icholakov/iStock Editorial via Getty Images

At the onset of the Covid-19 pandemic, cruise line equities suffered immensely as these companies were forced to take on loads of debt to remain afloat. One of these equities is Carnival Corporation & plc (NYSE:CCL) which is still down more than 60% since Covid lockdowns forced cruises to stop. That said, the pandemic woes are now a thing of the past as the cruise line industry is on track to have its busiest year ever in 2024. Considering Carnival’s leading market share in the cruise line industry, I expect the company to post a net income nearly triple management’s forecast this year. As such, I’m rating Carnival as a buy with a price target of $23.95 per share, implying 47% upside.

Industry Outlook

According to the Cruise Lines International Association, the cruise line industry reached 106% of 2019 levels in 2023 with 31.5 million passengers sailing. That figure is expected to increase to 36 million passengers this year which would represent a 20% increase from 2019 levels. As such, it’s safe to say that the cruise line industry is finally on the right track to resume its growth that was halted by the Covid-19 pandemic.

I believe this is favorable to Carnival due to its leading market share in the cruise line industry. In 2023, 12.5 million passengers sailed on Carnival’s cruises. This means that 40% of cruisers in 2023 were sailing with Carnival. In comparison, 6 million passengers took a Royal Caribbean (RCL) cruise and 2.7 million passengers were on a Norwegian Cruise Line (NCLH) cruise, good for a 19% and 9% market share for Carnival’s competitors.

Considering the industry’s passenger forecast in 2024, Carnival’s passengers this year can be projected to be 14.4 million, while Royal Caribbean and Norwegian’s passengers can be projected to be 6.8 million and 3 million, respectively.

My Estimates

Knowing Carnival’s projected passengers this year, I’ll be providing my estimates for the cruise line’s revenues and EPS. In terms of revenue, Carnival generates revenues from ticket sales and passengers’ onboard spending. With that in mind, management shared in the Q4 earnings call that they expect pricing to increase by low to mid single digits in 2024, 2025, and 2026. Meanwhile, the company’s ticket revenue per passenger was as follows in the previous 3 years.

|

Year |

Passengers |

Ticket Revenue |

Ticket Rev/Passenger |

|

2021 |

1,220,000 |

$1,000,000,000 |

$819.67 |

|

2022 |

7,730,000 |

$7,022,000,000 |

$908.41 |

|

2023 |

12,460,000 |

$14,067,000,000 |

$1,128.97 |

Assuming 3% growth in ticket revenue per passenger at the midpoint of management’s forecast, I’m projecting Carnival’s ticket revenues in 2024 to be $16.7 billion, representing 19% YoY growth.

|

Year |

Passengers |

Ticket Revenue |

Ticket Rev/Passenger |

|

2021 |

1,220,000 |

$1,000,000,000 |

$819.67 |

|

2022 |

7,730,000 |

$7,022,000,000 |

$908.41 |

|

2023 |

12,460,000 |

$14,067,000,000 |

$1,128.97 |

|

2024 |

14,400,000 |

$16,744,923,274 |

$1,162.84 |

As for onboard revenue, the average onboard spending by a cruise passenger is estimated to be $680. Given my projection for Carnival’s passengers this year, my onboard revenue estimate is $9.7 billion, representing 30% YoY growth.

|

Year |

Passengers |

Onboard Revenue |

Onboard Rev/Passenger |

|

2017 |

12,100,000 |

$4,566,000,000 |

$377.36 |

|

2018 |

12,410,000 |

$4,951,000,000 |

$398.95 |

|

2019 |

12,870,000 |

$6,721,000,000 |

$522.22 |

|

2021 |

1,220,000 |

$908,000,000 |

$744.26 |

|

2022 |

7,730,000 |

$5,147,000,000 |

$665.85 |

|

2023 |

12,460,000 |

$7,526,000,000 |

$604.01 |

|

2024 |

14,400,000 |

$9,792,000,000 |

$680.00 |

Based on this, I expect Carnival’s total revenue to increase 23% this year to $26.5 billion.

