Growing coin stacks representing compounding. pong-photo9/iStock via Getty Images

Finding out that an investment holding is going to send me more cash than I anticipated is one of many things that I love about dividend growth investing. When this happens, it’s a thing of beauty.

For more mature businesses, this is a sign that management is confident in the future of their company. They are retaining more than enough cash flow to invest in appropriate opportunities to further grow the business.

It also leaves me with more cash to selectively add to my investment holdings. And when is buying more stocks ever a bad thing given that I’m in the accumulation phase of my wealth building journey?

These reasons are why I was so pumped up to learn that Coca-Cola (NYSE:KO) announced a 5.4% raise in its quarterly dividend per share from $0.46 to $0.485. After the last two raises of $0.02 quarterly and three raises of $0.01 quarterly, Coca-Cola appears willing and able to return more value to shareholders.

Since I last covered the stock with a buy rating in November, it reported a strong fourth quarter to close out 2023. Today, I will take another look at Coca-Cola’s fundamentals and valuation to articulate why I’m reaffirming my buy rating for now.

Dividend Kings Zen Research Terminal

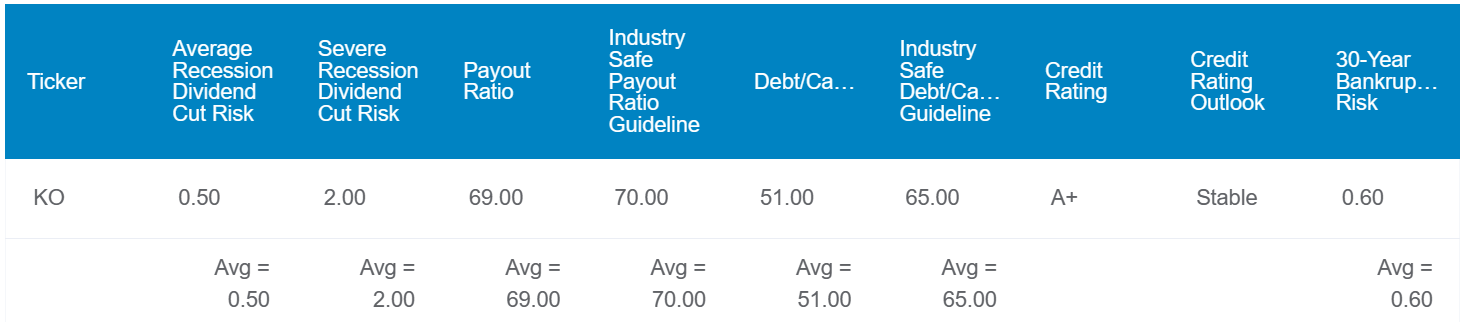

Coca-Cola’s 3.2% forward dividend yield is above the consumer staple sector median of 2.7% per Seeking Alpha’s Quant System. That’s enough to earn it a B grade on forward dividend yield. Thanks to the company’s 62 consecutive years of dividend growth, Seeking Alpha’s Quant System awards an A+ grade for dividend consistency.

In the years to come, there is also reason to believe dividend growth can keep up. Coca-Cola’s EPS payout ratio registers at 69%, which is just below the rating agencies industry-safe preference of 70% or better.

The beverage giant’s balance sheet is also rock-solid. Coca-Cola’s 51% debt-to-capital ratio is well under the 65% debt-to-capital ratio that rating agencies desire from the industry.

The company’s leadership within the global ready to drink beverage industry combined with these financial metrics are why S&P rates its debt A+ on a stable outlook. That puts the odds of Coca-Cola defaulting on debt in the next 30 years at just 0.6%.

All of these elements also explain the 0.5% likelihood of a dividend cut from the company in the next average recession. Even in the next severe recession, there is a 2% chance of a dividend cut. Put into perspective, each of these respective risks are the lowest possible for the Zen Research Terminal.

