debt.

NLY is operating at only 5.7x leverage, which is well below its historical averages. When asked what it would take for NLY to leverage up to increase earnings, CEO Finkelstein said:

“Sure. Give us rate cuts, give us no QT, give us stability around the world and we’ll certainly raise leverage. But look at the end of the day here, if you look at our spread shocks, if we do experience spread tightening, we’re still going to get very good returns as we saw in the latter half of last quarter, just in terms of the overall model, we are generating a more stable return with less leverage than what a mono-line agency firm would deliver and we feel very good about it.

Now to the extent there are some real green shoots out there as it relates to volatility in the market. Yes, we can increase leverage if spreads are attractive. And to the extent that we get a widening in spreads, we have ample liquidity and in the balance sheet to allow leverage to organically increase without having to worry about selling to manage our leverage.

So it’s a really good position to be in right here, Doug. But to the extent things do change for the better and the market is priced to that soft landing scenario, it’s priced perfection across all assets with possible exception of some mortgage related assets. So, we’re a little bit cautious here, but that could change.”

The yield curve has been inverted for a very long time, and the Fed’s inability to provide accurate guidance to the market hasn’t helped. The market remains extremely uncertain about what the Fed is going to do and when. NLY is sitting in a position where it can wait comfortably, with plenty of dry powder to deploy when management believes conditions are ripe.

Pick #2: GHI – Yield 9.2%

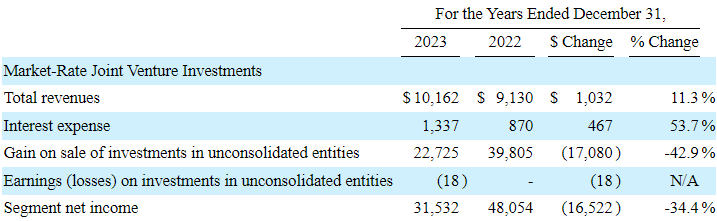

Greystone Housing Impact Investors LP (GHI) is a partnership that issues a K-1 and is involved in two distinct businesses: Investing in mortgage revenue bonds and developing multifamily properties. This dual approach has proven invaluable, as being a bond fund hasn’t been the best place to be the past few years. GHI‘s development business stepped up, covering the regular distribution and providing investors like us with many supplemental distributions. In fact, management announced another $0.07 supplemental distribution for Q1 2024.

For the year, GHI produced $2.07 in net income, and $1.93 in CAD (cash available for distribution) – the number we consider the most important. CAD easily covered GHI’s $1.69/unit distribution.

GHI previously owned some operating properties as well but sold its final one in Q4, simplifying its business.

Let’s take a look at each business segment:

Mortgage Revenue Bonds

GHI’s MRB business is a spread-based investment. GHI invests in bonds that pay interest, while simultaneously borrowing. It then profits from the difference between its revenues and costs. Source.