Turning to costs, it should be noted that management projects cruise costs without fuel per available lower berth per day (ALBD) to increase 4.5% due to a 4.5% increase in ALBD, per the Q4 earnings call. Management also expects fuel consumption per berth day to decrease 4% in 2024. Based on these figures, my projections for Carnival’s cruise costs are as follows.

|

Year |

ALBD |

Cruise Costs Excl. Fuel |

Cost Excl. Fuel/ALBD |

Fuel |

Fuel/ALBD |

Total Cruise Costs |

|

2022 |

72.5 |

$9,600,000,000 |

$132,413,793 |

$2,157,000,000 |

$29,751,724 |

$11,757,000,000 |

|

2023 |

91.3 |

$12,270,000,000 |

$134,392,114 |

$2,047,000,000 |

$22,420,591 |

$14,317,000,000 |

|

2024 |

95.4 |

$13,399,146,750 |

$140,439,759 |

$2,053,550,400 |

$21,523,768 |

$15,452,697,150 |

Moving on to non-cruise operating costs, Carnival recognizes selling and administrative costs as well as Depreciation. Regarding selling and administrative costs, management shared in the Q4 earnings call that they plan to maintain a similar level of advertising on a unit basis in 2024 compared to 2023. Considering that advertising costs are included in the selling and administrative costs, my projection for this cost is as follows.

|

Year |

Passengers |

Selling & Admin |

Selling & Admin/Passenger |

|

2022 |

7,730,000 |

$2,515,000,000 |

$325.36 |

|

2023 |

12,460,000 |

$2,950,000,000 |

$236.76 |

|

2024 |

14,400,000 |

$3,409,309,791 |

$236.76 |

Meanwhile, I expect depreciation expense to amount to $2.3 billion based on the average cost Carnival incurred in 2022 and 2023.

|

Year |

Depreciation |

|

2022 |

$2,275,000,000 |

|

2023 |

$2,370,000,000 |

|

2024 |

$2,322,500,000 |

This leaves non-operating expenses and tax expenses to be forecasted. In the Q4 earnings call, management shared that interest expenses are set to increase by $94 million. As a result, I’m projecting Carnival’s non-operating costs to be $2.1 billion in 2024. As for tax expenses, I expect it to be similar to 2023 at $13 million. As such, my projection for Carnival’s EPS in 2024 is as follows.

|

Revenue |

$26,536,923,274 |

|

Cruise Costs Excl. Fuel |

$13,399,146,750 |

|

Fuel |

$2,053,550,400 |

|

Cruise Costs |

$15,452,697,150 |

|

Selling & Admin |

$3,409,309,791 |

|

Depreciation |

$2,322,500,000 |

|

Operating Income |

$5,352,416,333 |

|

Non Operating Costs |

$2,112,000,000 |

|

Income Tax |

$13,000,000 |

|

Net Income |

$3,227,416,333 |

|

OS |

1,119,445,529 |

|

EPS |

$2.88 |

Considering management’s forecast of $1.2 billion in net income, per the Q4 earnings call, my projection would be 169% higher than the forecast.

Valuation

According to my estimates, I expect Carnival to post an EBITDA of $7.6 billion, higher than management’s forecast of $5.6 billion.

|

Revenue |

$26,536,923,274 |

|

Cruise Costs Excl. Fuel |

$13,399,146,750 |

|

Fuel |

$2,053,550,400 |

|

Cruise Costs |

$15,452,697,150 |

|

Selling & Admin |

$3,409,309,791 |

|

EBITDA |

$7,674,916,333 |

This means that Carnival is trading at a 6.48 EV/EBITDA ratio relative to my projected EBITDA, lower than the industry average of 9.55. As is, Royal Caribbean is trading at a 9.88 forward EV/EBITDA and Norwegian is trading at a 10.12 forward EV/EBITDA.

In light of this, I believe Carnival is undervalued at its current market cap of $18.2 billion and have a price target of $23.95 per share based on the industry average EV/EBITDA ratio, representing 47% upside from current levels.