Dividend Kings Zen Research Terminal

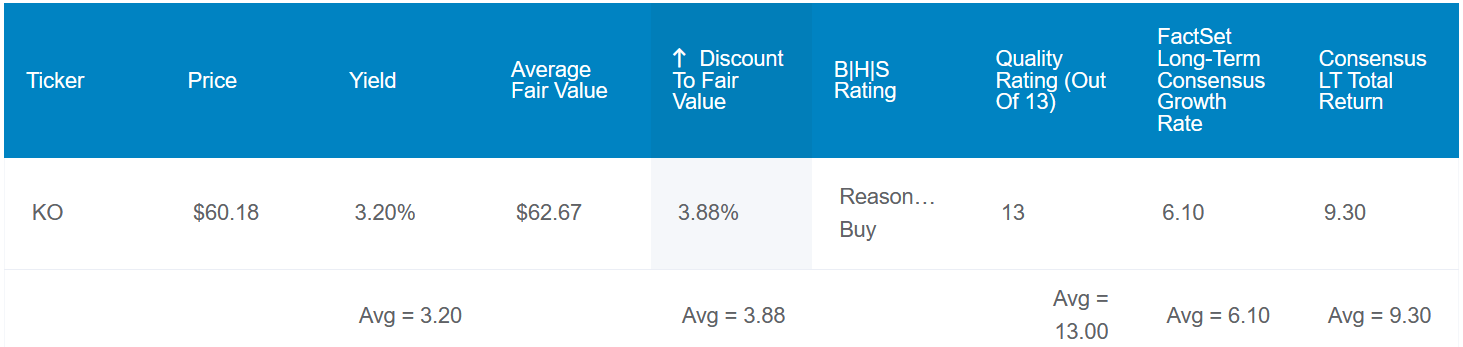

After gaining 5% in the last four months, Coca-Cola’s valuation appears to still be reasonable. The company’s 13-year average dividend yield of 3% according to the Automated Investment Decision Score Tool implies that shares are worth $64 each.

What’s more, Coca-Cola’s 13-year average P/E ratio of 22.6 suggests that shares are worth $61 apiece. Reversion to these fair values is arguably a reasonable assumption. That’s because, as I’ll discuss, the company’s growth story remains as intact as it has been in the last decade or so. This justifies a reversion to the mean from my perspective.

Finally, the following inputs into the discounted cash flows model demonstrate shares to be fairly valued at $62 each: $2.69 in comparable (non-GAAP) EPS in the last four quarters, a 6.25% five-year annual growth rate assumption, a 5.25% annual growth rate projection thereafter, and a 10% discount rate.

Adding these fair values together, I get a fair value of $62 apiece. Relative to the $60 share price (as of March 15, 2024), this would mean Coca-Cola’s shares are 4% undervalued.

If shares return to fair value and the company grows as anticipated, these are the total returns that it could generate over the next 10 years:

- 3.2% yield + 6.1% FactSet Research annual growth consensus + a 0.4% annual valuation multiple upside = 9.7% annual total return potential or a 152% 10-year cumulative total return versus the 10% annual total return potential of the S&P or a 159% 10-year cumulative total return

The Operating Fundamentals Remain Sound

Coca-Cola Q4 2023 Earnings Press Release

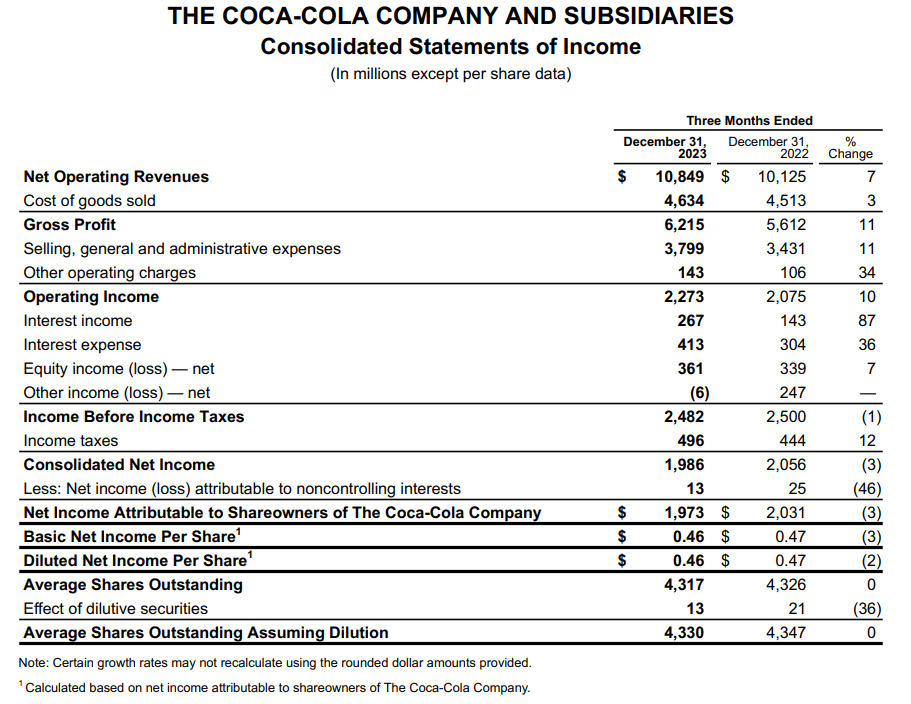

When Coca-Cola shared its financial results for the fourth quarter on Feb. 13, it was clear that the company’s fundamentals aren’t losing their kick. On the contrary, Coca-Cola’s fundamentals are becoming stronger.