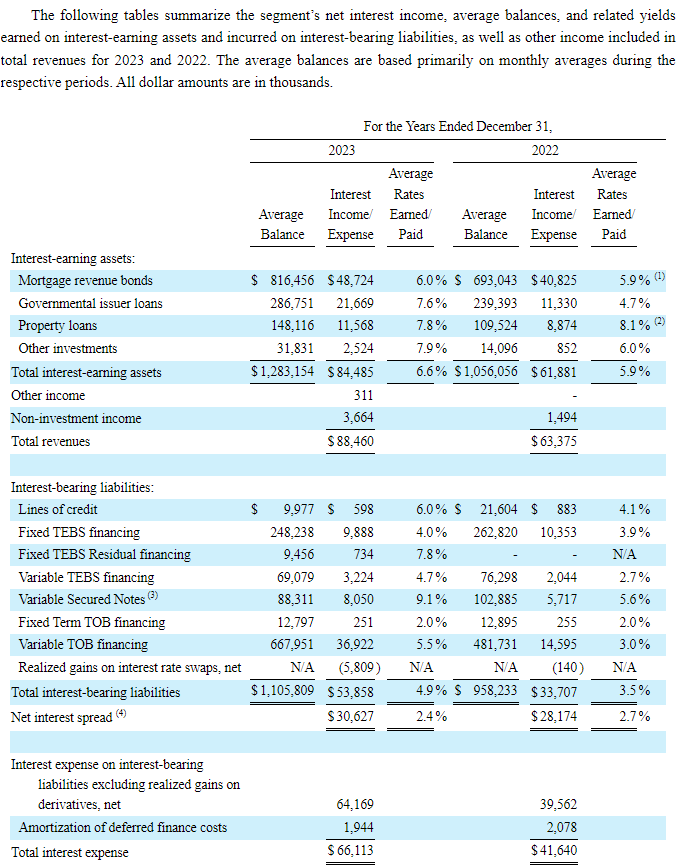

GHI 2024 10-K

Note that GHI deployed capital and increased interest-earning assets from $1.05 billion to $1.28 billion. However, higher interest expenses limited the benefit to the bottom line. GHI ended the year with about an 8.7% improvement in net interest spread earnings.

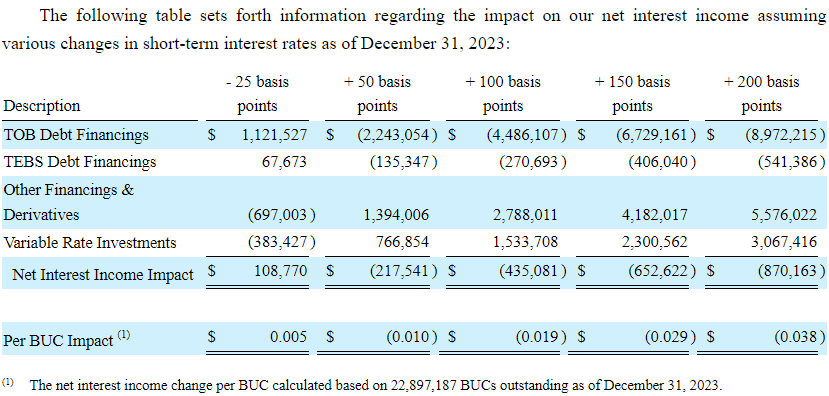

GHI uses various hedges, but overall is positioned to benefit from declining interest rates. Every 50 bps in interest rate changes will impact net interest income by approximately $0.01/unit. Higher rates have led to lower earnings, and lower rates will lead to higher earnings.