Technical Analysis

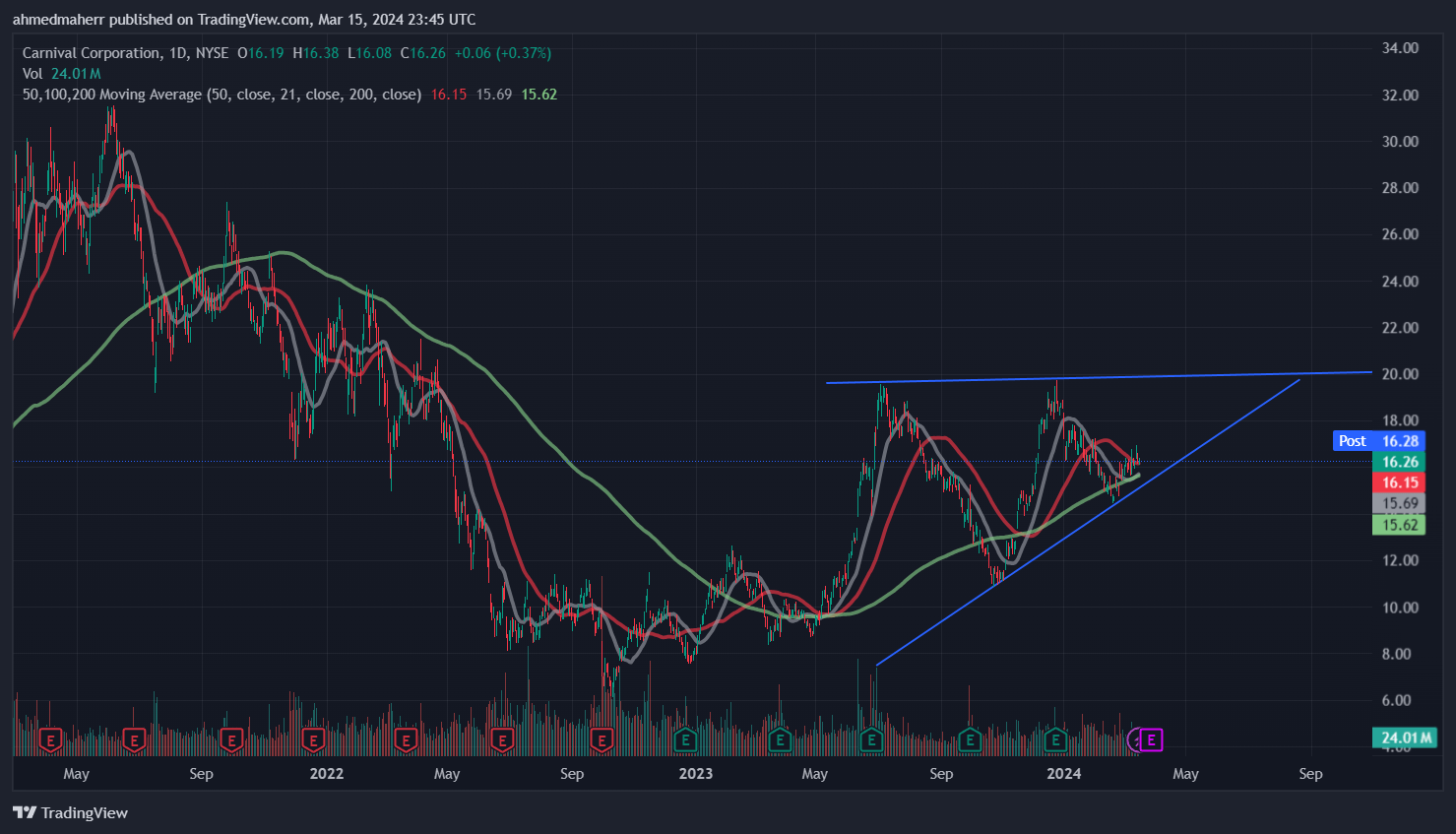

In my opinion, Carnival’s daily chart further proves my conviction. Currently, the stock is in an ascending triangle pattern which is a continuation pattern. At the same time, the stock is testing the 50 MA which is a key support level. Considering that Carnival will share its Q1 earnings on March 27, I expect the stock to test the upper trendline on a strong guidance which is why I believe the current share price is an ideal entry point.

TradingView

Risks

There are 2 risks to my bullish thesis on Carnival. The first risk is fuel costs which represent a significant expense to cruise lines. As such, any spike in fuel costs could have a negative impact on Carnival’s bottom line. Another risk to consider is geopolitical tensions, especially in the Middle East. Carnival already has an issue in the region as it already rerouted 12 cruise ships to avoid the Red Sea due to Yemeni cells targeting ships in Bab-el-Mandeb strait stemming from the ongoing Israel-Hamas conflict. As such rerouting these cruises around Africa would mean that Carnival could be without revenues from up to 6 weeks in some cases. With that in mind, the company previously shared that the rerouting could impact its full-year adjusted EPS by $.07 to $.08.

Conclusion

With the cruise line industry expected to resume its growth after a halt due to the pandemic, I believe Carnival is well-positioned to post a strong year revenue and earnings wise due to its leading market share in the industry. As is, I expect the company to post a net profit of $3.2 billion, 169% higher than management’s forecast. Given that I project Carnival to post an EBITDA of $7.6 billion, my price target for the stock is $23.59 per share, representing 47% upside from current levels, which is why I’m rating Carnival as a buy.

Q2 2024 Earnings Call Transcript")