The company’s net revenue surged 7.2% year-over-year to $10.8 billion during the fourth quarter. For context, that was $150 million ahead of the analyst consensus according to Seeking Alpha. What was behind the mega-cap company’s respectable topline growth in the quarter?

Just as I noted in my previous article, Coca-Cola’s exceptional brands were instrumental to its net revenue beat for the fourth quarter. The company’s 200+ brands sold in over 200 countries and territories have become a part of so many consumers’ daily routines. According to page 4 of 309 of Coca-Cola’s 10-K filing, the company’s brand portfolio accounted for 2.2 billion servings of beverages consumed around the world daily.

One of the biggest benefits of billions of people consuming these products on a regular basis is the pricing power that it affords the company. That’s because many people view these products as simple pleasures which they can enjoy.

Coca-Cola’s pricing actions and a more favorable sales mix contributed to a 9% tailwind during the fourth quarter. For the reason that I noted above, demand for these products remained steady. That is why concentrate sales to bottlers grew by 3% in the quarter.

These two headwinds were partially countered by two lesser headwinds. First, foreign currencies were weaker against the U.S. dollar into which Coca-Cola converts its net revenue. That weighed on net revenue to the tune of 4% for the fourth quarter. Secondly, the company had divestitures that negatively impacted net revenue. Coca-Cola refranchised its bottling operations in Cambodia in November 2022 and Vietnam in January 2023. In the short-term, these moves were a 1% drag on net revenue during the quarter.

Moving down to the bottom line, Coca-Cola’s comparable (non-GAAP) EPS climbed 10.4% over the year-ago period to $0.49 in the fourth quarter. That was in sync with the analyst consensus per Seeking Alpha. Disciplined management of cost of goods sold, its largest expense item, helped non-GAAP net profit margin expand by 50 basis points to 19.6% for the quarter. Along with a 0.4% reduction in the company’s diluted share count, that is how comparable EPS growth outpaced net revenue growth during the quarter.