GHI 2024 10-K

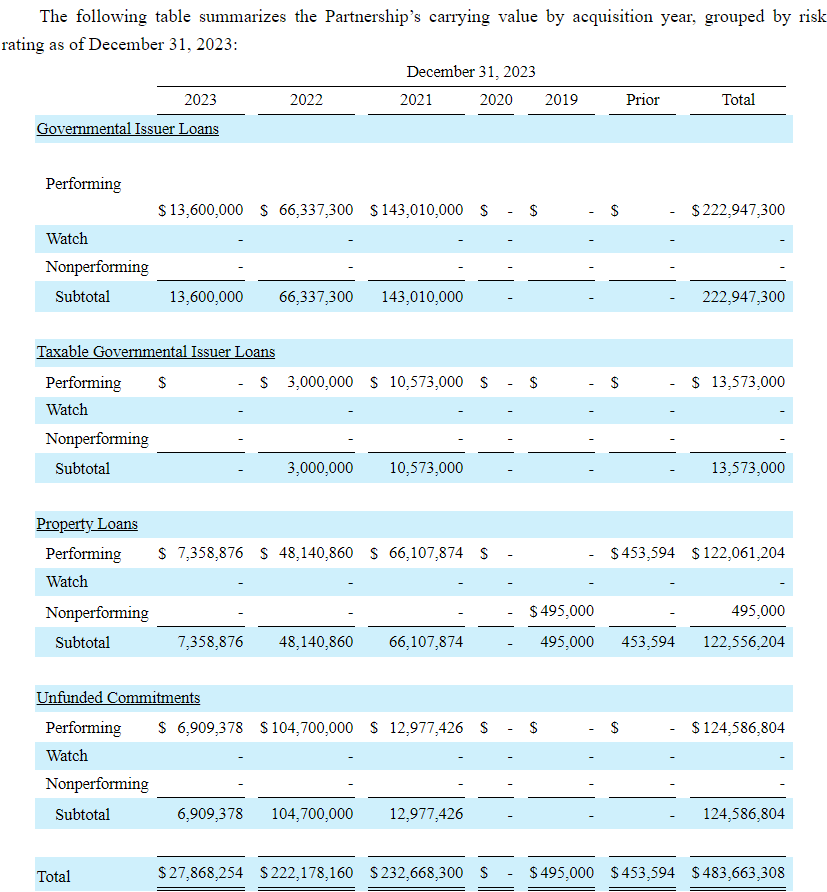

In terms of credit quality, GHI has seen some defaults over the years. In fact, the property they sold in Q4 was a property that defaulted and GHI foreclosed on and operated for many years before selling for a gain.

Currently, GHI has only one loan that is non-performing, which makes up 0.1% of its portfolio:

GHI 2024 10-K

As interest rates decline, we expect that this portion of GHI’s portfolio will experience better performance. Especially since GHI has taken advantage of high rates to increase the size of its portfolio, and it will have the option to refinance at lower interest rates for its own debt when rates decline.

Note that the interest from these bonds is federal tax-exempt – a benefit that is passed along to investors through the partnership structure. The portion of the annual distribution tied to these earnings will be tax-exempt.