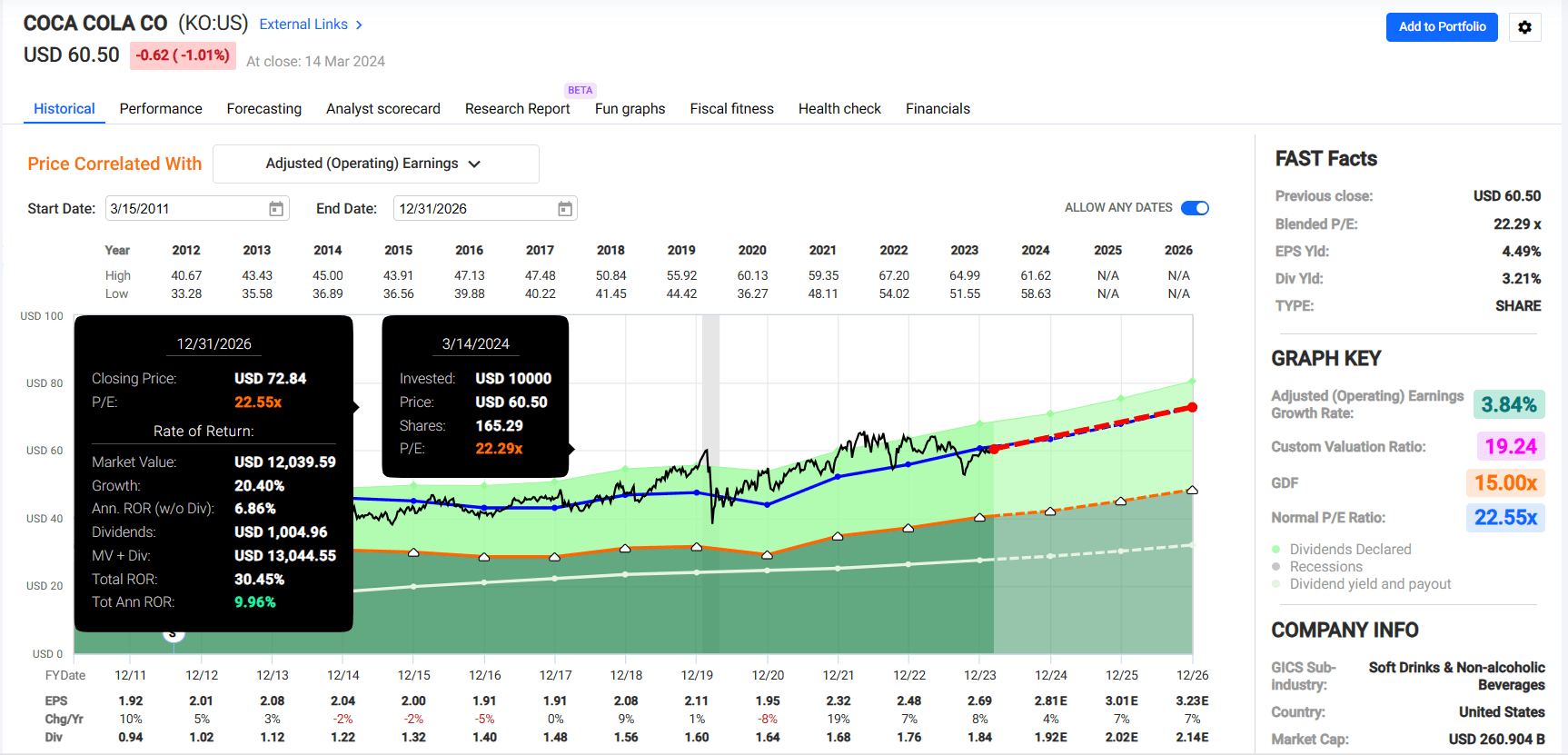

Looking out over the next few years, comparable EPS growth should come in at a mid- to high-single-digit clip annually. The FAST Graphs analyst consensus is for 4.5% growth over the 2023 comparable EPS base of $2.69 to $2.81 in 2024, 7.1% growth to $3.01 in 2025, and 7.3% growth to $3.23 in 2026.

This is based on the assumption that higher pricing should continue in the years ahead. That can be supported by the affordability of Coca-Cola’s products as a guilty pleasure of its customers. Going back to the 2.2 billion servings of Coca-Cola’s beverages that I mentioned were consumed daily in 2023, that’s a fraction of the estimated 64 billion total worldwide per the 10-K filing.

Product innovation should help capture even more of the overall market over time. Chairman and CEO James Quincey noted in his opening remarks during the Q4 2023 Earnings Call the company launched Sprite and Fanta reformulations in 25 markets. That delivered mid-single digit volume growth in those markets and was a catalyst for value share gains in the sparkling flavors market. In Japan, Quincey shared that the company also relaunched its Georgia Coffee brand. This also led to value share gains.

Coca-Cola’s financial health also remained great in 2023. The company’s net debt (cash, cash equivalents and short-term investments minus current maturities of long-term debt and long-term debt) was $25.1 billion during the year. Against the $15.6 billion in EBITDA that Coca-Cola produced for the year, that’s a net leverage ratio of 1.6. This shows that the company’s use of debt is within reason and the debt load is manageable (unless otherwise noted or hyperlinked, all details were sourced from Coca-Cola’s Q4 2023 Earnings Press Release).

Room For More Mid-Single-Digit Dividend Growth

Coca-Cola’s operating results and balance sheet indicate the fundamentals are appealing. Adding to the reasons to like the company, the dividend growth ahead could be decent.

Coca-Cola posted $9.8 billion in free cash flow in 2023. Compared to the nearly $8 billion in dividends paid out over that time, this is an 81% free cash flow payout ratio (info according to Coca-Cola’s Q4 2023 Earnings Press Release).

The company’s free cash flow was up a bit from the $9.6 billion in the prior year. That was even despite an additional ~$400 million in capex versus the year-ago period that is being allocated to digital bottling system investments. As these investments pay off, free cash flow growth could pick up to support further dividend growth.

Risks To Consider

Coca-Cola is a top-notch business, but there are risks to the investment thesis worth highlighting.

As I outlined in my previous article, the company’s business is weighted more toward away-from-home consumption avenues than PepsiCo (PEP). In economic recessions or pandemics (when most people are staying at home more often than usual), that could hurt Coca-Cola’s results.

The company’s business is also highly reliant on a smoothly running supply chain to keep operations running optimally. If these supply chains are disrupted, Coca-Cola’s results could suffer. That could harm the company’s operating results.

A final risk to Coca-Cola is the potential that it can’t adapt to shifting consumer taste preferences. If this happened, competitors could steal market share away from the company. That could negatively impact Coca-Cola’s growth prospects.

Summary: A Dividend King With Market-Matching Long-Term Return Potential

FAST Graphs, FactSet

I find Coca-Cola’s operating fundamentals, growth runway, balance sheet, and sustainable dividend to be sweet for my tastes as an investor. The valuation seals the deal for me to keep my buy rating. Shares are priced at a 22.3 blended P/E ratio, which is just below the 13-year normal P/E ratio of 22.6. If Coca-Cola matches the growth consensus through 2026 and reverts to its mean valuation, it could be positioned to generate 30% cumulative total returns through 2026.

Q2 2024 Earnings Call Transcript")