Development

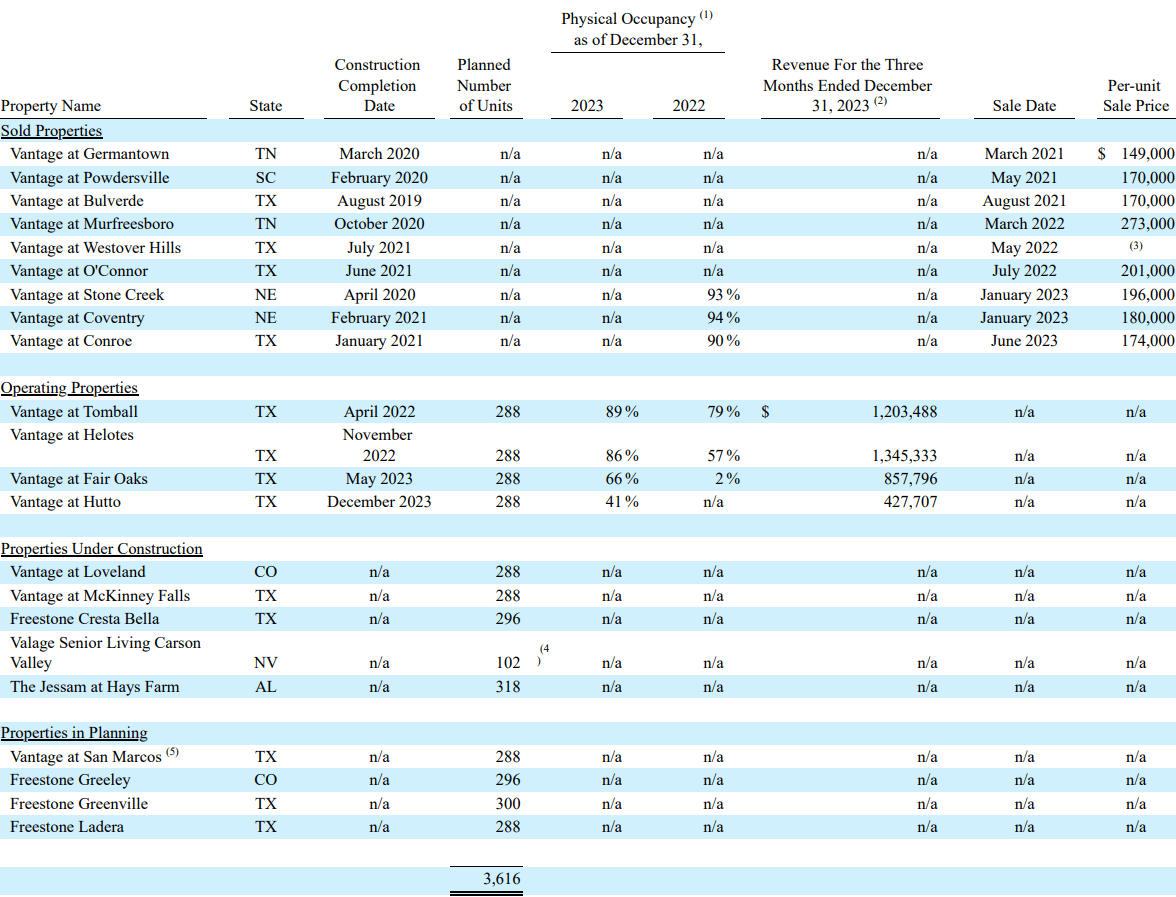

GHI’s development segment was previously a single JV (Joint Venture), the “Vantage JV” where GHI served as the capital provider, typically getting a preferred equity interest in the development. The partner would build and operate the apartment building and, once occupancy was stabilized, sell it for a gain. GHI collects a portion of the profits when the buildings are cash-flow positive, but then gets a larger payout when the building is sold.

The result is large, but often lumpy gains for GHI. This is why management has adopted the practice of distributing “supplementals” rather than raising the regular distribution. The timing and size of gains is not dependable enough to completely rely on them for a quarterly distribution.

Those of us who have held GHI for several years can tell you that it is a lot of fun collecting those supplements and specials! Lately, the supplementals have been paid in additional shares, which increases the income from our holding.

In 2023, sales were lower relative to 2022, but still provided a very meaningful return for GHI:

GHI 2024 10-K

This strategy has been working so well for GHI that it has grown its pipeline. GHI has four properties where construction is complete and they could be sold this year. It sold three in 2023.

GHI 2024 10-K

There are another five properties that are under construction and four that are in the planning stages. GHI has expanded beyond just the Vantage JV, starting two other JVs with a similar business plan.

Coming Together

For the past several years, the story for GHI has seemed to be that only one segment could be outperforming at a time. In 2020, no properties were sold from their Vantage JV. It was decided that the market was too poor and there was no reason to sell at poor prices. As a result, GHI leaned entirely on the MRB segment for all of its earnings.

In 2022 and 2023, it was a tough period for bonds. Prices dropped, and the cost of borrowing was going up, putting pressure on spreads. GHI leaned heavily on its Vantage JV, and it didn’t disappoint.

Today, our outlook is that interest rates are done climbing and could start declining in the second half of the year – this should help improve performance in GHI’s MRB business. Meanwhile, real estate prices have gotten softer, but GHI has a larger pipeline. They will have the ability in 2024 and 2025 to make up for lower gains from individual properties with more volume.

In short, GHI is likely to see both of its segments improve in 2024, and going into 2025, we could see both segments knocking the ball out of the park at the same time.

Conclusion

When it comes to investing in the housing market, I prefer to be a debt holder rather than an active participant as far as building homes or issuing new mortgages. For this reason, I avoid companies that originate mortgages and look for companies that simply hold them and collect the interest and benefit from them. For this reason, I love NLY and its ability to simply hold a vast array of mortgages and enjoy the money that is coming in from them.

I also enjoy my holdings in GHI because it is involved in funding affordable homes being built and enjoying tax benefits because of that while also building multifamily facilities and being able to fill them with new residents and sell them off for profit. Both opportunities provide us a way to benefit from the current housing situation but also be able to support avenues that allow people to have homes, whether they stay in their current home or get a new one.

When it comes to retirement, the last thing I want to do is have to try and figure out where I can get money from regularly. Owning investments that benefit from long-term mortgages provides me with a long-term runway of income – whether this is a mortgage revenue bond or Agency MBS. That way, the only thing I have to worry about with my retirement is what I’m going to have for dinner tonight at my home or if I’m going to go to a restaurant, whether my holidays are going to be spent with my children or with just my spouse. Being able to solve the big issues of life allows me to enjoy the finer moments.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Q2 2024 Earnings Call Transcript")